Authored by Simon White, Bloomberg macro strategist,

The Fed’s actions to stave off the banking crisis should not be taken as a loosening in financial conditions – far less QE – and in fact tighter conditions should be expected.

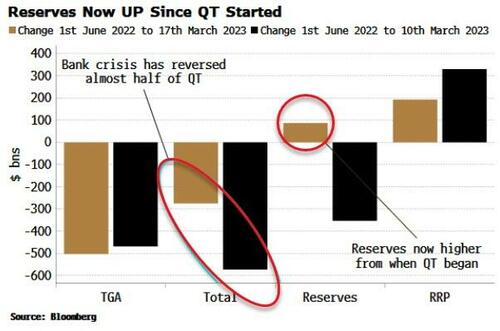

The banking crisis led to an almost $300 billion rise in the Fed’s balance sheet last week, reversing almost half of the decline since QT began last June.

But even more relevant is the change in reserves. Reserves are generally higher velocity, and therefore the true economic and financial impact from QT comes from the changes in reserves. Reserves are now actually higher than they were before QT began.

First of all, this is not QE. QE is the open-ended purchase of securities. The Fed’s new BTFP facility (to which much of the discount window lending is likely to migrate) is essentially a repo facility (although with no haircut) with a maturity of up to one year.

Furthermore it cannot be used as a limitless carry vehicle for banks to buy discounted debt, and repo it to the Fed at par. The small print shows that the BTFP can only be used for collateral that was owned by the borrower as of March 12.

Secondly, financial conditions are likely to tighten even as the Fed’s balance sheet has recently expanded. The reserves that are leaving the smaller banks in the shape of bank deposits are going to larger banks, who don’t want them (one reason why deposit rates have remained stubbornly low).

While bill rates are similar or lower to the rate offered by the RRP facility, much of the new reserves are poised to end up at the RRP, or the Treasury’s account at the Fed (the TGA) as they replenish it after any debt-ceiling resolution.

So new reserves created could soon end up in the “black-hole” of the RRP facility or the TGA, leading to a steep fall in money velocity and hence much tighter financial conditions.

Authored by Simon White, Bloomberg macro strategist,

The Fed’s actions to stave off the banking crisis should not be taken as a loosening in financial conditions – far less QE – and in fact tighter conditions should be expected.

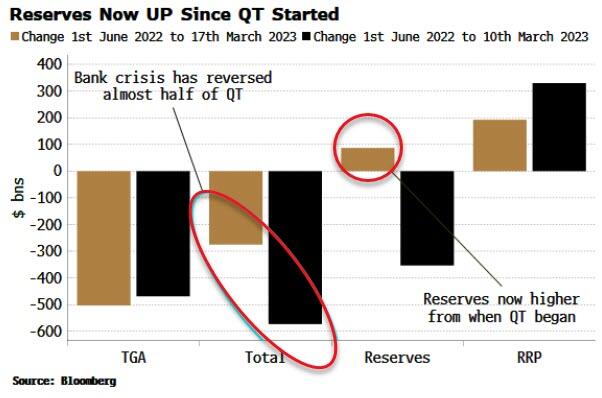

The banking crisis led to an almost $300 billion rise in the Fed’s balance sheet last week, reversing almost half of the decline since QT began last June.

But even more relevant is the change in reserves. Reserves are generally higher velocity, and therefore the true economic and financial impact from QT comes from the changes in reserves. Reserves are now actually higher than they were before QT began.

First of all, this is not QE. QE is the open-ended purchase of securities. The Fed’s new BTFP facility (to which much of the discount window lending is likely to migrate) is essentially a repo facility (although with no haircut) with a maturity of up to one year.

Furthermore it cannot be used as a limitless carry vehicle for banks to buy discounted debt, and repo it to the Fed at par. The small print shows that the BTFP can only be used for collateral that was owned by the borrower as of March 12.

Secondly, financial conditions are likely to tighten even as the Fed’s balance sheet has recently expanded. The reserves that are leaving the smaller banks in the shape of bank deposits are going to larger banks, who don’t want them (one reason why deposit rates have remained stubbornly low).

While bill rates are similar or lower to the rate offered by the RRP facility, much of the new reserves are poised to end up at the RRP, or the Treasury’s account at the Fed (the TGA) as they replenish it after any debt-ceiling resolution.

So new reserves created could soon end up in the “black-hole” of the RRP facility or the TGA, leading to a steep fall in money velocity and hence much tighter financial conditions.

Loading…