The Quiet Coup Part II

In 2009, the year after the great financial crisis, Simon Johnson published a memorable piece in The Atlantic, entitled “The Quiet Coup.” Johnson, a former chief economist of the International Monetary Fund, described the scandalous process by which financiers “played a central role in creating the crisis, making ever-larger gambles, with the implicit backing of the government, until the inevitable collapse.”

These words might seem familiar today, as we ponder a new scandal: the open-ended bailouts of depositors at Silicon Valley Bank (SVB) and Signature Bank, which former Treasury Secretary Larry Summers suggests has already cost each American adult $100 and counting, making it a tax increase by a different name. And, of course, we’re all still worrying about the next bank(s) to drop.

Simon Johnson article from the May 2009 issue of The Atlantic.

In his essay, Johnson noted that in the 1970s and 1980s, the U.S. financial sector never gained more than 16 percent of domestic corporate profits. But then, thanks to deregulation and deindustrialization — with banks often playing arbitrageur, helping to move factories and other assets offshore — finance profits started rising as a share of the total. In the decade of the 2000s, they reached a whopping 41 percent, meaning that more than two-fifths of American profits for anything were in finance. That money-surge paid for a lot of rich blue dots, for greater Democratic political power, and, of course, for plenty of wokeness. For his part, Johnson zeroed in on telling details:

Stanley O’Neal, the CEO of Merrill Lynch, pushed his firm heavily into the mortgage-backed-securities market at its peak in 2005 and 2006 … O’Neal took home a $14 million bonus in 2006; in 2007, he walked away from Merrill with a severance package worth $162 million.

The ultimate problem with the banks and finance houses, Johnson concluded, was their gargantuan scale: “Oversize institutions disproportionately influence public policy; the major banks we have today draw much of their power from being too big to fail.”

From left to right: Charles Prince and Richard Parsons of Citigroup, Stanley O’Neal of Merrill Lynch, John Finnegan of Amgen, and Angelo Mozilo and Harley W. Snyder of Countrywide are sworn in to testify before a House Oversight and Government Reform hearing on March 7, 2008, to examine the compensation given to the CEOs of corporations involved in the mortgage crisis. (Mark Wilson/Getty Images)

So, that was then. What’s happening now with the banks? Has anything really changed?

The seamy details — all that weird wokeness combined with carelessness about basic banking —involved in the failure of Silicon Valley Bank and Signature Bank are still spilling out. Yet the eminent financial historian Roger Lowenstein has seen enough already.

In a March 15 op-ed entitled, “The Silicon Valley Bank Rescue Just Changed Capitalism,” Lowenstein called attention to the federal government’s declaration that it would cover all deposits, even those way over the financial cap, set in law, of $250,000. Indeed, The Wall Street Journal reported on March 27 that that ten depositors had a total of $13.3 billion in SVB. So yeah, you can bet that those depositors worked really hard to get covered. (And it’s a safe bet, too, that plenty of them were Democratic donors — and not small donors.)

Wrote Lowenstein of such special treatment, “This is a breathtaking leap.” That is, a leap toward Uncle Sam covering everyone and everything all at once, no matter how egregious. But that’s not a good way to run a banking system. The historian continued:

The first plank of capitalism is that it entails risk. You cannot sensibly invest without assessing the chance for loss. If venture firms relied on groupthink rather than financial due diligence, that was their doing. In the case of Signature, which was exposed to the crypto industry, the rescue probably bailed out gamblers on speculative assets.

Those last words, “gamblers on speculative assets,” remind us of what Simon Johnson wrote 14 years ago about financiers “making ever-larger gambles, with the implicit backing of the government.”

Maybe they’re right when they say, the more things change, the more they stay the same. And so Quiet Coup I begets Quiet Coup II.

Sen. Lankford Defends Oklahoma

In the meantime, of course, if the insiders are winning by gaming the system, that means the outsiders — namely, regular folks who play by the rules — are losing.

The astute blog Unusual Whales noticed right away who was losing. On March 15, it noted, “Bank of America benefited from Silicon Valley Bank’s collapse as it received over $15 billion in new deposits.” The blog noted that depositors were pulling out of small and mid-sized banks, moving their funds to the largest banks.

