By Henry Byers of FreightWaves

Last week, we forecast a further decline in U.S. containerized import volumes in the second half of 2023, and a “new” bottom for volumes during this downcycle.

The lingering effects of the “bullwhip effect” on inventories, along with the considerable downside risks that exist to consumer spending, the upcoming months are likely to witness an unprecedented level of caution among importers during this year’s peak season. This caution, combined with a weakening global macroeconomic backdrop, only heightens the risks of declining import volumes.

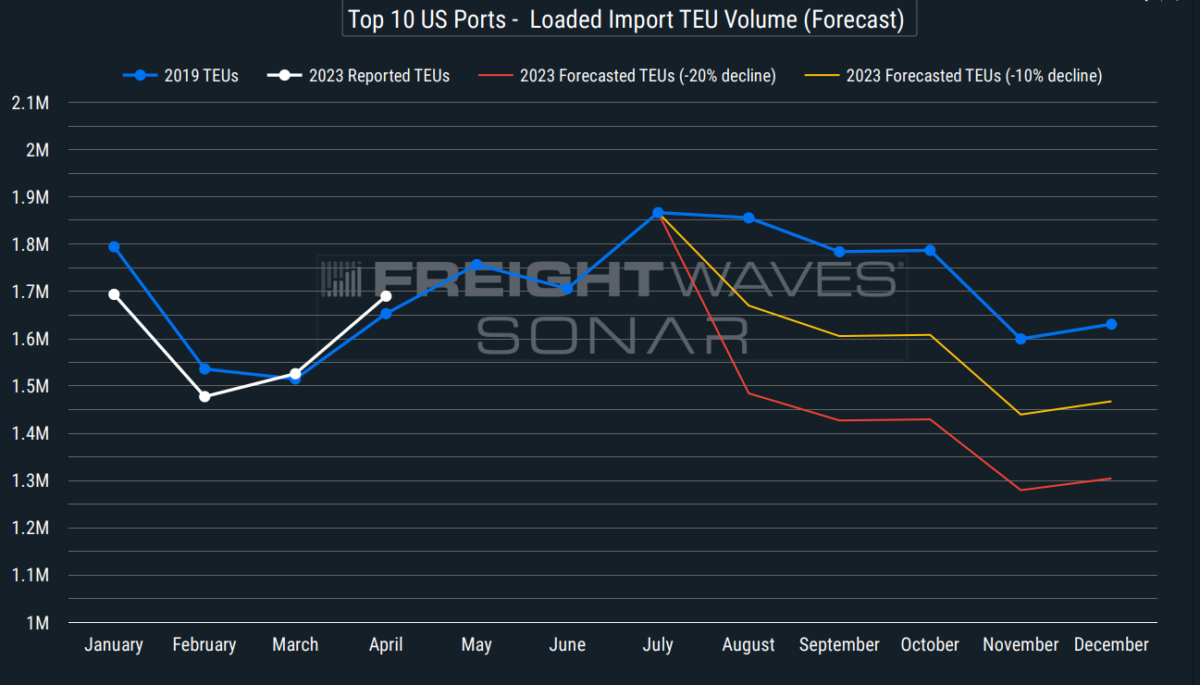

As we forecast, ocean container bookings in the first half of 2023 (white line) have continued trending right alongside 2019 levels (orange line). This is expected to continue through early Q3, at which point we will likely begin to see a detaching from 2019 levels to find a “new” bottom, ultimately resulting in a significant drop of 10% to 20% below levels experienced during the 2nd-half of 2019. Below is a chart of what that decline of 10% (orange) to 20% (red) in monthly loaded import TEUs would look like across the Top 10 U.S. ports.

The most recent May report from Logistics Managers’ Index (LMI) data highlights an important nuance in the persistently high inventories. While the supply chain activity reached an all-time low for the third consecutive month in May, inventory levels also contracted for the first time since the early days of the pandemic. However, even though inventory levels decreased by 1.5 points to 49.5 (marking the first time since February 2020 that inventories have entered contraction territory), it’s important to note that downstream retail inventories continue to grow at a rate of 54.4, while upstream manufacturer and wholesaler inventories are contracting at a rate of 46.7, which pulled down the overall figure for May.

