It's not just today's cooler than expected CPI print that is sending stocks soaring, the S&P up 4.2% at last check, its biggest increase since April 2020: amid today's barrage of Fed speakers.

- 09:00: Fed’s Harker Discusses The Economic Outlook

- 09:35: Fed’s Logan Speaks at Energy and the Economy Conference

- 11:00: Fed’s Daly Speaks with European Economics & Financial Center

- 12:30: Fed’s Mester Discusses the Economic Outlook

- 13:30: Fed’s George Speaks at Energy and the Economy Conference

... the first two have already come out with decidedly more dovish jawboning, echoing last week's Fed statement (if not Powell's far more hawkish presser).

The first was Philly Fed president Patrick Harker who said Thursday that the U.S. central bank is approaching a point where it may be able to moderate the pace of its rate rise campaign aimed at lowering too high levels of inflation.

“In the upcoming months, in light of the cumulative tightening we have achieved, I expect we will slow the pace of our rate hikes as we approach a sufficiently restrictive stance,” Harker said in a speech text. But he added that moving from what had been 75 basis point increases to something like a half percentage point rise would still be significant action.

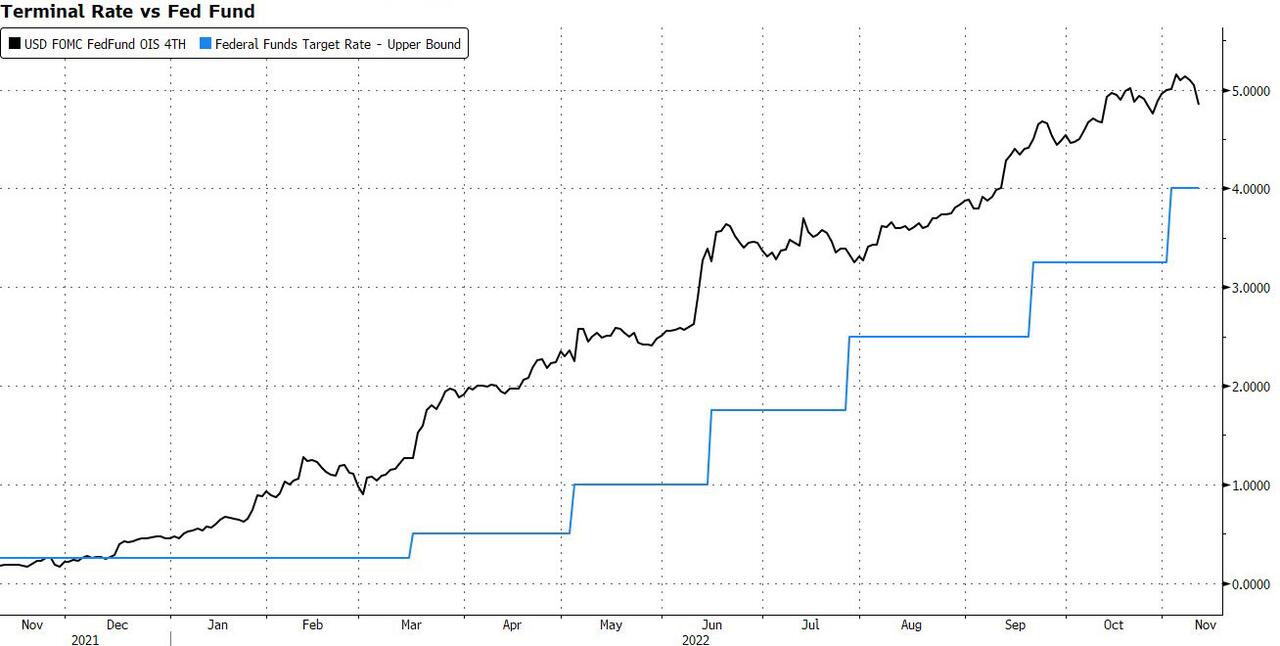

Harker added, “at some point next year, I expect we will hold at a restrictive rate for a while to let monetary policy do its work” as more expensive borrowing costs impact the economy. The central banker said what happens after that will be driven by the data and added “if we have to, we can always tighten further, based on the data.” Or, alternatively, the Fed will have just another 100bps more of rate hikes because as shown earlier, the terminal rate had slumped below 5% and now anticipates about 1% more in rate hikes before the Fed ends its tightening campaign.

