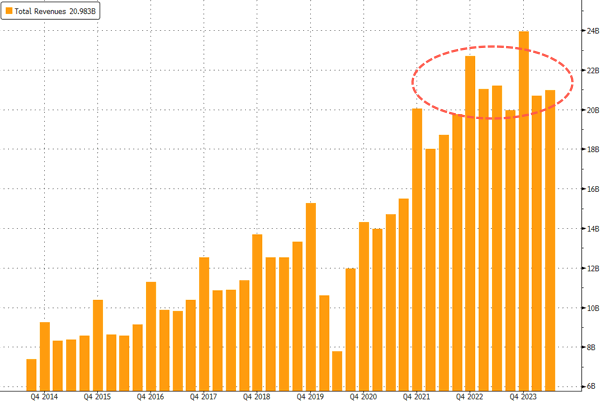

The world's largest luxury goods company reported third-quarter organic sales that missed the average analyst expectations tracked by Bloomberg. This signals a broader slowdown across luxury markets in China and the West. The results raise concerns about cost-conscious consumers as central banks reverse interest rate hiking cycles with interest rate cuts to prevent a hard economic landing in the global economy.

Paris-based LVMH Moët Hennessy Louis Vuitton, commonly known as LVMH, unexpectedly reported lower sales in the third quarter, primarily due to the pullback in Chinese luxury demand. It reported organic revenue of -3%, missing the Bloomberg Consensus of +.39%. Each division, from fashion to perfumes to watches to fine wine, missed analyst expectations. It reported revenue of 19.94 billion euros, which missed the 20.05 billion euro estimate.

Here's a snapshot of LVMH's third-quarter earnings (courtesy of Bloomberg):

-

Organic revenue -3%, estimate +0.93% (Bloomberg Consensus)

-

Fashion & Leather Goods organic sales -5%, estimate +0.48%

-

Wines & Spirits organic sales -7%, estimate -2.41%

-

Perfumes & Cosmetics organic sales +3%, estimate +4.26%

-

Watches & Jewelry organic sales -4%, estimate -3.71%

-

Selective Retailing organic sales +2%, estimate +5.09%

-

Revenue EU19.08 billion, -4.4% y/y, estimate EU20.05 billion

-

Fashion & Leather Goods revenue EU9.15 billion, -6.1% y/y, estimate EU9.74 billion

-

Wines & Spirits revenue EU1.39 billion, -8.2% y/y, estimate EU1.47 billion

-

Perfume & Cosmetics revenue EU2.01 billion, +1% y/y, estimate EU2.07 billion

-

Watches & Jewelry revenue EU2.39 billion, -5.5% y/y, estimate EU2.43 billion

LVMH's outlook was a dismal one that only suggests consumers in its top markets remain under pressure through year-end:

In an uncertain economic and geopolitical environment, the Group remains confident and will maintain a strategy focused on continuously enhancing the desirability of its brands, drawing on the authenticity and quality of its products, excellence in distribution and agile organization.

After the earnings report, RBC Capital Markets analyst Piral Dadhania told clients that results "indicate a more pronounced slowdown than expected."

The pandemic-era spending boom that drove luxury sales has run out of steam around the world. In the US, low/mid-tier consumers are cost-conscious and heavily indebted with depleted savings. The luxury behemoth is considered a bellwether for the entire sector.

In markets, LVMH ADRs dropped 6% late in the session, just 50bps from entering a bear market for the year.

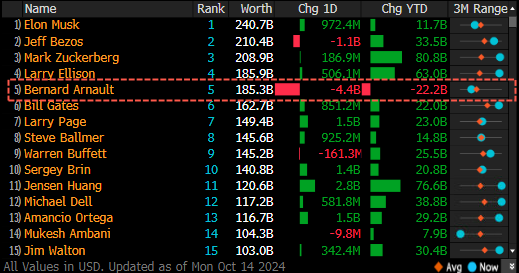

As LVMH shares decline, Bernard Arnault's luxury empire takes a hit, reducing his net worth by billions of dollars (according to Bloomberg data):

Rivals Ralph Lauren Corp., Estee Lauder Cos, and the ADRs of Gucci owner Kering SA also fell in New York as growing concerns mounted among traders that consumers were losing momentum.

Update (0658ET)

LVMH shares in Paris tumbled as much as 7.5% on Wednseday – the lowest level in over two years. The world’s largest luxury goods company missed estimates for third-quarter organic sales amid a worsening slowdown in China.

