By Ye Xie and Amy Li, Bloomberg Markets Live reporter and strategists

The sovereign wealth fund’s investment in the big banks shows that Beijing is committed to putting a floor under the stock market.

The purchase is limited in size, but the signaling effect could be more important. Unfortunately, the signaling effect works only if investors believe that the National Team has deep pockets to keep buying the dip. The reality is that the cash pile at Central Huijin Investment Ltd. is dwindling fast.

Chinese equity markets responded positively to the news that Huijin bought about $65 million of shares in the four largest Chinese banks, and pledged to increase holdings over the next six months.

It fits the historical pattern where intervention by the state fund tended to support the market in the short term, as this column noted yesterday. But history also shows these actions alone won’t be able to sustain the market over time.

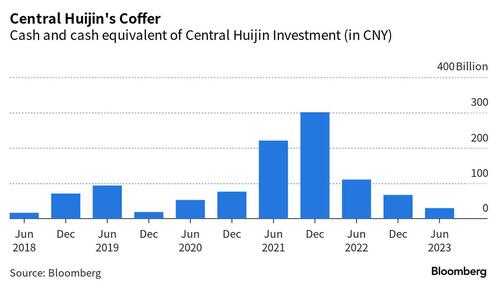

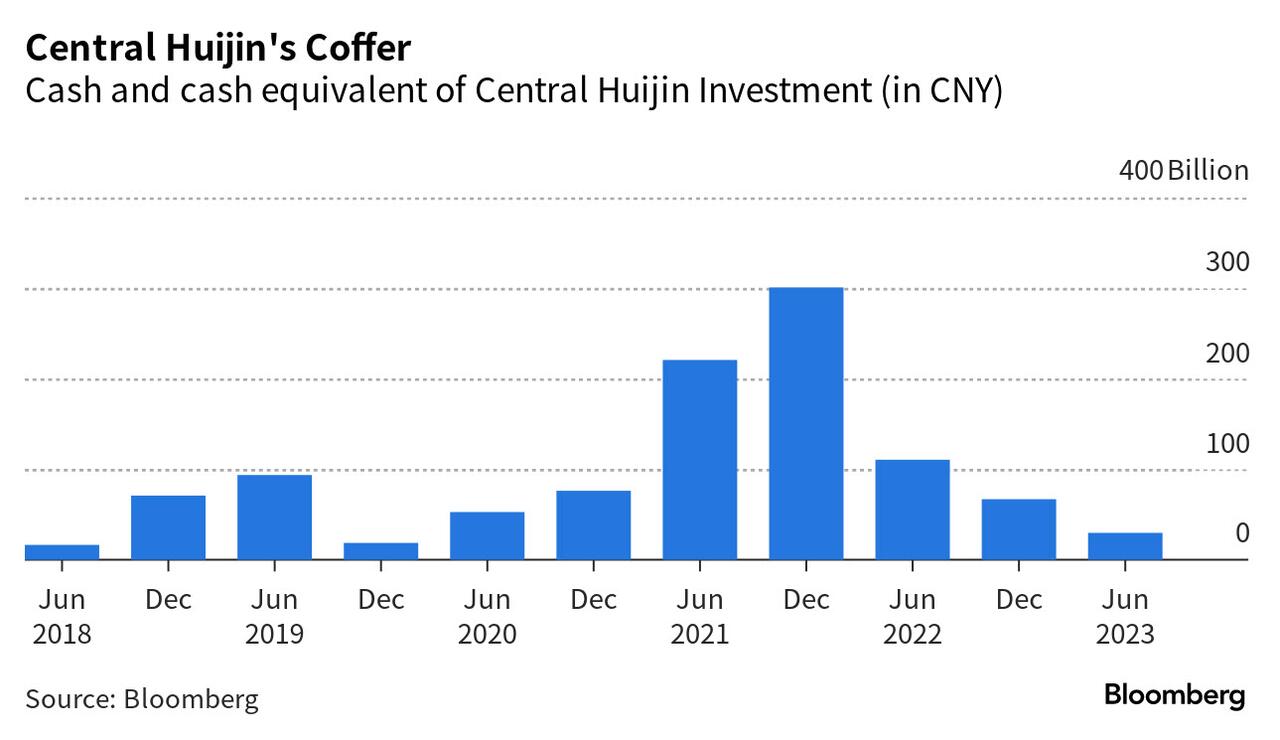

The sovereign wealth fund could be formidable if it has unlimited fire power. That’s not the case, though. Huijin has been burning through its cash over the past two years. Cash and cash equivalents have declined to 30 billion yuan ($4.1 billion) as of June, from a peak of 301 billion in 2021.

The cash has been used to pay dividends and interest to the fund’s shareholders — i.e. the government. Presumably, it was to help fund the cash-pinched government as the economy slowed.

Ultimately, to rejuvenate the market, the economy and corporate earnings growth need to pick up. And there’s not much the National Team can do to help with that.

By Ye Xie and Amy Li, Bloomberg Markets Live reporter and strategists

The sovereign wealth fund’s investment in the big banks shows that Beijing is committed to putting a floor under the stock market.

The purchase is limited in size, but the signaling effect could be more important. Unfortunately, the signaling effect works only if investors believe that the National Team has deep pockets to keep buying the dip. The reality is that the cash pile at Central Huijin Investment Ltd. is dwindling fast.

Chinese equity markets responded positively to the news that Huijin bought about $65 million of shares in the four largest Chinese banks, and pledged to increase holdings over the next six months.

It fits the historical pattern where intervention by the state fund tended to support the market in the short term, as this column noted yesterday. But history also shows these actions alone won’t be able to sustain the market over time.

The sovereign wealth fund could be formidable if it has unlimited fire power. That’s not the case, though. Huijin has been burning through its cash over the past two years. Cash and cash equivalents have declined to 30 billion yuan ($4.1 billion) as of June, from a peak of 301 billion in 2021.

The cash has been used to pay dividends and interest to the fund’s shareholders — i.e. the government. Presumably, it was to help fund the cash-pinched government as the economy slowed.

Ultimately, to rejuvenate the market, the economy and corporate earnings growth need to pick up. And there’s not much the National Team can do to help with that.

Loading…