Authored by Michael Every via Rabo bank,

Forget about geopolitics for once; or rather, don’t forget about it, but it isn’t the prime focus even as the Wall Steet Journal says ‘US, China plunge further into a spiral of hostility’.

Forget about politics, despite a headline-grabbing White House budget that won’t pass Congress, and how some in Congress just argued against how we used to think journalism should be done.

Forget about the climate, as Oilprice.com argues ‘Investors Start To Realize The Energy Transition Will Take Decades’, and that: “According to analysts, there is a broader understanding among the public and governments that until a clean energy system is ready, oil and gas will continue to play a prominent role in global energy supply and, like it or not, we are stuck with fossil fuels for our current energy needs. Right now, fossil fuels account for just over 80% of global energy supply.” Which implies messier geopolitics and politics, and higher inflation.

Forget about economic data like US initial claims data spiking to 211K, the highest since….. December, when it last didn’t mean anything.

Focus instead on the sudden sell-off in the US banking sector, which has seen a massive bull steepening of its yield curve and a serious reappraisal of the odds that the Great Pivot in the Sky may bring forth the abundance of riches that it usually does when the correct correction ceremony is performed.

The problems at the individual US banks involved vary. The broader problem echoes what we saw in the UK under Truss, and what we will see in other places as rates rise. And if they don’t, as China’s local governments sell their own land to themselves to try to remain solvent. What you see is a series of investments into assets --crypto and bonds in the West, and property in China)-- collapsing in value as rates rise, or under their own weight even if rates don’t. It’s not complicated, even if complex derivatives and spin, or market freezes, can pretend all is still well.

It’s ironic that this US sell-off is happening ahead of the BOJ meeting today, where governor Kuroda bows out after a decade throwing ridiculous amounts of liquidity at a system that hasn’t responded to it. The market had been whispering he might sign off with a surprise hawkish big bang to reverse yield curve control, smoothing the policy path for his successor Ueda-san. (Who would of course be in the loop, as would the Fed.) That may still happen, but you can bank on further market volatility ahead if it now does.

We will also soon find out if the Fed is worried by the Dow falling to a four-month low(!) and small banks being punished for bad investment decisions made under ultra-loose monetary policy(!) to act. Obviously, the market thinks the Fed will pivot again. That’s how our monetary policy cargo cult has worked for the past few decades: just do the correct correction ceremony, and riches rain down on you.

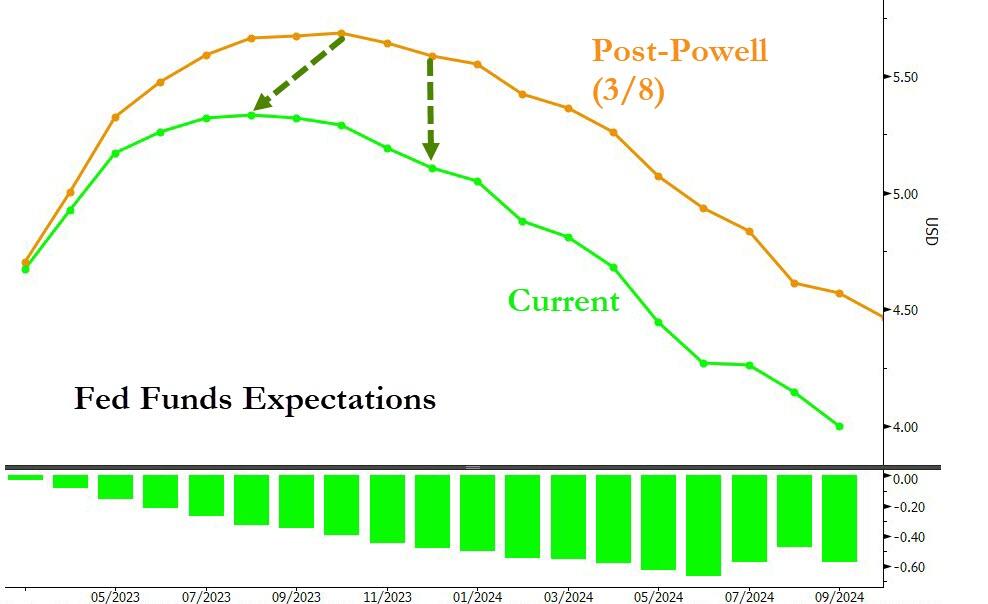

[ZH: The pivot is starting to get priced in...]

For those unfamiliar with the term, a cargo cult is defined as:

“an indigenist millenarian belief system, in which adherents perform rituals which they believe will cause a more technologically advanced society to deliver goods.

Cargo cults are marked by a number of common characteristics, including a "myth-dream" that is a synthesis of indigenous and foreign elements, the expectation of help from the ancestors, charismatic leaders, and lastly, belief in the appearance of an abundance of goods.”

