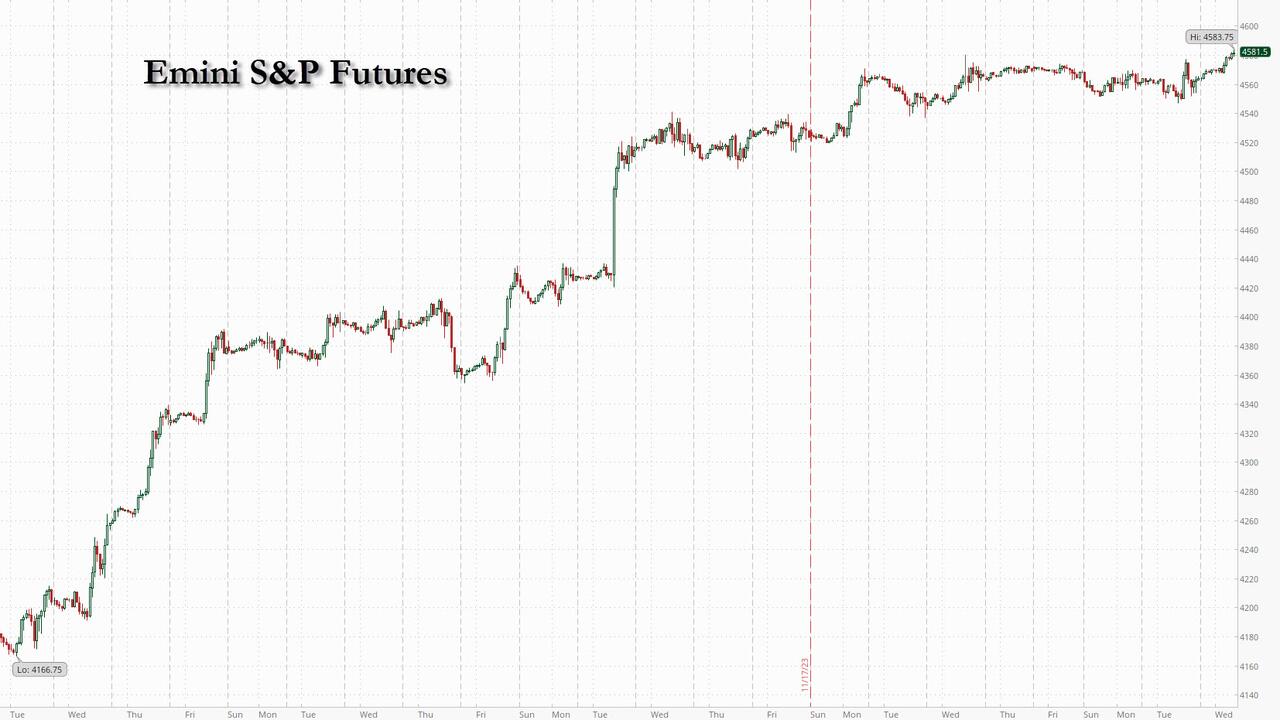

US equity futures, global markets and Treasuries extended their recent rallyall boosted by expectations that the Federal Reserve is not only done with hjking but will soon pivot and start cut rates early next year; in fact, according to Bill Ackman who has again flipflopped, the Fed will cut as soon as March (i.e., he is now long the same bonds he was so passionately shorting just a few months ago). This occurs as consumer confidence moved higher with holiday, retail sales numbers that illustrate a still strong consumer. As of 7:45am, US equity futures are up 0.4%, rising to the highest since Sept 1 and just shy of 2023 highs, while Nasdaq futures gained 0.6%; gold traded near record high, the dollar slide halted but is certainly not over, WTI oil futures rose 1.7% on the day, adding to Tuesday’s advance, while bitcoin traded just above $38K. The big question now is whether this rally can extend into December; the answer may be predicated on fundamentals rather than positioning/technicals. BBG reporting an uptick in corporate insider buying alongside stronger buyback activity. Today’s macro data focus includes 23Q3 GDP/Consumption/PCE, Beige Book, inventories, trade balance, and mtge applications.

