After two months in a row of MoM declines in spending, consensus forecasts both spending and incomes grew MoM in January and they were right but income grew by only 0.6% (+1.0% exp) while spending rose more than expected (+1.8% vs +1.4% exp). That is the biggest monthly jump in spending since March 2021...

Source: Bloomberg

And on a YoY basis, both income and spending accelerated in January...

Source: Bloomberg

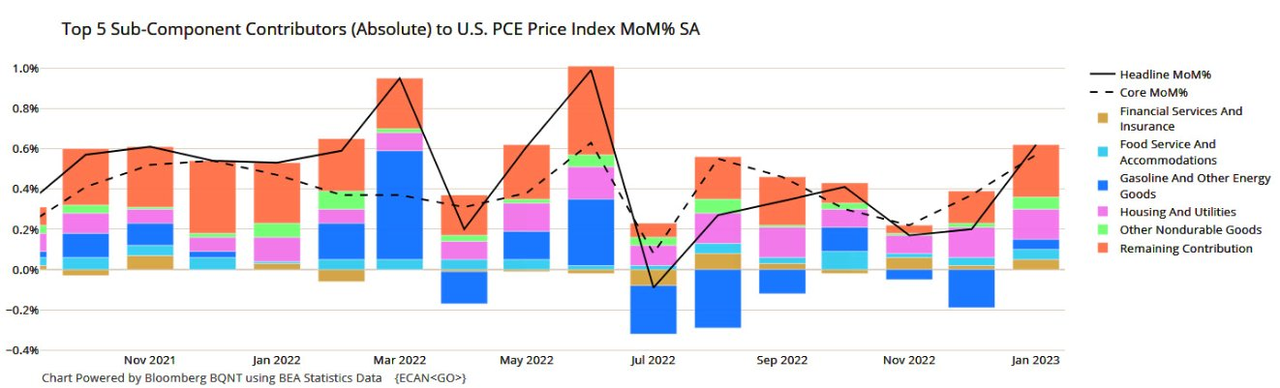

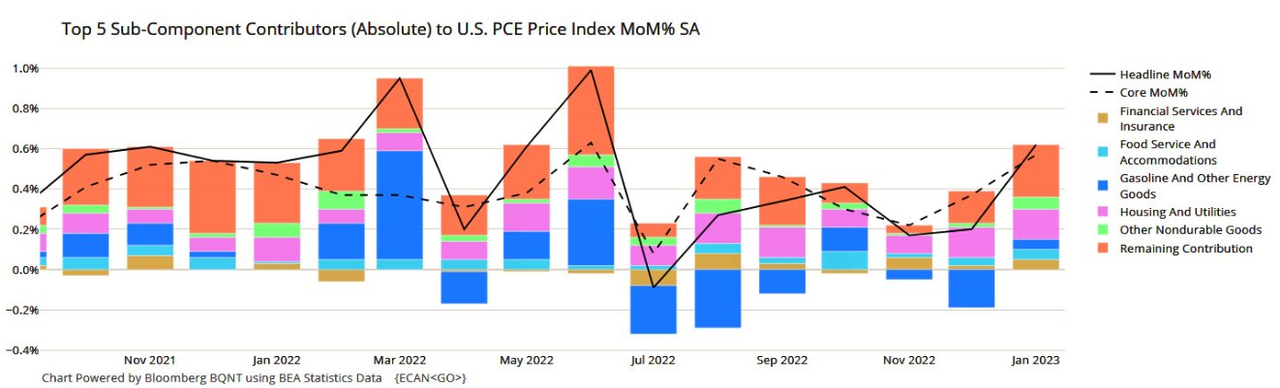

The biggest driver of the MoM jump in PCE was Housing and Other Services...

