A slightly-more-dovish-than-normal Atlanta Fed president did nothing to stop the 'good' jobs data sparking a pukefest across bonds and stocks. Crypto was lower, gold and the dollar were only marginally changed (as it looked like Japan's MoF stepped in to save the yen). VIX topped 20, and Treasury yields all soared to multi-decade highs.

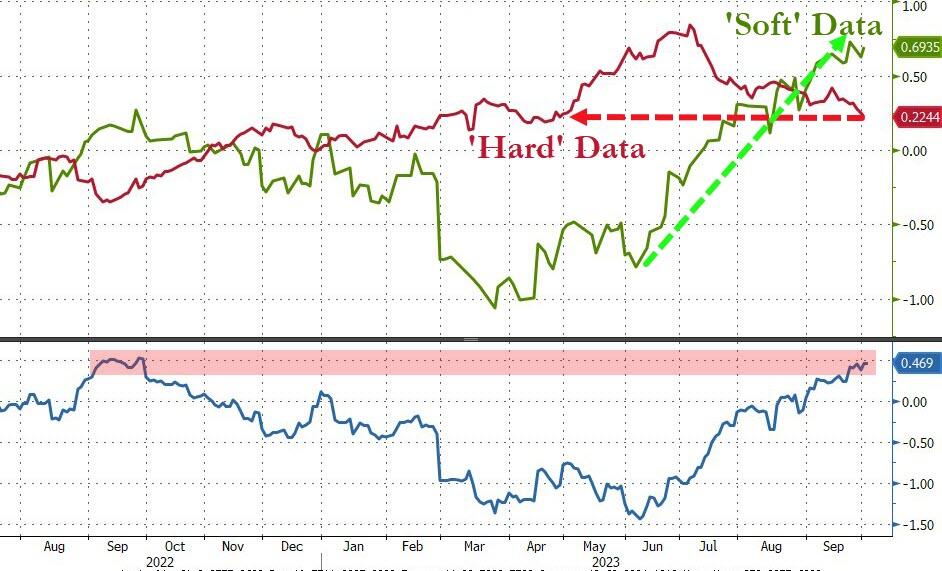

The survey-driven JOLTS data sent 'soft' data to a new cycle high while 'hard' data is at its lowest since April...

Source: Bloomberg

But, Financial Conditions are tightening aggressively...

Source: Bloomberg

Goldman warns that the 'good news' faces a few headwinds may impact growth soon, including the end of the student loan moratorium, a potential slowdown in consumer spending after a very strong summer, and higher oil prices among others - all of which could weigh on at least the willingness if not just the ability of the consumer to spend.

How bad could it get? Goldman estimates that real GDP growth will slow from 3.5% in Q3 to 0.7% in Q4

Futures were drifting lower into the cash open, saw the ubiquitous opening pump, but soon after came the JOLTS data which sent everything lower with Nasdaq leading the plunge...

The S&P is falling close to its 200DMA...

