By Ven Ram, Bloomberg Markets Live reporter and strategist

For a big Fed day, the one aspect that traders are least riveted on is the decision itself. Given the recent progress on disinflation, the Fed has an ample-enough real policy rate to stand pat, so investors will look beyond the decision.

That means the dot plot, the summary of economic projections and Chair Jerome Powell’s post-meeting remarks are what will move Treasuries.

Dot plot & the summary of economic projections:

-

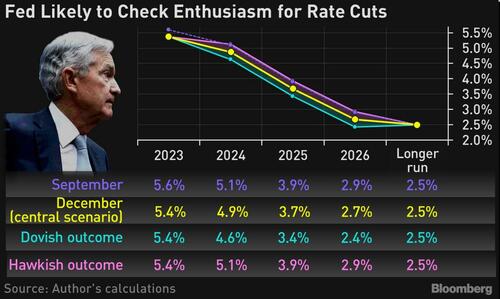

With core inflation still sticky at 4%, the Fed is unlikely to feel comfortable with recent market positioning that has swung between pricing 100 basis points and 125 basis points of cumulative rate cuts for 2024.

-

With financial conditions already considerably loose, the Fed has a lot at stake in showing its hand. It is unlikely, therefore, that its dot plot will show more than two rate cuts for 2024, a case laid out in detail here. It may also revise up its growth forecast for next year, both of which should send Treasury yields higher, especially at the front end.

-

Any upward revision of growth estimates will prolong the inversion in the yield curve.

-

The Fed’s implicit estimate of the real neutral rate will give us an inkling about how far its policy accommodation might go when it eventually pivots, but I don’t expect any change there.

Powell in the spotlight:

-

Powell will likely be asked if policymakers discussed rate cuts during their deliberations, though he will be at pains to emphasize that any talk of policy loosening at this stage is premature given the resilience of the real economy in general and, in particular, the labor market.

-

With the jobless rate having ticked lower in November, the Fed has its work cut out in sending a higher-for-longer message to the markets. At the moment, though, Treasuries are glossing over that prospect.

By Ven Ram, Bloomberg Markets Live reporter and strategist

For a big Fed day, the one aspect that traders are least riveted on is the decision itself. Given the recent progress on disinflation, the Fed has an ample-enough real policy rate to stand pat, so investors will look beyond the decision.

That means the dot plot, the summary of economic projections and Chair Jerome Powell’s post-meeting remarks are what will move Treasuries.

Dot plot & the summary of economic projections:

-

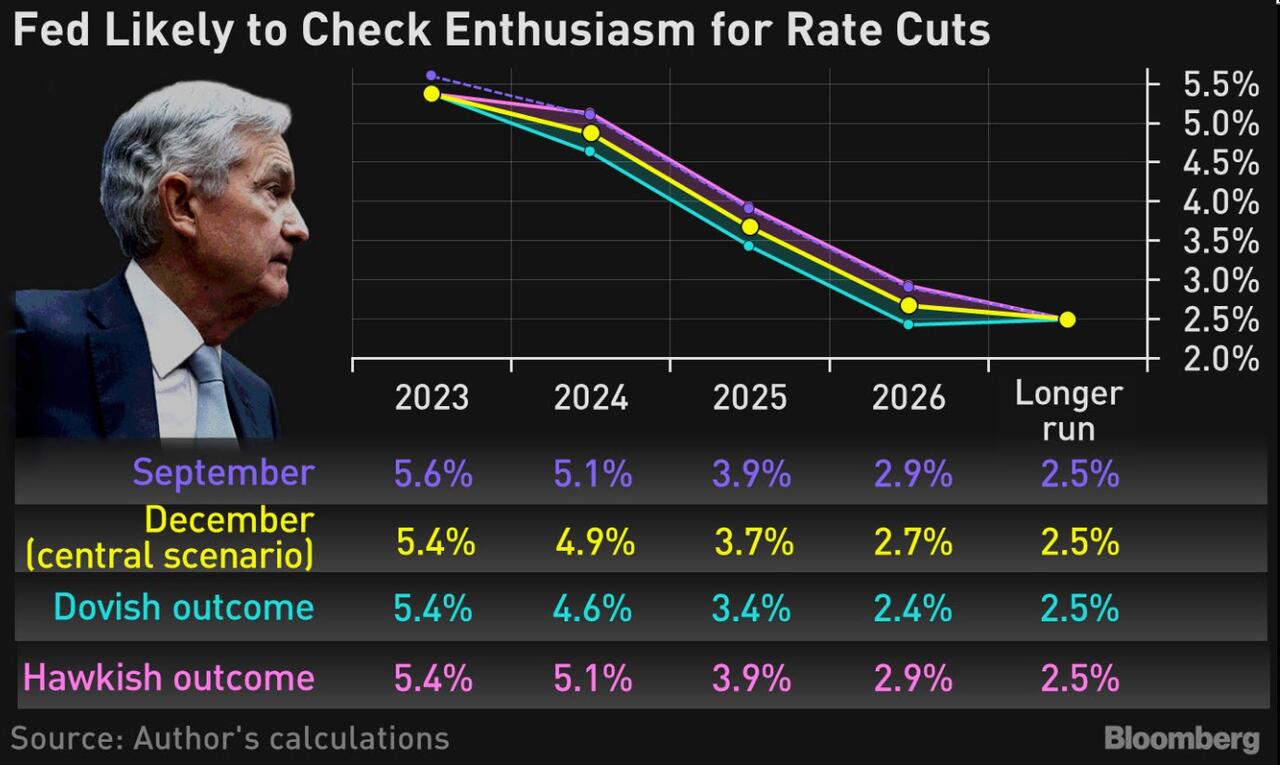

With core inflation still sticky at 4%, the Fed is unlikely to feel comfortable with recent market positioning that has swung between pricing 100 basis points and 125 basis points of cumulative rate cuts for 2024.

-

With financial conditions already considerably loose, the Fed has a lot at stake in showing its hand. It is unlikely, therefore, that its dot plot will show more than two rate cuts for 2024, a case laid out in detail here. It may also revise up its growth forecast for next year, both of which should send Treasury yields higher, especially at the front end.

-

Any upward revision of growth estimates will prolong the inversion in the yield curve.

-

The Fed’s implicit estimate of the real neutral rate will give us an inkling about how far its policy accommodation might go when it eventually pivots, but I don’t expect any change there.

Powell in the spotlight:

-

Powell will likely be asked if policymakers discussed rate cuts during their deliberations, though he will be at pains to emphasize that any talk of policy loosening at this stage is premature given the resilience of the real economy in general and, in particular, the labor market.

-

With the jobless rate having ticked lower in November, the Fed has its work cut out in sending a higher-for-longer message to the markets. At the moment, though, Treasuries are glossing over that prospect.

Loading…