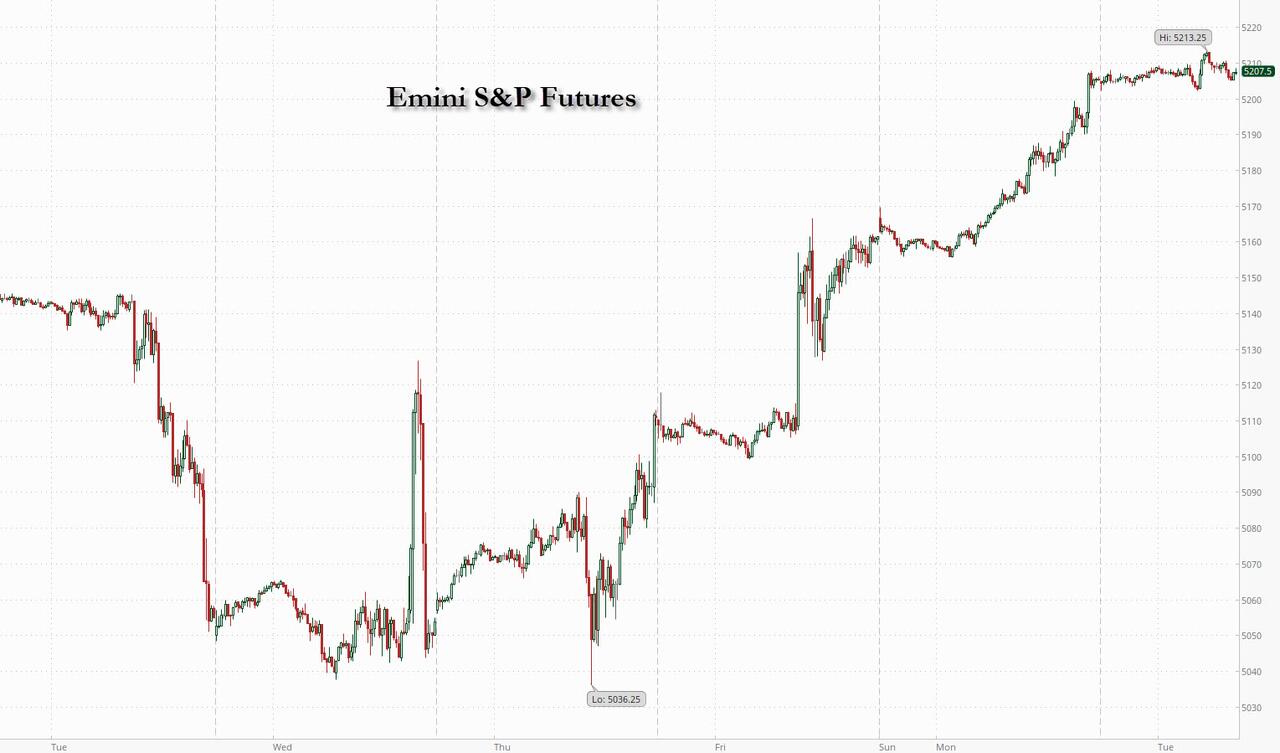

US stock futures are flat after the S&P 500 and Nasdaq 100 both closed 1% higher on Monday, helped by growing optimism among investors that the economy is finally slowing greenlighting earlier rate cuts by the Fed. As of 8:00am ET S&P futures were unchanged at 5,206, trading about 1% above its 50DMA, while Nasdaq futures were down 0.2% amid some mega-cap weakness. European stocks are higher, while indexes in Japan and the UK are catching up after being closed for holidays yesterday. Shares in Swiss bank UBS jumped after it returned to profit and showed more progress in its integration of Credit Suisse. Treasuries rise, with US 10-year yields falling 3bps to 4.46%. The Bloomberg Dollar Spot Index rises 0.1%. The yen weakens 0.4% against the greenback, pushing USD/JPY up to ~154.50. The Aussie falls 0.4% after the RBA kept rates on hold and maintained a neutral stance. Oil prices advance, with WTI rising 0.3% to trade near $78.70. Spot gold falls 0.4% and bitcoin traded in a range around $64,000 with the now daily European open/US slam down pattern. US economic data slate includes March consumer credit at 3pm, while Fed's Kashkari is scheduled to speak twice (11:30am, 1:20pm).

In premarket trading, Disney reported fiscal second-quarter profit that beat estimates, thanks to sharply narrower losses in its streaming TV business and higher ticket prices at theme parks. Still, the stock tumbled 6% after the company reported fewer subscribers to its Disney+ streaming service in the fiscal second quarter than analysts had projected. Here are some of the other notable US movers before the opening bell:

- Celsius falls 8.4% after the energy-drink maker reported first-quarter revenue that missed even the lowest estimate among analysts tracked by Bloomberg.

- Coherent climbs 8.5% after the maker of components for the telecommunications industry raised the bottom end of its year revenue forecast.

- Datadog slips 11% after the cloud software company said that Amit Agarwal will be stepping down as president. The company also posted 1Q results.

- Esperion Therapeutics rallies 25% after the drugmaker’s first-quarter revenue was ahead of analyst estimates.

- Fidelity National Information Services’ rises 4% after the company raised its outlook for full-year profit.

- Gap rises 3% after Citi raised its rating on the retailer to buy on positive momentum and margin upside.

- Hims & Hers Health jumps 14% after the telehealth company boosted its adjusted Ebitda guidance for the full year.

- Lucid drops 8% after the EV maker posted a wider-than-expected loss for the first quarter.

- Oscar Health climbs 15% after the health insurer reported earnings per share for the first quarter that outpaced Wall Street’s expectations.

- Palantir falls 13% as the market appeared unimpressed by the company’s outlook for annual sales after the stock has tripled in the past year.

- Symbotic jumps 14% after the warehouse robotics and automation firm posted forecast-beating 2Q revenue and surpassed expectations for its fiscal 3Q revenue outlook.

- Vimeo gains 10% after the video software company reported first-quarter results that beat analyst expectations and provided a forecast.

- Zeta rises 16% after the software company gave a forecast revenue for the second quarter that beat the average analyst estimate.

In a week light on data but heavy on Fedspeak, Minneapolis Fed President Neel Kashkari is set to appear Tuesday, one day after his Richmond President colleague Thomas Barkin said Monday said he expects high interest rates to eventually cool US inflation to the central bank’s 2% target. Despite the hawkish rhetoric, swaps traders are betting on about 45 basis points of Fed rate cuts by December, an increase vs before the disappointing jobs report.

