Ugly Canadian CPI, surging crude prices (early - on Azerbaijan angst)), mixed housing data, and a trigger happy group of traders anxiously awaiting tomorrow's Fed-sponsored narrative all sparked some chaotic moves in markets today.

The headline-making market of the day is USTs today with a double-barf sending yields 5-7bps higher on the day...

Source: Bloomberg

Which pushed yields to their highest since 2007...

Source: Bloomberg

With bonds at their cheapest to stocks since Oct 2007...

Source: Bloomberg

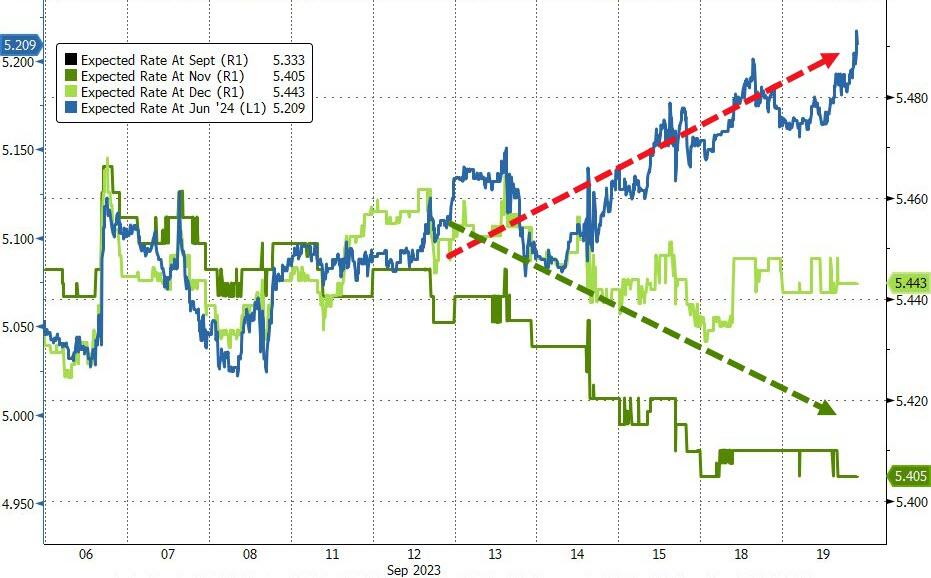

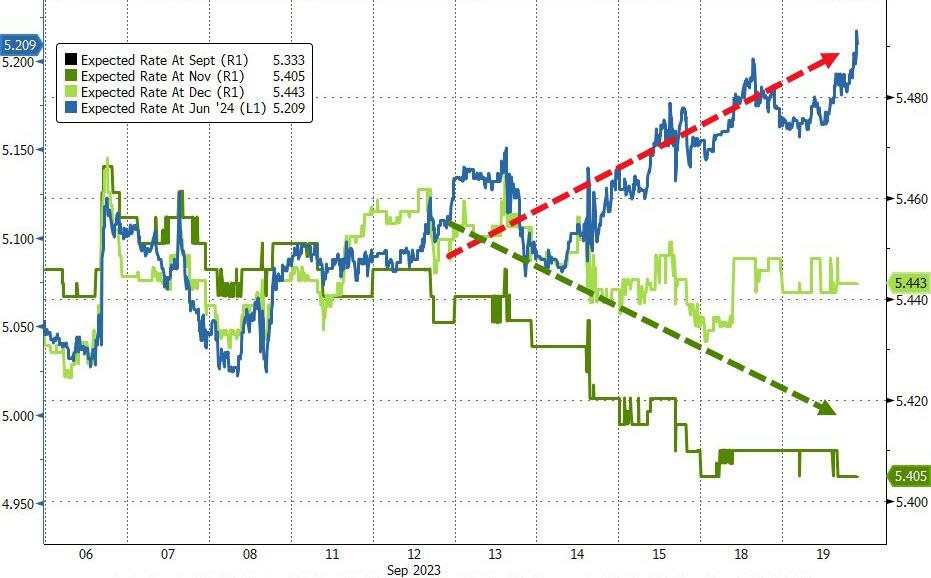

At the very short-end of the curve, the market has really started to embrace the 'higher for longer' narrative as this year's rate-change expectations have drifted (dovishly) lower (less expectations of more rate-hikes) while next year's rate-change expectations have surged (hawkishly) higher, pricing out expectations of rate-cuts...

Source: Bloomberg

All of which pressured stocks lower - especially longer-duration assets. After Europe closed, the algos tried to lift the major indices back to unch but failed. All the major indices closed red (down 02. to 0.3% on the day)...

CART IPO'd at $30, opened at $42, rallied up to $42.95 before fading the rest of the day...

