Goldilocks it wasn't... as inflation macro data surprised to the upside and growth macro data to the downside (we love the smell of stagflation in the morning)...

Source: Bloomberg

... but that didn't stop stocks soaring for the fifth straight week, with Small Caps exploding higher today (back into the green for the week)...

...as "most shorted" stocks saw a massive squeeze higher today...

Source: Bloomberg

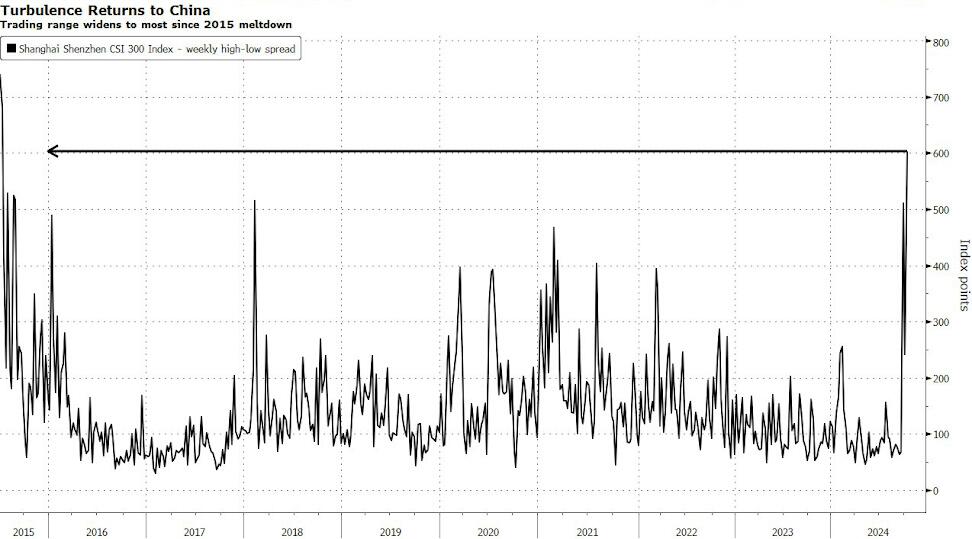

Of course, a market wrap would not be complete without discussing the shitshow in Shanghai as Chinese stocks witnessed the greatest volatility since their meltdown in 2015, capping almost $500 billion of combined losses in mainland and Hong Kong markets, as investors demanded even more stimulus than authorities in Beijing have already pledged.

The CSI 300 Index’s weekly trading range - the gap between high and low prices - surged above 600 index points this week for the first time since July 2015.

Source: Bloomberg

Back then, Chinese markets witnessed an exodus of foreigners driven by mounting economic concerns and a government crackdown on traders which only exacerbated the panic.

Source: Bloomberg

This time, the turbulence is driven by sluggish consumer demand that threatens even the scaled-down growth ambitions of the country. The index’s 10-day and 20-day realized volatility also rose to a nine-year high.

Notably, the rise in macro surprise data has come as financial conditions have loosened to their 'easiest' since Nov 2021...

Source: Bloomberg

Today saw the 45th all-time-high of the year, but none of the prior 44 have occurred alongside this elevated a level of volatility; this will be the first week of the year where the VIX has closed above 20 every day, and so ongoing elevated risk is expected as we progress through October...

Source: Bloomberg

The vol term structure is notably upward-sloping into the election now (and the coincidental FOMC meeting)...

Source: Bloomberg

Treasury yields were very mixed today and on the week the short-end dramatically outperforming (practically unch on the week as the long-end blew out)...

Source: Bloomberg

After a huge flattening last week, the yield curve steepened by the most since the start of August this week with 2s10s dropping to inversion to start the week and steepening to erase the post-payrolls plunge by the end...

Source: Bloomberg

Rate-cut expectations rose modestly this week (with all the focus on 2025 as 2024 remains priced for less than 2 full rate cuts now)...

Source: Bloomberg

The dollar rallied for the second straight week, testing up to August's highs before stalling a little today...

Source: Bloomberg

Despite the dollar strength, Gold extended yesterday's rebound to end the week higher, finding support at $2600 once again...

