Authored by Alasdair Macleod via GoldMoney.com,

The consequences of Russia and her Asian allies embracing gold backing for their currencies are poorly understood in western capital markets. This move could lead to the destruction of the global fiat currency system.

According to evidence which is widely ignored in western capital markets, a move by Russia to put a new trade settlement currency and possibly the rouble as well onto a new gold standard is becoming a certainty. As a weapon of mass fiat currency destruction, the timing is probably bound up in on-the-ground military considerations, which are already showing signs of escalating in Eastern Ukraine.

As well as using gold to undermine the western currency system, a return to a credible gold standard has significant advantages for Russia and for her allies in the Shanghai Cooperation Organisation, the Eurasian Economic Union, BRICS+, and all their commodity suppliers beyond Asia. At the same time, it would destroy the west’s fiat currencies and financial system.

This article explains how one part of the global economy can thrive while the other collapses.

Introduction

Recently, I have written about the signals emanating from Russia that President Putin is minded to re-adopt sound money by returning to some sort of gold standard. We do not yet know the details, but consider what he said at the St Petersburg International Economic Forum in June last year:

“Caught in the inflationary storm, many nations are asking, why bother exchanging goods for dollars and euros when they are losing value right before our eyes? Indeed, the economy of imaginary wealth is being inevitably replaced by the economy of real valuables and hard assets.

“According to the IMF, today’s global foreign currency reserves contain 7.1 trillion dollars and 2.5 trillion euros. And this money is depreciating at an annual rate of about 8%. Moreover, it can be confiscated or stolen at the whim of the US if it disapproves of something in a country’s policy.

I think this has become a very real threat for many countries that keep their gold and foreign exchange reserves in these currencies. According to objective expert analysis, in the coming years a conversion process of global reserves will get under way. Reserves will be converted from weakening currencies into tangible resources like food, energy, commodities, and other raw materials. Clearly, this process will further fuel global dollar inflation.”

This message was delivered to 81 official delegations, and 14,000 delegates from a further 49 countries, including heads of state and government attending unofficially. Putin’s message was that central banks will be dumping dollars and euros and accumulating gold reserves instead — the only “tangible resources” they can own, not stored in western vaults where they can be impounded as has happened to Venezuela. And government agencies will stockpile essential commodities, raw materials, and food instead.

The statement on gold reserves was not so specific, but by disposing of dollars and euros, trade and foreign exchange liquidity is bound to swing in favour of gold. With central banks reported to have accumulated record quantities of bullion last year, they appear to agree with President Putin.

In effect, delegates at the St Petersburg Forum were put on notice that the dollar will be attacked by Putin’s mobilisation of foreign liquidation of currency reserves in favour of tangible commodities and gold. For many central banks, the logic of maintaining official currency reserves will no longer apply, while increasing physical gold holdings under their direct control is the new priority.

The timing of the dollar’s demise will in large part be set by Putin’s geopolitical timing, because he can almost certainly trigger foreign liquidation simply by passing the word.

Separately, Putin’s senior economic adviser, Sergey Glazyev, has been working officially on a new trade settlement currency for use between members of the Eurasia Economic Union (EAEU), with an ambition to extend the settlement facility to all members of the Shanghai Cooperation Organisation (SCO) and BRICS+ (a rapidly expanding club of nations including non-Asian nations) who wish to use it. These groupings represent well over half the world’s population.

From the few statements on his thinking, it has become clear that having considered the options Glazyev now favours a currency solution based on gold alone.

We should also note that the proposal for an expanded Moscow gold exchange is being headed up by Glazyev himself. And in a move which appears to front-run developments, Sber — Russia’s largest bank — announced the introduction of a gold-backed digital financial fund.

On 27 December, the same day that Sber announced its new digital gold fund, in an article entitled “Golden rouble 3.0: How Russia can change foreign trade infrastructure”[i] written for Vedomosti, a Moscow-based Russian business newspaper, Glazyev laid out his latest thoughts. It was co-authored by Dmitry Mityaev, who is Assistant Member of the Board for Integration and Macroeconomics of the Eurasian Economic Commission — so this article is not just Glazyev’s musings, and it can be assumed to carry official weight.

From this article, the EAEU currency commission now appears to have dropped earlier proposals for a new currency entirely, using gold instead as the principal means of settling trade imbalances. It is likely to wrapped up as a digital representation of physical gold. If it copies the Bretton Woods model, perhaps only participating central banks will be permitted to demand physical delivery, but the digital currency would be more widely available as credit for trade settlement.

Presumably, the requirement to be prepared to settle national payment imbalances in gold bullion could be then minimised if one or more national currencies went onto a credible gold standard either by linking their currencies to the new trade settlement currency in an Asian version of Bretton Woods, or by going onto individual gold standards. The implication is that the rouble, and probably China’s yuan might do just that to produce a seamless gold-linked pan-Asian settlement system.

Whatever the detail, this is not a step to be taken lightly. China is highly dependent on exports to America and NATO members. But she appears to be refocusing on Asia and has the personal savings available to back the necessary capital investment, which in some cases will offset her imported energy costs. Both Russia and the Saudis heading up OPEC+ will be fully aware of the impact on the fiat petrodollar regime of switching payments to yuan, roubles, or other Asian national currencies for their primary export product — crude oil. Reserves of western alliance fiat currencies not sold might have to be written off. Consequently, the Saudis and other Gulf energy exporters are sure to have sought assurances about the stability of yuan and possibly roubles relative to the dollar.

Therefore, we have three elements pointing to an emerging gold standard in Asia, and for the nations that are associated with it. Firstly, President Putin made it clear that he sees a transition to sound currency values based on commodities (i.e. represented by gold), away from the dollars and euros which can be weaponised by America and alliance nations in its sphere of influence. Secondly, Putin’s view is being echoed by his senior economic adviser, Sergey Glazyev, who is the central figure formulating trade settlement arrangements. And thirdly, it is impossible to imagine that Middle Eastern energy exporters would accept payment in currencies other than dollars unless they were given sufficient reassurances about their future payment values relative to the petrodollar.

