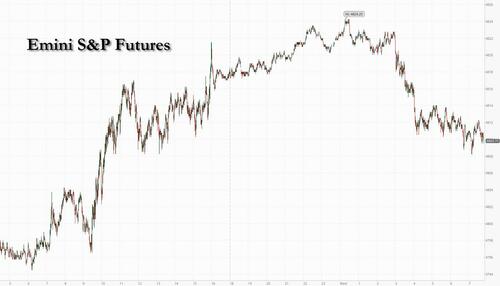

US equity futures and global markets reversed their torrid rally as bonds rallied and the dollar gained after a fresh batch of soft inflation data in the UK boosted the likelihood of interest-rate cuts, but also underscored the risk of an economic downturn. As of 7:45am, S&P eminis dropped 0.2% after the index notched a record high for the third successive session, with European and Asian stocks in the red. Germany 10-year yields dropped below 2% for the first time in nine months after a report showed producer prices fell more than expected in November. Meanwhile, British 10-year borrowing costs slid as much as 11 basis points as slower-than-expected inflation boosted the case for multiple rate cuts next year. Treasury yields slid four basis points to 3.9%, down more than 40 this month. Brent jumped above $80 to a 3 week high after the US considered possible military strikes against Houthi rebels in Yemen, in a recognition that a newly announced maritime task force meant to protect commercial ships in the Red Sea may not be enough to eliminate the threat to the vital waterway. US economic data includes 3Q current account balance (8:30am), November existing home sales and December consumer confidence (10am).

In premarket trading, FedEx shares tumbled as 10% after the parcel company’s fiscal second-quarter profit came in below expectations, with analysts pointing to a particularly disappointing performance from the Express air-freight unit, which was hit by slowing volumes. Brokers added that the company’s outlook lacked visibility, with Citi calling it “vague.” Here are some other notable premarket movers:

- Cinemark drops 3.5% in premarket trading as Wells Fargo downgrades the movie theater operator to underweight from equal-weight based on an unattractive box office outlook.

- Clear Channel Outdoor Holdings rises 7.7% in premarket trading on Wednesday after Wells Fargo Securities raised the recommendation on the advertising company to overweight from equal-weight. The broker says the upgrade comes as the company returns to growth.

- Coupang slides 1.6% in premarket trading as UBS downgrades its rating to neutral, awaiting greater clarity on the e-commerce company’s strategy.

- Discover Financial shares rise as much as 1.4% in premarket trading Wednesday after the credit card issuer was upgraded to buy from neutral at Citigroup, which also opened a 90-day catalyst watch on the stock saying investors should get more insight about the scope of credit losses when it reports fourth-quarter results in January.

- General Mills (GIS) slides 4.7% ahead of the bell after the packaged food company reported organic volume and sales for the second quarter that fell short of consensus estimates. GIS also cut its annual organic sales forecast, citing a slower-than-expected volume recovery amid a more cautious consumer economic outlook and a faster normalization of product availability from competitors. .

- Kellanova, Kraft Heinz and Conagra fall premarket after General Mills reported sales and volumes that missed consensus estimates for the second quarter and cut its annual organic sales view. Kellanova -1.6%, Kraft -1.2%, Conagra -1%.

Markets have rallied hard in recent weeks after the Fed's dovish pivot which helped put the tech-heavy Nasdaq 100 on course for its best year since 1999, while the S&P 500 is less than 1% off its record closing peak. Bulls got fresh encouragement Tuesday from Richmond Fed President Thomas Barkin, who suggested the US central bank would “respond appropriately” if recent progress on inflation continued. Money markets now price almost a 50% chance of an euro-area rate cut by next March, while seeing an even higher probability of a Fed cut that month. That said, even Powell's unofficial mouthpiece, Nikileaks, aka Nick Timiraos is now warning that the market that it has gone up too far, too fast.

Since their meeting last week, Fed officials have been flummoxed that investors expect even faster and deeper cuts. The result: Confusion over when and how quickly the Fed might cut.

— Nick Timiraos (@NickTimiraos) December 20, 2023

“The Fed shouldn’t have been surprised by the market running with it.” https://t.co/Tth5I2NzXe

At the same time, investors are also having to balance rate-cut optimism against the risk of economic recession. Recent data has backed that view, especially in the euro area, with analysts surveyed by Bloomberg forecasting the first recession since the pandemic.

“It’s hard to see such a fast and deep rate-cutting cycle as the market appears to assume, unless the base case is a deep recession,” said Daniele Antonucci, chief investment officer at Quintet Private Bank.

Investors are also starting to weigh risks stemming from potential shipping delays and freight cost increases, as companies divert cargoes away from the Red Sea to avoid militant attacks. This rerouting will mean higher shipping costs and longer delivery time, and has helped push brent crude prices above $80 for the first time in 3 weeks.

The big econ news overnight was the latest confirmation that a global deflationary wave is being unleashed, with UK reporting inflation that came in below the lowest estimate. The UK data “adds to the mounting evidence that global inflation has begun to crumble on a broader basis,” said Christoph Rieger, head of rates research at Commerzbank.

While the data initially boosted European stocks, gains on the Stoxx 600 index quickly evaporated, though London’s export-oriented FTSE 100 benchmark held its gains as the pound tumbled on the prospect of looser monetary policy. The telecom sector lead the advance, boosted by Spain’s Telefonica. The health-care sector underperforms, meanwhile, dragged lower by Argenx, which plunges after disappointing drug trial data. Among single stocks, shipping companies Hapag Lloyd AG and AP Moller-Maersk A/S rallied as militant attacks continued to disrupt Red Sea container traffic. Here are the biggest movers Wednesday:

- Telefonica shares jump as much as 7.2% after the Spanish state unveiled a plan to buy up to 10% in the telecom operator to counter stakebuilding by Saudi Telecom Co.