With retail inventories still in a period of expansion, retailers that are major U.S. importers can be expected to adopt a cautious approach as they navigate the excess inventories that have accumulated in the supply chain bullwhip. These retailers have been scaling back since recognizing the inventory issue in Q1 2022, but the reality is that high inventory levels persist and could extend the destocking cycle throughout (at least) the remainder of 2023. This will require importers to be increasingly strategic in their reordering efforts in the second half to prevent further inventory buildup and manage costs effectively while addressing any additional shifts in consumer demand.

As a prime example, Target, one of the major retail players (and the second-largest U.S. importer of containerized goods) entered 2023 with a sense of caution due to its inventory glut and potential shifts in consumer spending patterns. The company’s fiscal year 2022 report highlighted the challenges posed by rapid changes in consumer preferences and supply chain volatility, necessitating careful inventory planning to minimize markdowns. In the most recent quarter, Target has now seen both a decline in foot traffic (down 9% y/y) and sales figures (down 5% y/y) as reported by CitiBank analysts, which has likely only increased Target’s concerns about reordering/restocking. In the report from CitiBank, which downgraded Target’s stock price, the Citi analysts also noted other growing concerns for the retailer, such as the competitive pressure posed by Walmart, which is expected to continue gaining market share (largely due to its strong Grocery segment), potentially impacting Target’s discretionary sales, which account for 55% of its overall sales. With Target serving as a prime example of the issues that major retailers are potentially facing heading into the second half of 2023, it is becoming increasingly evident why the company would be incredibly cautious with bringing in new container volumes.

Looking a little further upstream, wholesalers are also facing larger inventory problems than may be perceived from solely looking at the most recent LMI report. Since November 2022, the inventory-to-sales ratio has been higher than during the worst months of the Great Recession. If sales do not rebound (increasingly unlikely that they will), inventories must undergo substantial reductions in the second half. The imbalance between excessive inventories and only a slight softening of sales is causing significant strain throughout the global supply chain, especially when it comes to major origin countries and production centers for U.S. containerized goods.

