Authored by Alasdair Macleod via GoldMoney.com,

We are all now aware that the global banking system is extremely fragile. Driving bank failures is contracting credit, which in turn drives interest rates higher. Though it is not generally appreciated, central banks have failed to suppress them.

Some regional banks have failed in the US and the run on Credit Suisse’s deposits has forced the Swiss authorities into forcing a reluctant rescue by UBS. Undoubtedly, as the great credit unwind plays out, there will be more rescues to come.

In this, the earliest stages of a banking crisis, some questions are being answered. We can probably rule out bail-ins in favour of bail outs, and we can assume that nearly all banks will be rescued — they must be in order to prevent systemic contagion.

In this article I quantify the position of the global systemically important banks (the G-SIBs) and point out that the central banks which are meant to backstop them are themselves bankrupt — or rather they would be properly accounted for.

Because even a minor failure in the banking system could undermine the entire global banking system, the much heralded pivot is now here, but not in plain sight. Because central banks have lost control over interest rates, the focus on preserving the financial markets underpinning the banking system has shifted to supressing bond yields. This is why the Fed has introduced its Bank Term Funding Programme, likely to be copied in other jurisdictions.

It is Powell’s hidden pivot — his line in the sand. But it is the last desperate throw of the dice and depends entirely on inflation being transient and interest rates not rising much more.

The price of even a successful preservation of the banking system is the destruction of fiat currencies, because the bigger picture is still of the greatest credit bubble in history unwinding.

And that process has only recently started...

The great unwind accelerates

Now that everyone in finance knows that there is a banking crisis, cynicism prevails. When a central banker or treasury minister tries to reassure the public, it is disbelieved. The risk to an extremely fragile global banking system is that if disbelief in public statements spreads from financial sceptics to the wider public, the system is doomed. All credit is based on confidence and confidence alone.

It is still too early to say that confidence has been irretrievably shaken. But last weekend, UBS was unwillingly forced by the Swiss authorities into taking over Credit Suisse on a share swap, which valued the latter’s shares at about 70 centimes. That put Credit Suisse’s shares on a discount to book value of 94%. Admittedly, this figure is unreliable when deposits are running out of the door and the full value of foreign exchange derivatives are not accounted for. But it does raise a question over the valuations of all the other global systemically important European banks. And why stop there — the G-SIBs have all taken in each other’s laundry, so if one fails so might all the rest. Perhaps they should all be similarly valued.

Presumably, in their groupthink the central bankers represented by the three wise monkeys in the illustration above never thought it would come to this. After all, their regulators have frequently conducted stress tests and all major banks routinely pass them with flying colours. But as Kevin Dowd, Professor of Finance and Economics at Durham University put it in 2016 in one of his several critical reviews of bank regulation,

“The purpose of the stress testing programme should be to highlight the vulnerability of our banking system and the need to rebuild it. Instead, it has achieved the exact opposite, portraying a weak banking system as strong. This is like having a ship radar system that cannot detect an iceberg in plain view.

“As the EU banking system goes into a renewed crisis, the UK banking system is in no fit state to withstand the storm. Once contagion spreads from Italy to Germany and then to the UK, we will have a new banking crisis but on a much grander scale than 2007-08.

“The Bank of England is asleep at the wheel again, and we will be back to beleaguered banksters begging for bailouts – and the taxpayer will be ripped off yet again, but bigger this time."

Unfortunately, it is Professor Dowd’s analysis and conclusion that have stood the test of time. And nothing, repeat nothing, has been done to alter this situation. Only last Monday, the President of the ECB proved this point by releasing the following official statement:

“I welcome the swift action and the decisions taken by the Swiss authorities. They are instrumental for restoring orderly market conditions and ensuring financial stability. The euro area banking sector is resilient, with strong capital and liquidity positions. In any case, our policy toolkit is fully equipped to provide liquidity support to the euro area financial system if needed and to preserve the smooth transmission of monetary policy.” (italics are my emphasis)[ii]

The group-thinking on stress testing is based on commonly agreed parameters between central banks and regulators for constructing stress models, and their desire to be seen discharging their duties rather than the actuality. That being the case, what we have seen in Switzerland which led to Credit Suisse being valued at only 6% of its book value is an important message not just for European bank regulation, but elsewhere as well.

Whatever their mollifying statements, the central bank groupthinkers must now be very worried. But they appear to lack coordination. The Swiss National Bank decided that as part of bailing out Credit Suisse, it would bail in higher ranking bond holders, writing off Sf17bn. That shareholders should get something while senior creditors get nothing is a travesty of company law. Following the market’s reaction, it has been swiftly denounced by regulators in Europe and London, only days after the ECB President issued the formal statement above, extoling the Swiss authorities for their actions.

The consequences of the Swiss National Bank writing off senior creditors are likely not just to impose losses on other banks which are in a fragile state themselves and can ill afford their senior debt to be traduced in this way, but to make future bond financing of banks more difficult. Furthermore, banks, insurance companies, and pension funds will be reassessing their risk exposure to all Swiss franc denominated bonds, even to the extent of impacting UBS, Credit Suisse’s rescuer.

The legal wrangling and rating downgrades probably start here, and no one comes out of it without damage to their reputations. And as already noted above, credit depends entirely on confidence. One can only assume that this will get central banks and their regulators to drop the whole bail-in concept in their attempts to ensure the survival of their commercial banking systems. Perhaps the Swiss should backtrack on their decision to save a paltry Sf17bn. We can understand and accept that Swiss banks get into trouble. But the Swiss authorities’ clumsy handling of the Credit Suisse crisis is risking its national reputation for financial probity and stability.

The broader problem is that confidence in banking is beginning to be publicly undermined. It is not just a matter of identifying the weakest links, but it is becoming a systemic problem of the widest proportions. The illusion of control by central banks is being shattered by the great credit unwind. Consequently, the policy priority is pivoting from the inflation mandate to pure survival. And as we have seen illustrated by the Swiss authorities, the scope for error is chasmic.