- Intertek gains as much as 3.7% after BNP Paribas Exane double-upgrades to outperform, saying in note that consensus is now overly bearish on margin outlook

- Raiffeisen Bank surges 12%, the most since March 2022, following its deal to buy a stake in Austrian construction company Strabag, with Citi upgrading the stock to buy from neutral

- British stocks rally as data showed inflation in the UK slowed far more than expectations, driving European stocks closer to early 2022 record, with landlords leading the advance

- Indivior gains as much as 4.5% after settling a drug patent dispute with rival Actavis, which now is granted a license to the patent that would enable Actavis to launch a generic variant

- Ionos gains for a ninth day as Morgan Stanley says the webhosting firm has delivered “two early Christmas presents” in strong guidance on Tuesday and last week’s debt refinancing.

- Argenx shares plunge as much as 35% after its key drug Vyvgart (efgartigimod) failed another trial, a second setback in less than a month for the Brussels-listed biotech firm

- DS Smith falls as much as 2.8% after UBS downgraded the paper and packaging company to neutral from buy, saying the downgrade reflects weaker containerboard prices

- Inficon shares fell as much as 5.3%, the most in two months, after the Swiss vacuum instruments manufacturer was downgraded to reduce from add at Baader Helvea

- Resurs Holding drops as much as 8.3% after SEB Equities downgrades the retail finance company to sell from hold, giving the stock its only negative analyst rating

Earlier in the session, Asian stocks rose for a second straight day, as Japanese shares extended gains following the Bank of Japan’s decision to stand pat on interest rates on Tuesday. The MSCI Asia Pacific Index advanced as much as 1% to its highest since Aug. 8, with Tencent and Samsung Electronics among the biggest contributors to the gauge’s rise. Exporter stocks led Japan’s benchmarks higher as the yen weakened after the country held on to the world’s last negative interest rate regime. Indexes across South Korea, Hong Kong and Southeast Asia also gained as traders looked past Federal Reserve officials’ pushback on aggressive interest rate-cut expectations. The gains across Asia follow two days of cautious trading during which investors assessed the path of US monetary policy in 2024.

- Hang Seng and Shanghai Comp traded mixed with the former's gains spearheaded by large caps with US listings, including Alibaba, JD.com, and Baidu. Mainland China was subdued after PBoC maintained its Loan Prime Rates as expected and despite more liquidity injections by the central bank.

- Nikkei 225 surged as the index reacted to BoJ Governor Ueda's dovish press conference following the unchanged announcement yesterday.

- ASX 200 saw its upside supported by the Energy and Metals sectors, whilst Tech lagged with shallower gains.

In FX, GBP/USD falls as much as 0.7% to below $1.27 after UK CPI data, EUR/USD down 0.3%; the Bloomberg Dollar Spot Index is largely unchanged as the US currency’s gains versus European currencies are offset by its slide against the yen. The Japanese yen is the best performer among the G-10 currencies, rising 0.3% versus the greenback on false expectations that the BOJ will end its negative rate policy in the coming months which has supported the yen. The dollar has been struggling as investors seek more guidance from the Fed on how soon it will begin cutting rates next year as inflation slows; however Chicago Fed’s Goolsbee said on Tuesday that the market may be getting ahead of itself when it comes to rate cuts.

“Speculative bets on a BOJ policy change are likely to ease for now,” said Fukuhiro Ezawa, head of financial markets in Tokyo at Standard Chartered Bank. “Markets price in deep Fed rate cuts, weighing on the dollar” against peers including the yen, he said

In rates, the yield on the 10-year US Treasury slips 4bps to 3.88%, its lowest since late July. Traders are betting that the Fed will cut rates by 150bps by the end of 2024, compared with around 140 bps on Tuesday. UK gilts rallied while the pound drops after data showed UK inflation slowed more than expected in November, fueling bets on interest rate cuts by the Bank of England next year. UK two-year yields fall 15 basis points to 4.14%, a seven-month low.

In commodities, oil extended its recent rally amid prospects of more disruptions in the Red Sea, while the US weighs military strikes on Houthis. Brent jumped above $80 to a three week high. Brent March call options in the $90s were active again on Tuesday as traders continue to weigh the risks to traffic in the Red Sea. WTI’s second-month 25-delta put skew was the least bearish since mid-November. Brent’s prompt spread climbed to the strongest since Dec. 5, while its Dec.-Dec. spread was the firmest this month.

Bitcoin (+0.6%) and Ethereum (+1.2%) extended gains as BTC rose back over USD 43k. BlackRock, Nasdaq, SEC met regarding a Bitcoin (BTC) ETF, via CoinDesk

Looking to the day ahead now, and data releases from the US include the Conference Board’s consumer confidence for December, existing home sales for November, and the Q3 current account balance. In the Euro Area, there’s the European Commission’s preliminary consumer confidence indicator for December, and there’s also the UK CPI and German PPI readings for November. From central banks, we’ll hear from the Fed’s Goolsbee and the ECB’s Lane.

Market Snapshot

- S&P 500 futures down 0.2% to 4,812.50

- STOXX Europe 600 little changed at 476.63

- MXAP up 0.5% to 165.32

- MXAPJ up 0.2% to 515.45

- Nikkei up 1.4% to 33,675.94

- Topix up 0.7% to 2,349.38

- Hang Seng Index up 0.7% to 16,613.81

- Shanghai Composite down 1.0% to 2,902.11

- Sensex down 1.1% to 70,636.67

- Australia S&P/ASX 200 up 0.7% to 7,537.88

- Kospi up 1.8% to 2,614.30

- German 10Y yield little changed at 1.99%

- Euro down 0.2% to $1.0961

- Brent Futures up 0.8% to $79.87/bbl

- Gold spot up 0.1% to $2,041.67

- U.S. Dollar Index little changed at 102.26

Top Overnight News

- Bond yields across the euro region fell on Wednesday as worsening economic data and slowing inflation underscored expectations for interest-rate cuts next year.

- UK inflation slowed far more than economists forecast in November, a surprise that prompted traders to boost bets the Bank of England will soon have to abandon its higher-for-longer narrative on interest rates.