Source: Bloomberg

Oil was flat today holding on to gains on the week (with WTI back above $75)...

Source: Bloomberg

Bitcoin exploded back higher today (from $59,000 to $63,000), to end the week solidly in the green (after testing near one-month lows)...

Source: Bloomberg

Is this the start of Bitcoin's rip on the back of surging liquidity...

Source: Bloomberg

Finally, this weekend represents the two year anniversary from the bear market lows. The S&P is up 66% from the lows in October 2021, helped by and endless supply of liquidity from global central planners...]

Source: Bloomberg

BUT... the last week or two has seen liquidity start to contract a little (even as stocks soared to record-er highs)...

Source: Bloomberg

Will the money-printers get back to work... or will stocks sink into the election (which Trump is now leading in all the prediction markets - but not the polls)?

Source: Bloomberg

There's no bears left...

Source: Bloomberg

...well maybe some...

Goldilocks it wasn’t… as inflation macro data surprised to the upside and growth macro data to the downside (we love the smell of stagflation in the morning)…

Source: Bloomberg

… but that didn’t stop stocks soaring for the fifth straight week, with Small Caps exploding higher today (back into the green for the week)…

…as “most shorted” stocks saw a massive squeeze higher today…

Source: Bloomberg

Of course, a market wrap would not be complete without discussing the shitshow in Shanghai as Chinese stocks witnessed the greatest volatility since their meltdown in 2015, capping almost $500 billion of combined losses in mainland and Hong Kong markets, as investors demanded even more stimulus than authorities in Beijing have already pledged.

The CSI 300 Index’s weekly trading range – the gap between high and low prices – surged above 600 index points this week for the first time since July 2015.

Source: Bloomberg

Back then, Chinese markets witnessed an exodus of foreigners driven by mounting economic concerns and a government crackdown on traders which only exacerbated the panic.

Source: Bloomberg

This time, the turbulence is driven by sluggish consumer demand that threatens even the scaled-down growth ambitions of the country. The index’s 10-day and 20-day realized volatility also rose to a nine-year high.

Notably, the rise in macro surprise data has come as financial conditions have loosened to their ‘easiest’ since Nov 2021…

Source: Bloomberg

Today saw the 45th all-time-high of the year, but none of the prior 44 have occurred alongside this elevated a level of volatility; this will be the first week of the year where the VIX has closed above 20 every day, and so ongoing elevated risk is expected as we progress through October…

Source: Bloomberg

The vol term structure is notably upward-sloping into the election now (and the coincidental FOMC meeting)…

Source: Bloomberg

Treasury yields were very mixed today and on the week the short-end dramatically outperforming (practically unch on the week as the long-end blew out)…

Source: Bloomberg

After a huge flattening last week, the yield curve steepened by the most since the start of August this week with 2s10s dropping to inversion to start the week and steepening to erase the post-payrolls plunge by the end…

Source: Bloomberg

Rate-cut expectations rose modestly this week (with all the focus on 2025 as 2024 remains priced for less than 2 full rate cuts now)…

Source: Bloomberg

The dollar rallied for the second straight week, testing up to August’s highs before stalling a little today…

Source: Bloomberg

Despite the dollar strength, Gold extended yesterday’s rebound to end the week higher, finding support at $2600 once again…

Source: Bloomberg

Oil was flat today holding on to gains on the week (with WTI back above $75)…

Source: Bloomberg

Bitcoin exploded back higher today (from $59,000 to $63,000), to end the week solidly in the green (after testing near one-month lows)…

Source: Bloomberg

Is this the start of Bitcoin’s rip on the back of surging liquidity…

Source: Bloomberg

Finally, this weekend represents the two year anniversary from the bear market lows. The S&P is up 66% from the lows in October 2021, helped by and endless supply of liquidity from global central planners…]

Source: Bloomberg

BUT… the last week or two has seen liquidity start to contract a little (even as stocks soared to record-er highs)…

Source: Bloomberg

Will the money-printers get back to work… or will stocks sink into the election (which Trump is now leading in all the prediction markets – but not the polls)?

Source: Bloomberg

There’s no bears left…

Source: Bloomberg

…well maybe some…

Loading…