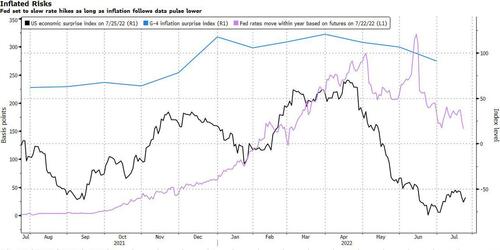

By Garfield Reynolds, Bloomberg Markets Live commentator and reporter

Risk Assets Are Hoping July Will Be Last Jumbo Fed Hike

The way yields and equities are dropping underscores the message from investors to the Fed: “You better slow down!”

The recession drumbeats grew louder after last week’s slump in US activity gauges and with rates traders pricing for the Fed rate to peak some time between November and February at about 3.3%. That’s going to make it very hard for the central bank to do anything but ease back, unless it wants to create real panic across markets.

The inflation-recession conundrum remains for the Fed, however, so such “tough love” can’t be ruled out. There’s been a strong undercurrent in Fedspeak and commentary from former Fed officials that the central bank has to be willing to risk recession to tame inflation if that’s what is needed.

Inflation data across major economies have cooled off a bit, relative to expectations, but the Fed may be reluctant to do much more than slow down to a 50bps/meeting-pace unless CPI readings suffer the sort of collapse seen across the rest of the economic indicators. After rates traders were well ahead of the Fed’s curve at the start of this cycle, that dynamic is close to flipping.