The G-SIB mess

Bail-in legislation was not the only G-20 response to the Lehman crisis. The Basel Committee’s third iteration of its regulations, still not fully implemented, was the Bank for International Settlement’s contribution to post-Lehman banking reform. The designation of a new category of bank, the global systemically important bank, or G-SIB, was created. G-SIBs are required to have additional capital buffers to address the systemic risks they are exposed to from international counterparties, relative to domestic regional banks.

Here are some relevant facts. At current exchange rates, total G-SIB balance sheet assets are recorded at $63,978 billion. But this is supported by only $4,444 billions of balance sheet equity, giving a ratio of assets to equity of 14.4 times. But this is not evenly spread, with the Eurozone’s seven G-SIBs averaging 19.7 times, and Japan’s three G-SIBs at 23 times. At the lower end of the scale, the US’s eight G-SIBs average 11.4 times and China’s four banks 12.0 times. All these ratios translate into unacceptable leverage when credit unwinds and interest rates increase, threatening to trigger rapidly rising levels of non-performing loans.

This is at least partially recognised in stock markets, where G-SIB shares commonly stand at significant discounts to book value. Only four out of the twenty-nine listed G-SIBs have price to book ratios greater than one. Based on last Monday’s share prices, the average price to book for Eurozone G-SIBs is a discount of 56%, for Japan 47%, for China 54%, and for the US it is only 7% bolstered by JPMorgan Chase and Morgan Stanley being the only two US banks trading at a reasonable premium to book value. There is considerable variance within these figures, but the message from the markets is clear: whatever the regulators and central banks say and despite their extra capital buffers, G-SIBs are still a risky investment.

These statistics do not tell the whole story. As we saw with the failure of Silicon Valley Bank, it was using widely adopted accounting methods to conceal losses on its bond investments. As of Dec. 31, 2022, SVB had about $120 billion in investments, primarily high quality bonds, such as US Treasuries and agency debt. According to its 10-K filed in February. the bank only had $74 billion of loans to borrowers. Therefore, its investments were significantly larger than its loans. Of the $120 billion in investments, $91 billion were classified as “held to maturity” investments and were not reported at fair value in each reporting period. Instead, they were reported at amortized cost, net of any reserves for credit losses in accordance with accounting convention.

SVB originally bought its bonds when the yield curve was positive. That is to say, the cost of short-term funding was less than the yield on the longer maturities which SVB bought. But when the Fed increased its fund rate from the zero bound, the yield curve turned sharply negative with two consequences for SVB. First, its short-term funding costs began to rise, and secondly the capital value of the bonds began to fall. Its shareholders’ capital on the balance sheet was soon wiped out, and belated attempts to rectify the situation simply broadcast SVB’s problems, leading to its demise.

It is a problem which is not confined to SVB. There will be other regional banks in the US and elsewhere which have fallen into the same trap. And it won’t be a problem restricted to regional banks. One can speculate that the incentive to buy longer maturity bonds than banks normally hold on their balance sheets was stronger in jurisdictions which imposed negative interest rates. A Eurozone or Japanese bank has had a zero or even slightly negative cost of short-term funding in their respective money markets, encouraging them to buy longer-dated government bonds. And like SVB, they will have been whipsawed by sharply rising short-term rates.

This leads us to speculate about how much of similar losses may be hidden in the entire G-SIB system. Like SVB, have they been sufficient to wipe out the notional shareholders’ capital of all the G-SIBs, which we know to be $4.444 trillion?

But this problem is not even the mother of all elephants in the room — that award goes to derivatives. The G-SIBs’ participation in regulated futures and over-the-counter derivatives is valued on their balance sheets at net mark-to-market values, which are very small fractions of their nominal values. Nevertheless, regulated futures are credit commitments for the full amounts, and should be valued as such. Options which have been sold are similarly commitments for their exercisable amounts, though bought options are not. The amounts of open interest involved at end-2022 are assessed by the Bank for International Settlements at $36,630bn for all regulated futures, and a further $43,182bn in options. These are just one side of open interest, the majority of which is bank exposure as market makers, traders, and banks acting as principals for their customers.

In OTC derivatives, foreign exchange and commodity contracts are liabilities for their full amounts, while credit swaps are not. At end-June 2022, foreign exchange contracts amounted to $109,587bn with a further $12,951bn in options. Commodity contracts add a further $2,341bn.[iii] We can exclude the large category of credit default swaps, because their gross values are purely notional. These exposures represent only one side of credit commitments, the other being distributed among non-bank financial institutions, hedgers, speculators, and other banks as well. From the G-SIBs’ collective balance sheet perspective, they should all be included at full value.

Last December, Claudio Borio, Head of the BIS’s Monetary and Economic Department even wrote a paper on this topic. Borio stated that “Foreign exchange swap positions point to over $80 trillion of hidden US dollar debt [part of the $109.587 trillion above], reported off-balance sheet”. And “The volume of daily foreign exchange turnover subject to settlement risk remains stubbornly high despite mechanisms to mitigate such risks”. In effect, Borio confirmed that for a true appreciation of global banking risk, gross OTC values for foreign exchange contracts should be recorded on both sides of bank balance sheets, and not just as net mark-to-market contract values.

Between regulated and unregulated derivatives, we are therefore staring down the barrel of a further $210 trillion of balance sheet liabilities, to be added to the $64 trillion of officially recorded total G-SIB balance sheets, all supported by only $4.444 trillion of shareholder’s funds. And while the US G-SIBs appear to be less leveraged than their opposite numbers in the Eurozone and Japan, it should be noted that as Borio points out the large majority of OTC exposure is in dollar-denominated contracts, for which the US G-SIBs are the counterparties.

If only one G-SIB fails, its counterparty risks could easily undermine all the others. As Borio pointed out, settlement risk remains stubbornly high. It explains why the Fed was ready to come up so swiftly with swap lines for the Swiss National Bank to aid it in its attempt to support Credit Suisse. And it allows us to draw a further conclusion: credit expansion at the central bank level to ensure the global financial system’s survival will place the greatest burden on the dollar, being the currency in which most of these derivative obligations are settled.