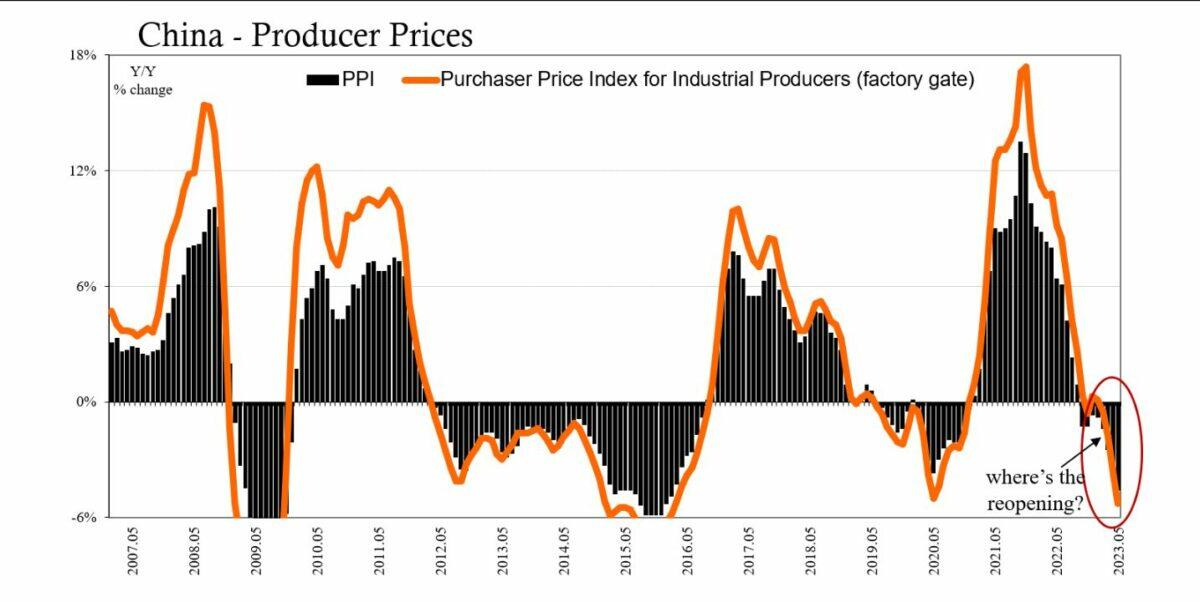

This strain is becoming increasingly apparent further upstream into major origin countries for U.S. containerized imports like China, where economic troubles continue to worsen. Jeffrey Snider of Eurodollar.University has been covering this in-depth in recent weeks, and in a recent video post, he pointed out that for the fourth consecutive month, consumer prices have dropped alongside the largest year-on-year decline in Producer Price Index (PPI) and factory gate prices since 2016. In the chart below, we can see that in May alone, China’s producer prices experienced a significant 0.9% decrease, further confirming that China’s reopening has been significantly overstated. These year-on-year declines are especially concerning given the fact that these comparisons are being made during last year when large manufacturing centers in China (i.e. Shanghai) were still largely on lockdown due to COVID restrictions.

Snider also pointed out that China’s economic woes are reverberating throughout Asia, driven by the global recession that has dragged down industries. This widespread contraction is evident in the sharp decline in imports from South Korea and Japan, with both countries experiencing a 26% year-to-date decrease in imports. There has also been a substantial decline in China’s exports. Specifically, the value of goods exported to the U.S. plummeted by 18% year on year in May. This is all supportive of the reality that the reverse bullwhip effect has dealt a large blow to China, resulting ultimately in lower prices while intensifying the global trade recession, which has spread deeper into Europe.

Europe’s PPI has sharply declined, primarily due to falling energy prices, but included a considerable decline in core prices as well. The HCOB Flash Manufacturing PMI for the Eurozone in May 2023 recorded a significant decline to 44.6 from April’s 45.8, far below the forecasted 46.2. This reading indicates the sharpest contraction in the factory sector in three years, with output, new orders, and backlogs of orders all declining at an accelerated pace. Input prices experienced the most substantial drop since February 2016, as manufacturers curtailed their input purchases, leading to a steep decline in inventories. Business confidence, especially within the manufacturing sector, weakened further, and Germany (already in an official recession) witnessed a particularly pronounced decline in manufacturing activity. Factory orders there have plummeted, especially from non-European markets, further indicating weakening global demand.