Until last year, the Russian and Chinese long-term policy of doing away with dollars for pricing commodities, settling cross-border trade, and intermediating in virtually all foreign exchange transactions has been defensive, letting America make the geopolitical running. Sanctions against Russia changed all that. Backed into a corner, Putin has no option but to seek to destabilise the western financial system deliberately. He quickly moved to protect the rouble. Now he is taking the initiative, and as part of his effort to remove the American threat from Eastern Europe entirely his strategy is both military and financial.

Pricing Russian commodities

As the world’s largest exporter of energy as well as of a wide range of industrial commodities and raw materials, the Russian economy stands to benefit enormously from a shift in global currencies away from the fiat dollar and associated western currencies to the currencies whose economic backing is commodity related. And when we think of the Russian economy, we think primarily in terms of oil. There is a further relevance to energy because it is a topic Putin thoroughly understands, his post-graduate qualification being in energy economics. He has always had a firm grip on the global energy scene, including gas and nuclear, fully understanding the western alliance’s pressure points. And on the evidence, with his close advisers he also appears to have a better grasp of monetary theory than his opposite numbers in the western alliance.

It is in this context that we should view the price of oil and its history.

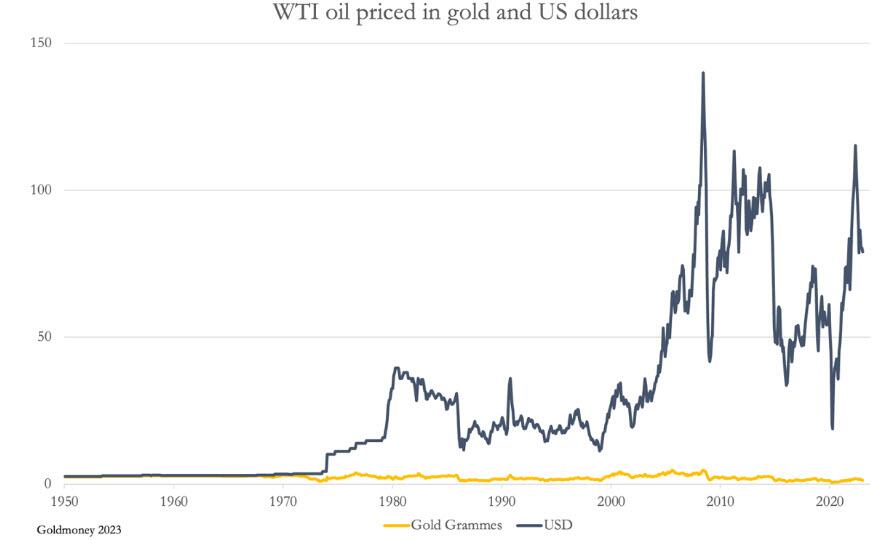

The chart above is instructive, particularly with respect to the price of oil in gold. In 1950, WTI benchmark oil was priced at $2.57, and with gold fixed at $35 to the ounce, the gold equivalent was 2.361 grammes to the barrel. The oil price increased to $3.56 (3.06 gold grammes) by the time the Bretton Woods agreement was suspended. Until then, priced in dollars the price had been remarkably stable, and some of that increase in the oil price before the end of the Bretton Woods agreement was understandable, because the dollar’s official value in gold began to be challenged in the markets before Bretton Woods was suspended in 1971.

The price stability between 1950 and 1971 (when Bretton Woods ceased) was remarkable. The expansion of credit, measured by M3 money supply between those dates was substantial, since 1960 more than doubling. According to the monetarists, the purchasing power of the dollar should have approximately halved. The plain fact that it didn’t is evidence that so long as a currency’s link with gold enjoys market credibility, it will not lose purchasing power due to credit expansion. What did give eventually was not prices, but an increasing run agaist US gold reserves which fell from a peak in 1949 of 21,828 tonnes to 9,070 tonnes by 1971.

Gold’s purchasing power enjoys unrivalled stability, which is why it has always been money throughout the ages. All evidence confirms this, illustrated in our next chart, which is of wholesale prices in the UK during the gold standard from 1817—1914.

Following the economic consequences of the Napoleonic Wars and when the new gold standard bedded in, over time price levels stabilised. As banking systems became increasingly refined following the 1844 Bank Charter Act and the Bank of England joining the London Clearing System in 1864, by this measure the general level of prices became increasingly constant.

To confirm gold’s price stability, we can go even further back to the time of Diocletian, who produced his edict of maximum prices in 301AD. The circumstances were that the purchasing power of the denarii coin was falling due to its debasement. From the edict, we find that a gramme of gold was fixed at 216 denarii, giving us a conversion value for goods listed in the edict for comparison with today. From this, we know that in today’s currency pork was about $4 a pound, sea fish about $8 a pound and a dozen eggs $3.32. Vin ordinaire was $2.96 for a 75cl bottle, and good quality wine $11.10 a bottle. Beer was $3 a litre. Clearly, prices for staples which we still consume were similar to today, irrefutable evidence that gold valued as money is stable even over thousands of years.

Following the ending of the Bretton Woods agreement, the price of oil in gold showed the same long-term relative stability at a time when it fluctuated wildly in dollars. Since 1971, measured in dollars WTI oil has been as high as $140 and even went negative due to problems emanating from futures markets in April, 2020. In gold grammes the range has been 4.88 and 0.35. There can be little doubt that price volatility in gold would have been considerably less if American attempts to demonetise gold, suppress its dollar price, and rig markets generally over the decades had not taken place. To see prices being considerably more volatile in dollars than in gold grammes following the end of Bretton Woods confirms the better means of pricing oil, and therefore the whole commodity complex, is in gold.

Bearing in mind that Russian economists were never exposed to Keynesian philosophy before the collapse of the Soviet Union, senior advisers such as Sergey Glazyev are almost certainly aware that gold remains money despite American propaganda that it has been superseded by the US dollar. Putin’s economic advisers had complained that the Bank of Russia’s policy of selling all mined gold into London before trade and financial sanctions were imposed showed that its senior management had been captured by the economic and monetary policies of western central bankers and did not represent their own views.

Putin will know that priced in gold, Russia’s commodity exports should have broadly retained their market value. Both Glazyev and Putin will also know that the gold price of oil today is 1.32 grammes per barrel, down 42% from the 1950 level of 2.36 grammes, and down 51% from 2.67 grammes price when the Bretton Woods agreement was suspended. Russia has lost badly from the west’s fiat currency regime.