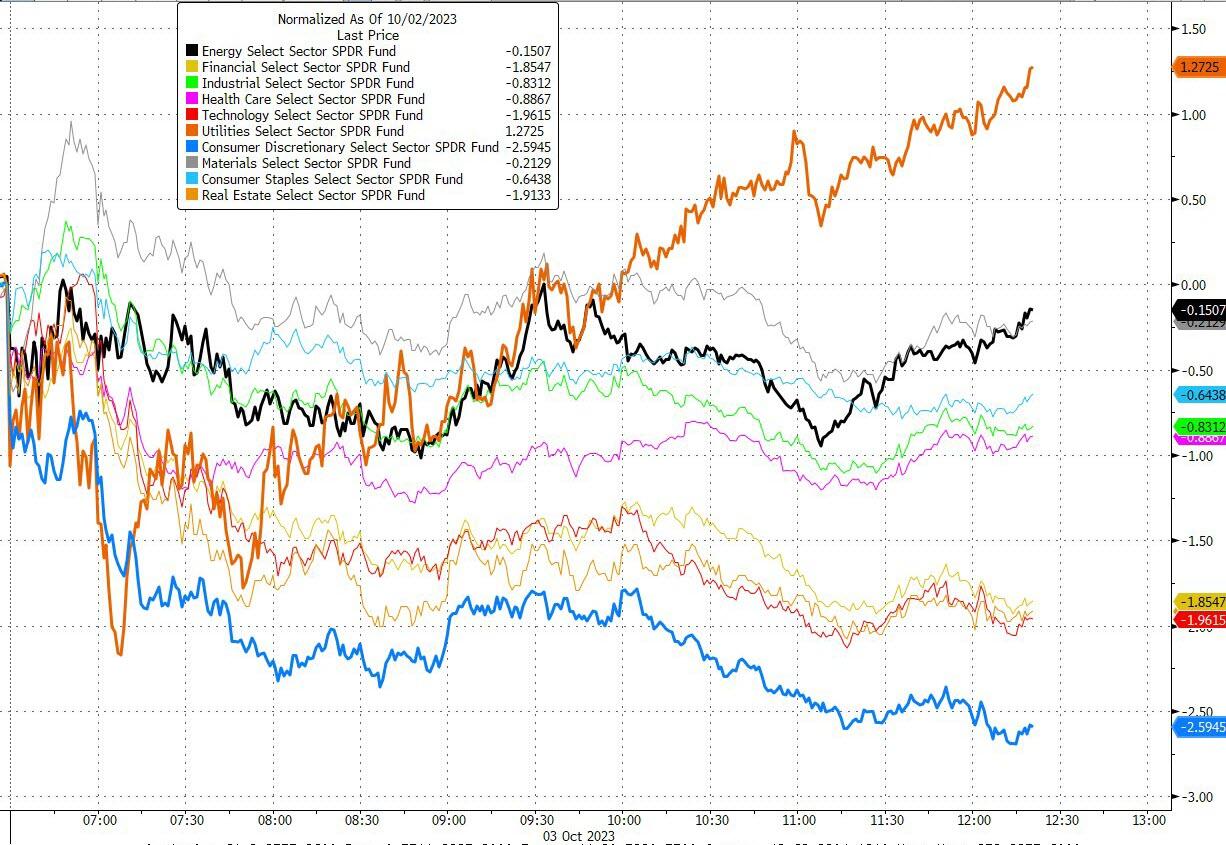

After its collapse yesterday, Utilities were the only sector green today. Energy almost got back to even on the day but Consumer Discretionary was the ugliest horse in the glue factory...