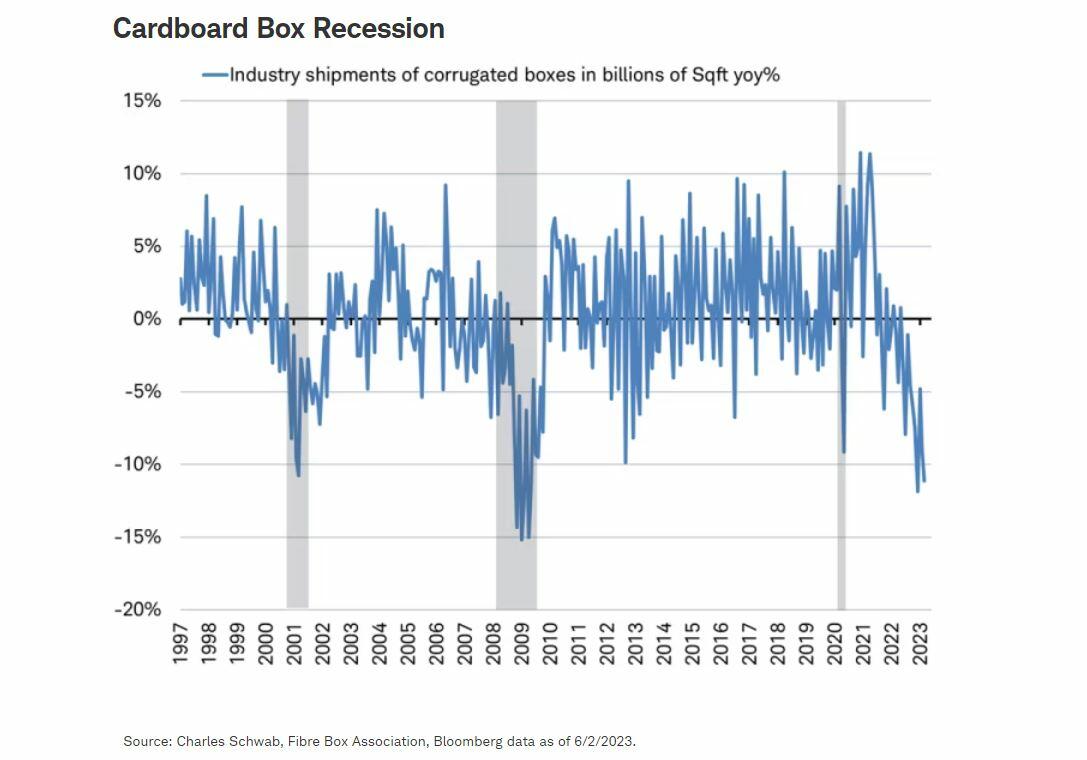

It is also important to note another major input in the manufacturing process: cardboard box demand. FreightWaves was among the first to cover the concerning signs surrounding cardboard box demand in the article, “Cardboard box demand plunging at rates unseen since the Great Recession.” Demand has remained soft ever since, and in a recent article from Charles Schwab’s chief global investment strategist, Jeffrey Kleintop, he proclaimed that the United States is currently experiencing a “cardboard box recession.” This refers to a situation in which manufacturing and trade experience a global recession while services industries continue to grow. Demand for manufacturing and trade-related goods has declined, as indicated by the decrease in demand for corrugated linerboard.

Circling all the way back to consumers, there are still a number of downside risks facing consumer spending in the 2nd-half, but one of the largest risks is student loan repayments. FreightWaves CEO Craig Fuller covered this risk at length in his recent article “An unusually terrible freight market may get a lot worse.” The article points out factors that could worsen the freight market, including the potential end of various stimulus programs that have boosted personal income and freight demand, but specifically, it highlights the potential fallout caused by the impending resumption of student loan payments.

The end of the student loan deferment program, which allowed consumers to save an average of over $15,000 since March 2020, will have a significant impact on consumer spending. With 64% of the $1.7 trillion student loan debt remaining in forbearance, the resumption of payments will create a cash flow shock for many households, particularly among the 25 million Americans ages 18-44 who have deferred their payments. This demographic plays a crucial role in driving consumer spending, and the sudden increase of approximately $393 per month in loan payments will likely lead to reduced discretionary income and a potential decrease in spending capacity.

The lingering effects of the “bullwhip effect” on inventories at major U.S. importers, along with the considerable downside risks that exist to consumer spending, the upcoming months are likely to witness an unprecedented level of caution among importers. The prevailing global economic conditions further contribute to the downward risks facing import volumes. While it may not be a sharp drop, it is becoming increasingly probable that U.S. import demand will experience a fresh decline and establish a new low point in the second half of 2023.

By Henry Byers of FreightWaves

Last week, we forecast a further decline in U.S. containerized import volumes in the second half of 2023, and a “new” bottom for volumes during this downcycle.

The lingering effects of the “bullwhip effect” on inventories, along with the considerable downside risks that exist to consumer spending, the upcoming months are likely to witness an unprecedented level of caution among importers during this year’s peak season. This caution, combined with a weakening global macroeconomic backdrop, only heightens the risks of declining import volumes.

As we forecast, ocean container bookings in the first half of 2023 (white line) have continued trending right alongside 2019 levels (orange line). This is expected to continue through early Q3, at which point we will likely begin to see a detaching from 2019 levels to find a “new” bottom, ultimately resulting in a significant drop of 10% to 20% below levels experienced during the 2nd-half of 2019. Below is a chart of what that decline of 10% (orange) to 20% (red) in monthly loaded import TEUs would look like across the Top 10 U.S. ports.