“In this environment of growth not rolling over as much as we feared and potentially cuts coming in, there is upside for earnings going forward,” Beata Manthey, head of European equity strategy at Citigroup Inc., said in an interview with Bloomberg TV

"The market is taking a positive view about the US job data and anticipating that the Fed will indeed be able to cut rates," said Arnaud Girod, head of economics and cross-asset strategy at Kepler Cheuvreux in Paris.

European stocks rose for the third consecutive session, boosted by solid company earnings and renewed optimism the Federal Reserve will cut interest rates later this year. The Stoxx 600 is up 0.6%. UBS jumps more than 8% after it returned to profit and UniCredit climbed on better-than-forecast results. German semiconductor-maker Infineon Technologies AG cut its revenue forecast, signaling demand from the automotive industry remains weak.

Earlier in the session, Asia’s equity benchmark traded little changed on Tuesday as a catch-up rally in Korean and Japanese stocks on their return from a holiday was offset by declines in Hong Kong. The MSCI Asia Pacific Index rose 0.1% after capping a three-day gain on Monday. Technology was the best-performing sector in the region, much like in the US session overnight, amid rising hopes that the Federal Reserve may cut interest rates this year. Shares of Samsung Electronics and SK Hynix were the biggest contributors to gains on South Korea’s Kospi Index, which jumped 2%, the most in Asia. Shares in Hong Kong fell, with the Hang Seng Index snapping a 10-day winning streak that was the longest since 2018 amid some concern that the rally is overdone.

In FX, the Bloomberg Dollar Spot Index rose 0.1%, marking the second consecutive session of gains, as the greenback rose against most Group-of-10 currencies. The yen weakens 0.4% against the greenback, pushing USD/JPY up to ~154.50. The Aussie falls 0.4% after the RBA kept rates on hold and maintained a neutral stance.

- AUD/USD led losses falling as much as 0.6% to 0.6587, following the RBA’s interest rate decision; Australia’s central bank opted to maintain policy but markets likely expected the RBA to revert to prior guidance that a further increase in interest rates couldn’t be ruled out

- USD/JPY rose as much as 0.5% to 154.65, the highest level since May. 2, BOJ Governor Kazuo Ueda said he’s carefully watching the impact of the weak yen on prices and that he discussed recent moves with Prime Minister Fumio Kishida

- EUR/USD fell as much as 0.1% to 1.0754; German factory orders dropped 0.4% month-on-month in line with expectations, while eurozone March retail sales were up 0.8% from February

In rates, treasuries rose with US 10-year yields falling 3bps to 4.46%. Treasuries were underpinned by bigger gains in core European rates after Germany factory orders unexpectedly declined, pointing to persistent economic headwinds. During Asia session, Treasury futures drew support from dovish reaction to RBA maintaining its neutral bias, keeping interest rates at 4.35%. Focal points of US session include 3-year note auction, ahead of 10- and 30-year sales Wednesday and Thursday. US yields richer by 2bp to 3bp with the curve extending Monday’s flattening move; 10-year around 4.46% is ~2.5bp richer on the day with bunds and gilts outperforming by 1bp and 5bp in the sector. Treasury auction cycle begins at 1pm New York time with $58b 3-year note sale; $42b 10-year and $25b 30-year new issues follow Wednesday and Thursday.

In commodities, oil prices advance, with WTI rising 0.3% to trade near $78.70. Spot gold falls 0.4%.

In crypto, Bitcoin firmer today and has reclaimed the USD 64k handle, with Ethereum now holding around USD 3.2k.

Looking at today's calendar, US economic data slate includes March consumer credit at 3pm. Fed members’ scheduled speeches include Kashkari (11:30am, 1:20pm). Elsewhere we get, German March trade balance and factory orders data, French Q1 wages and Eurozone March retail sales. And as the earnings season continues to wind down, releases include Walt Disney, BP, Arista Networks, Duke Energy, McKesson, and Ferrari.

Market Snapshot

- S&P 500 futures little changed at 5,207.25

- STOXX Europe 600 up 0.6% to 511.10

- MXAP up 0.3% to 178.44

- MXAPJ up 0.3% to 552.71

- Nikkei up 1.6% to 38,835.10

- Topix up 0.6% to 2,746.22

- Hang Seng Index down 0.5% to 18,479.37

- Shanghai Composite up 0.2% to 3,147.74

- Sensex down 0.4% to 73,564.94

- Australia S&P/ASX 200 up 1.4% to 7,793.32

- Kospi up 2.2% to 2,734.36

- German 10Y yield little changed at 2.44%

- Euro little changed at $1.0762

- Brent Futures up 0.3% to $83.59/bbl

- Brent Futures up 0.3% to $83.58/bbl

- Gold spot down 0.3% to $2,315.95

- US Dollar Index up 0.16% to 105.22

Top Overnight News

- RBA leaves rates unchanged (as expected) and suggests there won’t by any additional hikes but also doesn’t seem in a rush to ease (new forecasts show no rate cuts until 2025). RTRS

- Taiwan’s CPI for Apr comes in below expectations, w/the headline number at +1.95% (vs. the Street +2.2% and down from +2.15% in Mar). BBG

- China tightened rules for hedge funds, raising the minimum-asset threshold of the 5.5 trillion yuan ($762 billion) industry while imposing restrictions on the use of derivatives and leverage. BBG

- Israel sent ground troops into Rafah on Monday night, seizing the main border crossing between Gaza and Egypt as international mediators struggled to continue talks aimed at ending the conflict. FT

- BP ended a mixed set of Big Oil results by maintaining share buybacks even as profit and cash flow fell more than expected. Aramco will pay $31 billion in dividends to the Saudi government and other investors despite lower profit. BBG

- UBS returned to profit with wealth management and the investment bank driving the beat. The firm targets another $1.5 billion in cost savings by year-end but sees integration expenses of $1.3 billion this quarter, and cautioned that the Swiss central bank’s recent rate cut will hurt NII. The stock climbed. BBG

- Social Security and Medicare will exhaust their funds in a little more than 10 years unless action is taken to address the shortfalls (although the new exhaustion dates for Social Security and Medicare are 1 and 5 years later than the prior forecasts). CNN

- Citigroup CEO Jane Fraser said Monday that consumer behavior has diverged as inflation for goods and services makes life harder for many Americans. Fraser, who leads one of the largest U.S. credit card issuers, said she is seeing a “K-shaped consumer.” That means the affluent continue to spend, while lower-income Americans have become more cautious with their consumption. CNBC

- AAPL has been working on its own chip designed to run artificial intelligence software in data center servers, a move that has the potential to give the company an advantage in the AI arms race. WSJ

- Donald Trump’s prized Manhattan office tower at 40 Wall St. is getting swept up by the worst storm to hit the office market since the global financial crisis. Like thousands of other U.S. office buildings, 40 Wall is now under duress because of weakening office demand. WSJ

Earnings

- Infineon (IFX GY) Q2 (EUR): Revenue 3.63bln (exp. 3.6bln), adj. EPS 0.42 (exp. 0.38), Gross Margin 38.6% (exp. 39.8%).

