With just hours left until futures open for trading late on Sunday afternoon, the situation remains extremely fluid and for now it appears that regulators, central bankers and treasury officials (we won't mention the White House where the most competent financial advisor is Hunter Biden) still don't have a clear idea of how they will coordinate or respond.

Take Janet Yellen, who said on Sunday morning that the US government was working closely with banking regulators to help depositors at Silicon Valley Bank but dismissed the idea of a bailout.

Speaking with CBS on Sunday, the treasury secretary sought to assure US customers of the failed tech lender that policies were being discussed to stem the fallout from the sudden collapse this week. The Federal Deposit Insurance Corporate (FDIC) took control of the bank on Friday morning.

“Let me be clear that during the financial crisis, there were investors and owners of systemic large banks that were bailed out . . . and the reforms that have been put in place means we are not going to do that again,” Yellen said (oh but you will, you just don't know it yet).

“But we are concerned about depositors, and we’re focused on trying to meet their needs.”

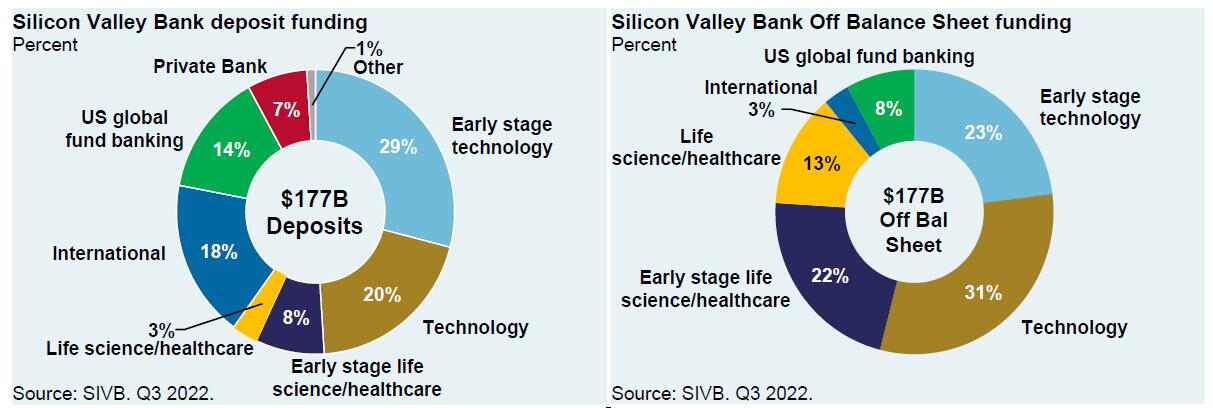

It wasn't clear which depositors she meant: as we first pointed out on Friday, out of SIVB’s $173 billion of customer deposits at the end of 2022, $152 billion were uninsured (i.e., over the $250,000 FDIC insurance threshold) and only $4.8 billion were fully insured. As we also noted last week, a further look at SIVB funding (pie charts) shows unusually high reliance on corporate/VC funding; only the small red private bank slice looks like traditional retail deposits to us.

As a result, as JPM's Michael Cembalest says "It’s fair to ask about the underwriting discipline of VC firms that put most of their liquidity in a single bank with this kind of risk profile. At the end of 2022, SIVB only offered 0.60% more on deposits than its peers as compensation for the risks illustrated below; in 2021 this premium was 0.04%".

Meanwhile, late last night, Bloomberg reported that the FDIC and the Fed are "weighing creating a fund that would allow regulators to backstop more deposits at banks that run into trouble following Silicon Valley Bank’s collapse."

According to the report which cites people familiar with the matter, "regulators discussed the new special vehicle in conversations with banking executives." And here the punchline:

The hope is that setting up such a vehicle would reassure depositors and help contain any panic, said the people. They asked not to be identified because the talks weren’t public.

Well, needless to say, any time one mentions "hope" as a wise macroprudential policy, alarms go off, because the entire banking system suddenly becomes reduced to a game of chicken as follows: Fed/regulators won't backstop deposits today and won't admit a bank crisis is emerging, but if a bank crisis emerges and there is a flight of deposits on Monday morning, they will move.