A team of Goldman analysts led by Louise Singlehurst provided clients with a breakdown of the third-quarter earnings report:

LVMH reported 3Q24 sales with -3% cFX growth, below expectations. LVMH delivered organic sales growth of -3% cFX yoy in 3Q, below both Visible Alpha Consensus Data (+1%) and GSE (+0%). The largest division, Fashion and Leather, decreased -5% cFX (below expectations of +1%, GSE 0%) demonstrating the deceleration in spending from the Chinese cluster. Price mix remains close to flat and the underperformance largely reflects negative volumes. The Wines & Spirits division was -7% cFX, below cons -2% and GSE -5%, demonstrating weak demand despite Hennessy growing in the US as inventory across wholesale partners continues to normalise. The Watches and Jewellery division reported -4% cFX growth vs cons at -3% in line with last quarter.

Singlehurst continued:

LVMH delivered a disappointing sales performance despite expectations that had lowered ahead of the report, given concerns of a sequentially weakening Chinese consumer (vs Q224). We expect LVMH’s confirmation of a tough trading environment sets the scene for the upcoming Q324 updates from the luxury peers. As we have discussed (Sept 20), we see a challenging backdrop for luxury consumption and expect a difficult six months ahead. We update our forecasts for the 3Q24 release and now look for -0.5% cFX sales growth for the group in FY24 (from +1%). Overall our DCF derived 12m price target falls by c.6% to €770 (was €815). We remain Buy rated as we continue to prefer brands such as those in the LVMH group given scale benefits and ability for greater cost control.

Despite the slowdown in China, the analysts see improvement trends across the West:

(i) Chinese consumer cluster turned negative in F&L in Q324, weakening sequentially: Management highlighted a deterioration in the performance of the Chinese cluster (spending at home and abroad). In context, within F&L this reflects a slowdown from mid to high-single digit positive growth in Q224 to mid-single digit negative in Q324. We also note that the group performance in APAC (ex Japan) decelerated to -16% yoy (from -14%). While too early to have a complete picture of the Golden holiday period in China (Monday 1-7th October), management commented that they have not seen any material change in trends compared to Q3. Management also highlighted that Chinese spending was still 40-45% offshore vs 30-35% a year ago but changing tourism patterns particularly given ongoing FX headwinds have seen Japan decelerating from +57% cFX yoy in 2Q24 to +20% cFX yoy, which was broadly in line with our expectations (+22% cFX). While Japan remains positive for now, in our estimates (see 10th October) Japan is likely to turn negative for the industry in 2025 given slowing tourism spend and a high base of comparison.

(ii) Modest improvement in trends in both US and Europe: LVMH reported +2% cFX in Europe and +0% cFX in the US with management highlighting flat to slightly improving American (although still negative) and European clusters in the Q324 period. Overall, we expect broader macro pressures coupled with a normalisation in post Covid consumer spending to weigh on performance, while we expect the high-end is relatively more resilient.

(iii) Focus on cost control ahead of FY results: Management had lowered expenses in 1H24, particularly A&P spend, to navigate the more modest top-line environment. Looking forward, while we expect overall continued controls on opex spend, management reiterated its focus on investments into distribution, communication and product design although noting some potential deceleration in spending to protect margins. Management also commented on working capital headwinds given slightly higher inventories.

They remain ‘Buy’- rated on LVMH with a 12-month price target of 770 euros. That’s about a 28% upside from current levels of 600 euros.

Valuation – Remain Buy; 12-month PT €770 (from €815). We continue to use a DCF valuation methodology for LVMH (8.5% WACC, 3.0% LT growth; unchanged). Our price target decreases c.6% in line with the decline in our long-term earnings and FCF forecasts. As we have previously discussed (Sept 20), we see a challenging backdrop for luxury and we expect a difficult six months ahead. In this context, we continue to prefer brands such as those in the LVMH group given scale benefits and ability for greater cost control. On our estimates, LVMH trades on 15x adjusted EV/EBIT and 22x adjusted P/E in 2025E. This compares to the LVMH’s 10-yr average P/E of 21x (we exclude Covid (April 20-Oct 21).

Analysts from other research desks told clients that LVMH’s ER update offers a “clear negative” for the industry, plus more confirmation of waning consumers:

Telsey Advisory Group (outperform, cuts PT to €750 from €800)

- While slowing luxury demand, especially from China, does not come as a surprise, LVMH’s 3% organic sales decline is still disappointing, says analyst Dana Telsey in a note

- This update adds to the global growth concerns across the international luxury group, and investors will be looking for signs of benefits from government stimulus efforts in the fourth quarter and beyond

Jefferies (hold, PT cut to €560 from €600)

- LVMH’s update confirms a tough industry backdrop in recent months, writes analyst James Grzinic in a note, adding that recent Chinese stimulus measures are unlikely to have turned the tide

Deutsche Bank (hold, PT cut to €670 from €750)

- The view of the industry remains that this is a consumer confidence-led cyclical downturn that will rebound, says analyst Adam Cochrane, though the question remains one of timing