Harker, who doesn’t hold a vote on the FOMC this year but will in 2023, laid out what it will take for him to call for a shift in monetary policy. “What we really need to see is a sustained decline in a number of inflation indicators before we let up on tightening monetary policy,” he said, adding “we need to make sure inflation expectations don’t become unanchored.”

To be sure, the Philly Fed president offered the token dose of hawkishness, but nothing the market hasn't heard a thousand times already: in his remarks, Harker said there are signs the economy is slowing but he added “the job market continues to run extremely hot” and inflation “remains far, far too high.” Well, check back next month on the employment number - with midterms over, the BLS can finally tell the truth.

Harker said in his speech that he believes the U.S. GDP will be flat for this year, rise by 1.5% next year and 2% in 2024. Unemployment should rise from its current 3.7% level to 4.5% next year before falling to 4% in 2024. He said there’s evidence the Fed can lower inflation “without doing unnecessary damage to the labor market.”

As for inflation, he said inflation as measured by the core personal consumption expenditures price index, which stood at 5.1% in September, should ease to 4.8% this year, 3.5% next year and 2.5% in 2024. The Fed’s target is 2%.

But far more important that non-voter Harker's speech is what the former head of the PPT and current Dallas Fed president, Lorie Logan said after today's CPI: speaking at a conference hosted by her bank in Houston on Thursday, she said that the Federal Reserve looked closer to moderating aggressive interest-rate increases after welcome news on inflation. More importantly, she emphasized that the Fed should start looking at financial conditions, a clear sign that the Fed is starting to pay attention not just to inflation and employment but how it's actions are breaking the market.

“While I believe it may soon be appropriate to slow the pace of rate increases so we can better assess how financial and economic conditions are evolving, I also believe a slower pace should not be taken to represent easier policy,” Logan said adding that “this morning’s CPI data were a welcome relief, but there is still a long way to go,” she said. Not only is inflation far above the Fed’s 2% target, “but with aggregate demand continuing to outstrip supply, inflation has repeatedly come in higher than forecasters expected.”

"I believe it may soon be appropriate to slow the pace of rate increases so we can better assess how financial and economic conditions are evolving," Logan added even as she warned markets not to confuse a slower pace of monetary policy tightening with easier policy.

Last but not least, Powell's own mouthpiece, WSJ's Nick Timiraos said that "the October inflation report is likely to keep the Fed on track to approve a 50-basis-point interest-rate increase next month. Officials had already signaled they wanted to slow the pace of rises and were somewhat insensitive to near-term inflation data."

Fed officials have signaled they would prefer to see evidence that inflation is moderating before they pause rate rises.

— Nick Timiraos (@NickTimiraos) November 10, 2022

The hot August and September CPI prints restarted the clock on gathering a string of sequential moderations in inflation.

And in a subsequent tweet, Timiraos confirmed that the Fed's attention is now turning to financial conditions:

Dallas Fed President Lorie Logan: The Fed must get inflation down but "we should also try, if we can, to avoid incurring costs that are higher than necessary."

— Nick Timiraos (@NickTimiraos) November 10, 2022

Financial conditions can eventually tighten in ways that aren't linear. https://t.co/QHhA1k8FGs pic.twitter.com/o7nh3PkeXa

News of the better-than-expected CPI report sent bond yields plummeting and saw investors harden bets that the Fed would scale back the size of its next rate increase in December to 50 basis points, with rates peaking around 4.8% next year. And sure enough, odds of the December rate hike have collapsed to 0% after the CPI, while odds of a 50bps hike are now 100%.

What happens after December, will depend on next month's jobs report. And if recent mass layoffs are any indication, not to mention that the midterms are now history, we are looking at a deeply payrolls negative number next month.