ARM fell back below its post-IPO opening price...

Regional banks keep falling - now back at SVB tumble lows...

The dollar chopped around but ended back in the very tight range of the last couple of days...

Source: Bloomberg

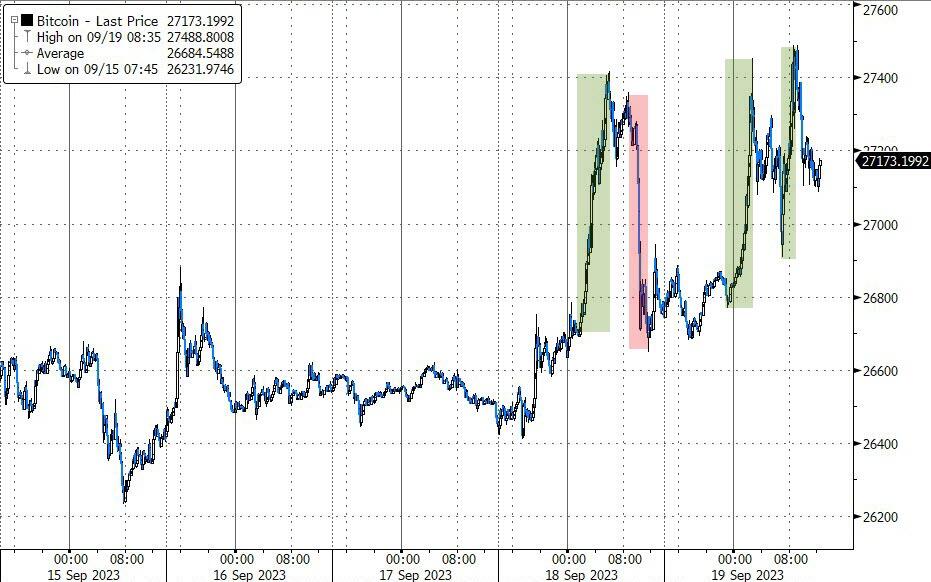

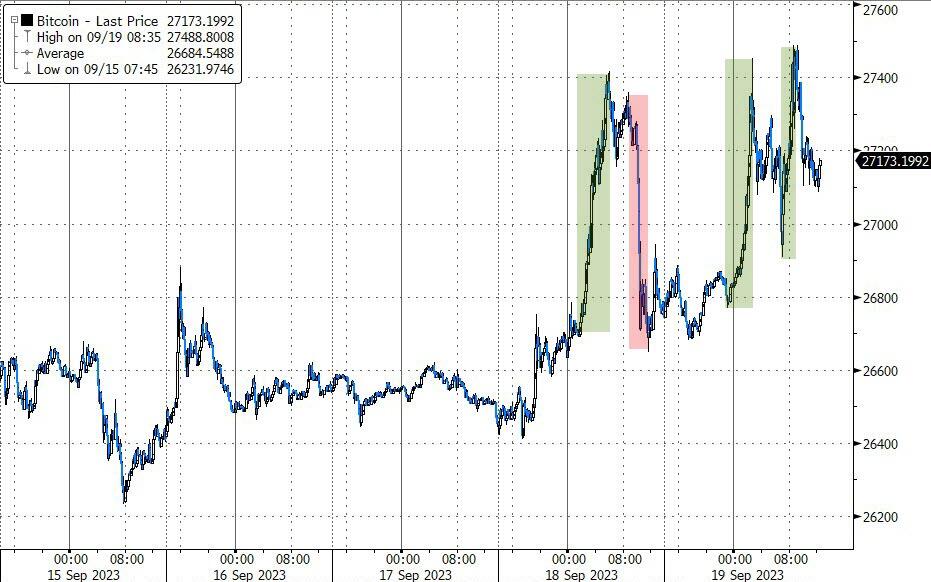

Bitcoin bounced back above $27,000...

Source: Bloomberg

Gold (spot) neared $1940 intraday, but ended unchanged...