But then it will be far too late as once a bank run has started it is virtually impossible to stop it under controlled circumstances and is why the number one prerogative for regulators is to avoid just this kind of outcome, which is catastrophic for a fractional reserve system that is entirely based on confidence, and where available "demand money" is merely a fraction of the $18 trillion in deposits, far more than the $2.2 trillion in circulating currency.

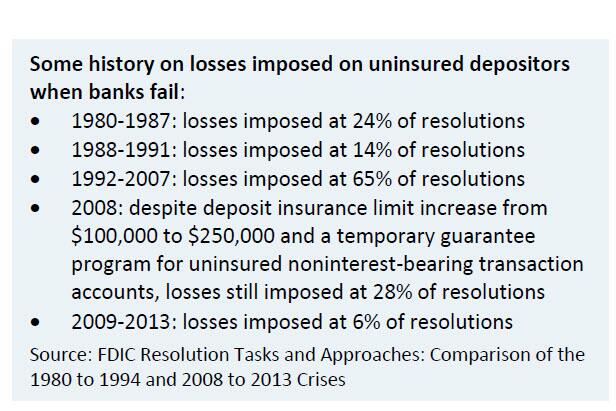

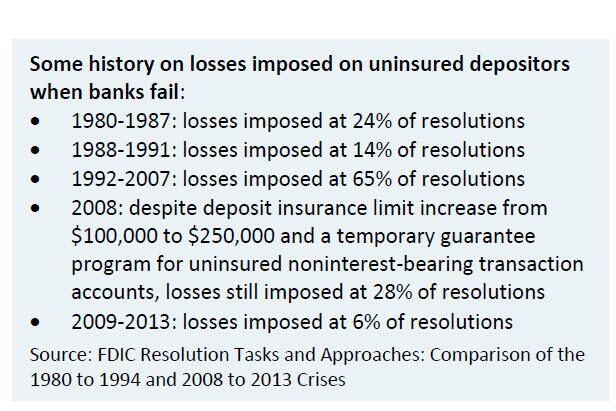

Furthermore, a quick look at historical unsecured depositor impairment numbers show that losses imposed on uninsured depositors range between 6% and 65%: huge numbers in today's context even assuming that banks are mostly solvent (which they likely won't be once the commercial real estate crisis hurricane hits).

Meanwhile, as Jason Calacanis writes, this is just the beginning.

ON MONDAY 100,000 AMERICANS WILL BE LINED UP AT THEIR REGIONAL BANK DEMANDING THEIR MONEY — MOST WILL NOT GET IT

— @jason (@Jason) March 12, 2023

THIS WENT FROM SILICON VALLEY INSIDERS ON THURSDAY TO THE MIDDLE CLASS ON SATURDAY — MAIN STREET FINDS OUT MONDAY

And while he may be conflicted - he certainly has some material losses as a result of the SVB failure - one look at what is already taking place at some smaller, vulnerable banks such as this First Republic Branch in Brentwood should be sufficient to see what comes tomorrow if the Fed makes the wrong decision today.

I’ve never seen a bank run in Brentwood Los Angeles in over 40 years — this is at first republic bank branch. People standing in rain pic.twitter.com/k31PqqpyO3

— pjb.eth (@Dr_PhillipB) March 11, 2023

The flipside to all this is that the longer the Fed waits to assure depositors - even uninsured depositors - that they are safe, the more firepower (bailout funds, TARP 2.0, rate cuts, QE) it will have to deploy much sooner than anyone previously expected as the crisis spirals out of control.

With just hours left until futures open for trading late on Sunday afternoon, the situation remains extremely fluid and for now it appears that regulators, central bankers and treasury officials (we won’t mention the White House where the most competent financial advisor is Hunter Biden) still don’t have a clear idea of how they will coordinate or respond.