Source: Bloomberg

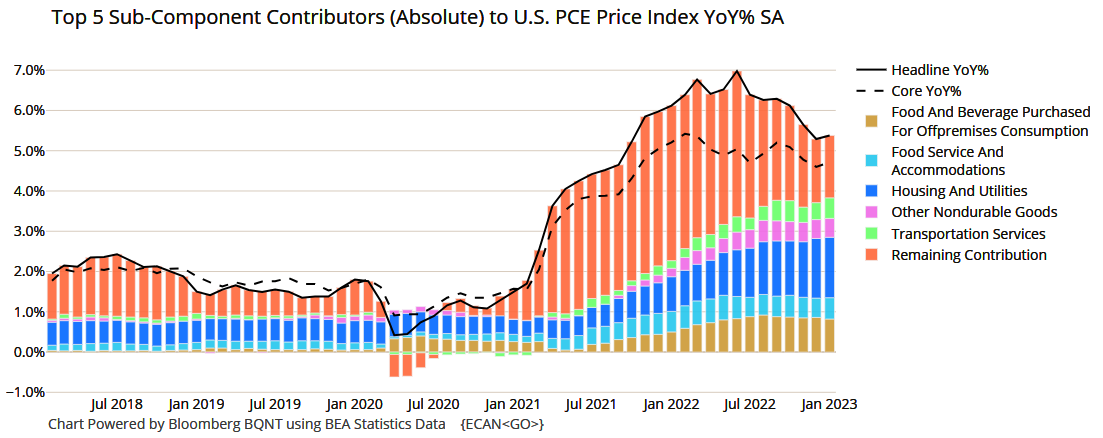

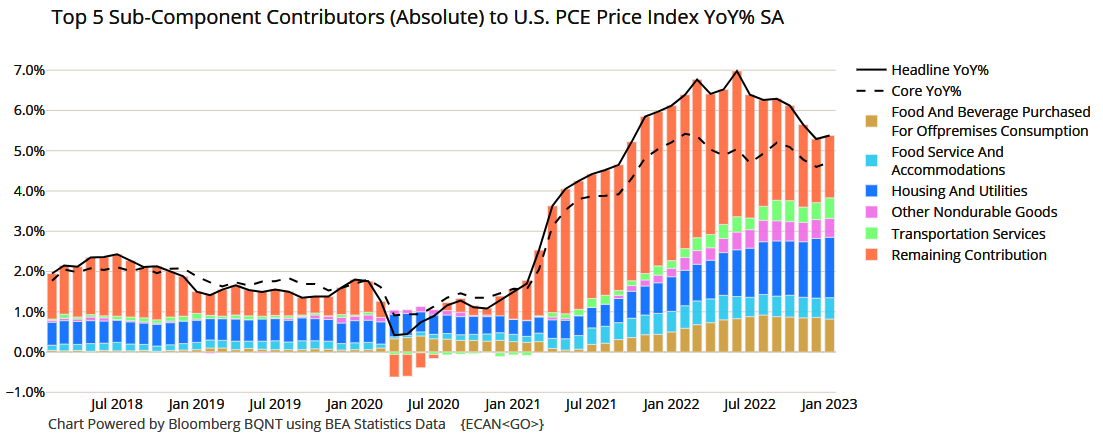

Housing and Transportation are the biggest YoY drivers of PCE...