Can central banks actually handle a credit crisis?

Having invested in government and other bonds at the top of the market — a top created by them to be far higher than they would otherwise have been — central banks are now demonstrably bankrupt unless they recapitalise themselves. For all of them, excepting the ECB, it is theoretically easy to do but best done before commercial banks need their support.

The simplest way of recapitalising a central bank is by expanding its balance sheet assets in favour of equity instead of other liabilities. Delaying addressing the same problems faced by Silicon Valley Bank on the basis they need not doesn’t serve central banks well. The losses can be assumed to continue to accumulate as commercial bank credit continues to contract, because it is credit contraction which drives up the true level of interest rates. Already, the Bank of Japan has been accumulating financial assets at negative yields, so that even with a small rise on yields, its losses from last year are over four thousand times its balance sheet capital of only 100 million yen. Sooner or later, its credibility is bound to be questioned if it fails to address this issue.

But of all the central banks, the ECB is probably the most difficult to recapitalise. The ECB’s shareholders are not a single state, but the national central banks of the twenty member nations (including Croatia which joined the euro system in January). Unfortunately, with few exceptions the NCBs in the euro system are also all in need of recapitalisation.

Imagine the legislative hurdles. The Bundesbank, let’s say, presents a case to the Bundestag to pass enabling legislation to permit it to recapitalise itself and to subscribe to more capital in the ECB on the basis of its share of the ECB’s equity — the capital key — to restore it to solvency as well. One can imagine finance ministers being persuaded that there is no alternative to the proposal, but then it will be noticed by pedestrian politicians that the Bundesbank is owed over €1.1 trillion through the TARGET2 system. Surely, it will almost certainly be argued, if those liabilities were paid to the Bundesbank, there would be no need for it to recapitalise itself.

If only it were so simple. But clearly, it is not in the Bundesbank’s interest to involve politicians in monetary affairs. The public debate would risk spiralling out of control, with possibly fatal consequences for the entire euro system. It would be a row at the worst possible time. And with twenty NCB shareholders facing similar hurdles, their contributions to refinancing the ECB requires unanimous consent for proportional subscriptions in accordance with their capital keys.

Besides the confusion over bail-ins and bail outs which we can now hope has been settled, there still remains a huge question mark over whether the central banks have the wherewithal to discharge the potentially enormous burden of bail out commitments. In any event, it will need massive quantities of additional central bank credit in all relevant currencies to backstop the system. The destruction to balance sheets at both central and commercial bank levels reinforces the point, that central banks are likely to move their attention away from short-term interest rates over which they have lost control to bond yields which they can still influence. Different versions of the Fed’s Bank Term Funding Programme (more on which follows) are likely to be devised. It is becoming a hidden pivot.

The hidden pivot

In a classic banking crisis, bank balance sheets become overextended and bankers become cautious in their lending, restricting the expansion of credit. The credit shortage leads to higher interest rates for the few borrowers deemed creditworthy and able to pay them. Both producers and consumers are affected. The shortage of credit and higher borrowing costs result in businesses failing, and a slump in economic activity follows. This leads in turn to the problem identified by Irving Fisher, which he described as his debt-deflation theory.[iv] According to Fisher, when the cycle of bank lending turns down and higher interest rates and falling collateral values follow, it forces banks to call in loans, liquidating collateral and driving colateral values down further. The self-feeding nature of this phenomenon deepens the slump and leads to banking failures.

Fisher’s paper was published in the wake of record numbers of bank failures in America between 1930—1933. And it should also be noted that it has informed every state economist ever since. The fear of a slump exacerbated by collateral liquidation is in the back of every mainstream economist’s mind. But so far, there has been not much evidence of credit shortages undermining the non-financial economy. Presumably, the downturns in credit expansion reflected in broad money supply statistics have reflected banks withdrawing from financial activities, so the hit to non-financial activity is yet to come. But the issue of falling collateral values identified by Fisher has resurfaced in problems created by policy makers themselves, because the sudden rise in interest rates has had the same effect.

This is why we are now witnessing central banks pivoting from control of inflation to the preservation of the global commercial banking system. The danger of systemic failure is more hardwired into central bankers’ DNA than that of inflation. And frankly, they have proved pretty clueless on interest rate management anyway. They are set to do “whatever it takes” to preserve both financial market values and the status quo. But things have moved on from Mario Draghi’s famous aphorism. No longer just a finger-wagging threat, whatever it takes is likely to end up undermining the purchasing power of currencies. Whatever it takes is now an open-ended commitment to whatever it costs.

There can be no question that pivoting from fear of inflation to fear of a banking crisis undermines currencies. But central bankers appear to find it difficult to concede it publicly. The Fed’s solution is to offer to take in all US Treasuries, agency debt, mortgage-backed securities, and “other qualifying assets as collateral” at par with no haircut against cash liquidity for one year. Furthermore, with foreigners no longer net buyers of Treasuries, there is a funding problem to address.

The Fed stated that its new bank term funding programme (BTFP)

“…will make available additional funding to eligible depository institutions to help assure banks have the ability to meet the needs of all their depositors. This action will bolster the capacity of the banking system to safeguard deposits and ensure the ongoing provision of money and credit to the economy. The Federal Reserve is prepared to address any liquidity pressures that may arise.”

It is a policy that might have been scripted by Irving Fisher’s ghost. The one-year term of the facility shows that the Fed regards this as a temporary problem to be reversed when the situation improves, and inflation returns towards its two per cent target. Yes, all the forecasts are still for inflation to be transient — only it is taking just a little longer than originally thought.