- Attacks in the Red Sea linked to the Israel-Hamas war will cause shipping delays and drive up the price of goods, bringing a new inflation risk to the economy.

- Jonathan Hoffman, John Bonello and Jonathan Tipermas share more than just similar first names. They’re the driving force behind a gigantic wager on government debt that’s been giving regulators sleepless nights.

- Donald Trump is ineligible to serve as US president because of his actions inciting the Jan. 6, 2021 attack on the US Capitol, Colorado’s highest court found, in an unprecedented ruling that’s headed for the US Supreme Court.

- Throngs of consultants wearing Western attire have become a common sight in the lobbies of Riyadh’s plushest hotels as Crown Prince Mohammed Bin Salman embarks on a multi-trillion dollar plan to wean Saudi Arabia off oil. In recent months they’ve been joined by another cohort of besuited individuals: fund managers, keen to get an early foothold in the next big emerging-market growth story.

A more detailed look at global markets courtesy of NEwsquawk

Asia-Pac stocks traded mostly positively following the tailwinds from Wall Street, although newsflow overnight was on the quieter side amid the pre-Christmas lull. ASX 200 saw its upside supported by the Energy and Metals sectors, whilst Tech lagged with shallower gains. Nikkei 225 surged as the index reacted to BoJ Governor Ueda's dovish press conference following the unchanged announcement yesterday. Hang Seng and Shanghai Comp traded mixed with the former's gains spearheaded by large caps with US listings, including Alibaba, JD.com, and Baidu. Mainland China was subdued after PBoC maintained its Loan Prime Rates as expected and despite more liquidity injections by the central bank.

Top Asian News

- PBoC maintained its 1-year and 5-year LPRs at 3.45% and 4.20% respectively, as expected.

- PBoC injected CNY 134bln through 7-day reverse repos at 1.80% and CNY 151bln via 14-day reverse repos at 1.95%; both rates maintained

- The Japanese government is to raise its long-term interest rate estimate to 1.9% for FY24 from 1.1% in FY23, according to Nikkei.

- Japanese Cabinet projects that income will increase more than prices in FY24, according to Nikkei.

- State-backed developer China South City averts default on July 2024 note after consent from bondholders, according to SCMP.

- RBNZ Governor Orr said interest rates are restricting spending and levels of core inflation remain too high, according to the Parliamentary hearing. He noted that Q3 GDP was surprisingly subdued, and inflation remains too high and the committee remains wary of ongoing inflationary surprises. He said the neutral interest rate is now 2.5%.

- New Zealand DMO and fiscal update: gross bond issuance for four years to June 2027 now totals NZD 136bln, up from NZD 129bln in the budget. 2023/24 gross bond issuance increases to NZD 38bln from NZD 36bln in budget. Treasury sees GDP growth in Q4 23 and through 2024.

- Japan is to draft an initial FY24 budget of JPY 112tln, via Kyodo News

- Japanese government is to lower the scheduled sales of JGBs to market by 11.2% from FY23 plan to JPY 171tln in FY24/25, via Reuters citing a draft

European bourses, Eurostoxx50 (-0.2%), are marginally weaker having spent much of the morning the green; the FTSE 100 (+0.8%) outperforms post-UK CPI. European sectors are mixed with Energy outperforming lifted by gains in underlying Crude prices and Telefonica (+5%) helps lift Telecoms; Technology narrowly lags. US Equity Futures are lower across the board as the Santa Rally comes to a pause, ES (-0.2%); FedEx (-9.9%) extends losses in the pre-market post-earnings.

Top European News

- ECB's Nagel says there is a high probability that the interest rate peak has been reached, according to t-online; would say to everyone who is speculating on an imminent interest rate cut: be careful, some people have already speculated.

- France and Germany see an EU deal on fiscal rules on Wednesday, according to Bloomberg.

- Bank of France Survey: Expectations for inflation one year out ease to 3.5% in Q4 (prev. 4%); 3.5% increase in wages (prev. 3%)

FX

- DXY propped up by the softer Pound and Euro, though with gains capped by upside in the Yen; within a 102.14-34 range.

- The Pound is the G10 laggard post-CPI, falling to a session low of 1.2648.

- EUR is weighed on by the firmer Dollar, with softer German PPI unhelpful for the Single-Currency while EUR/GBP action offers only marginal respite.

- The Yen is the best performer amongst the G10s, paring back some of yesterday's BoJ's induced losses, but yet to test 143.00.

- PBoC sets USD/CNY mid-point at 7.0966 vs exp. 7.1300 (prev. 7.0982)

Fixed Income

- USTs are modestly higher in tandem with Gilts as markets await the US 20yr auction and further speak from Fed's Goolsbee.

- Gilts outperforms after cooler-than-expected UK CPI, adding to dovish expectations for 2024; gapped higher by almost 100 ticks and thereafter eclipsed 103.00.

- Bunds are bid in conjunction with Gilts and after its own softer Producer Prices metrics; German 10yr yield sub-2.0% for the first time since March.

Commodities

- WTI and Brent (+1.2%) are bid having spent the overnight session relatively indecisive; specifics have been light and largely led by geopolitical themes.

- Spot Gold (-0.1%) resides on either side of the unchanged mark, holding on to the prior day's gains; Base metals are generally in the green, though with gains capped amid poorer sentiment in China overnight.

- Intensive talks are underway on a potential second Gaza truce, via Reuters citing sources; envoys looking at which hostages could go free.

Geopolitics

- US reportedly weighs whether to attack Houthis beyond defensive task force and possible strikes on Houthis in Yemen considered, according to Bloomberg sources; no decision made yet on striking Houthis. The US and its allies are considering possible military strikes against Houthi rebels in Yemen, in recognition that a newly announced maritime task force meant to protect commercial ships in the Red Sea may not be enough to eliminate the threat to the vital waterway. Planning is underway for actions intended to cripple the Houthis’ ability to target commercial ships by hitting the militant group at the source.