There is a further issue in that the only significant sources of oil which require minimal energy to extract are in the Middle East and Siberia. Elsewhere, oil, particularly shale requires substantial energy input, fuelled by oil derivatives. It is in this context that we must view attempts by Russia in partnership with the Saudis and Iran to take command of global oil pricing.

According to British Petroleum’s 2022 statistical review, global crude oil supply in 2021 was 89,877,000 barrels daily, of which Russia and the Middle East combined was 41,985,000. Viewed this way, the strategic importance for both Russia and the Middle East to work together to control pricing becomes clear. Furthermore, with the advanced nations in the west bent on reducing fossil fuel dependency and therefore their own oil production hands further pricing power to Asian suppliers.

If Russia decides to push up global prices while continuing to offer oil at discounted prices to her allies, then the price in gold grammes becomes relevant, given the increasing evidence that gold will return to underpin trade and possibly national currencies in the SCO, the EAEU, and BRICS. As noted above, the gold gramme price when Bretton Woods was suspended was 2.67 grammes per barrel, today it is 1.42 grammes. At today’s gold to dollar exchange rate of $1840, that would be the equivalent of $150 per barrel.

The monetary consequences of Asian gold standards

We can assume that the consequences of the Asian hegemons backing their payment systems with gold will have been carefully considered by them, particularly by the Russians who have been forced into bringing forward a means of protecting their export revenues from weaponised dollars.

Besides bringing stability to export values there are other advantages to reintroducing gold into currency systems. Interest rate stability at lower rates is an obvious benefit. Currently, the Bank of Russia’s key interest rate is 7.5% and price inflation is estimated at 11.8%. The yield on Russia’s 10-year OFZ bond is 11%. If the rouble becomes a credible gold substitute, price inflation, interest rates, and bond yields can be expected to decline towards levels that reflect gold’s long-term stability. And assuming that credit expansion by Russia’s commercial banks is not excessive, there is no reason to expect otherwise than that financial stability for the currency and the Russian economy would continue in the long-term. Coupled with low taxes (Russia’s income tax is a flat 13%) this stability can be expected foster genuine economic progress and the accumulation of personal wealth for the Russian people.

Following the Napoleonic Wars, these are the conditions that led Britain to becoming the most powerful commercial entity in the world by the First World War. They will foster the industrial revolution planned by both Russia and China in partnership with the Eurasian continent’s members of the SCO and EAEU. The stability that gold gives to participating currencies is bound to attract other nations away from the US dollar-based fiat currency system to participate in this success. And as momentum for the new currency regime grows, Russia’s price inflation, interest rates and bond yields are bound to decline to zero, 2%, and 3% or 4% respectively.

However, a move towards gold backing for their currencies by the Asian hegemons can be expected to undermine the purchasing power of western fiat currencies. International capital will leave fiat currencies for commodities, with nations rebuilding stockpiles of energy, metals, and other raw materials. Precious metals, specifically gold, will be sought and its price can be expected to increase.

The consequences for commodity prices being measured in gold grammes or in gold currency substitutes will be to drive commodity prices measured in declining fiat currencies even higher. In the example given earlier in this article, which suggests that in today’s dollars the pre-Bretton Woods oil price would be the equivalent of $150 per barrel, this value is struck with gold at $1840. A rise in the gold price measured in declining fiat currency would easily take this oil price estimate to well over $200.

The consequences for wholesale and consumer prices in the western nations would rapidly become obvious, with central banks forced to revise their expectations for price inflation sharply higher, forced to adjust their interest rate policies accordingly. Bond yields can be expected to rise, undermining all financial and property values. As this negative outlook clarifies, measured against gold fiat currencies will likely enter a substantial relative decline.

The consequences of the emergence of gold backing for currencies in Asia on the currencies and economies of the western alliance are bound to differ in their detail. Briefly, the following difficulties for the major players are likely to emerge:

-

The reliance on inward foreign investment has protected the dollar from continual trade deficits and played a key role in funding US Government debt since the end of Bretton Woods. It has allowed the US Government to run budget deficits more or less continually. The accumulation of foreign capital as the counterpart of trade imbalances now appears to have slowed and will reverse if President Putin follows through on his warning at the St Petersburg Economic Forum, persuading attendees to actively sell dollars. The US Government will face significant funding hurdles against foreign liquidation of Treasuries. Bond yields and funding costs for the government are bound to rise to crisis levels. And the Fed’s own financial condition will become a further source of concern for foreign exchange markets. Furthermore, the commercial banks have balance sheet constraints, restricting their ability to create further credit under Basel III rules.

-

The consequences for the EU and the eurozone would be both politically and economically divisive. If it were not for political constraints, Germany would naturally drift towards cooperation with the sound money regimes emerging to her east, particularly as the finances of the Mediterranean club deteriorate, needing yet more support at the expense of Germany’s wealth. With falling bond prices, the entire euro system comprised of the ECB and its national central banks would need to be recapitalised, being already in negative equity. The eurozone’s global systemically important banks (G-SIBs) are extremely highly leveraged and unlikely to survive the combination of falling asset values and bad debts that would be the certain consequences of the euro’s declining purchasing power. Having been assembled at the behest of a political committee and now managed by a political cabal, the euro is at risk of losing all market credibility.

-

The consequences for the Japanese yen will also be harsh. The Japanese economy is highly dependent on imported commodities and raw materials. Higher prices in yen will feed through to yet higher prices through the value chain. Already, Japanese inflation is recorded at 4%. The CPI includes prices suppressed by government subsidies giving a cosmetic effect. The Bank of Japan has taken a losing bet on the inflation outlook, continuing to assume that it was transient long after other major central banks accepted that inflation was not going to subside so easily as they originally thought. Government bond yields up to two years maturity still have negative yields, illustrating the unreality of the BoJ’s three-wise-monkeys approach to price inflation and interest rate policy. For now, the BoJ is aggressively rigging the bond market to keep yields suppressed by buying enormous quantities of 10-year JGBs to cap their yield at 0.5%. One way or another, the ending of this policy is going to forced upon the BoJ and the shock to government finances will be tremendous. The government debt to GDP ratio stands at over 250%, and a rise in funding costs is likely to be catastrophic for the yen.