It’s not just today’s cooler than expected CPI print that is sending stocks soaring, the S&P up 4.2% at last check, its biggest increase since April 2020: amid today’s barrage of Fed speakers.

- 09:00: Fed’s Harker Discusses The Economic Outlook

- 09:35: Fed’s Logan Speaks at Energy and the Economy Conference

- 11:00: Fed’s Daly Speaks with European Economics & Financial Center

- 12:30: Fed’s Mester Discusses the Economic Outlook

- 13:30: Fed’s George Speaks at Energy and the Economy Conference

… the first two have already come out with decidedly more dovish jawboning, echoing last week’s Fed statement (if not Powell’s far more hawkish presser).

The first was Philly Fed president Patrick Harker who said Thursday that the U.S. central bank is approaching a point where it may be able to moderate the pace of its rate rise campaign aimed at lowering too high levels of inflation.

“In the upcoming months, in light of the cumulative tightening we have achieved, I expect we will slow the pace of our rate hikes as we approach a sufficiently restrictive stance,” Harker said in a speech text. But he added that moving from what had been 75 basis point increases to something like a half percentage point rise would still be significant action.

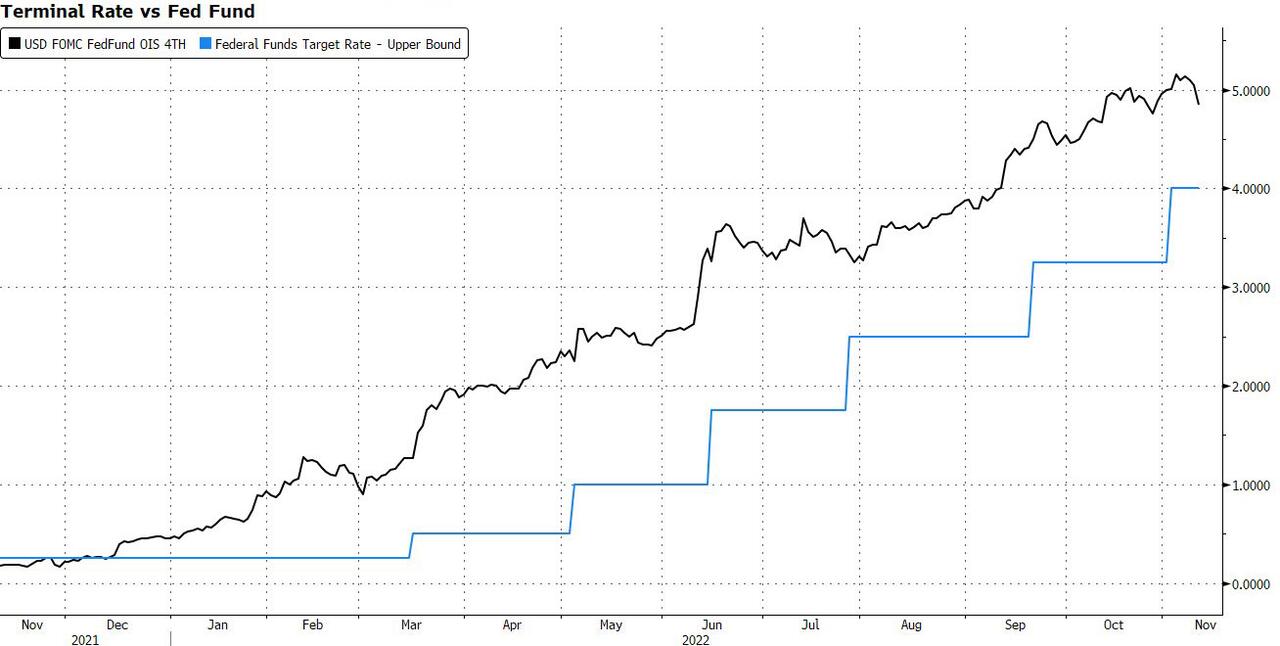

Harker added, “at some point next year, I expect we will hold at a restrictive rate for a while to let monetary policy do its work” as more expensive borrowing costs impact the economy. The central banker said what happens after that will be driven by the data and added “if we have to, we can always tighten further, based on the data.” Or, alternatively, the Fed will have just another 100bps more of rate hikes because as shown earlier, the terminal rate had slumped below 5% and now anticipates about 1% more in rate hikes before the Fed ends its tightening campaign.