- Israel is offering to pause the fighting in Gaza for at least one week as part of a new deal to get Hamas to release more than three dozen hostages, according to Axios sources.

- Malaysia bans Israeli-based shipping firm Zim from its ports, with the ban set to take effect immediately, according to the Malaysian PM.

US Event Calendar

- 07:00: Dec. MBA Mortgage Applications -1.5%, prior 7.4%

- 08:30: 3Q Current Account Balance, est. -$196b, prior -$212.1b

- 10:00: Nov. Home Resales with Condos, est. 3.78m, prior 3.79m

- Nov. Existing Home Sales MoM, est. -0.4%, prior -4.1%

- 10:00: Dec. Conf. Board Consumer Confidence, est. 104.5, prior 102.0

- Dec. Conf. Board Present Situation, prior 138.2

- Dec. Conf. Board Expectations, prior 77.8

DB's Henry Allen concludes the overnight wrap

The relentless market rally has continued over the last 24 hours, with investors remaining confident that central banks will soon pivot towards rate cuts, despite the pushback from several officials over recent days. In fact, yesterday saw the S&P 500 (+0.59%) hit another 23-month high, which leaves the index less than 1% beneath its all-time closing peak back in January 2022. That also means t he index has now risen by +15.8% in less than two months, and we haven’t seen an advance that fast since March-May 2020, back when the S&P 500 was recovering from the initial Covid selloff. At the same time, sovereign bonds have continued to rally, and overnight the 10yr Treasury yield has fallen to its lowest level since July, at 3.91% .

This growing anticipation of rate cuts was supported by Richmond Fed President Barkin, who said that “If you’re going to assume that inflation comes down nicely, of course we would respond appropriately”. That helped push Treasury yields lower, and offered support for the idea that the Fed would cut rates if inflation fell, since otherwise it would mean that policy was becoming more restrictive in real terms. But we also had a more hawkish take from Atlanta Fed President Bostic, who said that “there’s not going to be urgency for us to pull off our restrictive stance”, expecting only two rate cuts in 2024, rather than the three rate cuts that the median dot suggested. Both are voting members of the FOMC in 2024.

Against that backdrop, investors continued to price in a strong chance of a Fed rate cut by March, with the probability moving up from 75% to 83% yesterday. And it was the same story for the ECB, where the chance of a March cut rose from 35% to 49%, even as Latvia’s central bank governor said that “it is too early to declare victory over inflation” .

Those moves led to a s izeable rally in sovereign bonds in the European session. Yields on 10yr OATs (-8.5bps) fell to their lowest level since February, those on 10yr gilts (-4.3bps) fell to their lowest since April, and those on 10yr BTPs (-13.4bps) were at their lowest since December 2022. 10yr bund yields (-6.3bps) also fell back, although they were just above their closing level from Friday, at 2.01%. Over in the US, 10yr Treasury yields had traded nearly -4bps lower early on in the US session but were flat by the close (-0.1bps) at 3.93%, but overnight they’ve since fallen -2.4bps to 3.91%.

That growing conviction about rate cuts came despite some hawkish-leaning data that was released yesterday. For instance, Canada’s CPI print for November was stronger than expected, with headline CPI remaining at +3.1% (vs. +2.9% expected). Moreover, US housing starts also surprised on the upside, hitting a 6-month high in November as they rose to an annualised rate of 1.56m (vs. 1.36m expected). The release meant that the Atlanta Fed’s GDPNow estimate rose another tenth yesterday, and it now sees US Q4 GDP expanding at an annualised +2.7% pace .

The prospect of faster growth alongside rate cuts proved supportive for equities, and the S&P 500 (+0.59%) advanced for the 8th time in the last 9 sessions. It was a broad-based advance, with 23 of the 24 S&P 500 industry group up on the day and both the FANG+ index (+0.51%) and the Dow Jones (+0.68%) reaching all-time highs. Small-cap stocks did particularly well on the day, and the Russell 2000 (+1.94%) surpassed its recent peak in July to close at its highest level since August 2022. Meanwhile in Europe, the STOXX 600 (+0.36%) closed at a 22-month high, with its YTD gain now standing at +12.27%.

That optimism has been echoed in Asia overnight, where most indices have seen a decent rally. That includes the KOSPI (+1.65%), the Nikkei (+1.51%) and the Hang Seng (+1.08%), although the CSI 300 (-0.50%) and the Shanghai Comp (-0.42%) have seen an underperformance. That follows the move by Chinese banks to leave the 1yr and 5yr loan prime rate unchanged. Otherwise, US equity futures are broadly flat this morning, with those on the S&P 500 up +0.03%.

Meanwhile in Japan, sovereign bond yields have continued to fall after the BoJ’s decision to leave its policy unchanged yesterday, with the 10yr JGB yield down a further -6.4bps overnight to its lowest since July, at 0.55%. As we were going to press yesterday, Governor Ueda said in the press conference that there “isn’t much likelihood of us suddenly announcing that we’ll raise rates a month in advance”, so that’s a different approach to other central banks like the Fed, who tend to signal their moves in advance. Looking forward, investors still see a serious probability that the BoJ will move away from their negative interest rate policy over the months ahead, and currently they price in a 39% chance of a shift in January, and a 75% chance of a move by April. This morning, the Japanese yen has stabilised against the dollar, strengthening +0.10% to trade at 143.69 per dollar as we go to press. However, Japanese banks have continued to lose ground amidst the continuation of low borrowing costs, and the TOPIX Banks Index (-0.19%) is on track to lose ground for a 5th consecutive session, and is currently at its lowest level since July .

In the commodity space, oil prices advanced yesterday, with Brent crude up +1.64% to $79.23/bbl and WTI up +1.34% to $73.44/bbl. The two oil benchmarks have risen by +8.2% and +7.0% respectively over the past week, with the main driver being the pause of much commercial shipping via the Red Sea in response to recent attacks and rising perceptions of geopolitical risks.