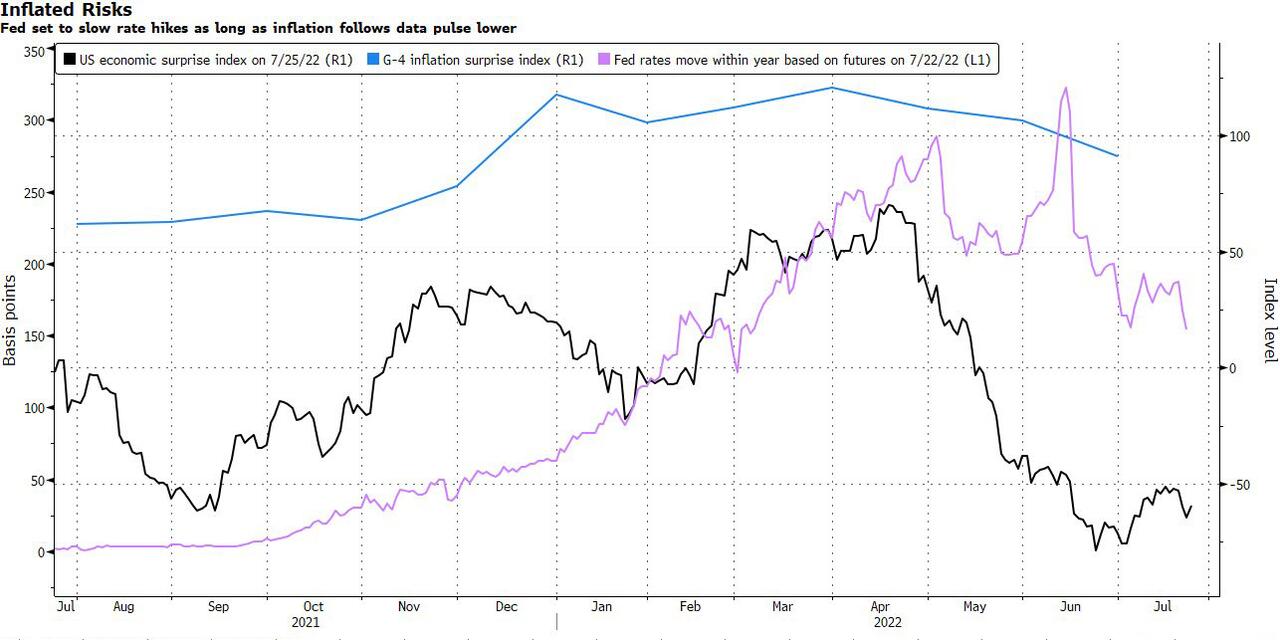

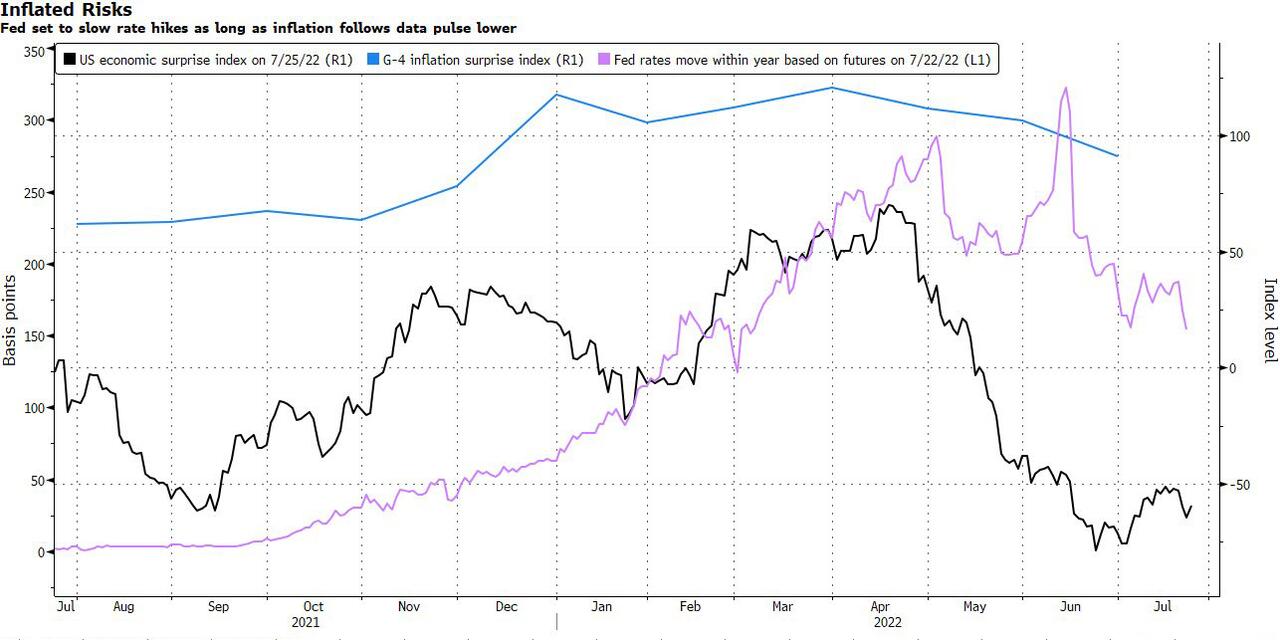

By Garfield Reynolds, Bloomberg Markets Live commentator and reporter

Risk Assets Are Hoping July Will Be Last Jumbo Fed Hike

The way yields and equities are dropping underscores the message from investors to the Fed: “You better slow down!”

The recession drumbeats grew louder after last week’s slump in US activity gauges and with rates traders pricing for the Fed rate to peak some time between November and February at about 3.3%. That’s going to make it very hard for the central bank to do anything but ease back, unless it wants to create real panic across markets.

The inflation-recession conundrum remains for the Fed, however, so such “tough love” can’t be ruled out. There’s been a strong undercurrent in Fedspeak and commentary from former Fed officials that the central bank has to be willing to risk recession to tame inflation if that’s what is needed.

Inflation data across major economies have cooled off a bit, relative to expectations, but the Fed may be reluctant to do much more than slow down to a 50bps/meeting-pace unless CPI readings suffer the sort of collapse seen across the rest of the economic indicators. After rates traders were well ahead of the Fed’s curve at the start of this cycle, that dynamic is close to flipping.