- BP (BP/ LN) Q1 (USD): Adj. Net 2.72bln (exp. 2.92bln). Revenue 49.96bln (exp. 52.44bln). Adj. EPS 0.16 (exp. 0.17). Dividend 0.0727 (exp. 0.0730)Announces USD 1.75bln share buyback for Q1. Continues to expect 2024 Capex around USD 16bln.

- Nintendo (7974 JT) 2023/24 (JPY): Net 490.6bln, +13.4%; Operating 528bln, +4.9%; Recurring 680bln, +13.2%. Sold 15.7mln Switch consoles in FY23/24 (exp. 15.5mln, prev. 17.9mln FY22/23). To make an announcement on a Switch successor in FY24; will not be announcing anything re. successor hardware at Nintendo Direct in June.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed as the region only partly sustained the momentum from Wall St where the major indices extended on post-NFP advances amid rate cut hopes, while key markets returned from the long weekend. ASX 200 traded higher with a further boost in late trade after the RBA proved to be less hawkish than many feared. Nikkei 225 gained on return from holiday as it took its first opportunity to react to last week's NFP report and renewed US rate cut hopes. Hang Seng & Shanghai Comp were subdued with the former set to snap its 10-day win streak and longest consecutive run of gains since 2018, while the mainland index took a breather after yesterday's catch-up rally amid a lack of fresh catalysts.

Top Asian News

- US will host China's special envoy for climate change Liu Zhenmin in Washington on May 8th-9th, according to the State Department.

- Japanese top FX diplomat Kanda said it is important for currencies to move in a stable manner reflecting fundamentals and the government must take appropriate steps if there's excessive volatility in the FX market, while he added it is usual that they don't comment whether currency intervention was carried out.

- RBA kept the Cash Rate Target unchanged at 4.35%, as expected, while it reiterated the Board remains resolute in its determination to return inflation to the target and it is not ruling anything in or out. RBA stated that returning inflation to the target within a reasonable timeframe remains the board’s highest priority, as well as noted that inflation remains high and is falling more gradually than expected. Furthermore, the RBA raised its inflation forecasts for 2024 but trimmed forecasts for GDP and unemployment, while its forecasts assume that rates will stay at 4.35% until mid-2025 which is nine months longer than previously assumed.

- RBA's Bullock says they must be vigilant on inflation risks, believe rates are at the correct level to get inflation back to target. Board discussed the option of hiking. Will tighten if necessary, do not think they necessarily have to tighten again. Should not read too much into the technical assumptions re. rate forecasts. Policy risks remain reasonably balanced.

- Nintendo (7974 JT) 2023/24 (JPY): Net 490.6bln, +13.4%; Operating 528bln, +4.9%; Recurring 680bln, +13.2%; is to make an announcement on a Switch successor in FY24. Will not be announcing anything re. successor hardware at Nintendo Direct in June

- Japanese Business Lobby Keidanren Chief Tokura says it is desirable for FX to reflect fundaments in mid and long-term; USD/JPY above 150 is "too much". Does not know if the authorities intervened in the FX market, but if they did, thinks timing was very good. Undesirable for FX to fluctuate through speculators.

- BoJ Governor Ueda had regular exchange of views with Japanese PM Kishida; discussed FX; confirmed with the PM that the BoJ will take into account impact of economy and prices which could be potentially big. Stands ready to keep close eye out on how JPY moves affect trend inflation; to closely monitor how a weak JPY will impact prices. Explained BoJ's stance of guiding policy from standpoint of sustainably reaching inflation goal.

APAC DATA RECAP

Top European News

- Barclaycard said UK April consumer spending fell 4.0% Y/Y (prev. +3.5%) which is the lowest since February 2021.

FX

- DXY is incrementally firmer and in a tight range thus far as markets await fresh impetus following last Friday's post-FOMC NFP-induced slide. DXY sits in a 105.03-28 intraday parameter, with 21 DMA at 105.20.

- EUR is moving in tandem with the Dollar, and has seen no notable catalysts this morning with key releases for the bloc also light this week. EUR/USD sits in a 1.0755-76 range after briefly dipping under yesterday's low (1.0753).

- GBP is subdued ahead of Thursday's BoE confab with the MPC expected to keep the Base Rate at 5.25%. GBP/USD trades in a 1.2533-70 range and dipped under its 200 DMA (1.2544).

- Modestly softer session for the JPY with USD/JPY reclaiming 154.00 status overnight (currently 154.50), whilst Japanese Business Lobby Keidanren Chief Tokura said FX should reflect fundaments in mid and long-term. Elsewhere, BoJ Governor Ueda spoke to PM Kishida regarding FX, though with specifics light.

- Divergence across the Antipodeans following the RBA policy decision in which the central bank left rates unchanged at 4.35% as expected, whilst analysts framed the release as less-hawkish-than-feared. AUD/USD trades in a 0.6588-6643 range.

- PBoC set USD/CNY mid-point at 7.1002 vs exp. 7.2143 (prev. 7.0994).

Fixed Income

- USTs are bid but holding a handful of ticks shy of Friday's 109-09+ payrolls peak & the 10yr yield is holding just above 4.45% by extension. Attention turns to the week's supply, with geopols also a key theme.

- Bunds have surpassed Friday's post-NFP 131.57 peak, printing a fresh high at 131.71. European specifics light with no reaction to the latest Construction PMIs as the broader market awaits a significant update to the Israel-Hamas situation around Rafah.

- Gilts gapped higher by 56 ticks after Monday's Bank Holiday, a move which accounts for that the geopol-related upside and a continuation of the post-payrolls dovish price action. Currently holding around 97.75 and higher by 79 ticks thus far.

Commodities

- Choppy session for the crude complex, as markets await updates from Israel/Rafah; most recently the operation has been said to be "limited". Brent Jul'24 trades between USD 83.30-83.82/bbl.

- Downbeat price action across precious metals despite a steady Dollar, with the complex failing to gain much impetus from a "limited" Israeli operation in Rafah. Spot gold trades in a USD 2,312.00-2,329.93/oz parameter.

- LME prices are mostly firmer as the exchange returns from the early May UK Bank Holiday. Elsewhere, JFE executives expects iron ore prices to remain at current levels in FY24/25 amid sluggish Chinese demand.

- US Senior Adviser for Energy and Investment Hochstein said the US has sufficient supply in Strategic Petroleum Reserve to address any supply concerns and the Biden administration is monitoring markets, according to Reuters.