To the day ahead now, and data releases from the US include the Conference Board’s consumer confidence for December, existing home sales for November, and the Q3 current account balance. In the Euro Area, there’s the European Commission’s preliminary consumer confidence indicator for December, and there’s also the UK CPI and German PPI readings for November. From central banks, we’ll hear from the Fed’s Goolsbee and the ECB’s Lane.

US equity futures and global markets reversed their torrid rally as bonds rallied and the dollar gained after a fresh batch of soft inflation data in the UK boosted the likelihood of interest-rate cuts, but also underscored the risk of an economic downturn. As of 7:45am, S&P eminis dropped 0.2% after the index notched a record high for the third successive session, with European and Asian stocks in the red. Germany 10-year yields dropped below 2% for the first time in nine months after a report showed producer prices fell more than expected in November. Meanwhile, British 10-year borrowing costs slid as much as 11 basis points as slower-than-expected inflation boosted the case for multiple rate cuts next year. Treasury yields slid four basis points to 3.9%, down more than 40 this month. Brent jumped above $80 to a 3 week high after the US considered possible military strikes against Houthi rebels in Yemen, in a recognition that a newly announced maritime task force meant to protect commercial ships in the Red Sea may not be enough to eliminate the threat to the vital waterway. US economic data includes 3Q current account balance (8:30am), November existing home sales and December consumer confidence (10am).

In premarket trading, FedEx shares tumbled as 10% after the parcel company’s fiscal second-quarter profit came in below expectations, with analysts pointing to a particularly disappointing performance from the Express air-freight unit, which was hit by slowing volumes. Brokers added that the company’s outlook lacked visibility, with Citi calling it “vague.” Here are some other notable premarket movers:

- Cinemark drops 3.5% in premarket trading as Wells Fargo downgrades the movie theater operator to underweight from equal-weight based on an unattractive box office outlook.

- Clear Channel Outdoor Holdings rises 7.7% in premarket trading on Wednesday after Wells Fargo Securities raised the recommendation on the advertising company to overweight from equal-weight. The broker says the upgrade comes as the company returns to growth.

- Coupang slides 1.6% in premarket trading as UBS downgrades its rating to neutral, awaiting greater clarity on the e-commerce company’s strategy.

- Discover Financial shares rise as much as 1.4% in premarket trading Wednesday after the credit card issuer was upgraded to buy from neutral at Citigroup, which also opened a 90-day catalyst watch on the stock saying investors should get more insight about the scope of credit losses when it reports fourth-quarter results in January.

- General Mills (GIS) slides 4.7% ahead of the bell after the packaged food company reported organic volume and sales for the second quarter that fell short of consensus estimates. GIS also cut its annual organic sales forecast, citing a slower-than-expected volume recovery amid a more cautious consumer economic outlook and a faster normalization of product availability from competitors. .

- Kellanova, Kraft Heinz and Conagra fall premarket after General Mills reported sales and volumes that missed consensus estimates for the second quarter and cut its annual organic sales view. Kellanova -1.6%, Kraft -1.2%, Conagra -1%.

Markets have rallied hard in recent weeks after the Fed’s dovish pivot which helped put the tech-heavy Nasdaq 100 on course for its best year since 1999, while the S&P 500 is less than 1% off its record closing peak. Bulls got fresh encouragement Tuesday from Richmond Fed President Thomas Barkin, who suggested the US central bank would “respond appropriately” if recent progress on inflation continued. Money markets now price almost a 50% chance of an euro-area rate cut by next March, while seeing an even higher probability of a Fed cut that month. That said, even Powell’s unofficial mouthpiece, Nikileaks, aka Nick Timiraos is now warning that the market that it has gone up too far, too fast.

Since their meeting last week, Fed officials have been flummoxed that investors expect even faster and deeper cuts. The result: Confusion over when and how quickly the Fed might cut.

“The Fed shouldn’t have been surprised by the market running with it.” https://t.co/Tth5I2NzXe

— Nick Timiraos (@NickTimiraos) December 20, 2023

At the same time, investors are also having to balance rate-cut optimism against the risk of economic recession. Recent data has backed that view, especially in the euro area, with analysts surveyed by Bloomberg forecasting the first recession since the pandemic.

“It’s hard to see such a fast and deep rate-cutting cycle as the market appears to assume, unless the base case is a deep recession,” said Daniele Antonucci, chief investment officer at Quintet Private Bank.

Investors are also starting to weigh risks stemming from potential shipping delays and freight cost increases, as companies divert cargoes away from the Red Sea to avoid militant attacks. This rerouting will mean higher shipping costs and longer delivery time, and has helped push brent crude prices above $80 for the first time in 3 weeks.

The big econ news overnight was the latest confirmation that a global deflationary wave is being unleashed, with UK reporting inflation that came in below the lowest estimate. The UK data “adds to the mounting evidence that global inflation has begun to crumble on a broader basis,” said Christoph Rieger, head of rates research at Commerzbank.

While the data initially boosted European stocks, gains on the Stoxx 600 index quickly evaporated, though London’s export-oriented FTSE 100 benchmark held its gains as the pound tumbled on the prospect of looser monetary policy. The telecom sector lead the advance, boosted by Spain’s Telefonica. The health-care sector underperforms, meanwhile, dragged lower by Argenx, which plunges after disappointing drug trial data. Among single stocks, shipping companies Hapag Lloyd AG and AP Moller-Maersk A/S rallied as militant attacks continued to disrupt Red Sea container traffic. Here are the biggest movers Wednesday:

- Telefonica shares jump as much as 7.2% after the Spanish state unveiled a plan to buy up to 10% in the telecom operator to counter stakebuilding by Saudi Telecom Co.

- Intertek gains as much as 3.7% after BNP Paribas Exane double-upgrades to outperform, saying in note that consensus is now overly bearish on margin outlook

- Raiffeisen Bank surges 12%, the most since March 2022, following its deal to buy a stake in Austrian construction company Strabag, with Citi upgrading the stock to buy from neutral

- British stocks rally as data showed inflation in the UK slowed far more than expectations, driving European stocks closer to early 2022 record, with landlords leading the advance

- Indivior gains as much as 4.5% after settling a drug patent dispute with rival Actavis, which now is granted a license to the patent that would enable Actavis to launch a generic variant

- Ionos gains for a ninth day as Morgan Stanley says the webhosting firm has delivered “two early Christmas presents” in strong guidance on Tuesday and last week’s debt refinancing.

