By Michael Msika, Bloomberg Markets Live reporter and analyst

Growing worries over a recession and the cumulative effect of months of interest rate hikes mean equity investors have plenty on their minds. Violent protests in France have added an extra layer of concern in one of Europe’s top-performing markets.

The CAC 40 is up 9.5% this year, trailing only Italy’s FTSE MIB among the major European benchmarks, with a stellar lineup of luxury names boosted by bets on China’s economic reopening. Now, the case for French stocks is being challenged by days of confrontations on the streets over pension reform that could damage investor sentiment.

“Surveys suggest the economy is holding up well so far and may even manage to expand slightly in the first quarter,” says Bloomberg economist Maeva Cousin. “But as social tensions persist, adding to the tightening of monetary conditions and heightened financial uncertainty, risks for the rest of 2023 appear increasingly tilted to the downside.”

Anger over the plan to raise the retirement age to 64 from 62 — which has won support from the OECD — boiled over when the government said March 16 it would push the bill through parliament without a vote. Judging by past episodes of national protest, like the Yellow Vest movement which started in 2018, the hospitality and transport industries will be worst affected, while the overall result representing a loss of roughly than 0.1% of GDP in the first quarter, according to

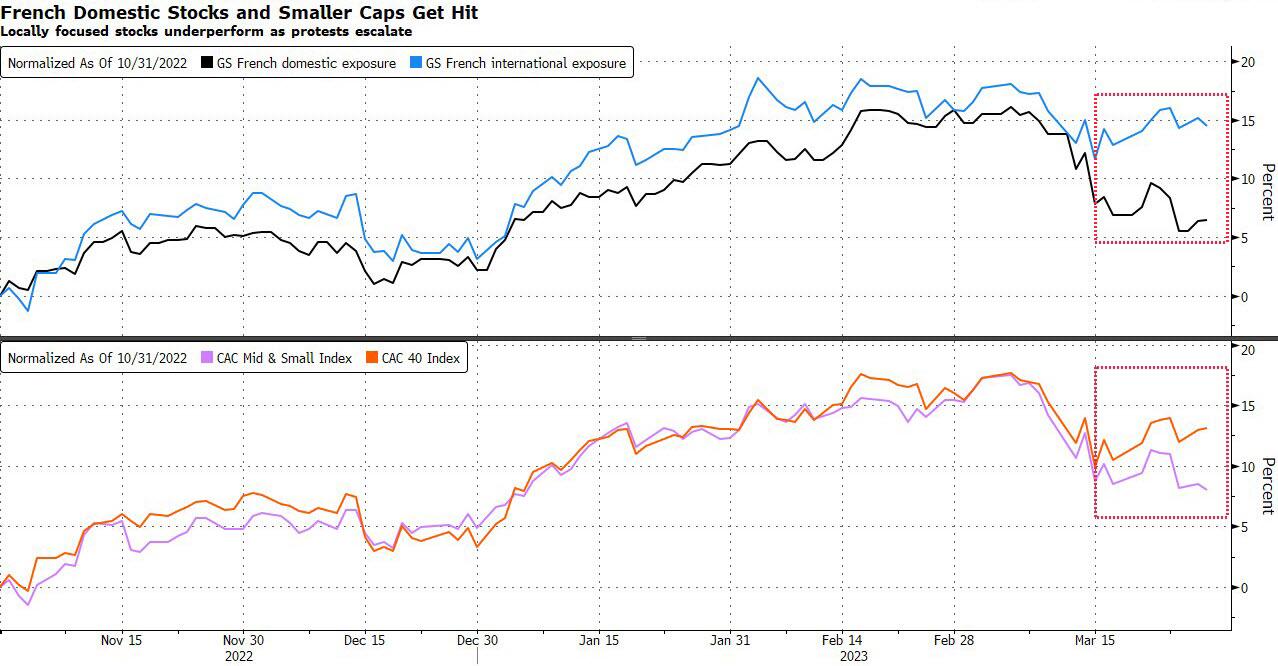

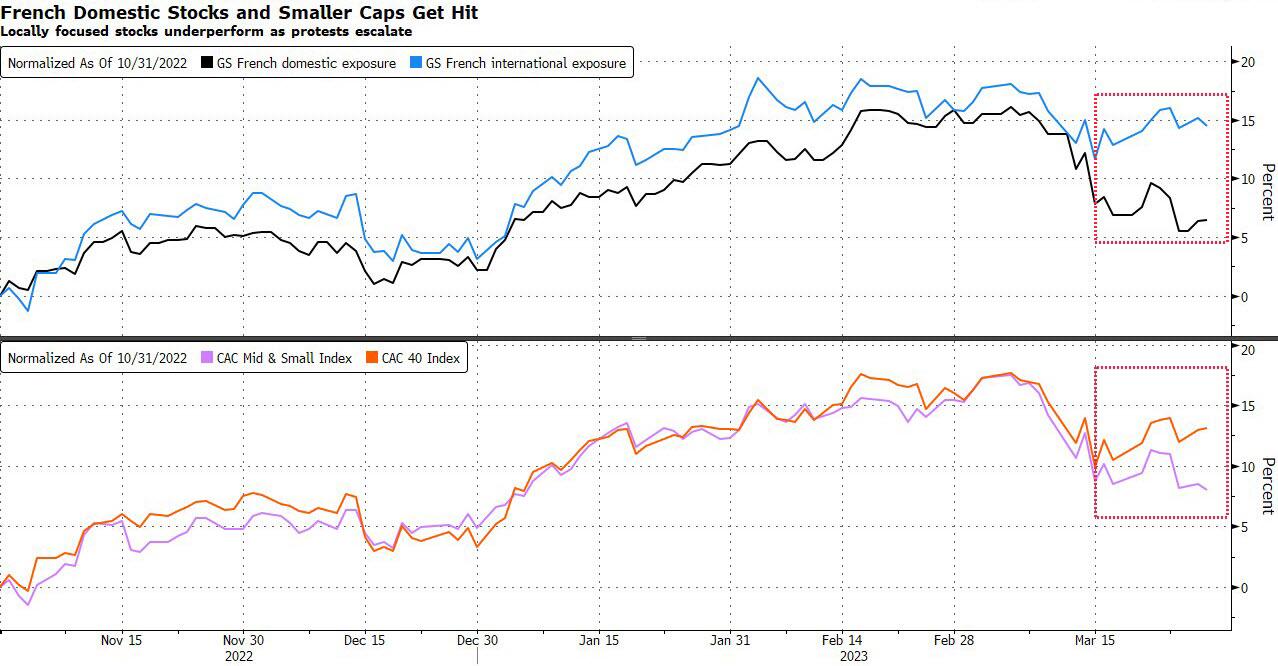

Domestic stocks are likely to feel the most pain. A Goldman Sachs basket of French companies with a high reliance on the local economy has underperformed internationally exposed peers by more than five percentage points since March 13. This group includes the likes of Carrefour, Vinci, Bouygues, Gecina, Getlink and Orange.