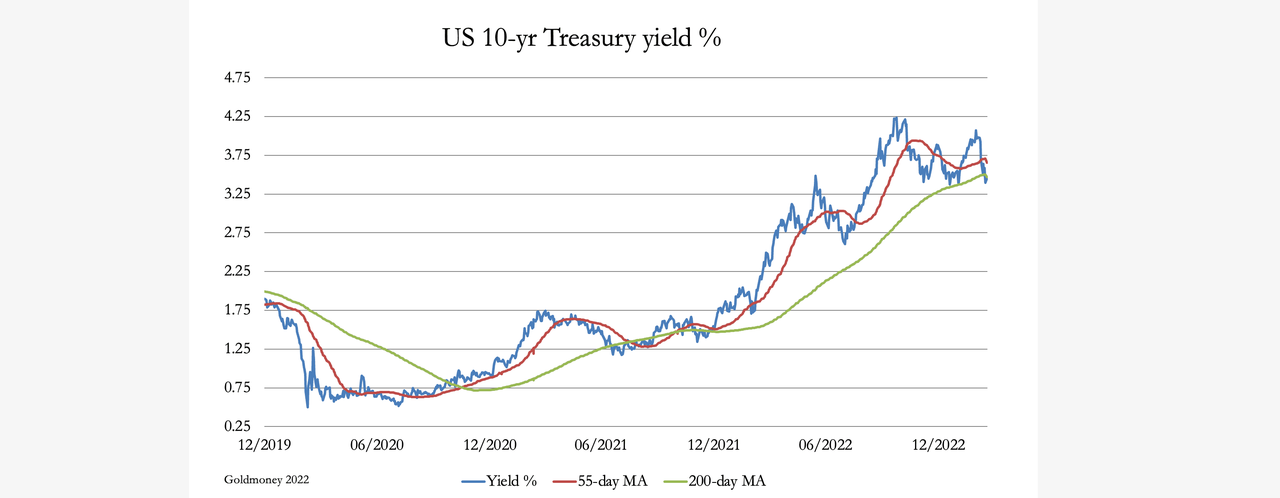

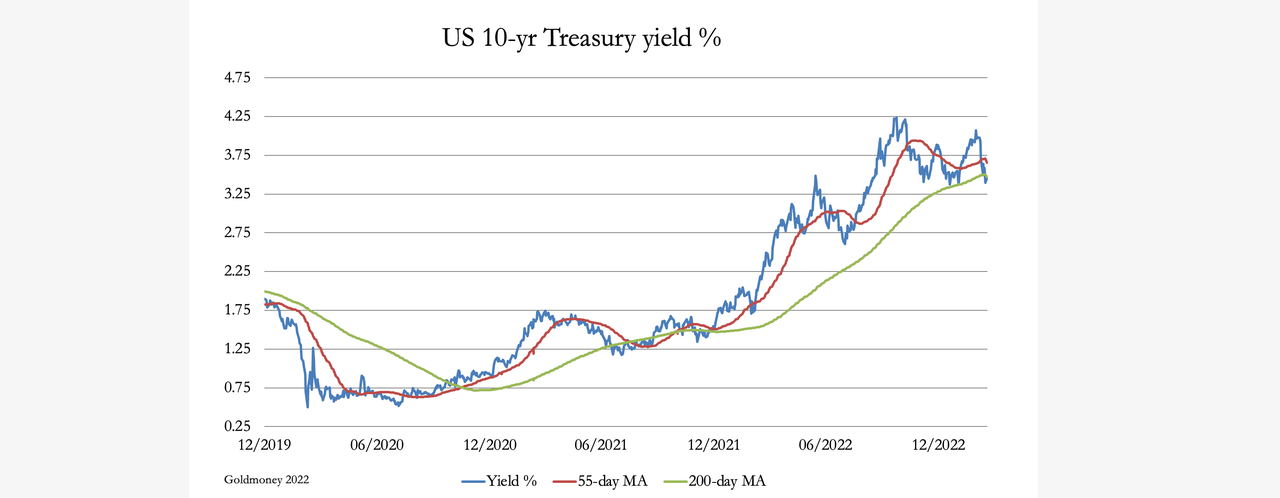

The BTFP is QE by another name, injecting credit into the banks —admitted in the Fed’s statement above. But we have seen that the Fed’s few attempts to reverse QE have always threatened the credit bubble. As soon as bankers realise that because of the history of quantitative tightening, which is what the ending of the facility will amount to, the loan terms can be regarded by them as perpetual. Any bond standing at a discount can be collateralised with the Fed at final redemption value, notwithstanding its current market value at a discount. Already, this has driven the 10-year US Treasury yield below its major moving averages, indicating further falls in yield are to come.

Clearly, this is a facility which is likely to lead to a massive and additional expansion of the Fed’s balance sheet. But by putting a one-year loan term on this facility, the Fed will feel justified in disregarding the automatic loss the BTFP facility creates on the basis that the bonds bought will simply returned to the sellers who will repay the money borrowed. It will be treated like a long-term repurchase agreement.

While we know that realistically this repo will turn out to be perpetual, purchases in the market by banks to benefit from the BTFP facility allows the Fed to reduce its losses on its existing bond holdings as their yields fall further. And importantly, the government’s deficit will continue to be funded.

The banking crisis similarly exists in other jurisdictions, so it is likely that the other major central banks will introduce their own versions of the Fed’s BTFP. All that’s required is an unhealthy dose of group-thinking that the inflation monster will retreat into its cave, and that therefore the outlook for bond yields is for them to fall. Driving this hope is the benefit to central bank balance sheets, which if their assets were properly valued currently puts them all deeply into negative equity.[vi]

If it works, the pressure will diminish on banks with bonds shown as held to maturity and the situation might become manageable. But there is still the ongoing problem of credit contraction, which is not going to go away. Can the Fed suppress bond yields by much when the real cost of borrowing, which is driven by credit contraction, continues to rise? The Fed’s BTFP looks like its final gamble.

The refuge from this credit crisis is only real money — gold.

This article attempts to explain the true state of global credit. Everything appeared to be fine, until the Fed realised it was losing control over interest rates and had to raise them from the zero bound. This was followed by other central banks, with the lone exception of the Bank of Japan. Consequently, the global credit bubble which had been inflating financial asset values over the last forty years, has now burst.