The most recent May report from Logistics Managers’ Index (LMI) data highlights an important nuance in the persistently high inventories. While the supply chain activity reached an all-time low for the third consecutive month in May, inventory levels also contracted for the first time since the early days of the pandemic. However, even though inventory levels decreased by 1.5 points to 49.5 (marking the first time since February 2020 that inventories have entered contraction territory), it’s important to note that downstream retail inventories continue to grow at a rate of 54.4, while upstream manufacturer and wholesaler inventories are contracting at a rate of 46.7, which pulled down the overall figure for May.

With retail inventories still in a period of expansion, retailers that are major U.S. importers can be expected to adopt a cautious approach as they navigate the excess inventories that have accumulated in the supply chain bullwhip. These retailers have been scaling back since recognizing the inventory issue in Q1 2022, but the reality is that high inventory levels persist and could extend the destocking cycle throughout (at least) the remainder of 2023. This will require importers to be increasingly strategic in their reordering efforts in the second half to prevent further inventory buildup and manage costs effectively while addressing any additional shifts in consumer demand.

As a prime example, Target, one of the major retail players (and the second-largest U.S. importer of containerized goods) entered 2023 with a sense of caution due to its inventory glut and potential shifts in consumer spending patterns. The company’s fiscal year 2022 report highlighted the challenges posed by rapid changes in consumer preferences and supply chain volatility, necessitating careful inventory planning to minimize markdowns. In the most recent quarter, Target has now seen both a decline in foot traffic (down 9% y/y) and sales figures (down 5% y/y) as reported by CitiBank analysts, which has likely only increased Target’s concerns about reordering/restocking. In the report from CitiBank, which downgraded Target’s stock price, the Citi analysts also noted other growing concerns for the retailer, such as the competitive pressure posed by Walmart, which is expected to continue gaining market share (largely due to its strong Grocery segment), potentially impacting Target’s discretionary sales, which account for 55% of its overall sales. With Target serving as a prime example of the issues that major retailers are potentially facing heading into the second half of 2023, it is becoming increasingly evident why the company would be incredibly cautious with bringing in new container volumes.

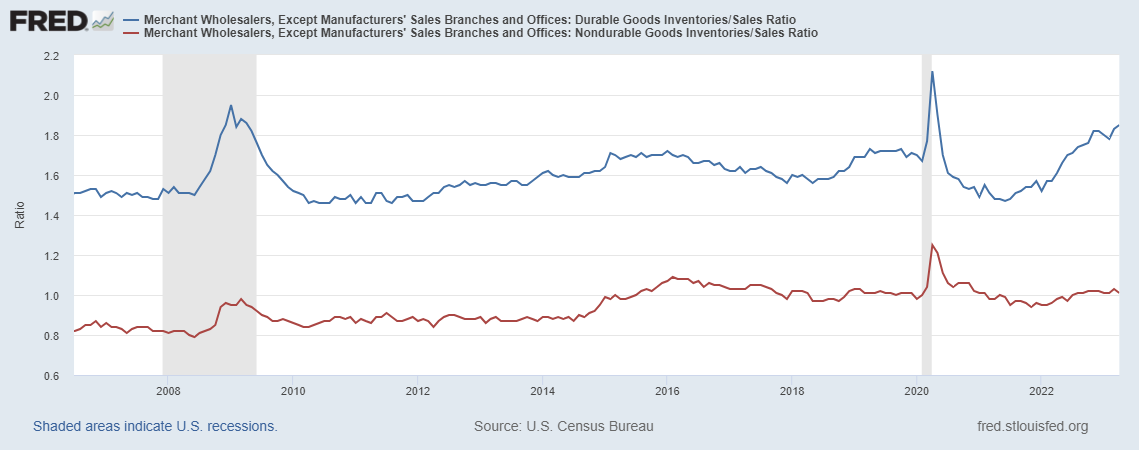

Looking a little further upstream, wholesalers are also facing larger inventory problems than may be perceived from solely looking at the most recent LMI report. Since November 2022, the inventory-to-sales ratio has been higher than during the worst months of the Great Recession. If sales do not rebound (increasingly unlikely that they will), inventories must undergo substantial reductions in the second half. The imbalance between excessive inventories and only a slight softening of sales is causing significant strain throughout the global supply chain, especially when it comes to major origin countries and production centers for U.S. containerized goods.

