By Bas van Geffen, senior macro strategist at Rabobank

In yesterday’s daily, we noted how an increasing number of US households is struggling to pay their utility bills. Yet, this situation pales in comparison to the price hikes that European consumers are facing. As a case in point, the OFGEM, UK’s energy regulator, lifted the energy price cap to £3,549 as of 1 October (from £1,971), adding a warning that prices could get “significantly worse” through 2023.

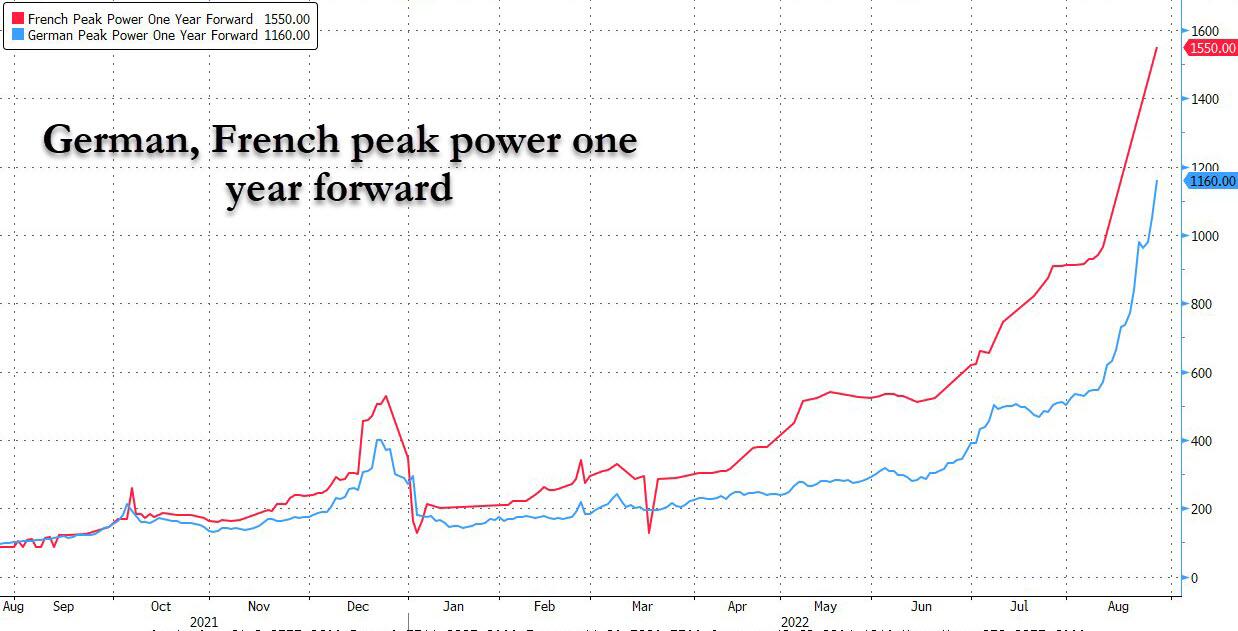

Indeed, yet another sharp move in European energy prices took benchmark rates to new record-highs. The 1 month forward Dutch TTF contract jumped to €311/MWh, while the 1 month French electricity contract reached a mindboggling €750/MWh. The fact that nobody wants to be short power right now certainly doesn’t help either as it reduces liquidity in the market – which may have been exacerbated by ICE’s decision to increase margin requirements on European gas futures.

These unfathomable price rises are adding pressure on European leaders to come up with a solution for the unfolding energy crisis that will stress many households. The Czech Prime Minister said he wants to push for an EU-wide response. One of the options that is being considered is a price cap on gas, but that leaves many risks and questions regarding the design and implementation of any such proposals.

All in all, these developments in the energy complex in Europe suggests that the acceleration in inflation that we pencilled in for Q4 may get more brutal – but so may the recession, if companies shut down production ‘voluntarily’ (i.e., due to production being uneconomical) or because they are forced to (i.e., rationing).

Even though monetary policy is powerless in such a situation –in the sense that higher rates will not solve the energy shortage– central bankers continue to debate over the value (or damage) of going an additional 25bp at their next policy meeting. The accounts of the July ECB meeting suggested that the central bank won’t slow its pace in the near-term as inflation continues to elude the central bank and risks becoming entrenched in expectations.

Yesterday’s accounts noted that “a very large number of members agreed that it was appropriate to raise the ECB’s key interest rates by 50 basis points”, although “some members argued in favour of 25bp” as this would be consistent with the Council’s earlier communication. As we already concluded after the meeting, this suggests that there was an intrinsic desire even amongst moderate doves to implement a bigger hike, and that it wasn’t a trade-off with the hawks in return for a more potent Transmission Protection Instrument. And even though President Lagarde described the 50bp move as ‘frontloading’, there was nothing in the accounts that suggested that this frontloading should be limited to just the previous meeting or that the ECB is now done with 50bp moves.

In fact, if anything, the discussion regarding the inflation outlook sounded quite hawkish. In summary, the Council concluded that inflation risks had intensified. But whereas Lagarde’s press conference mostly seemed to focus on increased short-term risks, the accounts show growing concern about the medium-term inflation outlook. According to some, even a recession would not necessarily diminish upside risks to inflation – and we would agree to the extent that higher gas prices are now the driving factor behind the worsening outlook for both prices and growth.

The ECB is clearly worried about inflation becoming entrenched in expectations. Although the Council concluded that there were no signs of significant second-round effects yet, repeated upward inflation surprises are increasing the probability of such effects. The ECB particularly seemed concerned about the latest surveys and market-based indicators of inflation expectations: “The probability that markets assigned to high inflation outcomes of above 4% over a five-year horizon five years ahead had risen steadily since the start of the year”, and nearly 20% of the SPF respondents saw inflation remain above 2.5%.

