By Ven Ram, Bloomberg Markets Live strategist and reporter

The credit and the stock markets are telegraphing a message of caution on how global financial assets and the economy may evolve.

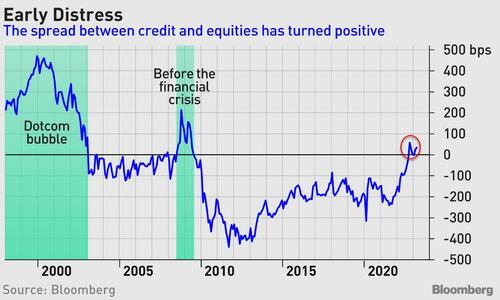

The spread between BBB rated dollar-denominated corporate debt and the earnings available on the S&P 500 Index of stocks is now above zero for the first time since the global financial crisis. The average yield on investment-grade bonds is 5.77%, compared with an estimated earnings yield of 5.42% on the S&P

The differential is typically negative, reflecting the higher risk of capital that is invested in equities even as corporate bond yields stay elevated. However, when speculative money flocks into equities, it turns positive, suggesting that investors may be overlooking the risk embedded in stocks.

The spread turned positive during the days of the dot-com boom, peaking at about 470 basis points before the bubble burst. It again turned positive in the run-up to the financial crisis, reaching almost 215 basis points. Neither of those movies ended well.

The median rating of companies in the S&P 500 basket is BBB+, according to data compiled by S&P Global Ratings, so the spread tends to isolate like-for-like credit and equity risk. As such, the current positive reading tends to serve as a note of caution on the evolution of asset prices.

That message from the markets is consistent with other markers as well. For instance, the Nasdaq 100 has held onto its stunning gains of about 12% this year, almost concurrent with a massive outflow from junk bonds. It’s possible that funds are flowing from speculative-grade credit into high-risk, higher-velocity stocks represented by technology names.

We are just about positive on the differential now, well dwarfed by the peaks we saw during the dot-com bubble and the financial crisis. In other words, this script may yet continue before something snaps in the US economy.

The positive spread suggests that investors may be getting overenthusiastic in buying the dip on stocks. The current earnings yield on stocks is about equal to the terminal Fed rate being priced in by the markets. It is as though the markets are contending that stocks don’t require any additional risk premium over Treasuries, which would be a monumental folly.

A study of the S&P 500’s duration showed that the index will decline about 7% for every 100-basis point increase in the Fed funds rate, underscoring the potential for stocks to fall further should the Fed keep tightening more than what’s priced in.

The speculative money flowing into stocks is focused on a single-point outcome: that the Fed will slash rates at the first hint of distress in the economy. Yet it’s highly unlikely that Chair Jerome Powell will be as accommodative as the central bank was in 2019. Back then, there was little inflation, so the scope to cut rates was high. Yet here we are, with headline inflation still running at more than three times the Fed’s target — so the speculative positions come with a lot of embedded risk.

By Ven Ram, Bloomberg Markets Live strategist and reporter

The credit and the stock markets are telegraphing a message of caution on how global financial assets and the economy may evolve.

The spread between BBB rated dollar-denominated corporate debt and the earnings available on the S&P 500 Index of stocks is now above zero for the first time since the global financial crisis. The average yield on investment-grade bonds is 5.77%, compared with an estimated earnings yield of 5.42% on the S&P

The differential is typically negative, reflecting the higher risk of capital that is invested in equities even as corporate bond yields stay elevated. However, when speculative money flocks into equities, it turns positive, suggesting that investors may be overlooking the risk embedded in stocks.

The spread turned positive during the days of the dot-com boom, peaking at about 470 basis points before the bubble burst. It again turned positive in the run-up to the financial crisis, reaching almost 215 basis points. Neither of those movies ended well.

The median rating of companies in the S&P 500 basket is BBB+, according to data compiled by S&P Global Ratings, so the spread tends to isolate like-for-like credit and equity risk. As such, the current positive reading tends to serve as a note of caution on the evolution of asset prices.

That message from the markets is consistent with other markers as well. For instance, the Nasdaq 100 has held onto its stunning gains of about 12% this year, almost concurrent with a massive outflow from junk bonds. It’s possible that funds are flowing from speculative-grade credit into high-risk, higher-velocity stocks represented by technology names.

We are just about positive on the differential now, well dwarfed by the peaks we saw during the dot-com bubble and the financial crisis. In other words, this script may yet continue before something snaps in the US economy.

The positive spread suggests that investors may be getting overenthusiastic in buying the dip on stocks. The current earnings yield on stocks is about equal to the terminal Fed rate being priced in by the markets. It is as though the markets are contending that stocks don’t require any additional risk premium over Treasuries, which would be a monumental folly.

A study of the S&P 500’s duration showed that the index will decline about 7% for every 100-basis point increase in the Fed funds rate, underscoring the potential for stocks to fall further should the Fed keep tightening more than what’s priced in.

The speculative money flowing into stocks is focused on a single-point outcome: that the Fed will slash rates at the first hint of distress in the economy. Yet it’s highly unlikely that Chair Jerome Powell will be as accommodative as the central bank was in 2019. Back then, there was little inflation, so the scope to cut rates was high. Yet here we are, with headline inflation still running at more than three times the Fed’s target — so the speculative positions come with a lot of embedded risk.

Loading…