Source: Bloomberg

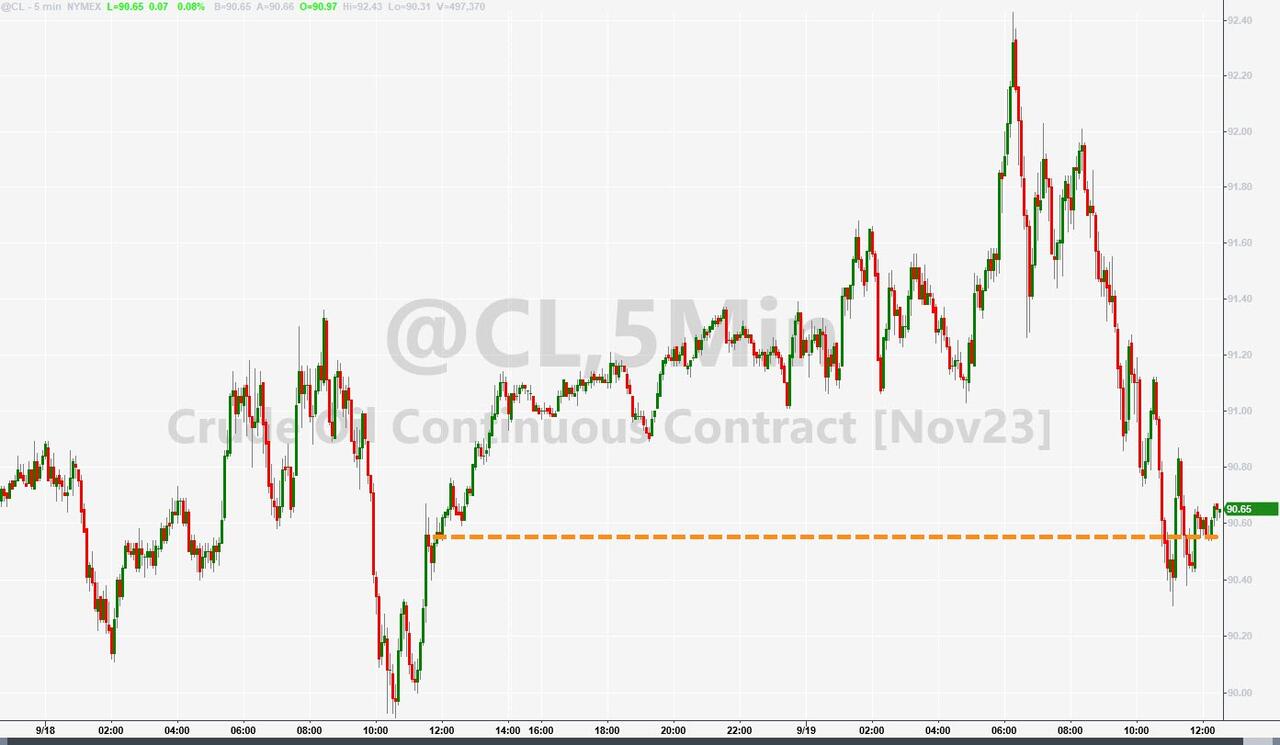

Oil prices pumped (to new cycle highs) and dumped (WTI finding support at $90) to end practically unchanged...

Finally, with real yields hitting fresh highs, one wonders when reality hits for equity valuations?

Source: Bloomberg

Consider what kind of shift (down) in real yields it would take to rationalize this valuation (economic depression?)

Ugly Canadian CPI, surging crude prices (early – on Azerbaijan angst)), mixed housing data, and a trigger happy group of traders anxiously awaiting tomorrow’s Fed-sponsored narrative all sparked some chaotic moves in markets today.

The headline-making market of the day is USTs today with a double-barf sending yields 5-7bps higher on the day…

Source: Bloomberg

Which pushed yields to their highest since 2007…

Source: Bloomberg

With bonds at their cheapest to stocks since Oct 2007…

Source: Bloomberg

At the very short-end of the curve, the market has really started to embrace the ‘higher for longer’ narrative as this year’s rate-change expectations have drifted (dovishly) lower (less expectations of more rate-hikes) while next year’s rate-change expectations have surged (hawkishly) higher, pricing out expectations of rate-cuts…

Source: Bloomberg

All of which pressured stocks lower – especially longer-duration assets. After Europe closed, the algos tried to lift the major indices back to unch but failed. All the major indices closed red (down 02. to 0.3% on the day)…

CART IPO’d at $30, opened at $42, rallied up to $42.95 before fading the rest of the day…

ARM fell back below its post-IPO opening price…

Regional banks keep falling – now back at SVB tumble lows…

1-Day VIX spiked today (as it tends to do pre-catalyst)

And we note that the world and his pet rabbit appears to be hedge as VIX Call Open Interest soared again…

The dollar chopped around but ended back in the very tight range of the last couple of days…

Source: Bloomberg

Bitcoin bounced back above $27,000…

Source: Bloomberg

Gold (spot) neared $1940 intraday, but ended unchanged…

Source: Bloomberg

Oil prices pumped (to new cycle highs) and dumped (WTI finding support at $90) to end practically unchanged…

Finally, with real yields hitting fresh highs, one wonders when reality hits for equity valuations?

Source: Bloomberg

Consider what kind of shift (down) in real yields it would take to rationalize this valuation (economic depression?)

Loading…