Source: Bloomberg

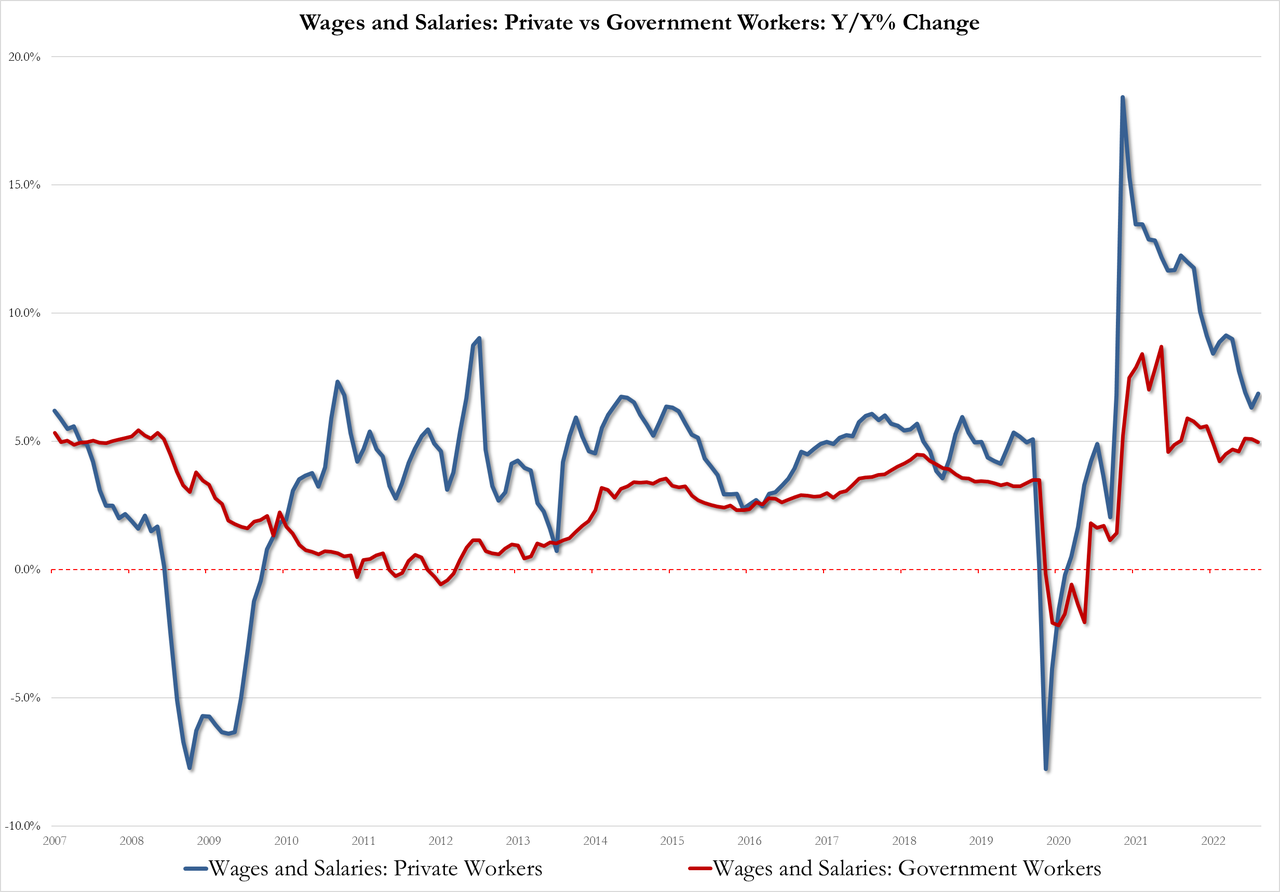

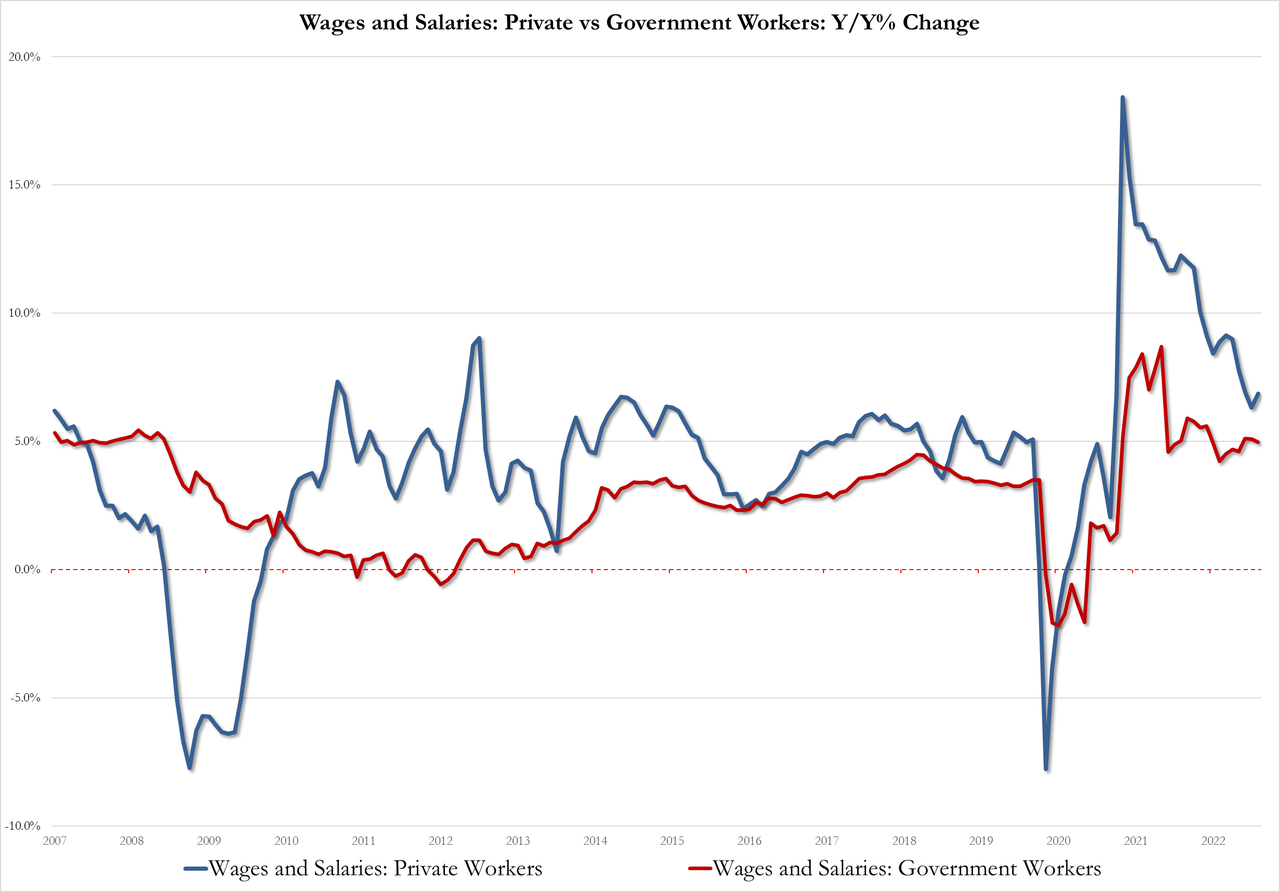

On the income side wages for private workers accelerated for the first time in 4 months, up 6.9% Y/Y, from 6.3% in Dec, but wage growth for govt workers slowed to 5.0% Y/Y, from 5.1%