Customers wait in line outside of a Silicon Valley Bank branch in Wellesley, Massachusetts, 0n March 13, 2023, following the bank’s collapse. (Sophie Park/Bloomberg via Getty Images)

Why was this happening? Evidence suggests that it’s not because the bigs are better run. Instead, it’s because the bigs are defined by the federal government as “Systemically Important Financial Institutions” (SIFI). That SIFI status means that these banks are going to be fully bailed out, including their depositors, no matter how supersized.

At the same time, nobody knows what would happen in the case of depositors in a Systemically Unimportant Financial Institution. Who will go to bat for some small bank in Flyover Country which, unlike Signature Bank, has no former Democratic Congressman and chairman of the House Committee on Financial Services sitting on its board of directors?

So, the depositor in the small bank might think: Why take the risk? Why not move my deposit to a big bank and be 100 percent safe, even if my deposit exceeds $250,000? After all, we’ve learned that the cap doesn’t apply to the connected.

French satirical Illustration from 1908 showing a run on the bank as panicked savers demand their cash. (Universal History Archive/Universal Images Group via Getty Images)

The money movement, from small to big, has accelerated. As Breitbart News reported, a whopping $120 billion fled small banks in a single week. That’s a virtual bank run of money exiting Main Street and entering the top five banks, which gained $67 billion. If you want an example of policy manipulation helping the rich to get richer, this is about as good as it gets.

One who views this cash exodus with alarm is Oklahoma Sen. James Lankford (R), a member of the Senate Finance Committee. In a hearing on March 16, Lankford challenged Treasury Secretary Janet Yellen to pledge that smaller banks would get the same guarantees as larger banks, such as Silicon Valley Bank:

Lankford: “Will every community bank . . . get the same treatment as SVB?”

Yellen: “Banks only get the treatment if . . . the failure to protected uninsured depositors would create systemic risk.”

Lankford responded that the Biden administration’s approach — a for-sure bailout for the big (SVB was the sixteenth largest bank in the nation), but not-so-sure for the small — would “accelerate” the flight from banks in his state.

Lankford summed up administration policy as “saying to our community banks, ‘We’re not going to make you whole, but if you go to one of our preferred banks, we will make you whole.’”

When Yellen started to mumble around in response, Lankford shot back, “It’s happening right now.”

[embedded content]

A few days later on Fox Business, the Oklahoma lawmaker said of the federal bank insurers:

They’re not going to be in small-town Oklahoma … They’re not going to cover the deposits of a local church or convenience store … They’re setting up a system where if you’re friends with someone at the FDIC and you’re one of their preferred relationships, we’re going to cover all your deposits; and if we don’t know you, if you’re somewhere out there in the nether land, we’re not going to cover you. It’s a terrible system for the United States, and it’s gong to destroy a lot of our community banks.

No amount of clean up work will cover up that this administration is putting billionaires before community banks. pic.twitter.com/dYliKAQsw7

— Sen. James Lankford (@SenatorLankford) March 22, 2023

Needless to say, the Biden administration doesn’t admit to this discrimination, even as its policies confess it loudly. Indeed, in the mind of some Democrats, the money flow from red zones to blue dots could be regarded as a feature, not a bug. (Why not defund Republicans and the Republican Party?) Lankford is blunt: “No amount of clean-up work will cover up that this administration is putting billionaires before community banks.”

Fair-minded Democrats, too, see the problem. For instance, Rep. Ro Khanna (D-CA) says, “I’m concerned about the danger to regional banking and community banking in this country. This should be deeply concerning, that our regional banks are losing deposits, and losing the ability to lend.”

In fact, the erosion of small banks has been a long-term trend. According to one group, “Two-thirds of banking institutions have disappeared since the early 1980s — declining from nearly 18,000 in 1984 to fewer than 5,000 in 2021.” In the meantime, the share of total assets held by the five largest banks has risen from 28 percent in 2000 to 46 percent in 2020. That’s an oligopoly, fully on par for oligarchs.

Indeed, given all the changes we’ve seen since, it seems likely that when newer numbers are available, they will show that the top-five concentration has further increased. In fact, there’s still substantial pressure from the top — “the top” being defined as Bloomberg News, that liberal-industrial complex of blue-state opinion formation — to have even fewer banks. (Alfredo Ortiz, a familiar figure to Breitbart News readers, co-authored a vigorous defense of small banks here.)