Harker, who doesn’t hold a vote on the FOMC this year but will in 2023, laid out what it will take for him to call for a shift in monetary policy. “What we really need to see is a sustained decline in a number of inflation indicators before we let up on tightening monetary policy,” he said, adding “we need to make sure inflation expectations don’t become unanchored.”

To be sure, the Philly Fed president offered the token dose of hawkishness, but nothing the market hasn’t heard a thousand times already: in his remarks, Harker said there are signs the economy is slowing but he added “the job market continues to run extremely hot” and inflation “remains far, far too high.” Well, check back next month on the employment number – with midterms over, the BLS can finally tell the truth.

Harker said in his speech that he believes the U.S. GDP will be flat for this year, rise by 1.5% next year and 2% in 2024. Unemployment should rise from its current 3.7% level to 4.5% next year before falling to 4% in 2024. He said there’s evidence the Fed can lower inflation “without doing unnecessary damage to the labor market.”

As for inflation, he said inflation as measured by the core personal consumption expenditures price index, which stood at 5.1% in September, should ease to 4.8% this year, 3.5% next year and 2.5% in 2024. The Fed’s target is 2%.

But far more important that non-voter Harker’s speech is what the former head of the PPT and current Dallas Fed president, Lorie Logan said after today’s CPI: speaking at a conference hosted by her bank in Houston on Thursday, she said that the Federal Reserve looked closer to moderating aggressive interest-rate increases after welcome news on inflation. More importantly, she emphasized that the Fed should start looking at financial conditions, a clear sign that the Fed is starting to pay attention not just to inflation and employment but how it’s actions are breaking the market.

“While I believe it may soon be appropriate to slow the pace of rate increases so we can better assess how financial and economic conditions are evolving, I also believe a slower pace should not be taken to represent easier policy,” Logan said adding that “this morning’s CPI data were a welcome relief, but there is still a long way to go,” she said. Not only is inflation far above the Fed’s 2% target, “but with aggregate demand continuing to outstrip supply, inflation has repeatedly come in higher than forecasters expected.”

“I believe it may soon be appropriate to slow the pace of rate increases so we can better assess how financial and economic conditions are evolving,” Logan added even as she warned markets not to confuse a slower pace of monetary policy tightening with easier policy.

Last but not least, Powell’s own mouthpiece, WSJ’s Nick Timiraos said that “the October inflation report is likely to keep the Fed on track to approve a 50-basis-point interest-rate increase next month. Officials had already signaled they wanted to slow the pace of rises and were somewhat insensitive to near-term inflation data.”

Fed officials have signaled they would prefer to see evidence that inflation is moderating before they pause rate rises.

The hot August and September CPI prints restarted the clock on gathering a string of sequential moderations in inflation.

— Nick Timiraos (@NickTimiraos) November 10, 2022

And in a subsequent tweet, Timiraos confirmed that the Fed’s attention is now turning to financial conditions:

Dallas Fed President Lorie Logan: The Fed must get inflation down but “we should also try, if we can, to avoid incurring costs that are higher than necessary.”

Financial conditions can eventually tighten in ways that aren’t linear. https://t.co/QHhA1k8FGs pic.twitter.com/o7nh3PkeXa

— Nick Timiraos (@NickTimiraos) November 10, 2022

News of the better-than-expected CPI report sent bond yields plummeting and saw investors harden bets that the Fed would scale back the size of its next rate increase in December to 50 basis points, with rates peaking around 4.8% next year. And sure enough, odds of the December rate hike have collapsed to 0% after the CPI, while odds of a 50bps hike are now 100%.

What happens after December, will depend on next month’s jobs report. And if recent mass layoffs are any indication, not to mention that the midterms are now history, we are looking at a deeply payrolls negative number next month.