Anyone who dispassionately analyses credit conditions must come to this conclusion. Furthermore, far from being an unexpected shock, we are seeing just the start of a great unwind — a great unwind which will continue to impose mounting strains on the global banking system. Even at the first hurdle, it has become clear that the world’s leading central banks in their dollar-based credit system will do whatever they can to preserve it. This is as expected, but the consequences are that the dollar’s credibility as credit will continue to be undermined as rescue after rescue proceeds.

First it was a banking crisis, and that is just the beginning of it. Now the Fed is acting to save financial asset values, likely to be followed by the other members of the central banking cabal. Then it will be the non-financial economy, as malinvestments and over-extended consumers are exposed, leading to further banking write-offs. And finally, it will be governments themselves, faced with soaring welfare costs and collapsing tax revenues, exacerbated by foreigners no longer buying Treasuries. There is only one probable outcome: being only credit, national currencies will eventually lose their credibility.

The root of credit valuation woes is that one form of credit, being that in the hands of commercial bank creditors, depends for its value on another form of credit, being manifest in bank notes. But unbeknown to most people, a bank note is not money: it is a credit liability of a central bank. An incorporeal form of wealth is wholly dependent upon another. But as we have seen, the rottenness of the credit system is not confined to a few bad apples in the banking system. The entire contents of the credit basket are rotten, from the top down.

For individuals, there is only one escape from the inevitable destruction of the value of credit. And that is to get out of the collapsing credit system altogether. The collapse may appear slow today, but at some indefinable stage in the future, it will become sudden. It won’t be just the sceptics and cynics finding fault in the system, but the general public will lose faith in their currencies. And when they do, the point of no return has been passed.

The corporeal, as opposed to incorporeal form of credit is gold. It is credit without any counterparty. It is credit only in the sense that it is the unspent product of labour and profit. This distinction allows us to define gold as the only stable medium of exchange, or true money. Gold has been money since the end of barter. In today’s monetary system, it has been legal money since Roman coin came into existence, which according to the Roman juror Gaius was at the time of the Duodecim Tabularum, the Twelve Tables ratified by the Centuriate Assembly in 449 BC. Credit comes and goes, but gold is there for ever.

Authored by Alasdair Macleod via GoldMoney.com,

We are all now aware that the global banking system is extremely fragile. Driving bank failures is contracting credit, which in turn drives interest rates higher. Though it is not generally appreciated, central banks have failed to suppress them.

Some regional banks have failed in the US and the run on Credit Suisse’s deposits has forced the Swiss authorities into forcing a reluctant rescue by UBS. Undoubtedly, as the great credit unwind plays out, there will be more rescues to come.

In this, the earliest stages of a banking crisis, some questions are being answered. We can probably rule out bail-ins in favour of bail outs, and we can assume that nearly all banks will be rescued — they must be in order to prevent systemic contagion.

In this article I quantify the position of the global systemically important banks (the G-SIBs) and point out that the central banks which are meant to backstop them are themselves bankrupt — or rather they would be properly accounted for.

Because even a minor failure in the banking system could undermine the entire global banking system, the much heralded pivot is now here, but not in plain sight. Because central banks have lost control over interest rates, the focus on preserving the financial markets underpinning the banking system has shifted to supressing bond yields. This is why the Fed has introduced its Bank Term Funding Programme, likely to be copied in other jurisdictions.

It is Powell’s hidden pivot — his line in the sand. But it is the last desperate throw of the dice and depends entirely on inflation being transient and interest rates not rising much more.

The price of even a successful preservation of the banking system is the destruction of fiat currencies, because the bigger picture is still of the greatest credit bubble in history unwinding.

And that process has only recently started…

The great unwind accelerates

Now that everyone in finance knows that there is a banking crisis, cynicism prevails. When a central banker or treasury minister tries to reassure the public, it is disbelieved. The risk to an extremely fragile global banking system is that if disbelief in public statements spreads from financial sceptics to the wider public, the system is doomed. All credit is based on confidence and confidence alone.

It is still too early to say that confidence has been irretrievably shaken. But last weekend, UBS was unwillingly forced by the Swiss authorities into taking over Credit Suisse on a share swap, which valued the latter’s shares at about 70 centimes. That put Credit Suisse’s shares on a discount to book value of 94%. Admittedly, this figure is unreliable when deposits are running out of the door and the full value of foreign exchange derivatives are not accounted for. But it does raise a question over the valuations of all the other global systemically important European banks. And why stop there — the G-SIBs have all taken in each other’s laundry, so if one fails so might all the rest. Perhaps they should all be similarly valued.

Presumably, in their groupthink the central bankers represented by the three wise monkeys in the illustration above never thought it would come to this. After all, their regulators have frequently conducted stress tests and all major banks routinely pass them with flying colours. But as Kevin Dowd, Professor of Finance and Economics at Durham University put it in 2016 in one of his several critical reviews of bank regulation,

“The purpose of the stress testing programme should be to highlight the vulnerability of our banking system and the need to rebuild it. Instead, it has achieved the exact opposite, portraying a weak banking system as strong. This is like having a ship radar system that cannot detect an iceberg in plain view.

“As the EU banking system goes into a renewed crisis, the UK banking system is in no fit state to withstand the storm. Once contagion spreads from Italy to Germany and then to the UK, we will have a new banking crisis but on a much grander scale than 2007-08.

“The Bank of England is asleep at the wheel again, and we will be back to beleaguered banksters begging for bailouts – and the taxpayer will be ripped off yet again, but bigger this time.”

Unfortunately, it is Professor Dowd’s analysis and conclusion that have stood the test of time. And nothing, repeat nothing, has been done to alter this situation. Only last Monday, the President of the ECB proved this point by releasing the following official statement:

“I welcome the swift action and the decisions taken by the Swiss authorities. They are instrumental for restoring orderly market conditions and ensuring financial stability. The euro area banking sector is resilient, with strong capital and liquidity positions. In any case, our policy toolkit is fully equipped to provide liquidity support to the euro area financial system if needed and to preserve the smooth transmission of monetary policy.” (italics are my emphasis)[ii]

The group-thinking on stress testing is based on commonly agreed parameters between central banks and regulators for constructing stress models, and their desire to be seen discharging their duties rather than the actuality. That being the case, what we have seen in Switzerland which led to Credit Suisse being valued at only 6% of its book value is an important message not just for European bank regulation, but elsewhere as well.