So what to do? Can we find a way to pump fiscal health back into places where capital has been drained away? Keep America from being at the mercy of just a few big banks?

The answer is, Yes we can. How do we know? Because it’s been done before.

Lessons from History: Why Regional Banks Are Needed to Protect Regional Interests

Sen. Lankford has been a worthy champion of his state’s financial interests, but it’s worth recalling that Sooners have long understood that they risk getting the short end of the banking stick. That’s been true for the entire 126 years of Oklahoma’s existence, even as the state has shifted from predominantly Democratic to overwhelmingly Republican. (In 2020, Donald Trump won the state by 33 points, carrying all 77 counties, and Republicans hold all federal and statewide offices.)

Still, it’s been rightly said: People don’t have permanent allies, but they do have permanent interests. The farmers, ranchers, drillers, and all the others with businesses and jobs in Oklahoma need steady credit. And the flow of credit is best assured by a close-in financial ecosystem knowledgeable about local conditions.

Yet, unfortunately, for Oklahoma — and for all other states with a similar producerist economic profile — it’s a recognized phenomenon that big banks in “money centers” have a way of vacuuming up wealth from the provinces, especially if there’s a central bank involved.

Why? One reason is that in peacetime, returns to capital are typically higher than returns to other kinds of economic activity. It’s easier to make money with money — to be a trader, as opposed to a maker. And if you can be a speculator and get bailed out if need be, well, that’s the easiest of all.