Source: Bloomberg

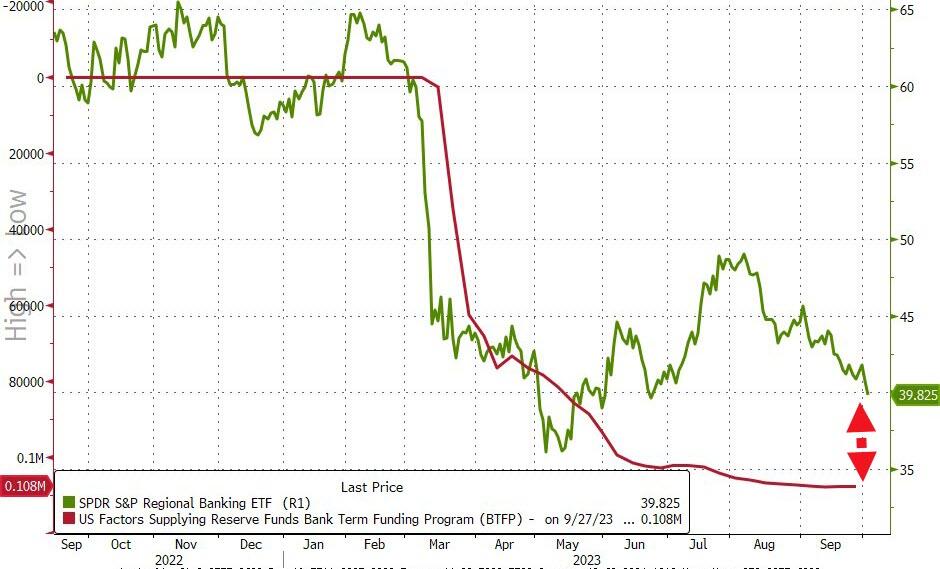

Banks continue to be a shitshow (should not be surprising given the $108BN hole in their balance sheets... that is getting worse with every tick higher in yields)...

Further to fall...

Selling was focused on unprofitable tech...

Source: Bloomberg

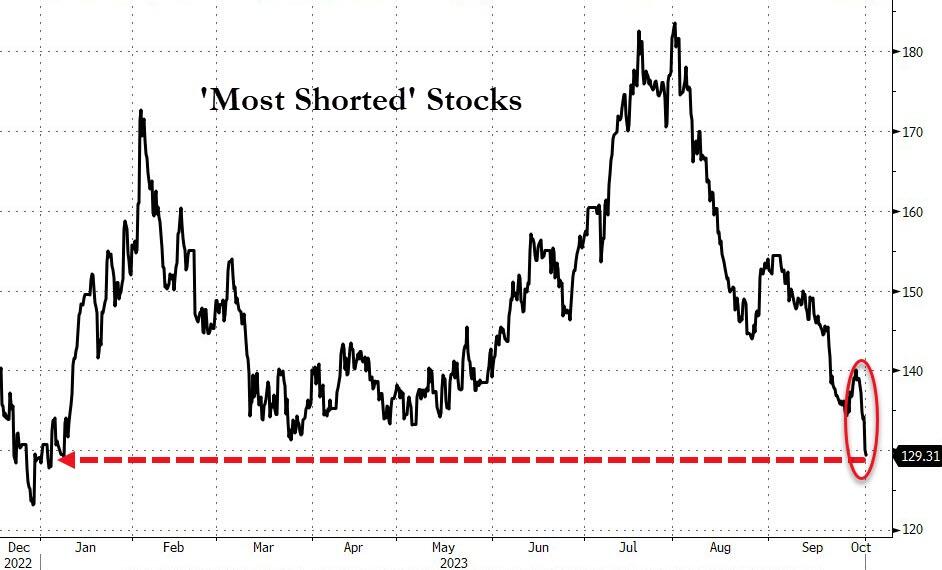

And "most shorted" stocks are now in the red for the year after today's puke...

Source: Bloomberg

...oh and don't forget the recent IPOs - CART'd out!

0-DTE traders bought the f**king dip early on (heavy call-buying) but it didn't work to spark any real positive momentum and the unwind dragged stocks to the lows of the day...

Source: SpotGamma

Treasuries were clubbed like a baby seal... again... with the long-end absolutely hammered (30Y +16bps, 2Y +4bps)...

Source: Bloomberg

30Y neared 4.95% (2007 highs) as the yield curve (2s30s) bear-steepened dramatically...