There is certainly a lot of that about in markets after 40 years of ‘charismatic’ leaders providing the liquidity and other societies the goods.

Just a year ago, Fed rates were still zero and it was finally ending QE with headline CPI at 8.5%(!), while expecting cheap stuff to keep flowing domestically and internationally. Most economists still think complex physical supply chains across geopolitical fault-lines work by divine providence: “I click, cheap stuff appears.” Naturally, large parts of the market also think that if we had zero rates and QE again that all would be well. Or at least they would be well: e.g., the $2,927bn increase in US household net worth reported for Q4, more than reversing a $392bn drop in Q3 and -$1,294bn in Q2.

However, just as the US crates falling from its planes onto remote Pacific Islands dried up after the end of WW2, leaving local cargo cults frustrated, so Fed liquidity has been disappearing as policy tightens. (Although, again ironically, to push back against China, there is a huge proposed increase in the White House budget for aid to Pacific Islands.) Bond markets should note that we have seen with crypto that the Fed is now quite prepared to smash assets to show that the Great Put in the Sky does not exist anymore. Indeed, what makes markets sure that even a small bank failing is not something the FOMC would be willing to see happen pour encourager les autres?

Of course, banking ripples could escalate, and global markets are mirroring what the US is seeing because they also had low rates for too long and bad investment decisions to match.

If the Fed stands back, the market is likely to frantically engage in a more correct correction ceremony to get the Great Pivot in the Sky to shower them with gifts again.

But that still doesn’t mean it will happen. Especially after today’s strong payrolls number and if CPI next Tuesday is too.

“What, me crypto?” may be the plaintive question some then have to ask.

Of course, if the Great Pivot happens because a bank nobody has heard of bought crypto assets nobody has heard of, then the ride on inflation ahead is likely to end up with many of us looking at empty shipping containers and praying they had goods inside them - again.

Yet if there is no more monetary cargo cult then we need new ceremonies: a dance around Austrianism? Or the esoteric exegesis of bifurcated ‘rate hikes and QE (for some)’ that prevailed before neoliberalism?

But that’s all too complex for most in markets to focus on. They keep looking down at their screens and then up at the sky.

[ZH: For the first time in decades, the Fed is confronted with the dual challenge of elevated inflation & relatively severe dislocation in the banking industry.]

Happy Friday!

Authored by Michael Every via Rabo bank,

Forget about geopolitics for once; or rather, don’t forget about it, but it isn’t the prime focus even as the Wall Steet Journal says ‘US, China plunge further into a spiral of hostility’.

Forget about politics, despite a headline-grabbing White House budget that won’t pass Congress, and how some in Congress just argued against how we used to think journalism should be done.

Forget about the climate, as Oilprice.com argues ‘Investors Start To Realize The Energy Transition Will Take Decades’, and that: “According to analysts, there is a broader understanding among the public and governments that until a clean energy system is ready, oil and gas will continue to play a prominent role in global energy supply and, like it or not, we are stuck with fossil fuels for our current energy needs. Right now, fossil fuels account for just over 80% of global energy supply.” Which implies messier geopolitics and politics, and higher inflation.

Forget about economic data like US initial claims data spiking to 211K, the highest since….. December, when it last didn’t mean anything.

Focus instead on the sudden sell-off in the US banking sector, which has seen a massive bull steepening of its yield curve and a serious reappraisal of the odds that the Great Pivot in the Sky may bring forth the abundance of riches that it usually does when the correct correction ceremony is performed.

The problems at the individual US banks involved vary. The broader problem echoes what we saw in the UK under Truss, and what we will see in other places as rates rise. And if they don’t, as China’s local governments sell their own land to themselves to try to remain solvent. What you see is a series of investments into assets –crypto and bonds in the West, and property in China)– collapsing in value as rates rise, or under their own weight even if rates don’t. It’s not complicated, even if complex derivatives and spin, or market freezes, can pretend all is still well.

It’s ironic that this US sell-off is happening ahead of the BOJ meeting today, where governor Kuroda bows out after a decade throwing ridiculous amounts of liquidity at a system that hasn’t responded to it. The market had been whispering he might sign off with a surprise hawkish big bang to reverse yield curve control, smoothing the policy path for his successor Ueda-san. (Who would of course be in the loop, as would the Fed.) That may still happen, but you can bank on further market volatility ahead if it now does.

We will also soon find out if the Fed is worried by the Dow falling to a four-month low(!) and small banks being punished for bad investment decisions made under ultra-loose monetary policy(!) to act. Obviously, the market thinks the Fed will pivot again. That’s how our monetary policy cargo cult has worked for the past few decades: just do the correct correction ceremony, and riches rain down on you.