-

The consequences for the UK pound will also be significant. In a similar debt trap to that of the US Government, the British have the further disadvantage of an economy suppressed by increasing taxes. Furthermore, with London being the international financial centre built on fiat currencies, the UK will be at the epicentre of a fiat currency crisis. For the size of her economy, the UK has little in the way of gold reserves, hampering any future escape from the fiat currency trap.

Not only will the major governments aligned both economically and intellectually with the fiat dollar as their reserve currency be left with a comparative disadvantage by an Asia moving to sound money standards, but their economies are exposed to highly costly welfare commitments. Politically, it is proving impossible for them to respond to developments in Asia with cuts in public spending. Rising prices, which in reality represent declining purchasing power for fiat currencies, will require significantly higher interest rates to stop foreign selling in favour of strategic commodity and gold reserves.

A moment of fundamental choice is rapidly approaching: will central banks continue to suppress interest rates to save financial markets and support economic activity, or will they act to protect the currency and ignore the financial and economic consequences? The political imperative is clear, not least because of the consequences for government funding costs and liabilities. Furthermore, economists in governments and central banks would be reluctant to abandon their embedded economic and monetary policies by protecting their currencies because it would be an admission of failure.

Already, financial commentators are aware of the approaching dilemma, referring to it as a policy pivot. Conditioned to be inflationists, they are all warning of the dangers of higher interest rates, and owners of financial assets are banking on this so-called pivot taking place. But a pivot only delays the outcome by very little time because the consequences of a rapidly depreciating currency relative to commodity and other cost inputs will soon lead to economic activity being hampered, business plans rapidly becoming obsolete, and unemployment rising catastrophically. The Keynesian response of economic stimulation will simply not be available.

The only salvation will be for western governments to jettison Keynesian macroeconomics entirely and revert to classical economic theories. The false assumptions that have built up over the last hundred years will have to be overturned. Therefore, economists in central banks and government departments will not be intellectually equipped to provide solutions. Re-education against a background of economic crisis driven by collapsing fiat currencies will take some time; time that markets are unlikely to grant.

Crises of this sort nearly always emanate in the foreign exchanges because it is foreign holders of currencies who are the first to recognise a currency’s weakness. Usually, it involves a specific currency. But this time, it will affect all the major currencies in the western alliance. Furthermore, instead of a shift between fiat currencies, much of the crisis will reflect the wholesale selling of fiat currencies for commodities and gold. Additionally, the error the western alliance made in rendering their currencies worthless in Russian hands has tipped off all foreign holders of fiat currencies to their true value.

A sensible course for any non-aligned government would be to swap currency reserves for strategic reserves, the latter being comprised of commodities, raw materials, and foodstuffs. The pressure this switch would bring to bear on markets is not restricted to currencies but is a reversal of the conditions which have underpinned the growth of derivatives. The scramble to cover paper obligations as demand for physical commodities begin to drive prices is sure to result in market dislocations, threatening the solvency of trading banks and speculators.

There is also likely to be an unwinding of positions between fiat currencies. Japan has been a source of capital for America through the carry trade, and to a lesser extent a source of direct investment into European bonds. The shock of higher interest rates in Japan is bound to cause a repatriation of these funds for two reasons: firstly, at times of heightened global uncertainty, investors will liquidate positions in markets foreign to them because their accounting is in their native currency and foreign investment is an additional investment risk; and secondly, losses in domestic investments have to be funded.

It's not just Japan. It is a problem that afflicts all foreign investors in bear markets caused by rising interest rates. The reversal of investment flows which have accumulated since the last financial crisis thirteen years ago is bound to dominate foreign exchange activity. China and Russia never participated in the trend to export capital, but members of the western alliance did. The reversal of these flows is a trend which is likely to hit the dollar hard, not just in terms of commodity prices, but initially against the euro and the yen in particular.

The impact on gold

Throughout history, money has been gold, and the rest credit. When you detach credit from gold, there are consequences. Pricing goods and services in credit diverges from pricing them in gold. It is really that simple.

In this article, the assumption has been that pricing everything in gold has led to minimal fluctuations in gold’s purchasing power. But fluctuations do occur, and because fiat currencies dominate pricing, they are driven mostly by changes in the status of credit. There was no clearer example of this than the divergence in pricing between gold and fiat which followed the end of the Bretton Woods era, illustrated in our earlier chart comparing oil priced in gold with oil priced in dollars. The chart below puts it directly in a gold versus fiat context.