Whatever their mollifying statements, the central bank groupthinkers must now be very worried. But they appear to lack coordination. The Swiss National Bank decided that as part of bailing out Credit Suisse, it would bail in higher ranking bond holders, writing off Sf17bn. That shareholders should get something while senior creditors get nothing is a travesty of company law. Following the market’s reaction, it has been swiftly denounced by regulators in Europe and London, only days after the ECB President issued the formal statement above, extoling the Swiss authorities for their actions.

The consequences of the Swiss National Bank writing off senior creditors are likely not just to impose losses on other banks which are in a fragile state themselves and can ill afford their senior debt to be traduced in this way, but to make future bond financing of banks more difficult. Furthermore, banks, insurance companies, and pension funds will be reassessing their risk exposure to all Swiss franc denominated bonds, even to the extent of impacting UBS, Credit Suisse’s rescuer.

The legal wrangling and rating downgrades probably start here, and no one comes out of it without damage to their reputations. And as already noted above, credit depends entirely on confidence. One can only assume that this will get central banks and their regulators to drop the whole bail-in concept in their attempts to ensure the survival of their commercial banking systems. Perhaps the Swiss should backtrack on their decision to save a paltry Sf17bn. We can understand and accept that Swiss banks get into trouble. But the Swiss authorities’ clumsy handling of the Credit Suisse crisis is risking its national reputation for financial probity and stability.

The broader problem is that confidence in banking is beginning to be publicly undermined. It is not just a matter of identifying the weakest links, but it is becoming a systemic problem of the widest proportions. The illusion of control by central banks is being shattered by the great credit unwind. Consequently, the policy priority is pivoting from the inflation mandate to pure survival. And as we have seen illustrated by the Swiss authorities, the scope for error is chasmic.

The G-SIB mess

Bail-in legislation was not the only G-20 response to the Lehman crisis. The Basel Committee’s third iteration of its regulations, still not fully implemented, was the Bank for International Settlement’s contribution to post-Lehman banking reform. The designation of a new category of bank, the global systemically important bank, or G-SIB, was created. G-SIBs are required to have additional capital buffers to address the systemic risks they are exposed to from international counterparties, relative to domestic regional banks.

Here are some relevant facts. At current exchange rates, total G-SIB balance sheet assets are recorded at $63,978 billion. But this is supported by only $4,444 billions of balance sheet equity, giving a ratio of assets to equity of 14.4 times. But this is not evenly spread, with the Eurozone’s seven G-SIBs averaging 19.7 times, and Japan’s three G-SIBs at 23 times. At the lower end of the scale, the US’s eight G-SIBs average 11.4 times and China’s four banks 12.0 times. All these ratios translate into unacceptable leverage when credit unwinds and interest rates increase, threatening to trigger rapidly rising levels of non-performing loans.

This is at least partially recognised in stock markets, where G-SIB shares commonly stand at significant discounts to book value. Only four out of the twenty-nine listed G-SIBs have price to book ratios greater than one. Based on last Monday’s share prices, the average price to book for Eurozone G-SIBs is a discount of 56%, for Japan 47%, for China 54%, and for the US it is only 7% bolstered by JPMorgan Chase and Morgan Stanley being the only two US banks trading at a reasonable premium to book value. There is considerable variance within these figures, but the message from the markets is clear: whatever the regulators and central banks say and despite their extra capital buffers, G-SIBs are still a risky investment.

These statistics do not tell the whole story. As we saw with the failure of Silicon Valley Bank, it was using widely adopted accounting methods to conceal losses on its bond investments. As of Dec. 31, 2022, SVB had about $120 billion in investments, primarily high quality bonds, such as US Treasuries and agency debt. According to its 10-K filed in February. the bank only had $74 billion of loans to borrowers. Therefore, its investments were significantly larger than its loans. Of the $120 billion in investments, $91 billion were classified as “held to maturity” investments and were not reported at fair value in each reporting period. Instead, they were reported at amortized cost, net of any reserves for credit losses in accordance with accounting convention.

SVB originally bought its bonds when the yield curve was positive. That is to say, the cost of short-term funding was less than the yield on the longer maturities which SVB bought. But when the Fed increased its fund rate from the zero bound, the yield curve turned sharply negative with two consequences for SVB. First, its short-term funding costs began to rise, and secondly the capital value of the bonds began to fall. Its shareholders’ capital on the balance sheet was soon wiped out, and belated attempts to rectify the situation simply broadcast SVB’s problems, leading to its demise.

It is a problem which is not confined to SVB. There will be other regional banks in the US and elsewhere which have fallen into the same trap. And it won’t be a problem restricted to regional banks. One can speculate that the incentive to buy longer maturity bonds than banks normally hold on their balance sheets was stronger in jurisdictions which imposed negative interest rates. A Eurozone or Japanese bank has had a zero or even slightly negative cost of short-term funding in their respective money markets, encouraging them to buy longer-dated government bonds. And like SVB, they will have been whipsawed by sharply rising short-term rates.

This leads us to speculate about how much of similar losses may be hidden in the entire G-SIB system. Like SVB, have they been sufficient to wipe out the notional shareholders’ capital of all the G-SIBs, which we know to be $4.444 trillion?

But this problem is not even the mother of all elephants in the room — that award goes to derivatives. The G-SIBs’ participation in regulated futures and over-the-counter derivatives is valued on their balance sheets at net mark-to-market values, which are very small fractions of their nominal values. Nevertheless, regulated futures are credit commitments for the full amounts, and should be valued as such. Options which have been sold are similarly commitments for their exercisable amounts, though bought options are not. The amounts of open interest involved at end-2022 are assessed by the Bank for International Settlements at $36,630bn for all regulated futures, and a further $43,182bn in options. These are just one side of open interest, the majority of which is bank exposure as market makers, traders, and banks acting as principals for their customers.

