Authored by Simon White, Bloomberg macro strategist,

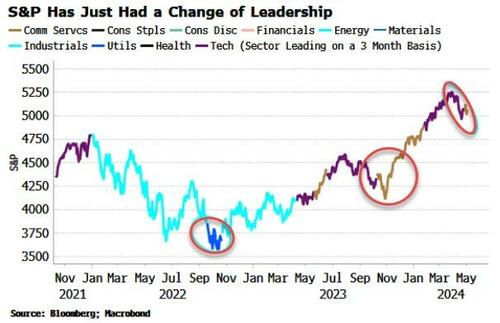

A change in sector leadership in US stocks suggests the correction might soon be over and a bottom is not too far away.

The tech sector has led the recent advance in the US stock-market (i.e. the sector with the highest three-month return on a three-month smoothed basis), but in the last two weeks it lost that mantle to the communication services sector.

(Tech stocks are leading today after the payrolls miss, but on a three-month return on a three-month smoothed basis communication services are still ahead.)

As the chart shows, the two previous market corrections were accompanied by a change of leadership. But that change came near the bottom and ahead of the next advance.

The tech sector is lagging as its main constituents, Microsoft, Apple and Nvidia, have been lagging, while the communication services sector, predominately Meta and Google, went into the lead, driven the latter’s positive earnings surprise last week.

Further confidence that the current fall in prices is just a correction is given by buoyant excess liquidity that continues to be supportive for stocks and relatively low near-term recession risk (although that is always subject to changes based on the data).

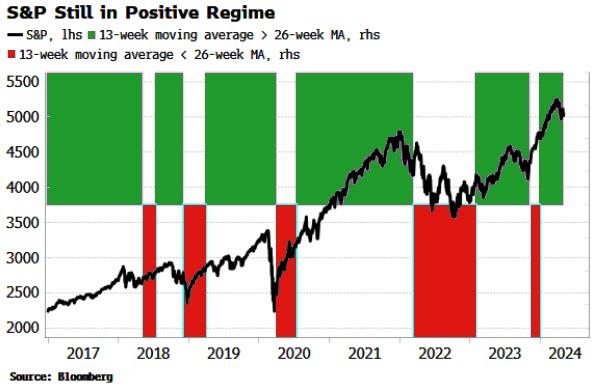

Also the primary bull trend in the stock market remains intact. The 13 versus 26-week moving average crossover signal for the S&P was one of the earliest signs that the market’s nascent advance in early 2023 was durable. The positive stock-market regime that began late last year remains in place.

Authored by Simon White, Bloomberg macro strategist,

A change in sector leadership in US stocks suggests the correction might soon be over and a bottom is not too far away.

The tech sector has led the recent advance in the US stock-market (i.e. the sector with the highest three-month return on a three-month smoothed basis), but in the last two weeks it lost that mantle to the communication services sector.

(Tech stocks are leading today after the payrolls miss, but on a three-month return on a three-month smoothed basis communication services are still ahead.)

As the chart shows, the two previous market corrections were accompanied by a change of leadership. But that change came near the bottom and ahead of the next advance.

The tech sector is lagging as its main constituents, Microsoft, Apple and Nvidia, have been lagging, while the communication services sector, predominately Meta and Google, went into the lead, driven the latter’s positive earnings surprise last week.

Further confidence that the current fall in prices is just a correction is given by buoyant excess liquidity that continues to be supportive for stocks and relatively low near-term recession risk (although that is always subject to changes based on the data).

Also the primary bull trend in the stock market remains intact. The 13 versus 26-week moving average crossover signal for the S&P was one of the earliest signs that the market’s nascent advance in early 2023 was durable. The positive stock-market regime that began late last year remains in place.

Loading…