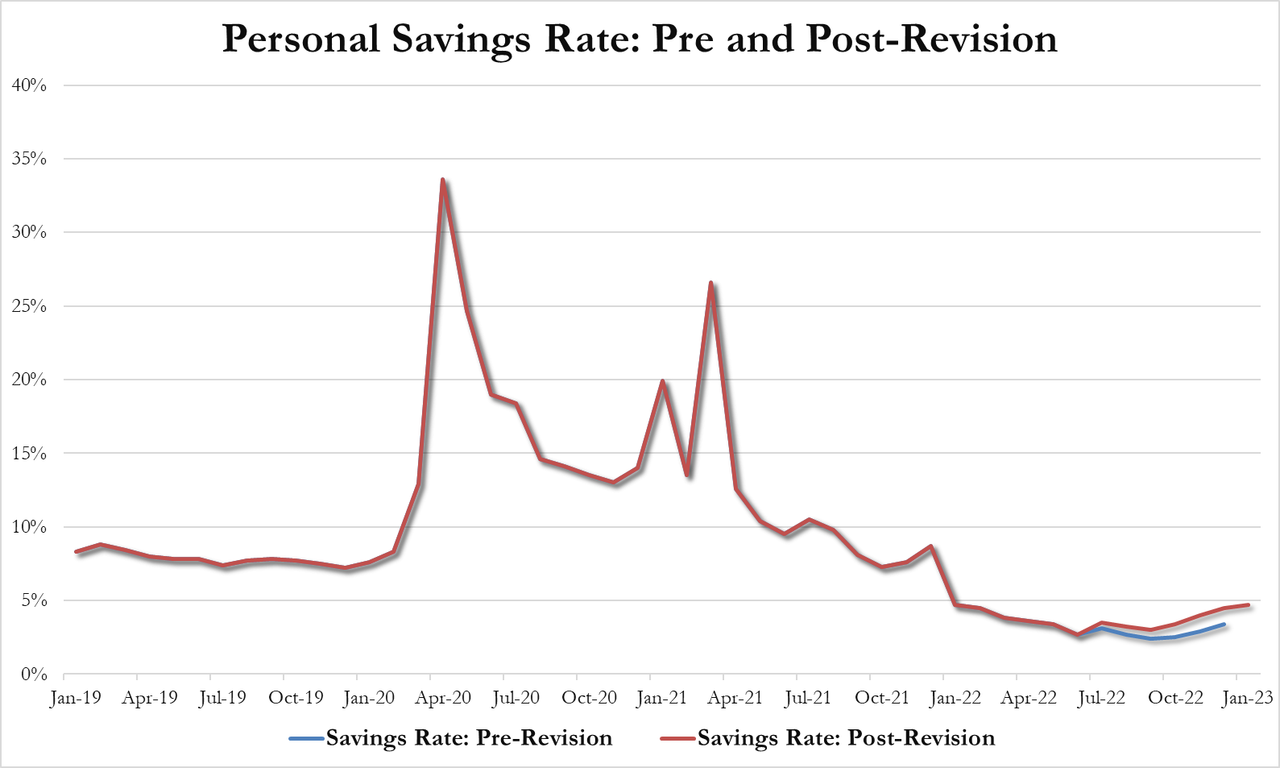

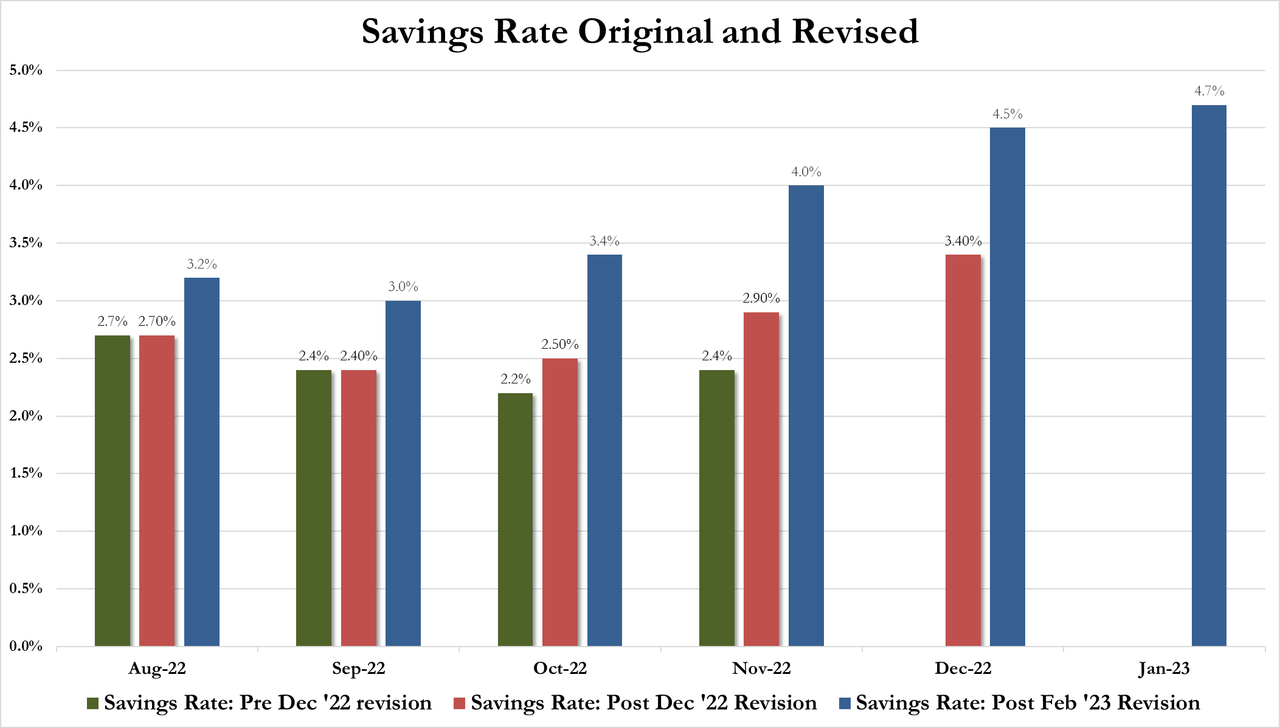

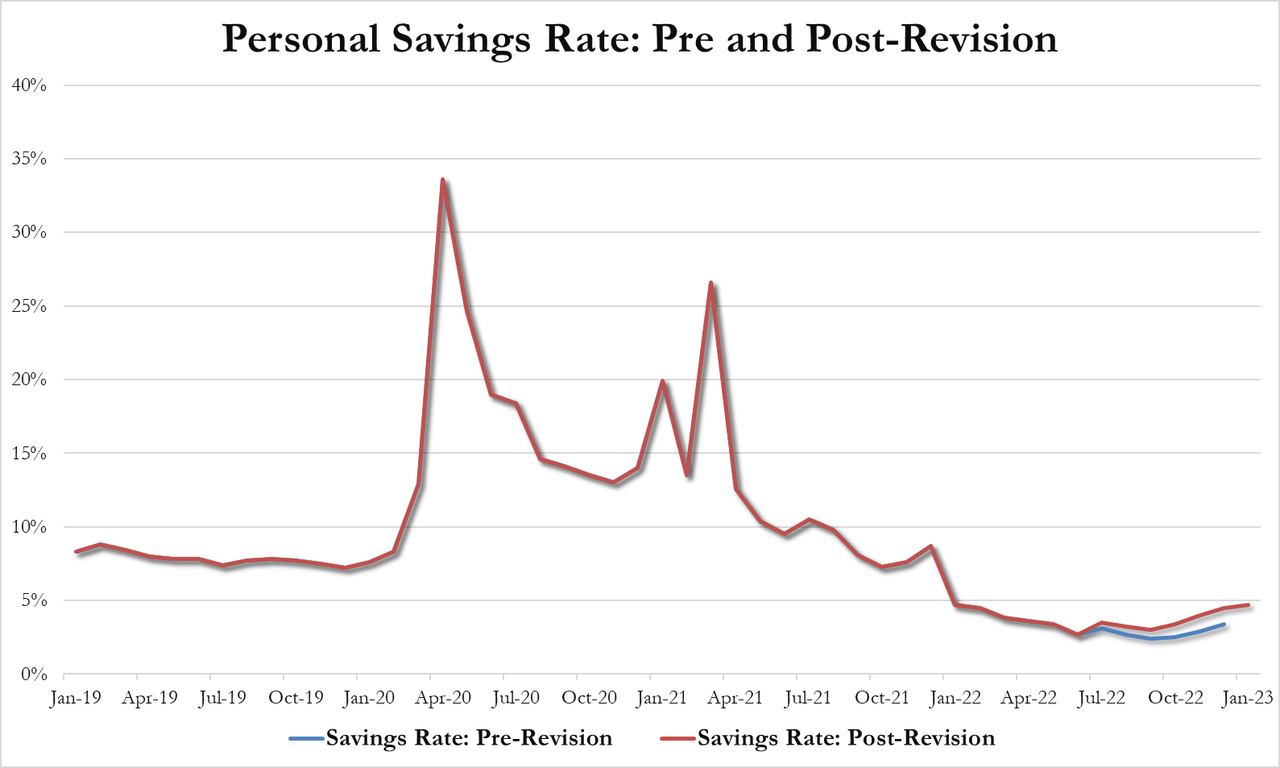

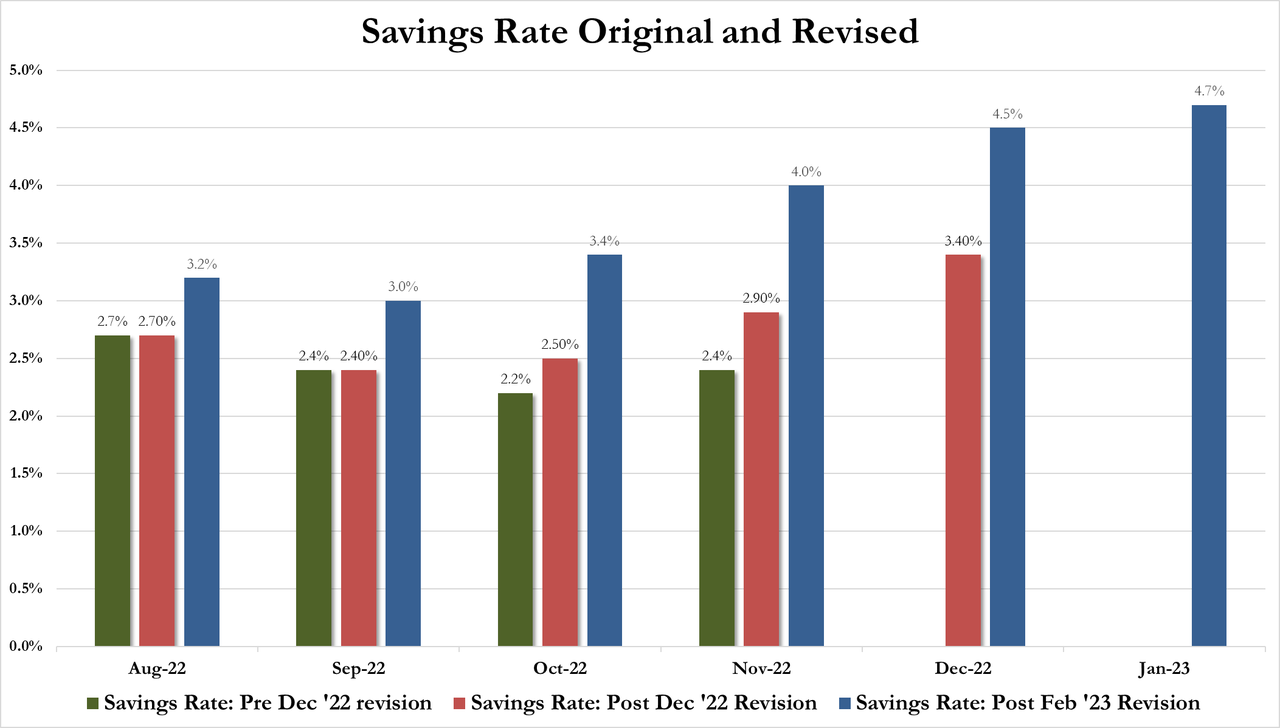

Americans' savings rate is now at 4.7%, up from 4.5% in Dec which was revised significantly higher (from 3.4% in Dec)...

The revisions are dramatic to say the least: what was 2.7% in Nov has become 4.0% and Jan is now 4.7%

But the real highlight of the report is the inflation signals from The Fed's favorite Core PCE Deflator.. and it was not good news. Both the headline and core PCE Deflators printed hotter than expected, rising 5.4% YoY and 4.7% YoY respectively ( +5.0% and 4.3% exp respectively)...

Source: Bloomberg

So much for that 'smooth'; ride lower in inflation that everyone hoped for.

Finally, we note that the market has dramatically repriced its inflation expectations (inflation swaps) in recent weeks, now at their highest for mid-2023 since November...