In OTC derivatives, foreign exchange and commodity contracts are liabilities for their full amounts, while credit swaps are not. At end-June 2022, foreign exchange contracts amounted to $109,587bn with a further $12,951bn in options. Commodity contracts add a further $2,341bn.[iii] We can exclude the large category of credit default swaps, because their gross values are purely notional. These exposures represent only one side of credit commitments, the other being distributed among non-bank financial institutions, hedgers, speculators, and other banks as well. From the G-SIBs’ collective balance sheet perspective, they should all be included at full value.

Last December, Claudio Borio, Head of the BIS’s Monetary and Economic Department even wrote a paper on this topic. Borio stated that “Foreign exchange swap positions point to over $80 trillion of hidden US dollar debt [part of the $109.587 trillion above], reported off-balance sheet”. And “The volume of daily foreign exchange turnover subject to settlement risk remains stubbornly high despite mechanisms to mitigate such risks”. In effect, Borio confirmed that for a true appreciation of global banking risk, gross OTC values for foreign exchange contracts should be recorded on both sides of bank balance sheets, and not just as net mark-to-market contract values.

Between regulated and unregulated derivatives, we are therefore staring down the barrel of a further $210 trillion of balance sheet liabilities, to be added to the $64 trillion of officially recorded total G-SIB balance sheets, all supported by only $4.444 trillion of shareholder’s funds. And while the US G-SIBs appear to be less leveraged than their opposite numbers in the Eurozone and Japan, it should be noted that as Borio points out the large majority of OTC exposure is in dollar-denominated contracts, for which the US G-SIBs are the counterparties.

If only one G-SIB fails, its counterparty risks could easily undermine all the others. As Borio pointed out, settlement risk remains stubbornly high. It explains why the Fed was ready to come up so swiftly with swap lines for the Swiss National Bank to aid it in its attempt to support Credit Suisse. And it allows us to draw a further conclusion: credit expansion at the central bank level to ensure the global financial system’s survival will place the greatest burden on the dollar, being the currency in which most of these derivative obligations are settled.

Can central banks actually handle a credit crisis?

Having invested in government and other bonds at the top of the market — a top created by them to be far higher than they would otherwise have been — central banks are now demonstrably bankrupt unless they recapitalise themselves. For all of them, excepting the ECB, it is theoretically easy to do but best done before commercial banks need their support.

The simplest way of recapitalising a central bank is by expanding its balance sheet assets in favour of equity instead of other liabilities. Delaying addressing the same problems faced by Silicon Valley Bank on the basis they need not doesn’t serve central banks well. The losses can be assumed to continue to accumulate as commercial bank credit continues to contract, because it is credit contraction which drives up the true level of interest rates. Already, the Bank of Japan has been accumulating financial assets at negative yields, so that even with a small rise on yields, its losses from last year are over four thousand times its balance sheet capital of only 100 million yen. Sooner or later, its credibility is bound to be questioned if it fails to address this issue.

But of all the central banks, the ECB is probably the most difficult to recapitalise. The ECB’s shareholders are not a single state, but the national central banks of the twenty member nations (including Croatia which joined the euro system in January). Unfortunately, with few exceptions the NCBs in the euro system are also all in need of recapitalisation.

Imagine the legislative hurdles. The Bundesbank, let’s say, presents a case to the Bundestag to pass enabling legislation to permit it to recapitalise itself and to subscribe to more capital in the ECB on the basis of its share of the ECB’s equity — the capital key — to restore it to solvency as well. One can imagine finance ministers being persuaded that there is no alternative to the proposal, but then it will be noticed by pedestrian politicians that the Bundesbank is owed over €1.1 trillion through the TARGET2 system. Surely, it will almost certainly be argued, if those liabilities were paid to the Bundesbank, there would be no need for it to recapitalise itself.

If only it were so simple. But clearly, it is not in the Bundesbank’s interest to involve politicians in monetary affairs. The public debate would risk spiralling out of control, with possibly fatal consequences for the entire euro system. It would be a row at the worst possible time. And with twenty NCB shareholders facing similar hurdles, their contributions to refinancing the ECB requires unanimous consent for proportional subscriptions in accordance with their capital keys.

Besides the confusion over bail-ins and bail outs which we can now hope has been settled, there still remains a huge question mark over whether the central banks have the wherewithal to discharge the potentially enormous burden of bail out commitments. In any event, it will need massive quantities of additional central bank credit in all relevant currencies to backstop the system. The destruction to balance sheets at both central and commercial bank levels reinforces the point, that central banks are likely to move their attention away from short-term interest rates over which they have lost control to bond yields which they can still influence. Different versions of the Fed’s Bank Term Funding Programme (more on which follows) are likely to be devised. It is becoming a hidden pivot.

The hidden pivot

In a classic banking crisis, bank balance sheets become overextended and bankers become cautious in their lending, restricting the expansion of credit. The credit shortage leads to higher interest rates for the few borrowers deemed creditworthy and able to pay them. Both producers and consumers are affected. The shortage of credit and higher borrowing costs result in businesses failing, and a slump in economic activity follows. This leads in turn to the problem identified by Irving Fisher, which he described as his debt-deflation theory.[iv] According to Fisher, when the cycle of bank lending turns down and higher interest rates and falling collateral values follow, it forces banks to call in loans, liquidating collateral and driving colateral values down further. The self-feeding nature of this phenomenon deepens the slump and leads to banking failures.

Fisher’s paper was published in the wake of record numbers of bank failures in America between 1930—1933. And it should also be noted that it has informed every state economist ever since. The fear of a slump exacerbated by collateral liquidation is in the back of every mainstream economist’s mind. But so far, there has been not much evidence of credit shortages undermining the non-financial economy. Presumably, the downturns in credit expansion reflected in broad money supply statistics have reflected banks withdrawing from financial activities, so the hit to non-financial activity is yet to come. But the issue of falling collateral values identified by Fisher has resurfaced in problems created by policy makers themselves, because the sudden rise in interest rates has had the same effect.