- Russian Deputy PM Novak says possibility of raising production under the OPEC+ deal is being analysed, according to Interfax. There is no need to predict further OPEC+ steps, need to look at the market. Had agreed that oil output could be tweaked if needed.

- Commerzbank expects Palladium price to rise to USD 1100/troy oz (current 975.78) by end of the year; expects platinum to rise to USD 1100/troy oz (current 963) by end of year

Geopolitics: Middle East

- "Israeli source to CNN: The operation in Rafah is limited and aims to pressure Hamas to conclude an acceptable deal", according to Al Arabiya.

- Gaza crossings authority said the Israeli army stormed the Rafah crossing, according to Al Arabiya. However, Palestinian media said the Egyptian side informed the crossing's authority that Israeli vehicles are conducting a security operation in the vicinity of the Rafah crossing and will retreat tomorrow. It was later reported Israeli military took control of the Palestinian side of the Rafah border with Egypt, according to Bloomberg..

- US official said the US has concerns about Israel's unfolding Rafah strikes but it does not appear to represent a major military operation, according to Reuters.

- 100 congressional staff called on US President Biden and members of Congress to demand an immediate halt to the Israeli offensive before it is too late, according to Axios.

- Qatar Foreign Ministry said Hamas sent mediators its reply to the truce proposal on Monday and the reply could be described as "positive", while it was separately reported that the Qatari delegation arrives in Cairo on Tuesday to resume negotiations on a truce agreement in Gaza, according to Sky News Arabia.

- Jordanian Foreign Minister said Israeli PM Netanyahu is jeopardising the ceasefire deal by bombing Rafah, according to Reuters.

Geopolitics: Other

- A US soldier was detained on charges of criminal misconduct in Russia's far eastern city of Vladivostok last week.

- China reportedly hacked the UK Ministry of Defence with MPs to be told on Tuesday of a large data breach targeting service personnel, according to Sky News.

US Event Calendar

- 11:30: Fed’s Kashkari Participates in Fireside Chat

- 13:20: Fed’s Kashakari Speaks on Bloomberg TV

- 15:00: March Consumer Credit, est. $15bn, prior $14.1bn

DB's Jim Reid concludes the overnight wrap

It was a bank holiday here in the UK and it didn’t stop raining. I had an early round of golf and half way round the greens were flooded and I was drenched. I may have called it a day but the alternative was childcare. Golf in a biblical downpour is more enjoyable that looking after three bored kids inside on a very wet day. The afternoon was proof of that.

The skies are reasonably bright in markets at the moment with the S&P 500 (+1.03% yesterday) extending its 3-day gain to +3.24% last night, the best such run since November. For 10-year yields, the 4-day decline (-19.3bps) is the largest since the start of February. The lack of a ceasefire in the Middle East hasn't so far impacted sentiment.

A strong close to the US session saw the Magnificent 7 (+1.68%) eke out a new all-time high, with the index up more than 10% from its recent low on April 19. Nvidia (+3.77%) and Meta (+3.04%) led the gains amid the mega caps, but the equity advance was broad-based with 76% of the S&P 500 higher on the day. Small caps also saw a modest outperformance, with the Russell 2000 up +1.23%. Europe’s equity markets recorded a more moderate rise earlier on, including for the Stoxx 600 (+0.53%), Dax (+0.96%), CAX (+0.49%), while FTSE MIB outperformed (+1.06%).

The equity move was helped along by the ongoing bond rally, as 10yr Treasury yields (-2.2bps) declined for a fourth consecutive session to 4.49%, their lowest level since the upside surprise in the March CPI print on April 10. The upcoming CPI print next Wednesday (May 15) will surely be key to the sustainability of this rally. The decline in yields did run out of steam at the front end, with 2yr yields up +1.5bps after falling by -21.8bps over the previous three sessions.

This came as Fed commentary largely echoed Powell’s tone last week, moving away from any signal on the timing of rate cuts but avoiding overtly hawkish messages. Richmond Fed President Barkin said he was “optimistic that today’s restrictive level of rates can take the edge off demand in order to bring inflation back to our target“, noting that “the full impact of higher rates is yet to come.” And New York Fed president Williams signaled eventual rate cuts, though with the timing of these to depend on “the totality of the data”.

We received the latest signal on the impact of the Feds’ earlier tightening with the latest quarterly Senior Loan Officer Survey. This showed the tightness in credit standards continuing to moderate for most loan categories, including mortgages and CRE lending. However, the improvement in conditions for commercial & industrial loans stalled, with credit standards for mid-size and large firms a little tighter (+15.6 vs. +14.5) and demand a little weaker (-26.6 vs. -25.0) than in the previous quarter. Nothing to get too concerned about, but some evidence to support the view that a good chunk of the impact from the tighter policy stance is yet to play out. The question is where will rates and credit standards be by the time borrowing needs accelerate.

Over in euro area, the final April PMIs added to the improving growth picture, with upward revisions to the services (53.3 vs 52.9 flash) and composite (51.7 vs 51.4 flash) readings. The euro area composite is at an 11-month high and has moved above the US one for the first time in 12 months. In other data, euro area PPI inflation for March came in line with expectations at -0.4% month-on-month. This did little to dissuade expectations of a June ECB cut, with ECB chief economist Lane noting in an interview that data since the April meeting “ improve my confidence that inflation should return to target in a timely manner ”. Overnight index swaps continued to price 74bps of ECB rate cuts this year, with a June cut 95% priced. 10yr bonds saw a similar modest rally in Europe as in the US, with yields on bunds (-2.7bps), OATs (-2.3bps) and BTPs (-2.2bps) all moving slightly lower.

In the commodity space, oil prices saw some volatility amid mixed Middle East headlines. Having opened higher on Monday, oil prices briefly fell to flat on the day following news that Hamas accepted a cease-fire proposal brokered by Egypt and Qatar . However, they rallied again soon after on reports that Israel’s’s war cabinet rejected the proposal as being “far from Israel’s necessary demands,” with Axios and AP reporting overnight that Israeli troops had entered the southern Gaza city of Rafah. After falling to a seven-week low on Friday, Brent crude ended Monday’s session +0.45% higher at $83.33/bbl, and is trading around another +0.30% higher overnight as I type. This backdrop also boosted gold, which gained +1.04% to $2,326/oz yesterday.

In Asia, the KOSPI (+1.91%) is leading gains hitting a one-month high with the Nikkei (+1.18%) also seeing notable gains as trading has resumed in both markets after a public holiday. Additionally, the S&P/ASX 200 (+1.25%) is spiking higher as we type after the RBA left rates on hold but could have been more hawkish than they were. The Aussie Dollar has weakened -0.40% with 3yr government bonds yields declining -8.6bps, to trade at 3.94% as I type.

