Having disappointed the market with a lack of detail on its big stimulus, it appears Chinese authorities have resorted to the usual western practice of leaking details (strawmen) to the press in an effort to measure the market's reaction function.

As we detailed over the weekend, Saturday's much-anticipated press conference by China's Ministry of Finance, where many China watchers were expecting another major stimulus announcement with some hoping for a number as large as 10 trillion rmb, was a dud.

"The policy to support consumption sounds quite weak,” said Jacqueline Rong, chief China economist at BNP Paribas SA.

“It is still too early to call an imminent significant turnaround in deflationary pressure or a bottoming-out of the property market, which are the two key issues faced by the Chinese economy.”

Investors and analysts expected China to deploy about 2 trillion yuan ($283 billion) in fresh fiscal stimulus (and as much as 11 trillion yuan on the high end), including potential subsidies, consumption vouchers and financial support for families with children.

But, in response to the question of just how big the stimmy package will be, MoF's Lan responded that "regarding the specific RMB amount you asked, we will disclose promptly to the general society after the proper legal procedures have been passed."

Investors were displeased with this lack of response and so it appears Beijing has reached out to its media mouthpieces to test the waters.

Caixin Global reports that, according to multiple sources with knowledge of the matter, China may raise 6 trillion yuan from ultra-long special treasury bonds over three years as part of its efforts to buttress the slowing economy through fiscal stimulus.

The funds will be partly used to help local governments resolve their off-the-books debts, according to the sources.

The 6 trillion yuan number sits right in the middle of the range of analysts' expectations, but presumably this 'leak' will be used by authorities to judge what the market demands.

Liu Shijin, a former member of the country’s top political advisory body, recently advocated for a stimulus package of more than 10 trillion yuan - roughly one-tenth of the nation’s annual GDP - to be implemented over the coming one to two years.

He said the amount is appropriate for an economy as big as China’s. A bigger tool is needed to pry a bigger stone, he told Caixin, comparing his plan to China’s 4-trillion-yuan stimulus package during the global financial crisis in 2008.

Of course, what this massive debt-financed stimulus will produce initially is higher rates - something that will crush the very markets (housing) that the CCP is trying to bailout.

What does that mean? Simple... China QE is inevitable to tamp down any adverse bond-market reaction.

And, as we detailed previously, that is exactly what the markets are hoping for.

Goldman: to escape deflation and for the rally to be sustainable, China's M1 has to overtake its M2. For that to happen, China will need to unleash a historic credit impulse (record new debt creation, launch QE) and global inflationary shockwave. https://t.co/suSRIU8wJ5 pic.twitter.com/OCW6CjBM5S

— zerohedge (@zerohedge) October 6, 2024

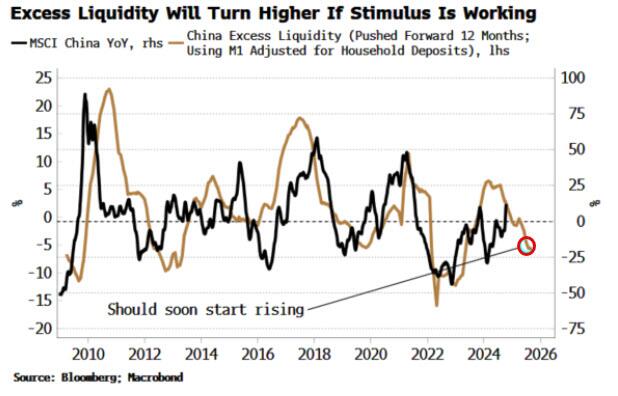

The current equity market exuberance will only be sustained by a resurgence in excess liquidity.

Of course, if Beijing doesn't unleash QE, M1 will fail to grow faster than M2, and the government "will spread the monetary crowding out to more weak borrowers in the economy", since the winners (successful corporates and rich households) will save the impulse and kill the multiplier, resulting in an even bigger hole for China 12-18 months from now, and global deflationary destruction.

On the other hand, if China does do QE, oil will soar, and bitcoin and gold will be orders of magnitude higher once Beijing triggers then next global reflationary tsunami.

Pick your poison.

Having disappointed the market with a lack of detail on its big stimulus, it appears Chinese authorities have resorted to the usual western practice of leaking details (strawmen) to the press in an effort to measure the market’s reaction function.

As we detailed over the weekend, Saturday’s much-anticipated press conference by China’s Ministry of Finance, where many China watchers were expecting another major stimulus announcement with some hoping for a number as large as 10 trillion rmb, was a dud.

“The policy to support consumption sounds quite weak,” said Jacqueline Rong, chief China economist at BNP Paribas SA.

“It is still too early to call an imminent significant turnaround in deflationary pressure or a bottoming-out of the property market, which are the two key issues faced by the Chinese economy.”

Investors and analysts expected China to deploy about 2 trillion yuan ($283 billion) in fresh fiscal stimulus (and as much as 11 trillion yuan on the high end), including potential subsidies, consumption vouchers and financial support for families with children.

But, in response to the question of just how big the stimmy package will be, MoF’s Lan responded that “regarding the specific RMB amount you asked, we will disclose promptly to the general society after the proper legal procedures have been passed.”

Investors were displeased with this lack of response and so it appears Beijing has reached out to its media mouthpieces to test the waters.

Caixin Global reports that, according to multiple sources with knowledge of the matter, China may raise 6 trillion yuan from ultra-long special treasury bonds over three years as part of its efforts to buttress the slowing economy through fiscal stimulus.

The funds will be partly used to help local governments resolve their off-the-books debts, according to the sources.

The 6 trillion yuan number sits right in the middle of the range of analysts’ expectations, but presumably this ‘leak’ will be used by authorities to judge what the market demands.

Liu Shijin, a former member of the country’s top political advisory body, recently advocated for a stimulus package of more than 10 trillion yuan – roughly one-tenth of the nation’s annual GDP – to be implemented over the coming one to two years.

He said the amount is appropriate for an economy as big as China’s. A bigger tool is needed to pry a bigger stone, he told Caixin, comparing his plan to China’s 4-trillion-yuan stimulus package during the global financial crisis in 2008.

Of course, what this massive debt-financed stimulus will produce initially is higher rates – something that will crush the very markets (housing) that the CCP is trying to bailout.

What does that mean? Simple… China QE is inevitable to tamp down any adverse bond-market reaction.

And, as we detailed previously, that is exactly what the markets are hoping for.

Goldman: to escape deflation and for the rally to be sustainable, China’s M1 has to overtake its M2. For that to happen, China will need to unleash a historic credit impulse (record new debt creation, launch QE) and global inflationary shockwave. https://t.co/suSRIU8wJ5 pic.twitter.com/OCW6CjBM5S

— zerohedge (@zerohedge) October 6, 2024

The current equity market exuberance will only be sustained by a resurgence in excess liquidity.

Of course, if Beijing doesn’t unleash QE, M1 will fail to grow faster than M2, and the government “will spread the monetary crowding out to more weak borrowers in the economy”, since the winners (successful corporates and rich households) will save the impulse and kill the multiplier, resulting in an even bigger hole for China 12-18 months from now, and global deflationary destruction.

On the other hand, if China does do QE, oil will soar, and bitcoin and gold will be orders of magnitude higher once Beijing triggers then next global reflationary tsunami.

Pick your poison.

Loading…