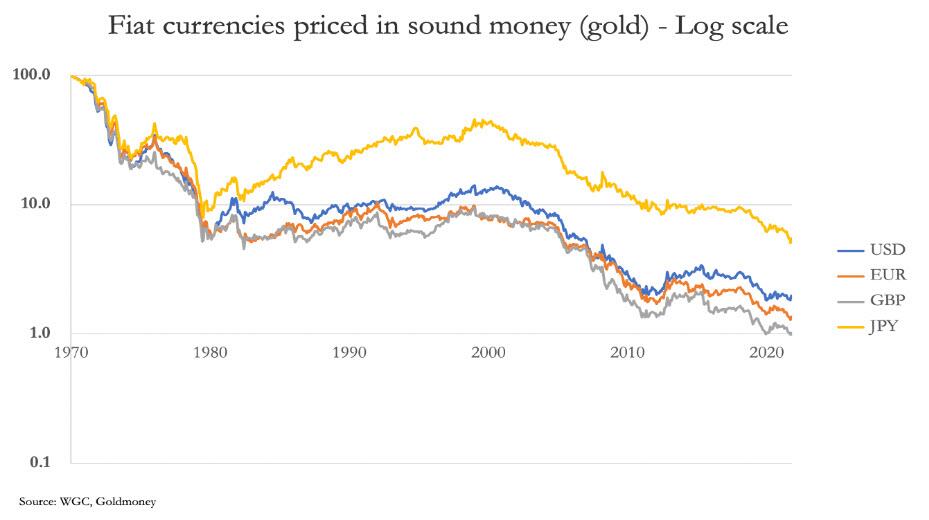

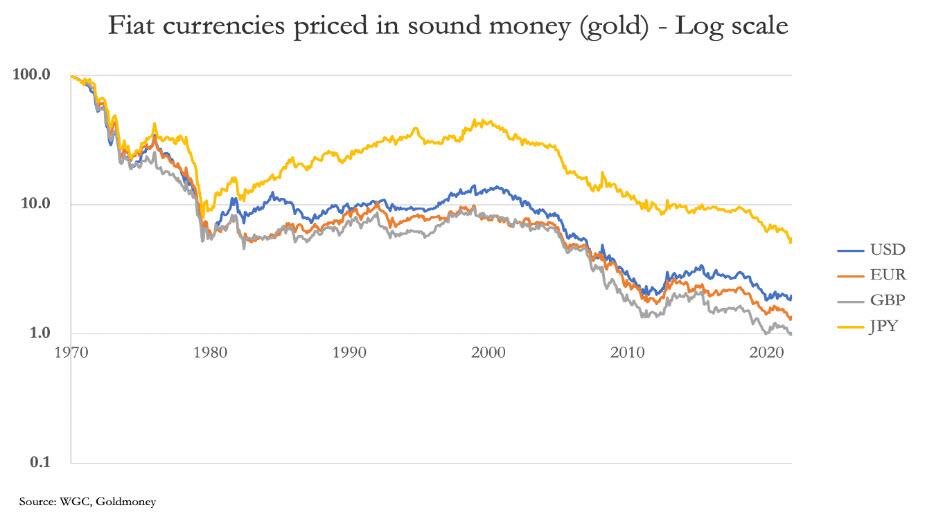

Since the suspension of Bretton Woods, the dollar has lost 98% of its value relative to real money, which is gold. The other major fiat currencies have been similarly impoverishing, and only now is the final act in their destruction looming.

An acceleration in the rate of collapse of fiat currencies will obviously lead to a significant increase in demand for gold. Therefore, commodities and goods values measured in gold will fall. This would also be reflected in the purchasing power of currencies on a credible gold standard, increasing their divergence from fiat currencies even further.

What we have described is the development of a world split by an acknowledgement that gold is money and that currencies must become credible substitutes for it, and a world hooked both practically and intellectually on fiat currencies. Instead of assuming the world economy is interdependent on the economic policies of all nations, we will discover that that is not the case, and while the fiat world sinks into a currency collapse, nations which embrace sound money are set for a new phase of economic prosperity.

Authored by Alasdair Macleod via GoldMoney.com,

The consequences of Russia and her Asian allies embracing gold backing for their currencies are poorly understood in western capital markets. This move could lead to the destruction of the global fiat currency system.

According to evidence which is widely ignored in western capital markets, a move by Russia to put a new trade settlement currency and possibly the rouble as well onto a new gold standard is becoming a certainty. As a weapon of mass fiat currency destruction, the timing is probably bound up in on-the-ground military considerations, which are already showing signs of escalating in Eastern Ukraine.

As well as using gold to undermine the western currency system, a return to a credible gold standard has significant advantages for Russia and for her allies in the Shanghai Cooperation Organisation, the Eurasian Economic Union, BRICS+, and all their commodity suppliers beyond Asia. At the same time, it would destroy the west’s fiat currencies and financial system.

This article explains how one part of the global economy can thrive while the other collapses.

Introduction

Recently, I have written about the signals emanating from Russia that President Putin is minded to re-adopt sound money by returning to some sort of gold standard. We do not yet know the details, but consider what he said at the St Petersburg International Economic Forum in June last year:

“Caught in the inflationary storm, many nations are asking, why bother exchanging goods for dollars and euros when they are losing value right before our eyes? Indeed, the economy of imaginary wealth is being inevitably replaced by the economy of real valuables and hard assets.

“According to the IMF, today’s global foreign currency reserves contain 7.1 trillion dollars and 2.5 trillion euros. And this money is depreciating at an annual rate of about 8%. Moreover, it can be confiscated or stolen at the whim of the US if it disapproves of something in a country’s policy.

I think this has become a very real threat for many countries that keep their gold and foreign exchange reserves in these currencies. According to objective expert analysis, in the coming years a conversion process of global reserves will get under way. Reserves will be converted from weakening currencies into tangible resources like food, energy, commodities, and other raw materials. Clearly, this process will further fuel global dollar inflation.”

This message was delivered to 81 official delegations, and 14,000 delegates from a further 49 countries, including heads of state and government attending unofficially. Putin’s message was that central banks will be dumping dollars and euros and accumulating gold reserves instead — the only “tangible resources” they can own, not stored in western vaults where they can be impounded as has happened to Venezuela. And government agencies will stockpile essential commodities, raw materials, and food instead.

The statement on gold reserves was not so specific, but by disposing of dollars and euros, trade and foreign exchange liquidity is bound to swing in favour of gold. With central banks reported to have accumulated record quantities of bullion last year, they appear to agree with President Putin.

In effect, delegates at the St Petersburg Forum were put on notice that the dollar will be attacked by Putin’s mobilisation of foreign liquidation of currency reserves in favour of tangible commodities and gold. For many central banks, the logic of maintaining official currency reserves will no longer apply, while increasing physical gold holdings under their direct control is the new priority.

The timing of the dollar’s demise will in large part be set by Putin’s geopolitical timing, because he can almost certainly trigger foreign liquidation simply by passing the word.

Separately, Putin’s senior economic adviser, Sergey Glazyev, has been working officially on a new trade settlement currency for use between members of the Eurasia Economic Union (EAEU), with an ambition to extend the settlement facility to all members of the Shanghai Cooperation Organisation (SCO) and BRICS+ (a rapidly expanding club of nations including non-Asian nations) who wish to use it. These groupings represent well over half the world’s population.

From the few statements on his thinking, it has become clear that having considered the options Glazyev now favours a currency solution based on gold alone.

We should also note that the proposal for an expanded Moscow gold exchange is being headed up by Glazyev himself. And in a move which appears to front-run developments, Sber — Russia’s largest bank — announced the introduction of a gold-backed digital financial fund.