Bryan Garnier (buy, PT cut to €800 from €835)

- LVMH’s third-quarter sales were poor, says analyst Loic Morvan, and confirm the current deterioration in the luxury industry, especially in Mainland China

Stifel (buy)

- Main factor behind the miss in fashion & leather goods was a substantial sequential deterioration for the Chinese cluster, says analyst Rogerio Fujimori in a note

- For long-term investors, expects the American cohort to improve next year and the Chinese cluster close to bottoming out

Morgan Stanley (equal-weight

- Analyst Edouard Aubin writes that the 5% organic sales decline in the fashion & leather goods (F&LG) segment is the “key sentiment driver” of the stock and came in “well below” investor expectations

- Says that excluding 2020, this is the first-time that F&LG has posted a quarterly decline since 2009

- 3Q exit rate was probably “weak”

- “While the market expectations for LVMH results had tempered in recent weeks, we believe that tonight’s results will nevertheless be taken negatively by the market,” he says

Citi (buy)

- “Clear negative for the industry ahead of the 3Q reporting season and in the run-up to key Christmas and Chinese New Year trading periods,” analyst Thomas Chauvet writes

- Says there’s “limited incremental visibility” on 4Q and first- half 2025 demand

RBC Capital Markets (outperform)

- Result will be viewed negatively by the market, and “indicates a more pronounced slowdown than expected,” analyst Piral Dadhania writes in a note

- Flags that all divisions missed consensus expectations

Bernstein (outperform)

- LVMH “badly misses” on third-quarter expectations, analyst Luca Solca says, which confirms the notion that the company is “suffering issues of its own” on top of a difficult market environment

- Notes that there were misses “across the board”

The company warned about an uncertain economic and geopolitical backdrop through year-end.

* * *

The world’s largest luxury goods company reported third-quarter organic sales that missed the average analyst expectations tracked by Bloomberg. This signals a broader slowdown across luxury markets in China and the West. The results raise concerns about cost-conscious consumers as central banks reverse interest rate hiking cycles with interest rate cuts to prevent a hard economic landing in the global economy.

Paris-based LVMH Moët Hennessy Louis Vuitton, commonly known as LVMH, unexpectedly reported lower sales in the third quarter, primarily due to the pullback in Chinese luxury demand. It reported organic revenue of -3%, missing the Bloomberg Consensus of +.39%. Each division, from fashion to perfumes to watches to fine wine, missed analyst expectations. It reported revenue of 19.94 billion euros, which missed the 20.05 billion euro estimate.

Here’s a snapshot of LVMH’s third-quarter earnings (courtesy of Bloomberg):

-

Organic revenue -3%, estimate +0.93% (Bloomberg Consensus)

-

Fashion & Leather Goods organic sales -5%, estimate +0.48%

-

Wines & Spirits organic sales -7%, estimate -2.41%

-

Perfumes & Cosmetics organic sales +3%, estimate +4.26%

-

Watches & Jewelry organic sales -4%, estimate -3.71%

-

Selective Retailing organic sales +2%, estimate +5.09%

-

Revenue EU19.08 billion, -4.4% y/y, estimate EU20.05 billion

-

Fashion & Leather Goods revenue EU9.15 billion, -6.1% y/y, estimate EU9.74 billion

-

Wines & Spirits revenue EU1.39 billion, -8.2% y/y, estimate EU1.47 billion

-

Perfume & Cosmetics revenue EU2.01 billion, +1% y/y, estimate EU2.07 billion

-

Watches & Jewelry revenue EU2.39 billion, -5.5% y/y, estimate EU2.43 billion

LVMH’s outlook was a dismal one that only suggests consumers in its top markets remain under pressure through year-end:

In an uncertain economic and geopolitical environment, the Group remains confident and will maintain a strategy focused on continuously enhancing the desirability of its brands, drawing on the authenticity and quality of its products, excellence in distribution and agile organization.

After the earnings report, RBC Capital Markets analyst Piral Dadhania told clients that results “indicate a more pronounced slowdown than expected.”

The pandemic-era spending boom that drove luxury sales has run out of steam around the world. In the US, low/mid-tier consumers are cost-conscious and heavily indebted with depleted savings. The luxury behemoth is considered a bellwether for the entire sector.

In markets, LVMH ADRs dropped 6% late in the session, just 50bps from entering a bear market for the year.

As LVMH shares decline, Bernard Arnault’s luxury empire takes a hit, reducing his net worth by billions of dollars (according to Bloomberg data):

Rivals Ralph Lauren Corp., Estee Lauder Cos, and the ADRs of Gucci owner Kering SA also fell in New York as growing concerns mounted among traders that consumers were losing momentum.

Loading…