In premarket trading, tech and small-caps are outperforming; megacap teach names are higher having added almost 14% MTD. General Motors jumped almost 6% in US premarket trading after announcing it will boost its dividend by 33% and implement a $10 billion share buyback program. Las Vegas Sands shares fell 5.6% as Miriam Adelson is selling $2 billion of stock in the casino company so the family can acquire a majority stake in the Dallas Mavericks NBA franchise from Mark Cuban. GameStop shares jump 12%, putting the stock on track to extend gains for a second consecutive session, ahead of its third-quarter results next week. Here are some other notable premarket movers:

- Airbnb shares slip 0.8% after Jefferies cut its recommendation on the short-term rental platform’s stock to hold from buy, citing a recent slowdown in bookings.

- CrowdStrike Holdings shares edged higher, rising 3.0%, after the security software company reported third-quarter results that beat expectations and raised its full-year revenue forecast.

- Fluence Energy shares jump 19% after the energy storage company’s results beat expectations, with analysts positive on its orders and prospects for 2024, especially against investors’ more sombre view on the renewables sector.

- NetApp shares jump 12% after the data storage company boosted its full-year adjusted earnings per share forecast above analyst expectations. Additionally, the company also reported second-quarter revenue that beat estimates. Analysts highlighted the traction in new products as well as strength in all-flash solutions.

- Okta shares fell 6.2% after the applications software company said it has found that hackers who had breached its network stole information on all users of its customer support system.

- Workday shares rise 8.92% after the application software company reported third-quarter results that beat expectations and raised its full-year forecast for subscription revenue.

- Foot Locker Inc surged as much as 13% after comparable sales beat the average analyst estimate.

The November stock party continues and the MSCI All Country World Index of stocks has gained 8.7% so far this month, the most since November 2020 amid a collapsing dollar (which however today paused a four-day retreat). It's not just stocks that are soaring: in the latest rerun of the QE trade, bonds are climbing at the fastest monthly pace since 2008 as inflation continues to slow and Fed officials strike a dovish tone.

The latest leg higher for stocks and bonds came after the otherwise hawkish Fed Governor Christopher Waller suggested the central bank is well positioned to push inflation to a 2% target. And then overnight, Bill Ackman said he’s betting Fed cuts could come as soon as the first quarter, something we first said two weeks ago.

It takes 8 months on average from the last rate hike to the first rate cut. So March https://t.co/J9IULydqcA pic.twitter.com/SXFwn95DEA

— zerohedge (@zerohedge) November 14, 2023

"The market is hanging on to everything Fed speakers say,” said Justin Onuekwusi, chief investment officer at UK wealth manager St James Place. “It was only the end of October when we were talking of 5% yields on US Treasuries. It does feel like the market is being a bit complacent."

Now, traders are looking ahead to data on Thursday that include the Fed’s preferred measure of underlying inflation, the core PCE, as well as a speech by Fed Chair Jerome Powell at the end of the week that could offer clues on potential policy easing. “I would expect some pushback on market rate expectations,” said Marc Ostwald, chief economist & global strategist at ADM Investor Services Int. Ltd. “Inflation will have to drop sharply in the coming months, and the labor market will need to loosen a lot more to justify a rate cut in the first half of 2024.”

European stocks are in the green after posting back-to-back losses for the first time in three weeks. The Stoxx 600 is up 0.6%, led by gains in real estate, auto and technology shares. The autos and real estate sectors are the best performers, with many property shares getting a boost from a renewed decline in yields. The energy and insurance sectors are the worst performers. Philips slumps on a new apnea machine safety issue. Here are some of the biggest movers on Wednesday:

- Vestas shares rise as much as 4% after Berenberg lifts recommendation on Danish wind turbine producer to buy from hold, citing rising momentum in margins over the last two quarters.

- BMW shares rise as much as 3.6%, with JPMorgan lauding a well balanced growth strategy at the German automaker and upgrading it to overweight from neutral.

- Musti shares gain as much as 29%, the most since the pet care firm went public in 2020, after the company’s board recommended a voluntary public cash tender offer from a group of investors that values the outstanding equity at €868m.