This strain is becoming increasingly apparent further upstream into major origin countries for U.S. containerized imports like China, where economic troubles continue to worsen. Jeffrey Snider of Eurodollar.University has been covering this in-depth in recent weeks, and in a recent video post, he pointed out that for the fourth consecutive month, consumer prices have dropped alongside the largest year-on-year decline in Producer Price Index (PPI) and factory gate prices since 2016. In the chart below, we can see that in May alone, China’s producer prices experienced a significant 0.9% decrease, further confirming that China’s reopening has been significantly overstated. These year-on-year declines are especially concerning given the fact that these comparisons are being made during last year when large manufacturing centers in China (i.e. Shanghai) were still largely on lockdown due to COVID restrictions.

Snider also pointed out that China’s economic woes are reverberating throughout Asia, driven by the global recession that has dragged down industries. This widespread contraction is evident in the sharp decline in imports from South Korea and Japan, with both countries experiencing a 26% year-to-date decrease in imports. There has also been a substantial decline in China’s exports. Specifically, the value of goods exported to the U.S. plummeted by 18% year on year in May. This is all supportive of the reality that the reverse bullwhip effect has dealt a large blow to China, resulting ultimately in lower prices while intensifying the global trade recession, which has spread deeper into Europe.

Europe’s PPI has sharply declined, primarily due to falling energy prices, but included a considerable decline in core prices as well. The HCOB Flash Manufacturing PMI for the Eurozone in May 2023 recorded a significant decline to 44.6 from April’s 45.8, far below the forecasted 46.2. This reading indicates the sharpest contraction in the factory sector in three years, with output, new orders, and backlogs of orders all declining at an accelerated pace. Input prices experienced the most substantial drop since February 2016, as manufacturers curtailed their input purchases, leading to a steep decline in inventories. Business confidence, especially within the manufacturing sector, weakened further, and Germany (already in an official recession) witnessed a particularly pronounced decline in manufacturing activity. Factory orders there have plummeted, especially from non-European markets, further indicating weakening global demand.

It is also important to note another major input in the manufacturing process: cardboard box demand. FreightWaves was among the first to cover the concerning signs surrounding cardboard box demand in the article, “Cardboard box demand plunging at rates unseen since the Great Recession.” Demand has remained soft ever since, and in a recent article from Charles Schwab’s chief global investment strategist, Jeffrey Kleintop, he proclaimed that the United States is currently experiencing a “cardboard box recession.” This refers to a situation in which manufacturing and trade experience a global recession while services industries continue to grow. Demand for manufacturing and trade-related goods has declined, as indicated by the decrease in demand for corrugated linerboard.

Circling all the way back to consumers, there are still a number of downside risks facing consumer spending in the 2nd-half, but one of the largest risks is student loan repayments. FreightWaves CEO Craig Fuller covered this risk at length in his recent article “An unusually terrible freight market may get a lot worse.” The article points out factors that could worsen the freight market, including the potential end of various stimulus programs that have boosted personal income and freight demand, but specifically, it highlights the potential fallout caused by the impending resumption of student loan payments.

The end of the student loan deferment program, which allowed consumers to save an average of over $15,000 since March 2020, will have a significant impact on consumer spending. With 64% of the $1.7 trillion student loan debt remaining in forbearance, the resumption of payments will create a cash flow shock for many households, particularly among the 25 million Americans ages 18-44 who have deferred their payments. This demographic plays a crucial role in driving consumer spending, and the sudden increase of approximately $393 per month in loan payments will likely lead to reduced discretionary income and a potential decrease in spending capacity.

The lingering effects of the “bullwhip effect” on inventories at major U.S. importers, along with the considerable downside risks that exist to consumer spending, the upcoming months are likely to witness an unprecedented level of caution among importers. The prevailing global economic conditions further contribute to the downward risks facing import volumes. While it may not be a sharp drop, it is becoming increasingly probable that U.S. import demand will experience a fresh decline and establish a new low point in the second half of 2023.

Loading…