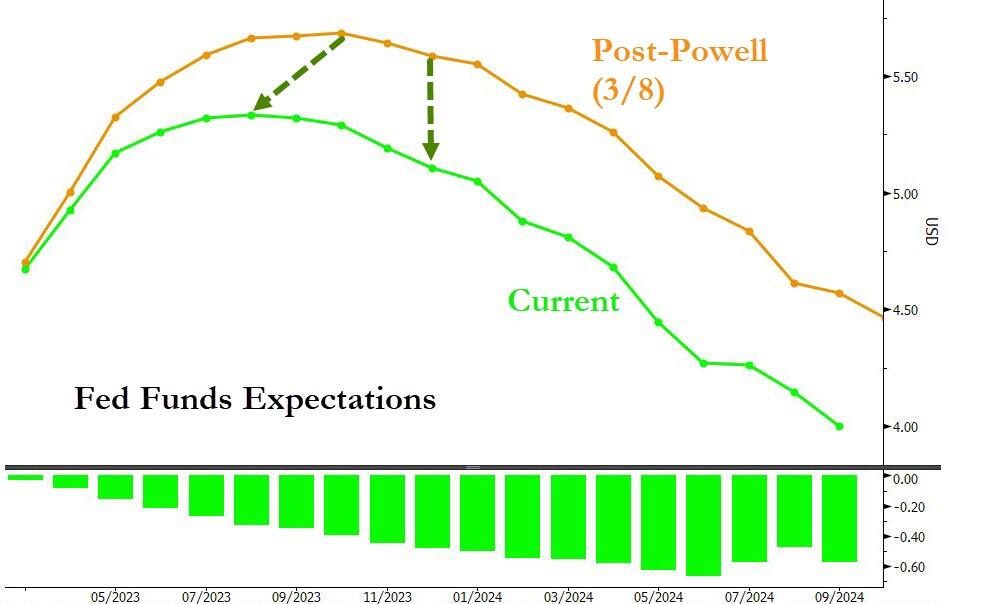

[ZH: The pivot is starting to get priced in…]

For those unfamiliar with the term, a cargo cult is defined as:

“an indigenist millenarian belief system, in which adherents perform rituals which they believe will cause a more technologically advanced society to deliver goods.

Cargo cults are marked by a number of common characteristics, including a “myth-dream” that is a synthesis of indigenous and foreign elements, the expectation of help from the ancestors, charismatic leaders, and lastly, belief in the appearance of an abundance of goods.”

There is certainly a lot of that about in markets after 40 years of ‘charismatic’ leaders providing the liquidity and other societies the goods.

Just a year ago, Fed rates were still zero and it was finally ending QE with headline CPI at 8.5%(!), while expecting cheap stuff to keep flowing domestically and internationally. Most economists still think complex physical supply chains across geopolitical fault-lines work by divine providence: “I click, cheap stuff appears.” Naturally, large parts of the market also think that if we had zero rates and QE again that all would be well. Or at least they would be well: e.g., the $2,927bn increase in US household net worth reported for Q4, more than reversing a $392bn drop in Q3 and -$1,294bn in Q2.

However, just as the US crates falling from its planes onto remote Pacific Islands dried up after the end of WW2, leaving local cargo cults frustrated, so Fed liquidity has been disappearing as policy tightens. (Although, again ironically, to push back against China, there is a huge proposed increase in the White House budget for aid to Pacific Islands.) Bond markets should note that we have seen with crypto that the Fed is now quite prepared to smash assets to show that the Great Put in the Sky does not exist anymore. Indeed, what makes markets sure that even a small bank failing is not something the FOMC would be willing to see happen pour encourager les autres?

Of course, banking ripples could escalate, and global markets are mirroring what the US is seeing because they also had low rates for too long and bad investment decisions to match.

If the Fed stands back, the market is likely to frantically engage in a more correct correction ceremony to get the Great Pivot in the Sky to shower them with gifts again.

But that still doesn’t mean it will happen. Especially after today’s strong payrolls number and if CPI next Tuesday is too.

“What, me crypto?” may be the plaintive question some then have to ask.

Of course, if the Great Pivot happens because a bank nobody has heard of bought crypto assets nobody has heard of, then the ride on inflation ahead is likely to end up with many of us looking at empty shipping containers and praying they had goods inside them – again.

Yet if there is no more monetary cargo cult then we need new ceremonies: a dance around Austrianism? Or the esoteric exegesis of bifurcated ‘rate hikes and QE (for some)’ that prevailed before neoliberalism?

But that’s all too complex for most in markets to focus on. They keep looking down at their screens and then up at the sky.

[ZH: For the first time in decades, the Fed is confronted with the dual challenge of elevated inflation & relatively severe dislocation in the banking industry.]

Happy Friday!

Loading…