Source: Bloomberg

It seems the market may be on to something... and that's not good for markets.

After two months in a row of MoM declines in spending, consensus forecasts both spending and incomes grew MoM in January and they were right but income grew by only 0.6% (+1.0% exp) while spending rose more than expected (+1.8% vs +1.4% exp). That is the biggest monthly jump in spending since March 2021…

Source: Bloomberg

And on a YoY basis, both income and spending accelerated in January…

Source: Bloomberg

The biggest driver of the MoM jump in PCE was Housing and Other Services…

Source: Bloomberg

Housing and Transportation are the biggest YoY drivers of PCE…

Source: Bloomberg

On the income side wages for private workers accelerated for the first time in 4 months, up 6.9% Y/Y, from 6.3% in Dec, but wage growth for govt workers slowed to 5.0% Y/Y, from 5.1%

Americans’ savings rate is now at 4.7%, up from 4.5% in Dec which was revised significantly higher (from 3.4% in Dec)…

The revisions are dramatic to say the least: what was 2.7% in Nov has become 4.0% and Jan is now 4.7%

But the real highlight of the report is the inflation signals from The Fed’s favorite Core PCE Deflator.. and it was not good news. Both the headline and core PCE Deflators printed hotter than expected, rising 5.4% YoY and 4.7% YoY respectively ( +5.0% and 4.3% exp respectively)…

Source: Bloomberg

So much for that ‘smooth’; ride lower in inflation that everyone hoped for.

Finally, we note that the market has dramatically repriced its inflation expectations (inflation swaps) in recent weeks, now at their highest for mid-2023 since November…

Source: Bloomberg

It seems the market may be on to something… and that’s not good for markets.

Loading…