On 27 December, the same day that Sber announced its new digital gold fund, in an article entitled “Golden rouble 3.0: How Russia can change foreign trade infrastructure”[i] written for Vedomosti, a Moscow-based Russian business newspaper, Glazyev laid out his latest thoughts. It was co-authored by Dmitry Mityaev, who is Assistant Member of the Board for Integration and Macroeconomics of the Eurasian Economic Commission — so this article is not just Glazyev’s musings, and it can be assumed to carry official weight.

From this article, the EAEU currency commission now appears to have dropped earlier proposals for a new currency entirely, using gold instead as the principal means of settling trade imbalances. It is likely to wrapped up as a digital representation of physical gold. If it copies the Bretton Woods model, perhaps only participating central banks will be permitted to demand physical delivery, but the digital currency would be more widely available as credit for trade settlement.

Presumably, the requirement to be prepared to settle national payment imbalances in gold bullion could be then minimised if one or more national currencies went onto a credible gold standard either by linking their currencies to the new trade settlement currency in an Asian version of Bretton Woods, or by going onto individual gold standards. The implication is that the rouble, and probably China’s yuan might do just that to produce a seamless gold-linked pan-Asian settlement system.

Whatever the detail, this is not a step to be taken lightly. China is highly dependent on exports to America and NATO members. But she appears to be refocusing on Asia and has the personal savings available to back the necessary capital investment, which in some cases will offset her imported energy costs. Both Russia and the Saudis heading up OPEC+ will be fully aware of the impact on the fiat petrodollar regime of switching payments to yuan, roubles, or other Asian national currencies for their primary export product — crude oil. Reserves of western alliance fiat currencies not sold might have to be written off. Consequently, the Saudis and other Gulf energy exporters are sure to have sought assurances about the stability of yuan and possibly roubles relative to the dollar.

Therefore, we have three elements pointing to an emerging gold standard in Asia, and for the nations that are associated with it. Firstly, President Putin made it clear that he sees a transition to sound currency values based on commodities (i.e. represented by gold), away from the dollars and euros which can be weaponised by America and alliance nations in its sphere of influence. Secondly, Putin’s view is being echoed by his senior economic adviser, Sergey Glazyev, who is the central figure formulating trade settlement arrangements. And thirdly, it is impossible to imagine that Middle Eastern energy exporters would accept payment in currencies other than dollars unless they were given sufficient reassurances about their future payment values relative to the petrodollar.

Until last year, the Russian and Chinese long-term policy of doing away with dollars for pricing commodities, settling cross-border trade, and intermediating in virtually all foreign exchange transactions has been defensive, letting America make the geopolitical running. Sanctions against Russia changed all that. Backed into a corner, Putin has no option but to seek to destabilise the western financial system deliberately. He quickly moved to protect the rouble. Now he is taking the initiative, and as part of his effort to remove the American threat from Eastern Europe entirely his strategy is both military and financial.

Pricing Russian commodities

As the world’s largest exporter of energy as well as of a wide range of industrial commodities and raw materials, the Russian economy stands to benefit enormously from a shift in global currencies away from the fiat dollar and associated western currencies to the currencies whose economic backing is commodity related. And when we think of the Russian economy, we think primarily in terms of oil. There is a further relevance to energy because it is a topic Putin thoroughly understands, his post-graduate qualification being in energy economics. He has always had a firm grip on the global energy scene, including gas and nuclear, fully understanding the western alliance’s pressure points. And on the evidence, with his close advisers he also appears to have a better grasp of monetary theory than his opposite numbers in the western alliance.

It is in this context that we should view the price of oil and its history.

The chart above is instructive, particularly with respect to the price of oil in gold. In 1950, WTI benchmark oil was priced at $2.57, and with gold fixed at $35 to the ounce, the gold equivalent was 2.361 grammes to the barrel. The oil price increased to $3.56 (3.06 gold grammes) by the time the Bretton Woods agreement was suspended. Until then, priced in dollars the price had been remarkably stable, and some of that increase in the oil price before the end of the Bretton Woods agreement was understandable, because the dollar’s official value in gold began to be challenged in the markets before Bretton Woods was suspended in 1971.

The price stability between 1950 and 1971 (when Bretton Woods ceased) was remarkable. The expansion of credit, measured by M3 money supply between those dates was substantial, since 1960 more than doubling. According to the monetarists, the purchasing power of the dollar should have approximately halved. The plain fact that it didn’t is evidence that so long as a currency’s link with gold enjoys market credibility, it will not lose purchasing power due to credit expansion. What did give eventually was not prices, but an increasing run agaist US gold reserves which fell from a peak in 1949 of 21,828 tonnes to 9,070 tonnes by 1971.

Gold’s purchasing power enjoys unrivalled stability, which is why it has always been money throughout the ages. All evidence confirms this, illustrated in our next chart, which is of wholesale prices in the UK during the gold standard from 1817—1914.

Following the economic consequences of the Napoleonic Wars and when the new gold standard bedded in, over time price levels stabilised. As banking systems became increasingly refined following the 1844 Bank Charter Act and the Bank of England joining the London Clearing System in 1864, by this measure the general level of prices became increasingly constant.

To confirm gold’s price stability, we can go even further back to the time of Diocletian, who produced his edict of maximum prices in 301AD. The circumstances were that the purchasing power of the denarii coin was falling due to its debasement. From the edict, we find that a gramme of gold was fixed at 216 denarii, giving us a conversion value for goods listed in the edict for comparison with today. From this, we know that in today’s currency pork was about $4 a pound, sea fish about $8 a pound and a dozen eggs $3.32. Vin ordinaire was $2.96 for a 75cl bottle, and good quality wine $11.10 a bottle. Beer was $3 a litre. Clearly, prices for staples which we still consume were similar to today, irrefutable evidence that gold valued as money is stable even over thousands of years.

Following the ending of the Bretton Woods agreement, the price of oil in gold showed the same long-term relative stability at a time when it fluctuated wildly in dollars. Since 1971, measured in dollars WTI oil has been as high as $140 and even went negative due to problems emanating from futures markets in April, 2020. In gold grammes the range has been 4.88 and 0.35. There can be little doubt that price volatility in gold would have been considerably less if American attempts to demonetise gold, suppress its dollar price, and rig markets generally over the decades had not taken place. To see prices being considerably more volatile in dollars than in gold grammes following the end of Bretton Woods confirms the better means of pricing oil, and therefore the whole commodity complex, is in gold.