Moreover, the ECB acknowledged that the weak EUR/USD rate is currently mostly a headwind to the Eurozone, as more expensive energy outweighs the benefits of exporters becoming more competitive globally. Interestingly, some members seem to believe that they can prop up the currency with tighter policy. The ECB estimates that about half of the EUR’s depreciation since the start of the year could be attributed to the policy divergence between the Fed and the ECB. This could be another reason for the ECB to maintain -or even increase- the pace of hikes ahead. However, we still believe that this is futile. Given the current macroeconomic backdrop, it’s hard to see how bigger ECB hikes would fundamentally support the EUR – although the ECB may be able to stem the currency’s bleeding.

Day ahead

To that extent, Powell’s keynote speech at Jackson Hole today will be closely watched for hints of direction. With markets still somewhat hopeful that the Fed will make a “dovish pivot” before next summer, Powell’s remarks could make for an unwelcome hawkish wake-up call. That would also be a challenge for the ECB, to the extent that they continue to subscribe to the view that monetary policy differentials –rather than the weak Eurozone outlook and global risk aversion–are a key force behind EUR’s weakness, and hence imported inflation .

By Bas van Geffen, senior macro strategist at Rabobank

In yesterday’s daily, we noted how an increasing number of US households is struggling to pay their utility bills. Yet, this situation pales in comparison to the price hikes that European consumers are facing. As a case in point, the OFGEM, UK’s energy regulator, lifted the energy price cap to £3,549 as of 1 October (from £1,971), adding a warning that prices could get “significantly worse” through 2023.

Indeed, yet another sharp move in European energy prices took benchmark rates to new record-highs. The 1 month forward Dutch TTF contract jumped to €311/MWh, while the 1 month French electricity contract reached a mindboggling €750/MWh. The fact that nobody wants to be short power right now certainly doesn’t help either as it reduces liquidity in the market – which may have been exacerbated by ICE’s decision to increase margin requirements on European gas futures.

These unfathomable price rises are adding pressure on European leaders to come up with a solution for the unfolding energy crisis that will stress many households. The Czech Prime Minister said he wants to push for an EU-wide response. One of the options that is being considered is a price cap on gas, but that leaves many risks and questions regarding the design and implementation of any such proposals.

All in all, these developments in the energy complex in Europe suggests that the acceleration in inflation that we pencilled in for Q4 may get more brutal – but so may the recession, if companies shut down production ‘voluntarily’ (i.e., due to production being uneconomical) or because they are forced to (i.e., rationing).

Even though monetary policy is powerless in such a situation –in the sense that higher rates will not solve the energy shortage– central bankers continue to debate over the value (or damage) of going an additional 25bp at their next policy meeting. The accounts of the July ECB meeting suggested that the central bank won’t slow its pace in the near-term as inflation continues to elude the central bank and risks becoming entrenched in expectations.

Yesterday’s accounts noted that “a very large number of members agreed that it was appropriate to raise the ECB’s key interest rates by 50 basis points”, although “some members argued in favour of 25bp” as this would be consistent with the Council’s earlier communication. As we already concluded after the meeting, this suggests that there was an intrinsic desire even amongst moderate doves to implement a bigger hike, and that it wasn’t a trade-off with the hawks in return for a more potent Transmission Protection Instrument. And even though President Lagarde described the 50bp move as ‘frontloading’, there was nothing in the accounts that suggested that this frontloading should be limited to just the previous meeting or that the ECB is now done with 50bp moves.

In fact, if anything, the discussion regarding the inflation outlook sounded quite hawkish. In summary, the Council concluded that inflation risks had intensified. But whereas Lagarde’s press conference mostly seemed to focus on increased short-term risks, the accounts show growing concern about the medium-term inflation outlook. According to some, even a recession would not necessarily diminish upside risks to inflation – and we would agree to the extent that higher gas prices are now the driving factor behind the worsening outlook for both prices and growth.

The ECB is clearly worried about inflation becoming entrenched in expectations. Although the Council concluded that there were no signs of significant second-round effects yet, repeated upward inflation surprises are increasing the probability of such effects. The ECB particularly seemed concerned about the latest surveys and market-based indicators of inflation expectations: “The probability that markets assigned to high inflation outcomes of above 4% over a five-year horizon five years ahead had risen steadily since the start of the year”, and nearly 20% of the SPF respondents saw inflation remain above 2.5%.

Moreover, the ECB acknowledged that the weak EUR/USD rate is currently mostly a headwind to the Eurozone, as more expensive energy outweighs the benefits of exporters becoming more competitive globally. Interestingly, some members seem to believe that they can prop up the currency with tighter policy. The ECB estimates that about half of the EUR’s depreciation since the start of the year could be attributed to the policy divergence between the Fed and the ECB. This could be another reason for the ECB to maintain -or even increase- the pace of hikes ahead. However, we still believe that this is futile. Given the current macroeconomic backdrop, it’s hard to see how bigger ECB hikes would fundamentally support the EUR – although the ECB may be able to stem the currency’s bleeding.

Day ahead

To that extent, Powell’s keynote speech at Jackson Hole today will be closely watched for hints of direction. With markets still somewhat hopeful that the Fed will make a “dovish pivot” before next summer, Powell’s remarks could make for an unwelcome hawkish wake-up call. That would also be a challenge for the ECB, to the extent that they continue to subscribe to the view that monetary policy differentials –rather than the weak Eurozone outlook and global risk aversion–are a key force behind EUR’s weakness, and hence imported inflation .