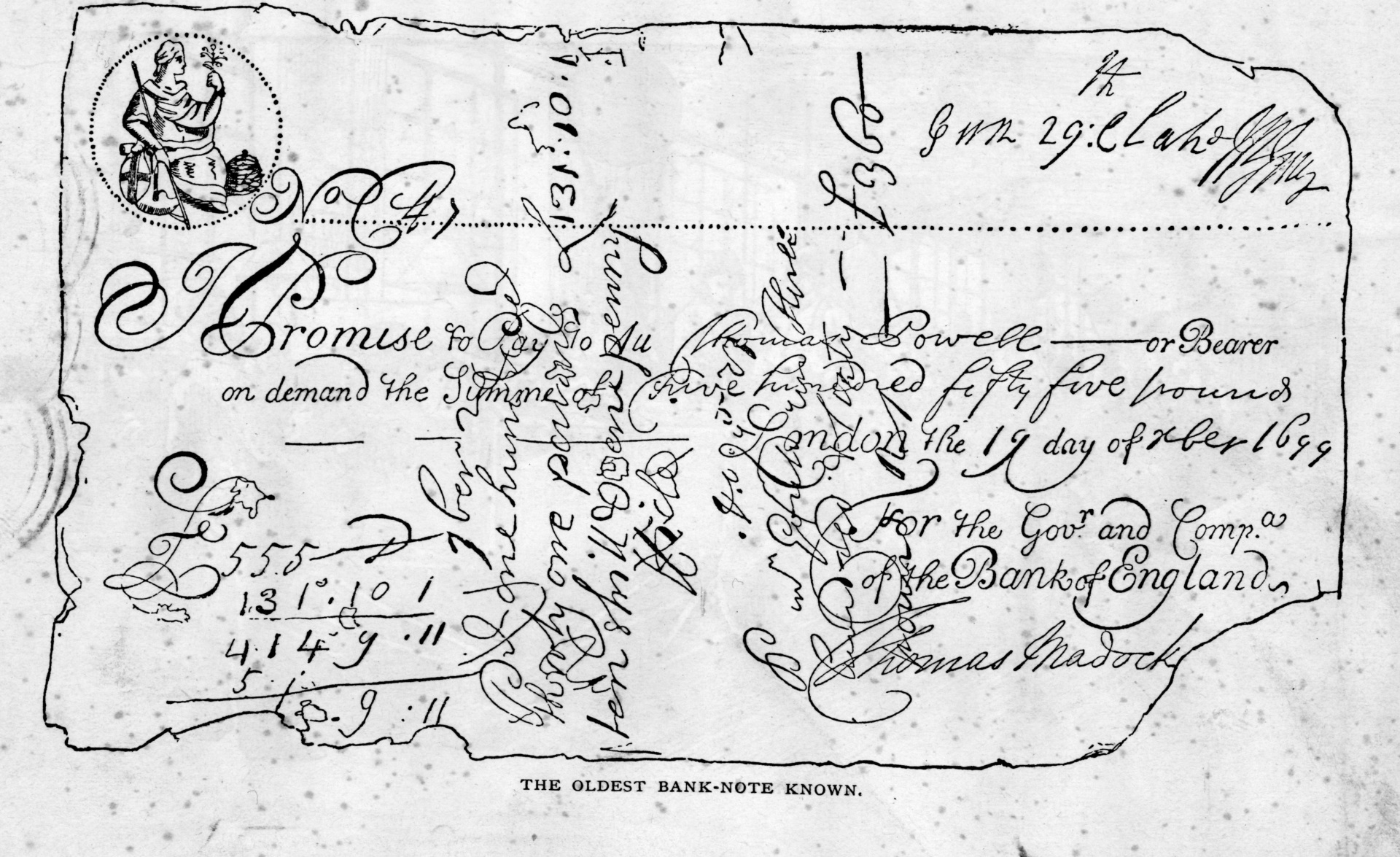

To cite one of many historical examples, we can look to London, where the Bank of England was established in 1694. In the following century, the concentration of capital in the British capital led a Scottish observer, Alexander Fletcher of Saltoun, to decry from a distance that “London should draw the riches and government of the three kingdoms [England, Scotland, and Wales] to the southeast corner of this island.” It is wrong, he continued, “for one city to possess the riches.” Wrong or not, it happened, and it keeps happening. Three centuries after Fletcher’s lament, London is still the richest part of the realm.

The oldest known bank-note, issued by the Bank of England in 1699. (Hulton Archive/Getty Images)

The Private Banking Department of the Bank of England, circa 1820. (Hulton Archive/Getty Images)

In this country, at the twain of the 19th and 20th centuries, the same amassing-of-wealth-in-the-city syndrome provoked Democrat William Jennings Bryan of Nebraska, “The Great Commoner,” to run presidential campaigns aimed largely at New York City-based financial interests. Bryan championed easier credit, as well as better prices and railroad rates, for farmers and small townsmen. He lost New York State but carried Oklahoma; Democrats were different in those days.

A poster for William Jennings Bryan’s 1900 presidential campaign. (Library of Congress/via Getty Images)

In the meantime, the Panic of 1907 convinced most Americans that something needed to be done to protect the banking system and thus the overall economy.

Indeed, two streams of thinking came together: First, New Yorkers and other Yankees (then mostly Republican) believed that a central bank would help prevent bank runs and panics. Second, the followers of Bryan and other populists (mostly Democrats) believed that assurances were needed to make sure that credit flowed all the way to the boonies.

Photograph of Wall Street, circa October 1907, during the financial Panic of 1907. (Fotosearch/Getty Images)

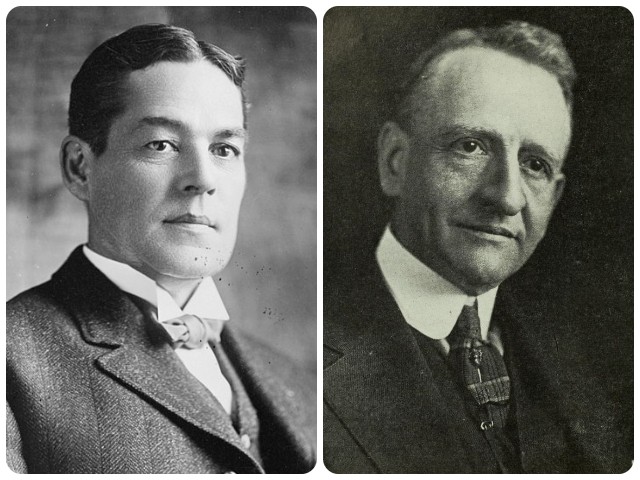

Two years ago, here at Breitbart News, this author wrote about Robert Latham Owen, who represented Oklahoma in the U.S. Senate from 1907 to 1925. As a small-town banker earlier in his life, Owen had experienced a credit drought; as chairman of the the Senate Banking Committee in 1913, he resolved to fix it.