- Harbour Energy shares rise as much as 5.1% and is among leading gainers on the Stoxx 600 energy index on Wednesday, after delivering a nine-month update that analysts describe as solid.

- Ferrovial shares gain as much as 3.2% after Spanish construction firm agreed to sell its stake in the parent company of Heathrow Airport to Ardian and Saudi Arabia’s Public Investment Fund for a total of $3 billion.

- Saipem shares gain as much as 3% after the engineering company got two offshore contracts in Guyana and Brazil worth approximately $1.9b.

- Philips falls as much as 7.7% after the Food and Drug Administration warned about a new safety issue involving the company’s DreamStation 2 machines used to treat obstructive sleep apnea.

- Halfords shares slide as much as 23%, the biggest intraday decline since Jan. 12, after the motoring and cycling products retailer reported interim results. RBC Capital Markets said pretax profit was below their expectations due to a softer showing in the company’s retail business, while Peel Hunt noted that the wider market was “not playing ball.”

- Aroundtown shares slump as much as 11%, its second slump this month, after third quarter results showed deleveraging remains a major issue at the German real estate firm, according to Morgan Stanley.

- Kindred shares fall as much as 9.7%, the most since January, after the Stockholm-listed online gambling operator reported third-quarter earnings weighed down by poor margins in its sports betting segment. The outcome of a strategic review is, however, seen as positive due to cost savings.

The MSCI Asia Pacific gauge fell 0.3% erasing earlier gains, even as the US 10-year yield dropped below the closely watched 100-day average, as gains in Australia were tempered by heavy losses in Chinese technology shares. Meituan was the biggest drag on the regional gauge after the Chinese firm warned that growth in its main meal delivery business would slow this quarter. A measure of technology stocks in Hong Kong also dropped to its lowest level in two weeks.

- Hang Seng and Shanghai Comp declined with underperformance in Hong Kong after the recent rises in domestic money market rates and with the PBoC’s open market operations resulting in a net daily drain.

- Nikkei 225 swung between gains and losses with early pressure from a firmer currency before the index rebounded off lows, while there were also comments from BoJ Adachi who stuck to the dovish script as he noted it is appropriate to patiently maintain easy policy and if needed, the BoJ will take additional easing steps.

- Australian stocks climbed after inflation cooled more-than-expected in October, bolstering the case for the Reserve Bank to resume pausing interest rates next week. New Zealand stocks also rose after its central bank kept rates unchanged.

- Indian stocks rallied, with the NSE Nifty 50 Index reclaiming the psychological 20,000 mark for the first time since dropping below it in September. The S&P BSE Sensex rose 1.1% to 66,901.91 at the 3:30 p.m. close in Mumbai, while the Nifty finished 1% higher at 20,096.60. The Nifty has logged similar or greater gains eight times in the past year. The gauge rose further the next day on six occasions, posting an average 0.4% gain, according to data compiled by Bloomberg. Wednesday’s gains were driven by automobiles and banks, which rose over 1.5% each. The laggards were media and realty, which ended in the red.

In FX, the Bloomberg Dollar Spot Index is unchanged after falling as much 0.2% to 1228,70, its lowest since early August amid growing bets that the Federal Reserve may start cutting interest rates next year, after two hawkish Fed officials signaled they could be comfortable holding rates steady for now. The kiwi is the best performer among the G-10’s, rising 0.2% versus the greenback after a hawkish hold from the RBNZ. The Aussie lags after CPI slowed in October. Oil prices advance, with WTI rising 1.4% to trade near $77.40. Spot gold falls 0.2%.

In rates, treasuries were richer by 4bps-5bps across the curve amid bigger gains in core European rates following bullish German state CPI readings ahead of the national print at 8am New York time. Two-year Treasury yields dropped four basis points to 4.69% after shedding 15 basis points Tuesday. Fed swaps are anticipating over 100 basis points of rate cuts by the end of 2024. Meanwhile, 10-year TSY yields are around 4.28%, richer by 4bp vs Tuesday close while trailing bunds and gilts in the sector by 1.5bp and 1bp on the day; new 2-year note auctioned Monday traded as rich as 4.664%, lowest for a current issue since mid-July and approaching 200-day moving average. Swaps market looks for deeper rate cuts next year, with May contracts priced for 23bp of cuts, or 92% chance of a 25bp move. German bonds rallied for a third day, the longest stretch in a month, after regional and state inflation data showed that inflation continued to slow. German 10-year yields fall 4bps to 2.45%.