Elsewhere, Chinese stocks are bucking the regional trend with the Hang Seng (-0.69%), the CSI (-0.12%) and the Shanghai Composite (-0.08%) all trading lower. US futures are flat and Treasury yields are edging slightly lower.

The Japanese yen (-0.38%) continues to drift lower trading at 154.50 against the dollar despite fresh warnings from Japanese officials following two rounds of suspected FX intervention last week. Notably, top currency official Masato Kanda indicated that the government will respond appropriately if there are excessive or disorderly movements in the FX market.

Central bank decisions will remain in focus for the rest of the week, most of all with the BoE on Thursday. Our UK economist expects this week’s meeting to set the stage for the first rate cut in June (see his preview here). Before that, tomorrow the Riksbank could deliver its first rate cut of the cycle. Finally, we have the accounts of April ECB meeting on Friday, and with plenty more ECB and Fed speak to digest before the end of the week. It will quieter be on the data front, with the University of Michigan consumer survey on Friday the arguable highlight given the recent softening in US consumer confidence indicators.

To the day ahead, data releases will include US March consumer credit, Germany March trade balance and factory orders data, France Q1 wages and Eurozone March retail sales. In central bank speak, we will hear from the Fed's Kashkari, and the ECB's De Cos and Nagel. And as the earnings season continues to wind down, releases include Walt Disney, BP, Arista Networks, Duke Energy, McKesson, and Ferrari.

US stock futures are flat after the S&P 500 and Nasdaq 100 both closed 1% higher on Monday, helped by growing optimism among investors that the economy is finally slowing greenlighting earlier rate cuts by the Fed. As of 8:00am ET S&P futures were unchanged at 5,206, trading about 1% above its 50DMA, while Nasdaq futures were down 0.2% amid some mega-cap weakness. European stocks are higher, while indexes in Japan and the UK are catching up after being closed for holidays yesterday. Shares in Swiss bank UBS jumped after it returned to profit and showed more progress in its integration of Credit Suisse. Treasuries rise, with US 10-year yields falling 3bps to 4.46%. The Bloomberg Dollar Spot Index rises 0.1%. The yen weakens 0.4% against the greenback, pushing USD/JPY up to ~154.50. The Aussie falls 0.4% after the RBA kept rates on hold and maintained a neutral stance. Oil prices advance, with WTI rising 0.3% to trade near $78.70. Spot gold falls 0.4% and bitcoin traded in a range around $64,000 with the now daily European open/US slam down pattern. US economic data slate includes March consumer credit at 3pm, while Fed’s Kashkari is scheduled to speak twice (11:30am, 1:20pm).

In premarket trading, Disney reported fiscal second-quarter profit that beat estimates, thanks to sharply narrower losses in its streaming TV business and higher ticket prices at theme parks. Still, the stock tumbled 6% after the company reported fewer subscribers to its Disney+ streaming service in the fiscal second quarter than analysts had projected. Here are some of the other notable US movers before the opening bell:

- Celsius falls 8.4% after the energy-drink maker reported first-quarter revenue that missed even the lowest estimate among analysts tracked by Bloomberg.

- Coherent climbs 8.5% after the maker of components for the telecommunications industry raised the bottom end of its year revenue forecast.

- Datadog slips 11% after the cloud software company said that Amit Agarwal will be stepping down as president. The company also posted 1Q results.

- Esperion Therapeutics rallies 25% after the drugmaker’s first-quarter revenue was ahead of analyst estimates.

- Fidelity National Information Services’ rises 4% after the company raised its outlook for full-year profit.

- Gap rises 3% after Citi raised its rating on the retailer to buy on positive momentum and margin upside.

- Hims & Hers Health jumps 14% after the telehealth company boosted its adjusted Ebitda guidance for the full year.

- Lucid drops 8% after the EV maker posted a wider-than-expected loss for the first quarter.

- Oscar Health climbs 15% after the health insurer reported earnings per share for the first quarter that outpaced Wall Street’s expectations.

- Palantir falls 13% as the market appeared unimpressed by the company’s outlook for annual sales after the stock has tripled in the past year.

- Symbotic jumps 14% after the warehouse robotics and automation firm posted forecast-beating 2Q revenue and surpassed expectations for its fiscal 3Q revenue outlook.

- Vimeo gains 10% after the video software company reported first-quarter results that beat analyst expectations and provided a forecast.

- Zeta rises 16% after the software company gave a forecast revenue for the second quarter that beat the average analyst estimate.

In a week light on data but heavy on Fedspeak, Minneapolis Fed President Neel Kashkari is set to appear Tuesday, one day after his Richmond President colleague Thomas Barkin said Monday said he expects high interest rates to eventually cool US inflation to the central bank’s 2% target. Despite the hawkish rhetoric, swaps traders are betting on about 45 basis points of Fed rate cuts by December, an increase vs before the disappointing jobs report.

“In this environment of growth not rolling over as much as we feared and potentially cuts coming in, there is upside for earnings going forward,” Beata Manthey, head of European equity strategy at Citigroup Inc., said in an interview with Bloomberg TV

“The market is taking a positive view about the US job data and anticipating that the Fed will indeed be able to cut rates,” said Arnaud Girod, head of economics and cross-asset strategy at Kepler Cheuvreux in Paris.

European stocks rose for the third consecutive session, boosted by solid company earnings and renewed optimism the Federal Reserve will cut interest rates later this year. The Stoxx 600 is up 0.6%. UBS jumps more than 8% after it returned to profit and UniCredit climbed on better-than-forecast results. German semiconductor-maker Infineon Technologies AG cut its revenue forecast, signaling demand from the automotive industry remains weak.

Earlier in the session, Asia’s equity benchmark traded little changed on Tuesday as a catch-up rally in Korean and Japanese stocks on their return from a holiday was offset by declines in Hong Kong. The MSCI Asia Pacific Index rose 0.1% after capping a three-day gain on Monday. Technology was the best-performing sector in the region, much like in the US session overnight, amid rising hopes that the Federal Reserve may cut interest rates this year. Shares of Samsung Electronics and SK Hynix were the biggest contributors to gains on South Korea’s Kospi Index, which jumped 2%, the most in Asia. Shares in Hong Kong fell, with the Hang Seng Index snapping a 10-day winning streak that was the longest since 2018 amid some concern that the rally is overdone.

In FX, the Bloomberg Dollar Spot Index rose 0.1%, marking the second consecutive session of gains, as the greenback rose against most Group-of-10 currencies. The yen weakens 0.4% against the greenback, pushing USD/JPY up to ~154.50. The Aussie falls 0.4% after the RBA kept rates on hold and maintained a neutral stance.