Bearing in mind that Russian economists were never exposed to Keynesian philosophy before the collapse of the Soviet Union, senior advisers such as Sergey Glazyev are almost certainly aware that gold remains money despite American propaganda that it has been superseded by the US dollar. Putin’s economic advisers had complained that the Bank of Russia’s policy of selling all mined gold into London before trade and financial sanctions were imposed showed that its senior management had been captured by the economic and monetary policies of western central bankers and did not represent their own views.

Putin will know that priced in gold, Russia’s commodity exports should have broadly retained their market value. Both Glazyev and Putin will also know that the gold price of oil today is 1.32 grammes per barrel, down 42% from the 1950 level of 2.36 grammes, and down 51% from 2.67 grammes price when the Bretton Woods agreement was suspended. Russia has lost badly from the west’s fiat currency regime.

There is a further issue in that the only significant sources of oil which require minimal energy to extract are in the Middle East and Siberia. Elsewhere, oil, particularly shale requires substantial energy input, fuelled by oil derivatives. It is in this context that we must view attempts by Russia in partnership with the Saudis and Iran to take command of global oil pricing.

According to British Petroleum’s 2022 statistical review, global crude oil supply in 2021 was 89,877,000 barrels daily, of which Russia and the Middle East combined was 41,985,000. Viewed this way, the strategic importance for both Russia and the Middle East to work together to control pricing becomes clear. Furthermore, with the advanced nations in the west bent on reducing fossil fuel dependency and therefore their own oil production hands further pricing power to Asian suppliers.

If Russia decides to push up global prices while continuing to offer oil at discounted prices to her allies, then the price in gold grammes becomes relevant, given the increasing evidence that gold will return to underpin trade and possibly national currencies in the SCO, the EAEU, and BRICS. As noted above, the gold gramme price when Bretton Woods was suspended was 2.67 grammes per barrel, today it is 1.42 grammes. At today’s gold to dollar exchange rate of $1840, that would be the equivalent of $150 per barrel.

The monetary consequences of Asian gold standards

We can assume that the consequences of the Asian hegemons backing their payment systems with gold will have been carefully considered by them, particularly by the Russians who have been forced into bringing forward a means of protecting their export revenues from weaponised dollars.

Besides bringing stability to export values there are other advantages to reintroducing gold into currency systems. Interest rate stability at lower rates is an obvious benefit. Currently, the Bank of Russia’s key interest rate is 7.5% and price inflation is estimated at 11.8%. The yield on Russia’s 10-year OFZ bond is 11%. If the rouble becomes a credible gold substitute, price inflation, interest rates, and bond yields can be expected to decline towards levels that reflect gold’s long-term stability. And assuming that credit expansion by Russia’s commercial banks is not excessive, there is no reason to expect otherwise than that financial stability for the currency and the Russian economy would continue in the long-term. Coupled with low taxes (Russia’s income tax is a flat 13%) this stability can be expected foster genuine economic progress and the accumulation of personal wealth for the Russian people.

Following the Napoleonic Wars, these are the conditions that led Britain to becoming the most powerful commercial entity in the world by the First World War. They will foster the industrial revolution planned by both Russia and China in partnership with the Eurasian continent’s members of the SCO and EAEU. The stability that gold gives to participating currencies is bound to attract other nations away from the US dollar-based fiat currency system to participate in this success. And as momentum for the new currency regime grows, Russia’s price inflation, interest rates and bond yields are bound to decline to zero, 2%, and 3% or 4% respectively.

However, a move towards gold backing for their currencies by the Asian hegemons can be expected to undermine the purchasing power of western fiat currencies. International capital will leave fiat currencies for commodities, with nations rebuilding stockpiles of energy, metals, and other raw materials. Precious metals, specifically gold, will be sought and its price can be expected to increase.

The consequences for commodity prices being measured in gold grammes or in gold currency substitutes will be to drive commodity prices measured in declining fiat currencies even higher. In the example given earlier in this article, which suggests that in today’s dollars the pre-Bretton Woods oil price would be the equivalent of $150 per barrel, this value is struck with gold at $1840. A rise in the gold price measured in declining fiat currency would easily take this oil price estimate to well over $200.

The consequences for wholesale and consumer prices in the western nations would rapidly become obvious, with central banks forced to revise their expectations for price inflation sharply higher, forced to adjust their interest rate policies accordingly. Bond yields can be expected to rise, undermining all financial and property values. As this negative outlook clarifies, measured against gold fiat currencies will likely enter a substantial relative decline.

The consequences of the emergence of gold backing for currencies in Asia on the currencies and economies of the western alliance are bound to differ in their detail. Briefly, the following difficulties for the major players are likely to emerge:

-

The reliance on inward foreign investment has protected the dollar from continual trade deficits and played a key role in funding US Government debt since the end of Bretton Woods. It has allowed the US Government to run budget deficits more or less continually. The accumulation of foreign capital as the counterpart of trade imbalances now appears to have slowed and will reverse if President Putin follows through on his warning at the St Petersburg Economic Forum, persuading attendees to actively sell dollars. The US Government will face significant funding hurdles against foreign liquidation of Treasuries. Bond yields and funding costs for the government are bound to rise to crisis levels. And the Fed’s own financial condition will become a further source of concern for foreign exchange markets. Furthermore, the commercial banks have balance sheet constraints, restricting their ability to create further credit under Basel III rules.

-

The consequences for the EU and the eurozone would be both politically and economically divisive. If it were not for political constraints, Germany would naturally drift towards cooperation with the sound money regimes emerging to her east, particularly as the finances of the Mediterranean club deteriorate, needing yet more support at the expense of Germany’s wealth. With falling bond prices, the entire euro system comprised of the ECB and its national central banks would need to be recapitalised, being already in negative equity. The eurozone’s global systemically important banks (G-SIBs) are extremely highly leveraged and unlikely to survive the combination of falling asset values and bad debts that would be the certain consequences of the euro’s declining purchasing power. Having been assembled at the behest of a political committee and now managed by a political cabal, the euro is at risk of losing all market credibility.