- Argenx shares plunge as much as 35% after its key drug Vyvgart (efgartigimod) failed another trial, a second setback in less than a month for the Brussels-listed biotech firm

- DS Smith falls as much as 2.8% after UBS downgraded the paper and packaging company to neutral from buy, saying the downgrade reflects weaker containerboard prices

- Inficon shares fell as much as 5.3%, the most in two months, after the Swiss vacuum instruments manufacturer was downgraded to reduce from add at Baader Helvea

- Resurs Holding drops as much as 8.3% after SEB Equities downgrades the retail finance company to sell from hold, giving the stock its only negative analyst rating

Earlier in the session, Asian stocks rose for a second straight day, as Japanese shares extended gains following the Bank of Japan’s decision to stand pat on interest rates on Tuesday. The MSCI Asia Pacific Index advanced as much as 1% to its highest since Aug. 8, with Tencent and Samsung Electronics among the biggest contributors to the gauge’s rise. Exporter stocks led Japan’s benchmarks higher as the yen weakened after the country held on to the world’s last negative interest rate regime. Indexes across South Korea, Hong Kong and Southeast Asia also gained as traders looked past Federal Reserve officials’ pushback on aggressive interest rate-cut expectations. The gains across Asia follow two days of cautious trading during which investors assessed the path of US monetary policy in 2024.

- Hang Seng and Shanghai Comp traded mixed with the former’s gains spearheaded by large caps with US listings, including Alibaba, JD.com, and Baidu. Mainland China was subdued after PBoC maintained its Loan Prime Rates as expected and despite more liquidity injections by the central bank.

- Nikkei 225 surged as the index reacted to BoJ Governor Ueda’s dovish press conference following the unchanged announcement yesterday.

- ASX 200 saw its upside supported by the Energy and Metals sectors, whilst Tech lagged with shallower gains.

In FX, GBP/USD falls as much as 0.7% to below $1.27 after UK CPI data, EUR/USD down 0.3%; the Bloomberg Dollar Spot Index is largely unchanged as the US currency’s gains versus European currencies are offset by its slide against the yen. The Japanese yen is the best performer among the G-10 currencies, rising 0.3% versus the greenback on false expectations that the BOJ will end its negative rate policy in the coming months which has supported the yen. The dollar has been struggling as investors seek more guidance from the Fed on how soon it will begin cutting rates next year as inflation slows; however Chicago Fed’s Goolsbee said on Tuesday that the market may be getting ahead of itself when it comes to rate cuts.

“Speculative bets on a BOJ policy change are likely to ease for now,” said Fukuhiro Ezawa, head of financial markets in Tokyo at Standard Chartered Bank. “Markets price in deep Fed rate cuts, weighing on the dollar” against peers including the yen, he said

In rates, the yield on the 10-year US Treasury slips 4bps to 3.88%, its lowest since late July. Traders are betting that the Fed will cut rates by 150bps by the end of 2024, compared with around 140 bps on Tuesday. UK gilts rallied while the pound drops after data showed UK inflation slowed more than expected in November, fueling bets on interest rate cuts by the Bank of England next year. UK two-year yields fall 15 basis points to 4.14%, a seven-month low.

In commodities, oil extended its recent rally amid prospects of more disruptions in the Red Sea, while the US weighs military strikes on Houthis. Brent jumped above $80 to a three week high. Brent March call options in the $90s were active again on Tuesday as traders continue to weigh the risks to traffic in the Red Sea. WTI’s second-month 25-delta put skew was the least bearish since mid-November. Brent’s prompt spread climbed to the strongest since Dec. 5, while its Dec.-Dec. spread was the firmest this month.

Bitcoin (+0.6%) and Ethereum (+1.2%) extended gains as BTC rose back over USD 43k. BlackRock, Nasdaq, SEC met regarding a Bitcoin (BTC) ETF, via CoinDesk

Looking to the day ahead now, and data releases from the US include the Conference Board’s consumer confidence for December, existing home sales for November, and the Q3 current account balance. In the Euro Area, there’s the European Commission’s preliminary consumer confidence indicator for December, and there’s also the UK CPI and German PPI readings for November. From central banks, we’ll hear from the Fed’s Goolsbee and the ECB’s Lane.

Market Snapshot

- S&P 500 futures down 0.2% to 4,812.50

- STOXX Europe 600 little changed at 476.63

- MXAP up 0.5% to 165.32

- MXAPJ up 0.2% to 515.45

- Nikkei up 1.4% to 33,675.94

- Topix up 0.7% to 2,349.38

- Hang Seng Index up 0.7% to 16,613.81

- Shanghai Composite down 1.0% to 2,902.11

- Sensex down 1.1% to 70,636.67

- Australia S&P/ASX 200 up 0.7% to 7,537.88

- Kospi up 1.8% to 2,614.30

- German 10Y yield little changed at 1.99%

- Euro down 0.2% to $1.0961

- Brent Futures up 0.8% to $79.87/bbl

- Gold spot up 0.1% to $2,041.67

- U.S. Dollar Index little changed at 102.26

Top Overnight News

- Bond yields across the euro region fell on Wednesday as worsening economic data and slowing inflation underscored expectations for interest-rate cuts next year.

- UK inflation slowed far more than economists forecast in November, a surprise that prompted traders to boost bets the Bank of England will soon have to abandon its higher-for-longer narrative on interest rates.

- Attacks in the Red Sea linked to the Israel-Hamas war will cause shipping delays and drive up the price of goods, bringing a new inflation risk to the economy.

- Jonathan Hoffman, John Bonello and Jonathan Tipermas share more than just similar first names. They’re the driving force behind a gigantic wager on government debt that’s been giving regulators sleepless nights.