Owen’s solution was a central bank, but with a decentralized architecture. Whereas the Northern Republicans of that era favored a “National Reserve Association,” Owen and his key ally in the House, Rep. Carter Glass (D-VA), chairman of the House Banking Committee, favored a Federal Reserve. That was a key distinction, “national” vs. “federal,” because federal implied carefully enumerated state powers, as in federalism. Owen and Glass and their fellow Democrats figured that if the power of the new bank was distributed across the states — and not just pooled up in New York City or Washington, D.C. — then their folks would be treated fairly.

Robert Latham Owen (L) circa 1910, and Carter Glass (R) circa 1919. (Library of Congress/The World’s Work)

Indeed, Owen’s bill establishing the Federal Reserve was so tilted toward the states that the states’ rights-minded Democrats in the Senate back then all voted aye, whereas all but four of the central bank-minded Republican voted nay. It’s because of this old-time Democratic influence that the Federal Reserve System has its distributed structure of 12 regional banks. The idea was that the Fed bank headquartered in, say, Kansas City would have real power to look out for its region.

As we have seen, Owen was a Democrat, and yet a century ago he had pretty much the same dim view of New York City finance as does Republican Lankford in our time. (To this day, Owen’s legacy is a point of pride in Oklahoma.)

So, we can see once again: The more things change, the more they stay the same.

Protecting the Heartland from Big Blue Banking

To be sure, some say that the whole idea of a central bank, federalized or otherwise, is a bad idea. And while critics raise plenty of good points, it’s hard to see the Fed being done away with. So, the thing to do is make it better by making sure that reform is a constant process. And after what we’ve seen in the past few weeks, reform seems all the more urgent.

Oklahomans can start with the baseline reality that theirs is still a relatively poor state—it ranks a mere 42nd in per capita income. (Yes, these rankings are complicated and debatable, especially when one takes housing costs into account, and yet still, Oklahoma’s population growth has been relatively flat. It lost a House seat after the 2000 Census.)

What’s clear, by any measure, is that the magnet of the money centers is always on. So, the bailouts of the coastal banks have been merely the latest instance of money magnetization that hurts Oklahoma—and all the other Oklahoma-ish states.

So, what to do?

One obvious answer is what Lankford says: Stop the federal government from transferring money away from Oklahoma, as it’s been doing with the big bank bailouts, which will raise deposit-insurance fees on sound banks to bail out the wastrels who will then be free to waste, and woke, again.

As Breitbart News’ John Carney argues in the Breitbart Business Digest, letting banks fail (while protecting small depositors) is the essence of the “creative destruction” that drives a free economy. Success and failure are the only ways to learn what works and what doesn’t.

(iStock/Getty Images)

Making a more systemic fix will require the reassertion of the federal structure of the Fed and the rest of the federal government. The 50 states must be actively jealous of their rights; otherwise, the central bank will happily subsidize its big-city cronies. Yellen and the Deep State will naturally pick winners and losers. Red States such as Oklahoma have been picked to be losers, while Blue States (at least the Democratic donors therein) are designated as winners.

To right this wrong, the vigorous power of the states, each empowered to chart its economic destiny, needs to be restored. More than a century ago, it was Democrats, such as Oklahoma’s Owen and Virginia’s Glass, who put the federal system of banking in place. Today, it’s their descendants — now Republicans — who need to carry out the federalist restoration.

Furthermore, Republicans (and the occasional Democrat) must scan the horizon for new threats to the wellbeing of the heartland. For instance, the bank bailouts signal the federal government’s continued commitment to inflationary policies. Yes, interest rates have gone higher, and yet Uncle Sugar is there with more spoonfuls of bailouts. So, yes, prices will go higher, which is not good for the middle class. Moreover, there’s the threat of central bank digital currency, a sort of federal crypto, touted by the Biden administration. In response, Red Staters should pay heed to this warning:

If you haven’t figured it out yet, the Federal Reserve, the Biden Administration, the ECB [European Central Bank] BlackRock etc are strategically “problematizing” the capitalist system so that they can gain control of the levers of power, cut out the middle man (local and regional banks) and centralize currency before digitizing currency.

Sounds like the money version of the Great Reset, eh?

Big Blue Banking and the Democrats plan to stay woke; and if and when they go broke, they will bail themselves out with other people’s money. That’s how the rich stay rich and get richer.

So yes, Oklahomans and regular folks everywhere have a lot of work to do to defend themselves.

But you knew that.