- AUD/USD led losses falling as much as 0.6% to 0.6587, following the RBA’s interest rate decision; Australia’s central bank opted to maintain policy but markets likely expected the RBA to revert to prior guidance that a further increase in interest rates couldn’t be ruled out

- USD/JPY rose as much as 0.5% to 154.65, the highest level since May. 2, BOJ Governor Kazuo Ueda said he’s carefully watching the impact of the weak yen on prices and that he discussed recent moves with Prime Minister Fumio Kishida

- EUR/USD fell as much as 0.1% to 1.0754; German factory orders dropped 0.4% month-on-month in line with expectations, while eurozone March retail sales were up 0.8% from February

In rates, treasuries rose with US 10-year yields falling 3bps to 4.46%. Treasuries were underpinned by bigger gains in core European rates after Germany factory orders unexpectedly declined, pointing to persistent economic headwinds. During Asia session, Treasury futures drew support from dovish reaction to RBA maintaining its neutral bias, keeping interest rates at 4.35%. Focal points of US session include 3-year note auction, ahead of 10- and 30-year sales Wednesday and Thursday. US yields richer by 2bp to 3bp with the curve extending Monday’s flattening move; 10-year around 4.46% is ~2.5bp richer on the day with bunds and gilts outperforming by 1bp and 5bp in the sector. Treasury auction cycle begins at 1pm New York time with $58b 3-year note sale; $42b 10-year and $25b 30-year new issues follow Wednesday and Thursday.

In commodities, oil prices advance, with WTI rising 0.3% to trade near $78.70. Spot gold falls 0.4%.

In crypto, Bitcoin firmer today and has reclaimed the USD 64k handle, with Ethereum now holding around USD 3.2k.

Looking at today’s calendar, US economic data slate includes March consumer credit at 3pm. Fed members’ scheduled speeches include Kashkari (11:30am, 1:20pm). Elsewhere we get, German March trade balance and factory orders data, French Q1 wages and Eurozone March retail sales. And as the earnings season continues to wind down, releases include Walt Disney, BP, Arista Networks, Duke Energy, McKesson, and Ferrari.

Market Snapshot

- S&P 500 futures little changed at 5,207.25

- STOXX Europe 600 up 0.6% to 511.10

- MXAP up 0.3% to 178.44

- MXAPJ up 0.3% to 552.71

- Nikkei up 1.6% to 38,835.10

- Topix up 0.6% to 2,746.22

- Hang Seng Index down 0.5% to 18,479.37

- Shanghai Composite up 0.2% to 3,147.74

- Sensex down 0.4% to 73,564.94

- Australia S&P/ASX 200 up 1.4% to 7,793.32

- Kospi up 2.2% to 2,734.36

- German 10Y yield little changed at 2.44%

- Euro little changed at $1.0762

- Brent Futures up 0.3% to $83.59/bbl

- Brent Futures up 0.3% to $83.58/bbl

- Gold spot down 0.3% to $2,315.95

- US Dollar Index up 0.16% to 105.22

Top Overnight News

- RBA leaves rates unchanged (as expected) and suggests there won’t by any additional hikes but also doesn’t seem in a rush to ease (new forecasts show no rate cuts until 2025). RTRS

- Taiwan’s CPI for Apr comes in below expectations, w/the headline number at +1.95% (vs. the Street +2.2% and down from +2.15% in Mar). BBG

- China tightened rules for hedge funds, raising the minimum-asset threshold of the 5.5 trillion yuan ($762 billion) industry while imposing restrictions on the use of derivatives and leverage. BBG

- Israel sent ground troops into Rafah on Monday night, seizing the main border crossing between Gaza and Egypt as international mediators struggled to continue talks aimed at ending the conflict. FT

- BP ended a mixed set of Big Oil results by maintaining share buybacks even as profit and cash flow fell more than expected. Aramco will pay $31 billion in dividends to the Saudi government and other investors despite lower profit. BBG

- UBS returned to profit with wealth management and the investment bank driving the beat. The firm targets another $1.5 billion in cost savings by year-end but sees integration expenses of $1.3 billion this quarter, and cautioned that the Swiss central bank’s recent rate cut will hurt NII. The stock climbed. BBG

- Social Security and Medicare will exhaust their funds in a little more than 10 years unless action is taken to address the shortfalls (although the new exhaustion dates for Social Security and Medicare are 1 and 5 years later than the prior forecasts). CNN

- Citigroup CEO Jane Fraser said Monday that consumer behavior has diverged as inflation for goods and services makes life harder for many Americans. Fraser, who leads one of the largest U.S. credit card issuers, said she is seeing a “K-shaped consumer.” That means the affluent continue to spend, while lower-income Americans have become more cautious with their consumption. CNBC

- AAPL has been working on its own chip designed to run artificial intelligence software in data center servers, a move that has the potential to give the company an advantage in the AI arms race. WSJ

- Donald Trump’s prized Manhattan office tower at 40 Wall St. is getting swept up by the worst storm to hit the office market since the global financial crisis. Like thousands of other U.S. office buildings, 40 Wall is now under duress because of weakening office demand. WSJ

Earnings

- Infineon (IFX GY) Q2 (EUR): Revenue 3.63bln (exp. 3.6bln), adj. EPS 0.42 (exp. 0.38), Gross Margin 38.6% (exp. 39.8%).

- BP (BP/ LN) Q1 (USD): Adj. Net 2.72bln (exp. 2.92bln). Revenue 49.96bln (exp. 52.44bln). Adj. EPS 0.16 (exp. 0.17). Dividend 0.0727 (exp. 0.0730)Announces USD 1.75bln share buyback for Q1. Continues to expect 2024 Capex around USD 16bln.

- Nintendo (7974 JT) 2023/24 (JPY): Net 490.6bln, +13.4%; Operating 528bln, +4.9%; Recurring 680bln, +13.2%. Sold 15.7mln Switch consoles in FY23/24 (exp. 15.5mln, prev. 17.9mln FY22/23). To make an announcement on a Switch successor in FY24; will not be announcing anything re. successor hardware at Nintendo Direct in June.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed as the region only partly sustained the momentum from Wall St where the major indices extended on post-NFP advances amid rate cut hopes, while key markets returned from the long weekend. ASX 200 traded higher with a further boost in late trade after the RBA proved to be less hawkish than many feared. Nikkei 225 gained on return from holiday as it took its first opportunity to react to last week’s NFP report and renewed US rate cut hopes. Hang Seng & Shanghai Comp were subdued with the former set to snap its 10-day win streak and longest consecutive run of gains since 2018, while the mainland index took a breather after yesterday’s catch-up rally amid a lack of fresh catalysts.