-

The consequences for the Japanese yen will also be harsh. The Japanese economy is highly dependent on imported commodities and raw materials. Higher prices in yen will feed through to yet higher prices through the value chain. Already, Japanese inflation is recorded at 4%. The CPI includes prices suppressed by government subsidies giving a cosmetic effect. The Bank of Japan has taken a losing bet on the inflation outlook, continuing to assume that it was transient long after other major central banks accepted that inflation was not going to subside so easily as they originally thought. Government bond yields up to two years maturity still have negative yields, illustrating the unreality of the BoJ’s three-wise-monkeys approach to price inflation and interest rate policy. For now, the BoJ is aggressively rigging the bond market to keep yields suppressed by buying enormous quantities of 10-year JGBs to cap their yield at 0.5%. One way or another, the ending of this policy is going to forced upon the BoJ and the shock to government finances will be tremendous. The government debt to GDP ratio stands at over 250%, and a rise in funding costs is likely to be catastrophic for the yen.

-

The consequences for the UK pound will also be significant. In a similar debt trap to that of the US Government, the British have the further disadvantage of an economy suppressed by increasing taxes. Furthermore, with London being the international financial centre built on fiat currencies, the UK will be at the epicentre of a fiat currency crisis. For the size of her economy, the UK has little in the way of gold reserves, hampering any future escape from the fiat currency trap.

Not only will the major governments aligned both economically and intellectually with the fiat dollar as their reserve currency be left with a comparative disadvantage by an Asia moving to sound money standards, but their economies are exposed to highly costly welfare commitments. Politically, it is proving impossible for them to respond to developments in Asia with cuts in public spending. Rising prices, which in reality represent declining purchasing power for fiat currencies, will require significantly higher interest rates to stop foreign selling in favour of strategic commodity and gold reserves.

A moment of fundamental choice is rapidly approaching: will central banks continue to suppress interest rates to save financial markets and support economic activity, or will they act to protect the currency and ignore the financial and economic consequences? The political imperative is clear, not least because of the consequences for government funding costs and liabilities. Furthermore, economists in governments and central banks would be reluctant to abandon their embedded economic and monetary policies by protecting their currencies because it would be an admission of failure.

Already, financial commentators are aware of the approaching dilemma, referring to it as a policy pivot. Conditioned to be inflationists, they are all warning of the dangers of higher interest rates, and owners of financial assets are banking on this so-called pivot taking place. But a pivot only delays the outcome by very little time because the consequences of a rapidly depreciating currency relative to commodity and other cost inputs will soon lead to economic activity being hampered, business plans rapidly becoming obsolete, and unemployment rising catastrophically. The Keynesian response of economic stimulation will simply not be available.

The only salvation will be for western governments to jettison Keynesian macroeconomics entirely and revert to classical economic theories. The false assumptions that have built up over the last hundred years will have to be overturned. Therefore, economists in central banks and government departments will not be intellectually equipped to provide solutions. Re-education against a background of economic crisis driven by collapsing fiat currencies will take some time; time that markets are unlikely to grant.

Crises of this sort nearly always emanate in the foreign exchanges because it is foreign holders of currencies who are the first to recognise a currency’s weakness. Usually, it involves a specific currency. But this time, it will affect all the major currencies in the western alliance. Furthermore, instead of a shift between fiat currencies, much of the crisis will reflect the wholesale selling of fiat currencies for commodities and gold. Additionally, the error the western alliance made in rendering their currencies worthless in Russian hands has tipped off all foreign holders of fiat currencies to their true value.

A sensible course for any non-aligned government would be to swap currency reserves for strategic reserves, the latter being comprised of commodities, raw materials, and foodstuffs. The pressure this switch would bring to bear on markets is not restricted to currencies but is a reversal of the conditions which have underpinned the growth of derivatives. The scramble to cover paper obligations as demand for physical commodities begin to drive prices is sure to result in market dislocations, threatening the solvency of trading banks and speculators.

There is also likely to be an unwinding of positions between fiat currencies. Japan has been a source of capital for America through the carry trade, and to a lesser extent a source of direct investment into European bonds. The shock of higher interest rates in Japan is bound to cause a repatriation of these funds for two reasons: firstly, at times of heightened global uncertainty, investors will liquidate positions in markets foreign to them because their accounting is in their native currency and foreign investment is an additional investment risk; and secondly, losses in domestic investments have to be funded.

It’s not just Japan. It is a problem that afflicts all foreign investors in bear markets caused by rising interest rates. The reversal of investment flows which have accumulated since the last financial crisis thirteen years ago is bound to dominate foreign exchange activity. China and Russia never participated in the trend to export capital, but members of the western alliance did. The reversal of these flows is a trend which is likely to hit the dollar hard, not just in terms of commodity prices, but initially against the euro and the yen in particular.

The impact on gold

Throughout history, money has been gold, and the rest credit. When you detach credit from gold, there are consequences. Pricing goods and services in credit diverges from pricing them in gold. It is really that simple.

In this article, the assumption has been that pricing everything in gold has led to minimal fluctuations in gold’s purchasing power. But fluctuations do occur, and because fiat currencies dominate pricing, they are driven mostly by changes in the status of credit. There was no clearer example of this than the divergence in pricing between gold and fiat which followed the end of the Bretton Woods era, illustrated in our earlier chart comparing oil priced in gold with oil priced in dollars. The chart below puts it directly in a gold versus fiat context.

Since the suspension of Bretton Woods, the dollar has lost 98% of its value relative to real money, which is gold. The other major fiat currencies have been similarly impoverishing, and only now is the final act in their destruction looming.

An acceleration in the rate of collapse of fiat currencies will obviously lead to a significant increase in demand for gold. Therefore, commodities and goods values measured in gold will fall. This would also be reflected in the purchasing power of currencies on a credible gold standard, increasing their divergence from fiat currencies even further.

What we have described is the development of a world split by an acknowledgement that gold is money and that currencies must become credible substitutes for it, and a world hooked both practically and intellectually on fiat currencies. Instead of assuming the world economy is interdependent on the economic policies of all nations, we will discover that that is not the case, and while the fiat world sinks into a currency collapse, nations which embrace sound money are set for a new phase of economic prosperity.

Loading…