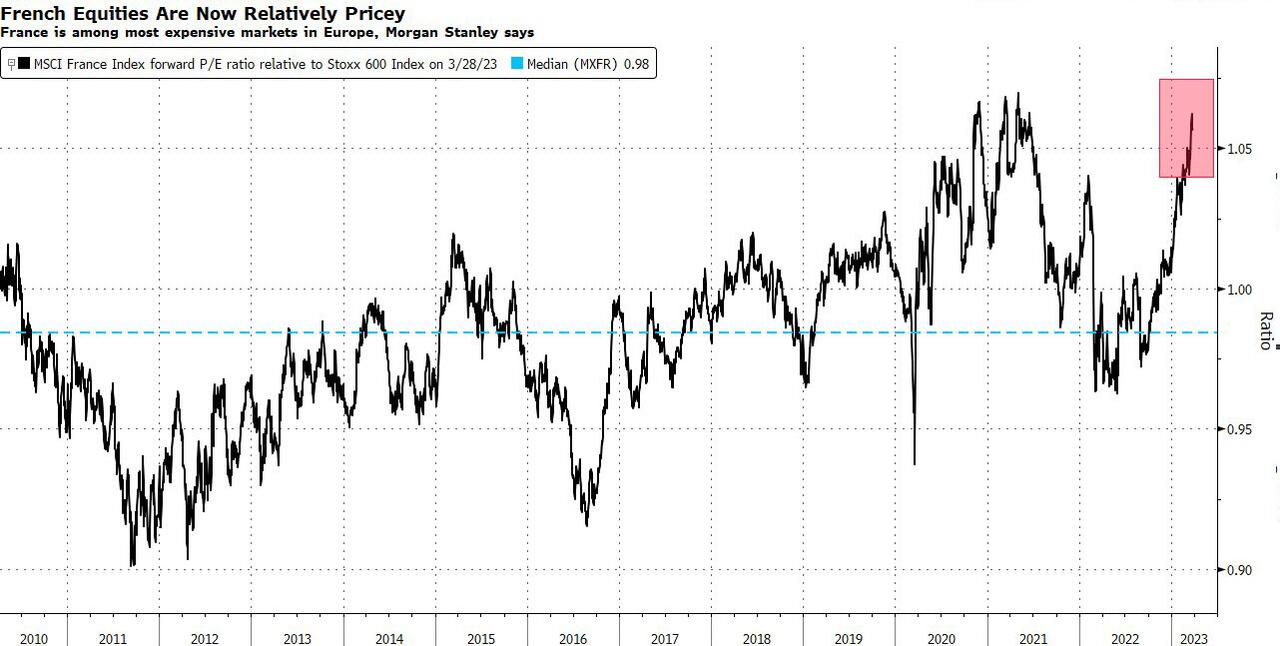

The other problem for the French equity market is that it has become among the most expensive in Europe, based on relative valuations compared with 10-year averages and measured against several metrics, according to Morgan Stanley strategists.

French blue chips have little exposure to their home country. CAC 40 members generate only 16% of their sales domestically, according to Goldman strategists. The index has a high weighting in companies with a global reach, like luxury, commodities and health care stocks. Locally focused utilities, telecoms, real estate and financials make up just 13% of the benchmark. Still, while luxury stocks get a modest 10% of their sales in France, tourists account for a healthy slice of that.

“Disruption to the economy is so far limited but could rise as we are now seeing more strikes,” says Bloomberg Intelligence strategist Laurent Douillet, adding that April’s readings on economic activity will be revealing. “Given that a large portion of merchandise transport is done by road, protests by truck drivers and road/refineries blockades are important to watch.”

Tourism has started to be affected, Douillet says, with hotels reporting cancellations running as high as 25% over the past two weeks as television images of clashes in Paris and piles of rubbish on the streets prompt foreigners to postpone trips. While a strike by refuse collection workers is due to be suspended Wednesday, France has asked airlines to cancel 20% to 25% of flights on Thursday and Friday.

In February, France’s national statistic agency published a note in which it said past social movements such as in 1995 and 2019 had little impact on economic output with activity catching up during the quarter following the disruption. It added that home working introduced during the Covid lockdown was also likely to mitigate the effect of disruptions.