This is why we are now witnessing central banks pivoting from control of inflation to the preservation of the global commercial banking system. The danger of systemic failure is more hardwired into central bankers’ DNA than that of inflation. And frankly, they have proved pretty clueless on interest rate management anyway. They are set to do “whatever it takes” to preserve both financial market values and the status quo. But things have moved on from Mario Draghi’s famous aphorism. No longer just a finger-wagging threat, whatever it takes is likely to end up undermining the purchasing power of currencies. Whatever it takes is now an open-ended commitment to whatever it costs.

There can be no question that pivoting from fear of inflation to fear of a banking crisis undermines currencies. But central bankers appear to find it difficult to concede it publicly. The Fed’s solution is to offer to take in all US Treasuries, agency debt, mortgage-backed securities, and “other qualifying assets as collateral” at par with no haircut against cash liquidity for one year. Furthermore, with foreigners no longer net buyers of Treasuries, there is a funding problem to address.

The Fed stated that its new bank term funding programme (BTFP)

“…will make available additional funding to eligible depository institutions to help assure banks have the ability to meet the needs of all their depositors. This action will bolster the capacity of the banking system to safeguard deposits and ensure the ongoing provision of money and credit to the economy. The Federal Reserve is prepared to address any liquidity pressures that may arise.”

It is a policy that might have been scripted by Irving Fisher’s ghost. The one-year term of the facility shows that the Fed regards this as a temporary problem to be reversed when the situation improves, and inflation returns towards its two per cent target. Yes, all the forecasts are still for inflation to be transient — only it is taking just a little longer than originally thought.

The BTFP is QE by another name, injecting credit into the banks —admitted in the Fed’s statement above. But we have seen that the Fed’s few attempts to reverse QE have always threatened the credit bubble. As soon as bankers realise that because of the history of quantitative tightening, which is what the ending of the facility will amount to, the loan terms can be regarded by them as perpetual. Any bond standing at a discount can be collateralised with the Fed at final redemption value, notwithstanding its current market value at a discount. Already, this has driven the 10-year US Treasury yield below its major moving averages, indicating further falls in yield are to come.

Clearly, this is a facility which is likely to lead to a massive and additional expansion of the Fed’s balance sheet. But by putting a one-year loan term on this facility, the Fed will feel justified in disregarding the automatic loss the BTFP facility creates on the basis that the bonds bought will simply returned to the sellers who will repay the money borrowed. It will be treated like a long-term repurchase agreement.

While we know that realistically this repo will turn out to be perpetual, purchases in the market by banks to benefit from the BTFP facility allows the Fed to reduce its losses on its existing bond holdings as their yields fall further. And importantly, the government’s deficit will continue to be funded.

The banking crisis similarly exists in other jurisdictions, so it is likely that the other major central banks will introduce their own versions of the Fed’s BTFP. All that’s required is an unhealthy dose of group-thinking that the inflation monster will retreat into its cave, and that therefore the outlook for bond yields is for them to fall. Driving this hope is the benefit to central bank balance sheets, which if their assets were properly valued currently puts them all deeply into negative equity.[vi]

If it works, the pressure will diminish on banks with bonds shown as held to maturity and the situation might become manageable. But there is still the ongoing problem of credit contraction, which is not going to go away. Can the Fed suppress bond yields by much when the real cost of borrowing, which is driven by credit contraction, continues to rise? The Fed’s BTFP looks like its final gamble.

The refuge from this credit crisis is only real money — gold.

This article attempts to explain the true state of global credit. Everything appeared to be fine, until the Fed realised it was losing control over interest rates and had to raise them from the zero bound. This was followed by other central banks, with the lone exception of the Bank of Japan. Consequently, the global credit bubble which had been inflating financial asset values over the last forty years, has now burst.

Anyone who dispassionately analyses credit conditions must come to this conclusion. Furthermore, far from being an unexpected shock, we are seeing just the start of a great unwind — a great unwind which will continue to impose mounting strains on the global banking system. Even at the first hurdle, it has become clear that the world’s leading central banks in their dollar-based credit system will do whatever they can to preserve it. This is as expected, but the consequences are that the dollar’s credibility as credit will continue to be undermined as rescue after rescue proceeds.

First it was a banking crisis, and that is just the beginning of it. Now the Fed is acting to save financial asset values, likely to be followed by the other members of the central banking cabal. Then it will be the non-financial economy, as malinvestments and over-extended consumers are exposed, leading to further banking write-offs. And finally, it will be governments themselves, faced with soaring welfare costs and collapsing tax revenues, exacerbated by foreigners no longer buying Treasuries. There is only one probable outcome: being only credit, national currencies will eventually lose their credibility.

The root of credit valuation woes is that one form of credit, being that in the hands of commercial bank creditors, depends for its value on another form of credit, being manifest in bank notes. But unbeknown to most people, a bank note is not money: it is a credit liability of a central bank. An incorporeal form of wealth is wholly dependent upon another. But as we have seen, the rottenness of the credit system is not confined to a few bad apples in the banking system. The entire contents of the credit basket are rotten, from the top down.

For individuals, there is only one escape from the inevitable destruction of the value of credit. And that is to get out of the collapsing credit system altogether. The collapse may appear slow today, but at some indefinable stage in the future, it will become sudden. It won’t be just the sceptics and cynics finding fault in the system, but the general public will lose faith in their currencies. And when they do, the point of no return has been passed.

The corporeal, as opposed to incorporeal form of credit is gold. It is credit without any counterparty. It is credit only in the sense that it is the unspent product of labour and profit. This distinction allows us to define gold as the only stable medium of exchange, or true money. Gold has been money since the end of barter. In today’s monetary system, it has been legal money since Roman coin came into existence, which according to the Roman juror Gaius was at the time of the Duodecim Tabularum, the Twelve Tables ratified by the Centuriate Assembly in 449 BC. Credit comes and goes, but gold is there for ever.

Loading…