Source: Bloomberg

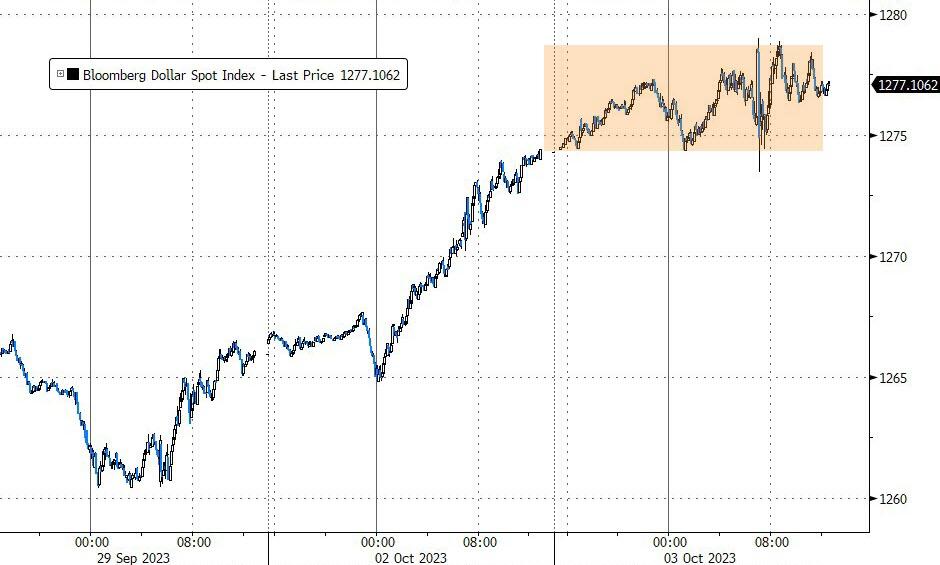

The dollar ended higher - but not much so - thanks in large part to JPY's move...

Source: Bloomberg

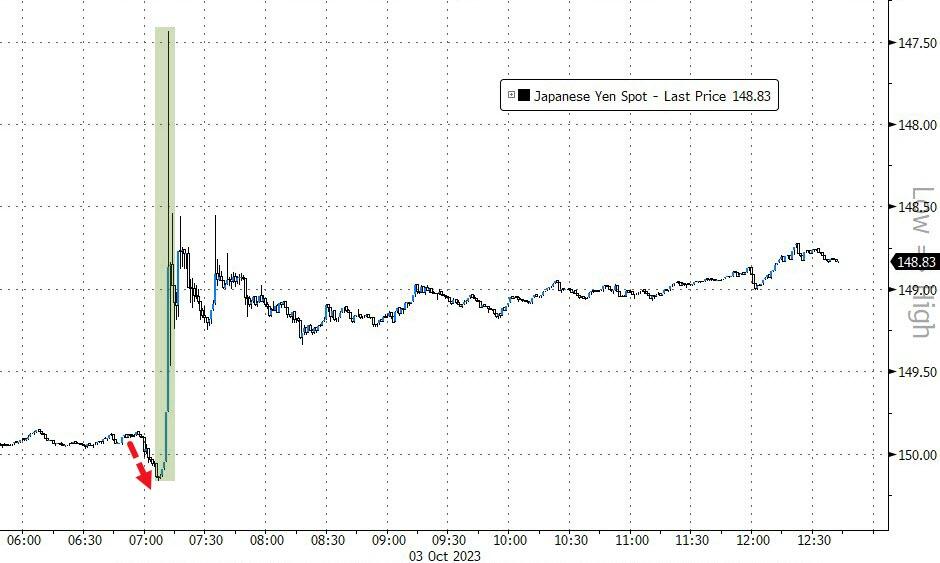

What looked like an intervention by Japan's MoF saved the day's volatility in the FX market. JPY's break above 150/USD seemed to trigger a massive wave of yen-buying...