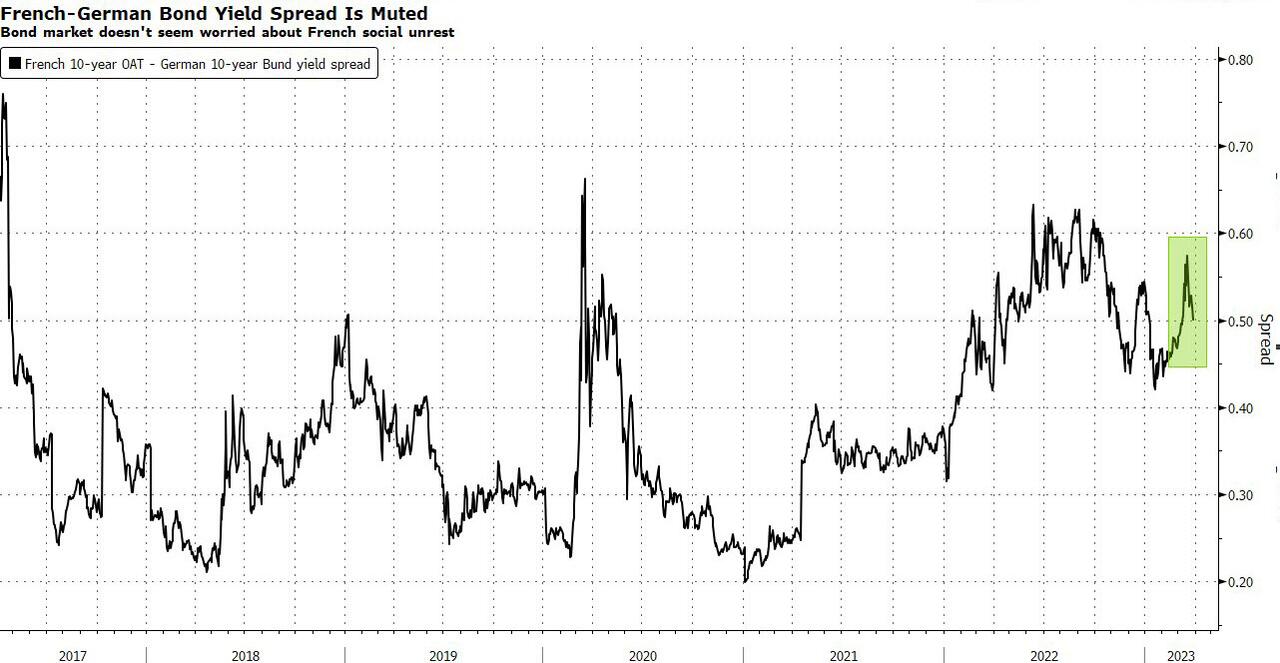

“It is too early to fully assess the impact of French strikes on economic dynamics, but we can already assume that the government will come out weaker from this episode, making other key reforms or budget deficit reduction difficult to pass in the next year or so,” says Stephanie de Torquat, chief economist at SILEX. “Anyhow, the context of high inflation and rapid monetary policy tightening by the ECB will likely remain the most important driver of slower growth in the quarters to come.”

By Michael Msika, Bloomberg Markets Live reporter and analyst

Growing worries over a recession and the cumulative effect of months of interest rate hikes mean equity investors have plenty on their minds. Violent protests in France have added an extra layer of concern in one of Europe’s top-performing markets.

The CAC 40 is up 9.5% this year, trailing only Italy’s FTSE MIB among the major European benchmarks, with a stellar lineup of luxury names boosted by bets on China’s economic reopening. Now, the case for French stocks is being challenged by days of confrontations on the streets over pension reform that could damage investor sentiment.

“Surveys suggest the economy is holding up well so far and may even manage to expand slightly in the first quarter,” says Bloomberg economist Maeva Cousin. “But as social tensions persist, adding to the tightening of monetary conditions and heightened financial uncertainty, risks for the rest of 2023 appear increasingly tilted to the downside.”

Anger over the plan to raise the retirement age to 64 from 62 — which has won support from the OECD — boiled over when the government said March 16 it would push the bill through parliament without a vote. Judging by past episodes of national protest, like the Yellow Vest movement which started in 2018, the hospitality and transport industries will be worst affected, while the overall result representing a loss of roughly than 0.1% of GDP in the first quarter, according to

Domestic stocks are likely to feel the most pain. A Goldman Sachs basket of French companies with a high reliance on the local economy has underperformed internationally exposed peers by more than five percentage points since March 13. This group includes the likes of Carrefour, Vinci, Bouygues, Gecina, Getlink and Orange.

The other problem for the French equity market is that it has become among the most expensive in Europe, based on relative valuations compared with 10-year averages and measured against several metrics, according to Morgan Stanley strategists.

French blue chips have little exposure to their home country. CAC 40 members generate only 16% of their sales domestically, according to Goldman strategists. The index has a high weighting in companies with a global reach, like luxury, commodities and health care stocks. Locally focused utilities, telecoms, real estate and financials make up just 13% of the benchmark. Still, while luxury stocks get a modest 10% of their sales in France, tourists account for a healthy slice of that.

“Disruption to the economy is so far limited but could rise as we are now seeing more strikes,” says Bloomberg Intelligence strategist Laurent Douillet, adding that April’s readings on economic activity will be revealing. “Given that a large portion of merchandise transport is done by road, protests by truck drivers and road/refineries blockades are important to watch.”

Tourism has started to be affected, Douillet says, with hotels reporting cancellations running as high as 25% over the past two weeks as television images of clashes in Paris and piles of rubbish on the streets prompt foreigners to postpone trips. While a strike by refuse collection workers is due to be suspended Wednesday, France has asked airlines to cancel 20% to 25% of flights on Thursday and Friday.

In February, France’s national statistic agency published a note in which it said past social movements such as in 1995 and 2019 had little impact on economic output with activity catching up during the quarter following the disruption. It added that home working introduced during the Covid lockdown was also likely to mitigate the effect of disruptions.

“It is too early to fully assess the impact of French strikes on economic dynamics, but we can already assume that the government will come out weaker from this episode, making other key reforms or budget deficit reduction difficult to pass in the next year or so,” says Stephanie de Torquat, chief economist at SILEX. “Anyhow, the context of high inflation and rapid monetary policy tightening by the ECB will likely remain the most important driver of slower growth in the quarters to come.”

Loading…