- Donald Trump is ineligible to serve as US president because of his actions inciting the Jan. 6, 2021 attack on the US Capitol, Colorado’s highest court found, in an unprecedented ruling that’s headed for the US Supreme Court.

- Throngs of consultants wearing Western attire have become a common sight in the lobbies of Riyadh’s plushest hotels as Crown Prince Mohammed Bin Salman embarks on a multi-trillion dollar plan to wean Saudi Arabia off oil. In recent months they’ve been joined by another cohort of besuited individuals: fund managers, keen to get an early foothold in the next big emerging-market growth story.

A more detailed look at global markets courtesy of NEwsquawk

Asia-Pac stocks traded mostly positively following the tailwinds from Wall Street, although newsflow overnight was on the quieter side amid the pre-Christmas lull. ASX 200 saw its upside supported by the Energy and Metals sectors, whilst Tech lagged with shallower gains. Nikkei 225 surged as the index reacted to BoJ Governor Ueda’s dovish press conference following the unchanged announcement yesterday. Hang Seng and Shanghai Comp traded mixed with the former’s gains spearheaded by large caps with US listings, including Alibaba, JD.com, and Baidu. Mainland China was subdued after PBoC maintained its Loan Prime Rates as expected and despite more liquidity injections by the central bank.

Top Asian News

- PBoC maintained its 1-year and 5-year LPRs at 3.45% and 4.20% respectively, as expected.

- PBoC injected CNY 134bln through 7-day reverse repos at 1.80% and CNY 151bln via 14-day reverse repos at 1.95%; both rates maintained

- The Japanese government is to raise its long-term interest rate estimate to 1.9% for FY24 from 1.1% in FY23, according to Nikkei.

- Japanese Cabinet projects that income will increase more than prices in FY24, according to Nikkei.

- State-backed developer China South City averts default on July 2024 note after consent from bondholders, according to SCMP.

- RBNZ Governor Orr said interest rates are restricting spending and levels of core inflation remain too high, according to the Parliamentary hearing. He noted that Q3 GDP was surprisingly subdued, and inflation remains too high and the committee remains wary of ongoing inflationary surprises. He said the neutral interest rate is now 2.5%.

- New Zealand DMO and fiscal update: gross bond issuance for four years to June 2027 now totals NZD 136bln, up from NZD 129bln in the budget. 2023/24 gross bond issuance increases to NZD 38bln from NZD 36bln in budget. Treasury sees GDP growth in Q4 23 and through 2024.

- Japan is to draft an initial FY24 budget of JPY 112tln, via Kyodo News

- Japanese government is to lower the scheduled sales of JGBs to market by 11.2% from FY23 plan to JPY 171tln in FY24/25, via Reuters citing a draft

European bourses, Eurostoxx50 (-0.2%), are marginally weaker having spent much of the morning the green; the FTSE 100 (+0.8%) outperforms post-UK CPI. European sectors are mixed with Energy outperforming lifted by gains in underlying Crude prices and Telefonica (+5%) helps lift Telecoms; Technology narrowly lags. US Equity Futures are lower across the board as the Santa Rally comes to a pause, ES (-0.2%); FedEx (-9.9%) extends losses in the pre-market post-earnings.

Top European News

- ECB’s Nagel says there is a high probability that the interest rate peak has been reached, according to t-online; would say to everyone who is speculating on an imminent interest rate cut: be careful, some people have already speculated.

- France and Germany see an EU deal on fiscal rules on Wednesday, according to Bloomberg.

- Bank of France Survey: Expectations for inflation one year out ease to 3.5% in Q4 (prev. 4%); 3.5% increase in wages (prev. 3%)

FX

- DXY propped up by the softer Pound and Euro, though with gains capped by upside in the Yen; within a 102.14-34 range.

- The Pound is the G10 laggard post-CPI, falling to a session low of 1.2648.

- EUR is weighed on by the firmer Dollar, with softer German PPI unhelpful for the Single-Currency while EUR/GBP action offers only marginal respite.

- The Yen is the best performer amongst the G10s, paring back some of yesterday’s BoJ’s induced losses, but yet to test 143.00.

- PBoC sets USD/CNY mid-point at 7.0966 vs exp. 7.1300 (prev. 7.0982)

Fixed Income

- USTs are modestly higher in tandem with Gilts as markets await the US 20yr auction and further speak from Fed’s Goolsbee.

- Gilts outperforms after cooler-than-expected UK CPI, adding to dovish expectations for 2024; gapped higher by almost 100 ticks and thereafter eclipsed 103.00.

- Bunds are bid in conjunction with Gilts and after its own softer Producer Prices metrics; German 10yr yield sub-2.0% for the first time since March.

Commodities

- WTI and Brent (+1.2%) are bid having spent the overnight session relatively indecisive; specifics have been light and largely led by geopolitical themes.

- Spot Gold (-0.1%) resides on either side of the unchanged mark, holding on to the prior day’s gains; Base metals are generally in the green, though with gains capped amid poorer sentiment in China overnight.

- Intensive talks are underway on a potential second Gaza truce, via Reuters citing sources; envoys looking at which hostages could go free.

Geopolitics

- US reportedly weighs whether to attack Houthis beyond defensive task force and possible strikes on Houthis in Yemen considered, according to Bloomberg sources; no decision made yet on striking Houthis. The US and its allies are considering possible military strikes against Houthi rebels in Yemen, in recognition that a newly announced maritime task force meant to protect commercial ships in the Red Sea may not be enough to eliminate the threat to the vital waterway. Planning is underway for actions intended to cripple the Houthis’ ability to target commercial ships by hitting the militant group at the source.

- Israel is offering to pause the fighting in Gaza for at least one week as part of a new deal to get Hamas to release more than three dozen hostages, according to Axios sources.

- Malaysia bans Israeli-based shipping firm Zim from its ports, with the ban set to take effect immediately, according to the Malaysian PM.