Source: Bloomberg

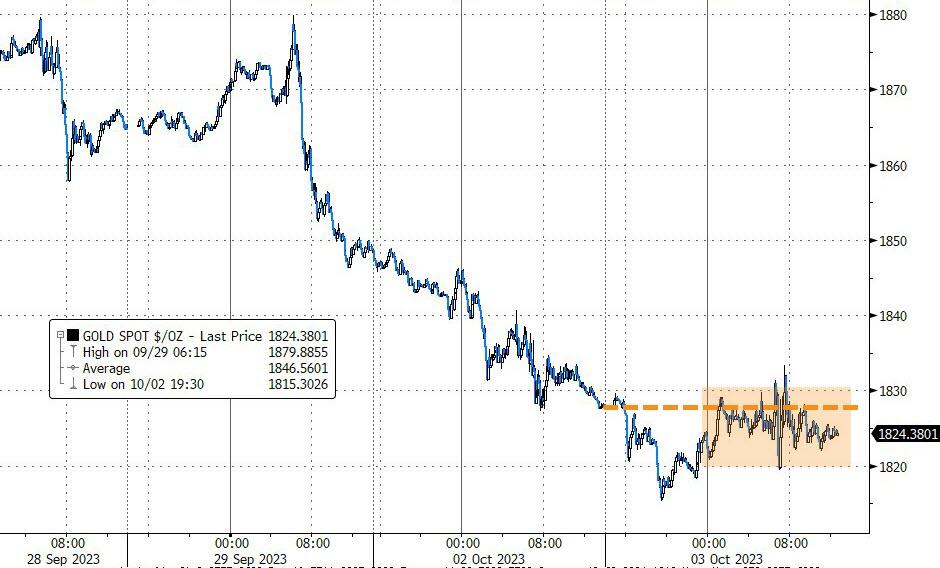

Gold ended the day only marginally lower

Source: Bloomberg

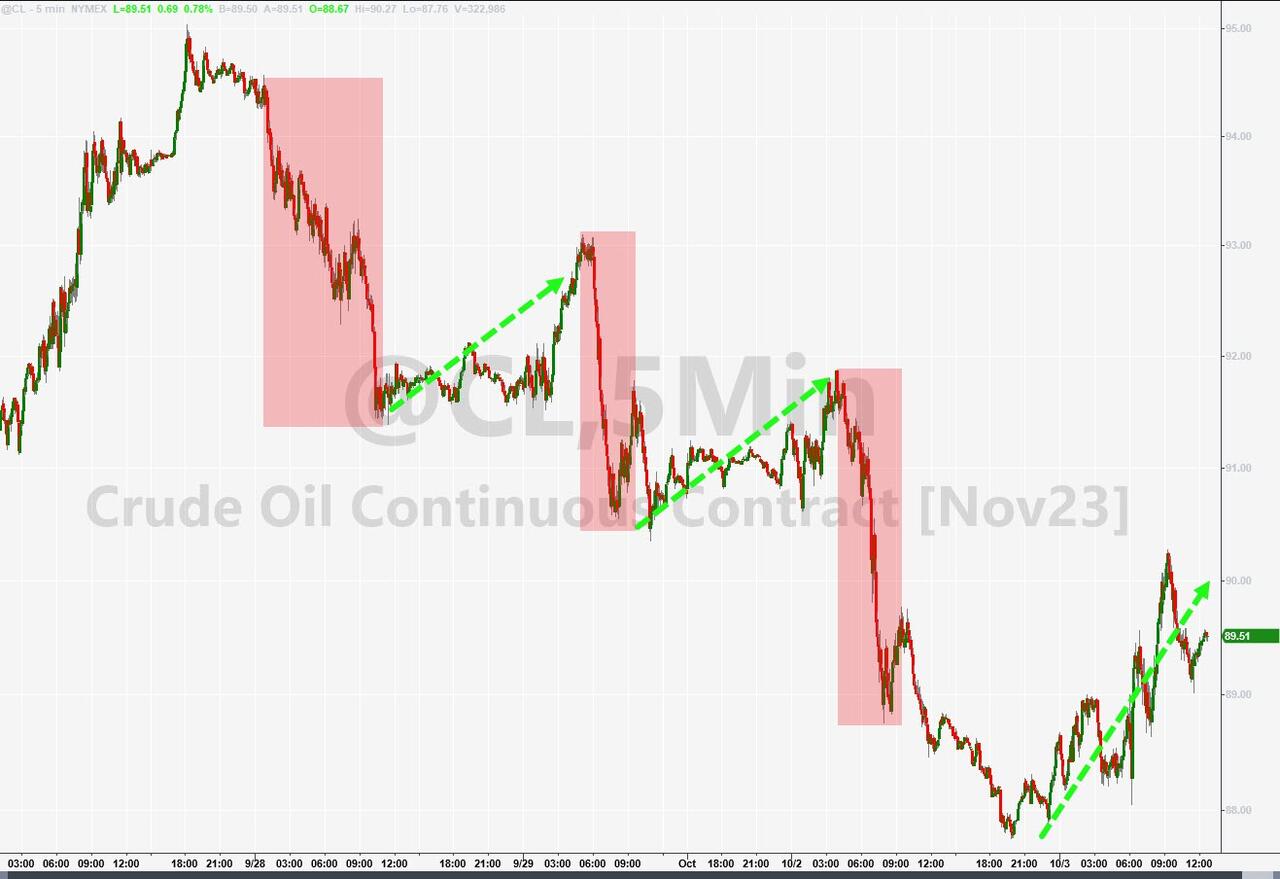

Crude managed gains on the day, with WTI bouncing back above $90 briefly intraday...

Finally, we just tumbled into 'Extreme Fear' levels...

And the other fear index - VIX - soared back above 20 - its first time since May...

..which perfectly fits with the seasonals...

Source: Bloomberg

...but are we done now?

A slightly-more-dovish-than-normal Atlanta Fed president did nothing to stop the ‘good’ jobs data sparking a pukefest across bonds and stocks. Crypto was lower, gold and the dollar were only marginally changed (as it looked like Japan’s MoF stepped in to save the yen). VIX topped 20, and Treasury yields all soared to multi-decade highs.

The survey-driven JOLTS data sent ‘soft’ data to a new cycle high while ‘hard’ data is at its lowest since April…

Source: Bloomberg

But, Financial Conditions are tightening aggressively…

Source: Bloomberg

Goldman warns that the ‘good news’ faces a few headwinds may impact growth soon, including the end of the student loan moratorium, a potential slowdown in consumer spending after a very strong summer, and higher oil prices among others – all of which could weigh on at least the willingness if not just the ability of the consumer to spend.

How bad could it get? Goldman estimates that real GDP growth will slow from 3.5% in Q3 to 0.7% in Q4

Futures were drifting lower into the cash open, saw the ubiquitous opening pump, but soon after came the JOLTS data which sent everything lower with Nasdaq leading the plunge…

The S&P is falling close to its 200DMA…