Take Janet Yellen, who said on Sunday morning that the US government was working closely with banking regulators to help depositors at Silicon Valley Bank but dismissed the idea of a bailout.

Speaking with CBS on Sunday, the treasury secretary sought to assure US customers of the failed tech lender that policies were being discussed to stem the fallout from the sudden collapse this week. The Federal Deposit Insurance Corporate (FDIC) took control of the bank on Friday morning.

“Let me be clear that during the financial crisis, there were investors and owners of systemic large banks that were bailed out . . . and the reforms that have been put in place means we are not going to do that again,” Yellen said (oh but you will, you just don’t know it yet).

“But we are concerned about depositors, and we’re focused on trying to meet their needs.”

It wasn’t clear which depositors she meant: as we first pointed out on Friday, out of SIVB’s $173 billion of customer deposits at the end of 2022, $152 billion were uninsured (i.e., over the $250,000 FDIC insurance threshold) and only $4.8 billion were fully insured. As we also noted last week, a further look at SIVB funding (pie charts) shows unusually high reliance on corporate/VC funding; only the small red private bank slice looks like traditional retail deposits to us.

As a result, as JPM’s Michael Cembalest says “It’s fair to ask about the underwriting discipline of VC firms that put most of their liquidity in a single bank with this kind of risk profile. At the end of 2022, SIVB only offered 0.60% more on deposits than its peers as compensation for the risks illustrated below; in 2021 this premium was 0.04%”.

Meanwhile, late last night, Bloomberg reported that the FDIC and the Fed are “weighing creating a fund that would allow regulators to backstop more deposits at banks that run into trouble following Silicon Valley Bank’s collapse.”

According to the report which cites people familiar with the matter, “regulators discussed the new special vehicle in conversations with banking executives.” And here the punchline:

The hope is that setting up such a vehicle would reassure depositors and help contain any panic, said the people. They asked not to be identified because the talks weren’t public.

Well, needless to say, any time one mentions “hope” as a wise macroprudential policy, alarms go off, because the entire banking system suddenly becomes reduced to a game of chicken as follows: Fed/regulators won’t backstop deposits today and won’t admit a bank crisis is emerging, but if a bank crisis emerges and there is a flight of deposits on Monday morning, they will move.

But then it will be far too late as once a bank run has started it is virtually impossible to stop it under controlled circumstances and is why the number one prerogative for regulators is to avoid just this kind of outcome, which is catastrophic for a fractional reserve system that is entirely based on confidence, and where available “demand money” is merely a fraction of the $18 trillion in deposits, far more than the $2.2 trillion in circulating currency.

Furthermore, a quick look at historical unsecured depositor impairment numbers show that losses imposed on uninsured depositors range between 6% and 65%: huge numbers in today’s context even assuming that banks are mostly solvent (which they likely won’t be once the commercial real estate crisis hurricane hits).

Meanwhile, as Jason Calacanis writes, this is just the beginning.

ON MONDAY 100,000 AMERICANS WILL BE LINED UP AT THEIR REGIONAL BANK DEMANDING THEIR MONEY — MOST WILL NOT GET IT

THIS WENT FROM SILICON VALLEY INSIDERS ON THURSDAY TO THE MIDDLE CLASS ON SATURDAY — MAIN STREET FINDS OUT MONDAY

— @jason (@Jason) March 12, 2023

And while he may be conflicted – he certainly has some material losses as a result of the SVB failure – one look at what is already taking place at some smaller, vulnerable banks such as this First Republic Branch in Brentwood should be sufficient to see what comes tomorrow if the Fed makes the wrong decision today.

I’ve never seen a bank run in Brentwood Los Angeles in over 40 years — this is at first republic bank branch. People standing in rain pic.twitter.com/k31PqqpyO3

— pjb.eth (@Dr_PhillipB) March 11, 2023

The flipside to all this is that the longer the Fed waits to assure depositors – even uninsured depositors – that they are safe, the more firepower (bailout funds, TARP 2.0, rate cuts, QE) it will have to deploy much sooner than anyone previously expected as the crisis spirals out of control.

Loading…