US Event Calendar

- 07:00: Dec. MBA Mortgage Applications -1.5%, prior 7.4%

- 08:30: 3Q Current Account Balance, est. -$196b, prior -$212.1b

- 10:00: Nov. Home Resales with Condos, est. 3.78m, prior 3.79m

- Nov. Existing Home Sales MoM, est. -0.4%, prior -4.1%

- 10:00: Dec. Conf. Board Consumer Confidence, est. 104.5, prior 102.0

- Dec. Conf. Board Present Situation, prior 138.2

- Dec. Conf. Board Expectations, prior 77.8

DB’s Henry Allen concludes the overnight wrap

The relentless market rally has continued over the last 24 hours, with investors remaining confident that central banks will soon pivot towards rate cuts, despite the pushback from several officials over recent days. In fact, yesterday saw the S&P 500 (+0.59%) hit another 23-month high, which leaves the index less than 1% beneath its all-time closing peak back in January 2022. That also means t he index has now risen by +15.8% in less than two months, and we haven’t seen an advance that fast since March-May 2020, back when the S&P 500 was recovering from the initial Covid selloff. At the same time, sovereign bonds have continued to rally, and overnight the 10yr Treasury yield has fallen to its lowest level since July, at 3.91% .

This growing anticipation of rate cuts was supported by Richmond Fed President Barkin, who said that “If you’re going to assume that inflation comes down nicely, of course we would respond appropriately”. That helped push Treasury yields lower, and offered support for the idea that the Fed would cut rates if inflation fell, since otherwise it would mean that policy was becoming more restrictive in real terms. But we also had a more hawkish take from Atlanta Fed President Bostic, who said that “there’s not going to be urgency for us to pull off our restrictive stance”, expecting only two rate cuts in 2024, rather than the three rate cuts that the median dot suggested. Both are voting members of the FOMC in 2024.

Against that backdrop, investors continued to price in a strong chance of a Fed rate cut by March, with the probability moving up from 75% to 83% yesterday. And it was the same story for the ECB, where the chance of a March cut rose from 35% to 49%, even as Latvia’s central bank governor said that “it is too early to declare victory over inflation” .

Those moves led to a s izeable rally in sovereign bonds in the European session. Yields on 10yr OATs (-8.5bps) fell to their lowest level since February, those on 10yr gilts (-4.3bps) fell to their lowest since April, and those on 10yr BTPs (-13.4bps) were at their lowest since December 2022. 10yr bund yields (-6.3bps) also fell back, although they were just above their closing level from Friday, at 2.01%. Over in the US, 10yr Treasury yields had traded nearly -4bps lower early on in the US session but were flat by the close (-0.1bps) at 3.93%, but overnight they’ve since fallen -2.4bps to 3.91%.

That growing conviction about rate cuts came despite some hawkish-leaning data that was released yesterday. For instance, Canada’s CPI print for November was stronger than expected, with headline CPI remaining at +3.1% (vs. +2.9% expected). Moreover, US housing starts also surprised on the upside, hitting a 6-month high in November as they rose to an annualised rate of 1.56m (vs. 1.36m expected). The release meant that the Atlanta Fed’s GDPNow estimate rose another tenth yesterday, and it now sees US Q4 GDP expanding at an annualised +2.7% pace .

The prospect of faster growth alongside rate cuts proved supportive for equities, and the S&P 500 (+0.59%) advanced for the 8th time in the last 9 sessions. It was a broad-based advance, with 23 of the 24 S&P 500 industry group up on the day and both the FANG+ index (+0.51%) and the Dow Jones (+0.68%) reaching all-time highs. Small-cap stocks did particularly well on the day, and the Russell 2000 (+1.94%) surpassed its recent peak in July to close at its highest level since August 2022. Meanwhile in Europe, the STOXX 600 (+0.36%) closed at a 22-month high, with its YTD gain now standing at +12.27%.

That optimism has been echoed in Asia overnight, where most indices have seen a decent rally. That includes the KOSPI (+1.65%), the Nikkei (+1.51%) and the Hang Seng (+1.08%), although the CSI 300 (-0.50%) and the Shanghai Comp (-0.42%) have seen an underperformance. That follows the move by Chinese banks to leave the 1yr and 5yr loan prime rate unchanged. Otherwise, US equity futures are broadly flat this morning, with those on the S&P 500 up +0.03%.

Meanwhile in Japan, sovereign bond yields have continued to fall after the BoJ’s decision to leave its policy unchanged yesterday, with the 10yr JGB yield down a further -6.4bps overnight to its lowest since July, at 0.55%. As we were going to press yesterday, Governor Ueda said in the press conference that there “isn’t much likelihood of us suddenly announcing that we’ll raise rates a month in advance”, so that’s a different approach to other central banks like the Fed, who tend to signal their moves in advance. Looking forward, investors still see a serious probability that the BoJ will move away from their negative interest rate policy over the months ahead, and currently they price in a 39% chance of a shift in January, and a 75% chance of a move by April. This morning, the Japanese yen has stabilised against the dollar, strengthening +0.10% to trade at 143.69 per dollar as we go to press. However, Japanese banks have continued to lose ground amidst the continuation of low borrowing costs, and the TOPIX Banks Index (-0.19%) is on track to lose ground for a 5th consecutive session, and is currently at its lowest level since July .

In the commodity space, oil prices advanced yesterday, with Brent crude up +1.64% to $79.23/bbl and WTI up +1.34% to $73.44/bbl. The two oil benchmarks have risen by +8.2% and +7.0% respectively over the past week, with the main driver being the pause of much commercial shipping via the Red Sea in response to recent attacks and rising perceptions of geopolitical risks.

To the day ahead now, and data releases from the US include the Conference Board’s consumer confidence for December, existing home sales for November, and the Q3 current account balance. In the Euro Area, there’s the European Commission’s preliminary consumer confidence indicator for December, and there’s also the UK CPI and German PPI readings for November. From central banks, we’ll hear from the Fed’s Goolsbee and the ECB’s Lane.

Loading…