After its collapse yesterday, Utilities were the only sector green today. Energy almost got back to even on the day but Consumer Discretionary was the ugliest horse in the glue factory…

Source: Bloomberg

Banks continue to be a shitshow (should not be surprising given the $108BN hole in their balance sheets… that is getting worse with every tick higher in yields)…

Further to fall…

Selling was focused on unprofitable tech…

Source: Bloomberg

And “most shorted” stocks are now in the red for the year after today’s puke…

Source: Bloomberg

…oh and don’t forget the recent IPOs – CART’d out!

0-DTE traders bought the f**king dip early on (heavy call-buying) but it didn’t work to spark any real positive momentum and the unwind dragged stocks to the lows of the day…

Source: SpotGamma

Treasuries were clubbed like a baby seal… again… with the long-end absolutely hammered (30Y +16bps, 2Y +4bps)…

Source: Bloomberg

30Y neared 4.95% (2007 highs) as the yield curve (2s30s) bear-steepened dramatically…

Source: Bloomberg

The dollar ended higher – but not much so – thanks in large part to JPY’s move…

Source: Bloomberg

What looked like an intervention by Japan’s MoF saved the day’s volatility in the FX market. JPY’s break above 150/USD seemed to trigger a massive wave of yen-buying…

Source: Bloomberg

Gold ended the day only marginally lower

Source: Bloomberg

Crude managed gains on the day, with WTI bouncing back above $90 briefly intraday…

Finally, we just tumbled into ‘Extreme Fear’ levels…

And the other fear index – VIX – soared back above 20 – its first time since May…

..which perfectly fits with the seasonals…

Source: Bloomberg

…but are we done now?

Loading…