Top Asian News

- US will host China’s special envoy for climate change Liu Zhenmin in Washington on May 8th-9th, according to the State Department.

- Japanese top FX diplomat Kanda said it is important for currencies to move in a stable manner reflecting fundamentals and the government must take appropriate steps if there’s excessive volatility in the FX market, while he added it is usual that they don’t comment whether currency intervention was carried out.

- RBA kept the Cash Rate Target unchanged at 4.35%, as expected, while it reiterated the Board remains resolute in its determination to return inflation to the target and it is not ruling anything in or out. RBA stated that returning inflation to the target within a reasonable timeframe remains the board’s highest priority, as well as noted that inflation remains high and is falling more gradually than expected. Furthermore, the RBA raised its inflation forecasts for 2024 but trimmed forecasts for GDP and unemployment, while its forecasts assume that rates will stay at 4.35% until mid-2025 which is nine months longer than previously assumed.

- RBA’s Bullock says they must be vigilant on inflation risks, believe rates are at the correct level to get inflation back to target. Board discussed the option of hiking. Will tighten if necessary, do not think they necessarily have to tighten again. Should not read too much into the technical assumptions re. rate forecasts. Policy risks remain reasonably balanced.

- Nintendo (7974 JT) 2023/24 (JPY): Net 490.6bln, +13.4%; Operating 528bln, +4.9%; Recurring 680bln, +13.2%; is to make an announcement on a Switch successor in FY24. Will not be announcing anything re. successor hardware at Nintendo Direct in June

- Japanese Business Lobby Keidanren Chief Tokura says it is desirable for FX to reflect fundaments in mid and long-term; USD/JPY above 150 is “too much”. Does not know if the authorities intervened in the FX market, but if they did, thinks timing was very good. Undesirable for FX to fluctuate through speculators.

- BoJ Governor Ueda had regular exchange of views with Japanese PM Kishida; discussed FX; confirmed with the PM that the BoJ will take into account impact of economy and prices which could be potentially big. Stands ready to keep close eye out on how JPY moves affect trend inflation; to closely monitor how a weak JPY will impact prices. Explained BoJ’s stance of guiding policy from standpoint of sustainably reaching inflation goal.

APAC DATA RECAP

Top European News

- Barclaycard said UK April consumer spending fell 4.0% Y/Y (prev. +3.5%) which is the lowest since February 2021.

FX

- DXY is incrementally firmer and in a tight range thus far as markets await fresh impetus following last Friday’s post-FOMC NFP-induced slide. DXY sits in a 105.03-28 intraday parameter, with 21 DMA at 105.20.

- EUR is moving in tandem with the Dollar, and has seen no notable catalysts this morning with key releases for the bloc also light this week. EUR/USD sits in a 1.0755-76 range after briefly dipping under yesterday’s low (1.0753).

- GBP is subdued ahead of Thursday’s BoE confab with the MPC expected to keep the Base Rate at 5.25%. GBP/USD trades in a 1.2533-70 range and dipped under its 200 DMA (1.2544).

- Modestly softer session for the JPY with USD/JPY reclaiming 154.00 status overnight (currently 154.50), whilst Japanese Business Lobby Keidanren Chief Tokura said FX should reflect fundaments in mid and long-term. Elsewhere, BoJ Governor Ueda spoke to PM Kishida regarding FX, though with specifics light.

- Divergence across the Antipodeans following the RBA policy decision in which the central bank left rates unchanged at 4.35% as expected, whilst analysts framed the release as less-hawkish-than-feared. AUD/USD trades in a 0.6588-6643 range.

- PBoC set USD/CNY mid-point at 7.1002 vs exp. 7.2143 (prev. 7.0994).

Fixed Income

- USTs are bid but holding a handful of ticks shy of Friday’s 109-09+ payrolls peak & the 10yr yield is holding just above 4.45% by extension. Attention turns to the week’s supply, with geopols also a key theme.

- Bunds have surpassed Friday’s post-NFP 131.57 peak, printing a fresh high at 131.71. European specifics light with no reaction to the latest Construction PMIs as the broader market awaits a significant update to the Israel-Hamas situation around Rafah.

- Gilts gapped higher by 56 ticks after Monday’s Bank Holiday, a move which accounts for that the geopol-related upside and a continuation of the post-payrolls dovish price action. Currently holding around 97.75 and higher by 79 ticks thus far.

Commodities

- Choppy session for the crude complex, as markets await updates from Israel/Rafah; most recently the operation has been said to be “limited”. Brent Jul’24 trades between USD 83.30-83.82/bbl.

- Downbeat price action across precious metals despite a steady Dollar, with the complex failing to gain much impetus from a “limited” Israeli operation in Rafah. Spot gold trades in a USD 2,312.00-2,329.93/oz parameter.

- LME prices are mostly firmer as the exchange returns from the early May UK Bank Holiday. Elsewhere, JFE executives expects iron ore prices to remain at current levels in FY24/25 amid sluggish Chinese demand.

- US Senior Adviser for Energy and Investment Hochstein said the US has sufficient supply in Strategic Petroleum Reserve to address any supply concerns and the Biden administration is monitoring markets, according to Reuters.

- Russian Deputy PM Novak says possibility of raising production under the OPEC+ deal is being analysed, according to Interfax. There is no need to predict further OPEC+ steps, need to look at the market. Had agreed that oil output could be tweaked if needed.

- Commerzbank expects Palladium price to rise to USD 1100/troy oz (current 975.78) by end of the year; expects platinum to rise to USD 1100/troy oz (current 963) by end of year

Geopolitics: Middle East

- “Israeli source to CNN: The operation in Rafah is limited and aims to pressure Hamas to conclude an acceptable deal”, according to Al Arabiya.

- Gaza crossings authority said the Israeli army stormed the Rafah crossing, according to Al Arabiya. However, Palestinian media said the Egyptian side informed the crossing’s authority that Israeli vehicles are conducting a security operation in the vicinity of the Rafah crossing and will retreat tomorrow. It was later reported Israeli military took control of the Palestinian side of the Rafah border with Egypt, according to Bloomberg..

- US official said the US has concerns about Israel’s unfolding Rafah strikes but it does not appear to represent a major military operation, according to Reuters.

- 100 congressional staff called on US President Biden and members of Congress to demand an immediate halt to the Israeli offensive before it is too late, according to Axios.

- Qatar Foreign Ministry said Hamas sent mediators its reply to the truce proposal on Monday and the reply could be described as “positive”, while it was separately reported that the Qatari delegation arrives in Cairo on Tuesday to resume negotiations on a truce agreement in Gaza, according to Sky News Arabia.

- Jordanian Foreign Minister said Israeli PM Netanyahu is jeopardising the ceasefire deal by bombing Rafah, according to Reuters.

Geopolitics: Other

- A US soldier was detained on charges of criminal misconduct in Russia’s far eastern city of Vladivostok last week.

- China reportedly hacked the UK Ministry of Defence with MPs to be told on Tuesday of a large data breach targeting service personnel, according to Sky News.

US Event Calendar

- 11:30: Fed’s Kashkari Participates in Fireside Chat

- 13:20: Fed’s Kashakari Speaks on Bloomberg TV

- 15:00: March Consumer Credit, est. $15bn, prior $14.1bn

DB’s Jim Reid concludes the overnight wrap

It was a bank holiday here in the UK and it didn’t stop raining. I had an early round of golf and half way round the greens were flooded and I was drenched. I may have called it a day but the alternative was childcare. Golf in a biblical downpour is more enjoyable that looking after three bored kids inside on a very wet day. The afternoon was proof of that.

The skies are reasonably bright in markets at the moment with the S&P 500 (+1.03% yesterday) extending its 3-day gain to +3.24% last night, the best such run since November. For 10-year yields, the 4-day decline (-19.3bps) is the largest since the start of February. The lack of a ceasefire in the Middle East hasn’t so far impacted sentiment.

A strong close to the US session saw the Magnificent 7 (+1.68%) eke out a new all-time high, with the index up more than 10% from its recent low on April 19. Nvidia (+3.77%) and Meta (+3.04%) led the gains amid the mega caps, but the equity advance was broad-based with 76% of the S&P 500 higher on the day. Small caps also saw a modest outperformance, with the Russell 2000 up +1.23%. Europe’s equity markets recorded a more moderate rise earlier on, including for the Stoxx 600 (+0.53%), Dax (+0.96%), CAX (+0.49%), while FTSE MIB outperformed (+1.06%).

The equity move was helped along by the ongoing bond rally, as 10yr Treasury yields (-2.2bps) declined for a fourth consecutive session to 4.49%, their lowest level since the upside surprise in the March CPI print on April 10. The upcoming CPI print next Wednesday (May 15) will surely be key to the sustainability of this rally. The decline in yields did run out of steam at the front end, with 2yr yields up +1.5bps after falling by -21.8bps over the previous three sessions.

This came as Fed commentary largely echoed Powell’s tone last week, moving away from any signal on the timing of rate cuts but avoiding overtly hawkish messages. Richmond Fed President Barkin said he was “optimistic that today’s restrictive level of rates can take the edge off demand in order to bring inflation back to our target“, noting that “the full impact of higher rates is yet to come.” And New York Fed president Williams signaled eventual rate cuts, though with the timing of these to depend on “the totality of the data”.

We received the latest signal on the impact of the Feds’ earlier tightening with the latest quarterly Senior Loan Officer Survey. This showed the tightness in credit standards continuing to moderate for most loan categories, including mortgages and CRE lending. However, the improvement in conditions for commercial & industrial loans stalled, with credit standards for mid-size and large firms a little tighter (+15.6 vs. +14.5) and demand a little weaker (-26.6 vs. -25.0) than in the previous quarter. Nothing to get too concerned about, but some evidence to support the view that a good chunk of the impact from the tighter policy stance is yet to play out. The question is where will rates and credit standards be by the time borrowing needs accelerate.

Over in euro area, the final April PMIs added to the improving growth picture, with upward revisions to the services (53.3 vs 52.9 flash) and composite (51.7 vs 51.4 flash) readings. The euro area composite is at an 11-month high and has moved above the US one for the first time in 12 months. In other data, euro area PPI inflation for March came in line with expectations at -0.4% month-on-month. This did little to dissuade expectations of a June ECB cut, with ECB chief economist Lane noting in an interview that data since the April meeting “ improve my confidence that inflation should return to target in a timely manner ”. Overnight index swaps continued to price 74bps of ECB rate cuts this year, with a June cut 95% priced. 10yr bonds saw a similar modest rally in Europe as in the US, with yields on bunds (-2.7bps), OATs (-2.3bps) and BTPs (-2.2bps) all moving slightly lower.

In the commodity space, oil prices saw some volatility amid mixed Middle East headlines. Having opened higher on Monday, oil prices briefly fell to flat on the day following news that Hamas accepted a cease-fire proposal brokered by Egypt and Qatar . However, they rallied again soon after on reports that Israel’s’s war cabinet rejected the proposal as being “far from Israel’s necessary demands,” with Axios and AP reporting overnight that Israeli troops had entered the southern Gaza city of Rafah. After falling to a seven-week low on Friday, Brent crude ended Monday’s session +0.45% higher at $83.33/bbl, and is trading around another +0.30% higher overnight as I type. This backdrop also boosted gold, which gained +1.04% to $2,326/oz yesterday.

In Asia, the KOSPI (+1.91%) is leading gains hitting a one-month high with the Nikkei (+1.18%) also seeing notable gains as trading has resumed in both markets after a public holiday. Additionally, the S&P/ASX 200 (+1.25%) is spiking higher as we type after the RBA left rates on hold but could have been more hawkish than they were. The Aussie Dollar has weakened -0.40% with 3yr government bonds yields declining -8.6bps, to trade at 3.94% as I type.

Elsewhere, Chinese stocks are bucking the regional trend with the Hang Seng (-0.69%), the CSI (-0.12%) and the Shanghai Composite (-0.08%) all trading lower. US futures are flat and Treasury yields are edging slightly lower.

The Japanese yen (-0.38%) continues to drift lower trading at 154.50 against the dollar despite fresh warnings from Japanese officials following two rounds of suspected FX intervention last week. Notably, top currency official Masato Kanda indicated that the government will respond appropriately if there are excessive or disorderly movements in the FX market.

Central bank decisions will remain in focus for the rest of the week, most of all with the BoE on Thursday. Our UK economist expects this week’s meeting to set the stage for the first rate cut in June (see his preview here). Before that, tomorrow the Riksbank could deliver its first rate cut of the cycle. Finally, we have the accounts of April ECB meeting on Friday, and with plenty more ECB and Fed speak to digest before the end of the week. It will quieter be on the data front, with the University of Michigan consumer survey on Friday the arguable highlight given the recent softening in US consumer confidence indicators.

To the day ahead, data releases will include US March consumer credit, Germany March trade balance and factory orders data, France Q1 wages and Eurozone March retail sales. In central bank speak, we will hear from the Fed’s Kashkari, and the ECB’s De Cos and Nagel. And as the earnings season continues to wind down, releases include Walt Disney, BP, Arista Networks, Duke Energy, McKesson, and Ferrari.

Loading…