"Attention will now move to Chair Powell’s speech on Friday to see if the tone points to a clear pivot towards easing,” Daragh Maher, head of FX strategy for the US at HSBC, wrote in a research note. “If it materializes, this would clearly be a challenge to our bullish US dollar view”

In commodities, oil climbed for a second day as traders awaited a high-stakes OPEC+ meeting on supply. WTI rose 1.4% to trade near $77.40. Gold extended gains to its highest level since May, also buoyed by hopes of a Fed policy shift.

To the day ahead now, and data releases include the preliminary German CPI reading for November, UK mortgage approvals for October, and in the US there’s the second estimate of Q3’s GDP (median est. 5% vs 4.9% initial). From central banks, we’ll hear from BoE Governor Bailey, Cleveland Fed President Mester, and the Fed will be releasing their Beige Book.

Market Snapshot

- S&P 500 futures up 0.3% to 4,576.75

- STOXX Europe 600 up 0.5% to 459.11

- MXAP down 0.3% to 161.59

- MXAPJ down 0.3% to 504.05

- Nikkei down 0.3% to 33,321.22

- Topix down 0.5% to 2,364.50

- Hang Seng Index down 2.1% to 16,993.44

- Shanghai Composite down 0.6% to 3,021.69

- Sensex up 1.1% to 66,881.45

- Australia S&P/ASX 200 up 0.3% to 7,035.35

- Kospi little changed at 2,519.81

- German 10Y yield little changed at 2.47%

- Euro down 0.1% to $1.0979

- Brent Futures up 0.4% to $82.01/bbl

- Gold spot down 0.3% to $2,035.68

- U.S. Dollar Index up 0.11% to 102.86

Top Overnight News

- Jack Ma has urged Alibaba to “change and reform” as the ecommerce giant he founded tries to find a new path after abandoning parts of its ambitious restructuring plan and its main Chinese rival gains ground. FT

- Australia’s inflation cools, with the CPI rising 4.9% in Oct (down from +5.6% in Sept and below the Street’s +5.2% forecast). BBG

- Spanish inflation unexpectedly eased, retreating for the first time since June thanks to drops in the costs of fuel and tourism. Consumer prices rose 3.2% from a year earlier in November, data Wednesday showed. That compares with 3.5% the previous month and defied the median estimate in a Bloomberg survey of economists for an acceleration to 3.7%. BBG

- German regional inflation cools in Nov, including Baden Wuerttemberg +3.4% (down from +4.4% in Oct), Bavaria +2.8% (down from +3.7% in Oct), Brandenburg +4.1% (down from +4.6% in Oct), Hesse +2.9% (down from +3.6% in Oct), North Rhine Westphalia +3% (down from +3.1% in Oct), and Saxony +3.9% (down from +4.5% in Oct). BBG

- Russian President Vladimir Putin will not make peace in Ukraine before he knows the results of the November 2024 U.S. election, a senior U.S. State Department official said on Tuesday, amid concerns that a potential victory for former President Donald Trump could upend Western support for Kyiv. RTRS

- Bill Ackman is betting the Federal Reserve will begin cutting interest rates sooner than markets are predicting. The Pershing Square Capital Management founder said such a move could happen as soon as the first quarter. Traders are fully pricing in a rate cut in June, with the chance of a cut happening in May priced at about 80%, according to swaps market data. BBG

- WDAY shares rose more than 8% premarket after the cloud enterprise company raised its outlook for the year and reported higher-than-expected revenue in the third quarter. WSJ

- OpenAI’s revamped board of directors doesn’t plan to include representatives from outside investors, according to a person familiar with the situation. It’s a sign that the board will prioritize safety practices ahead of investor returns. The Information

- The head of Amazon’s cloud division has used recent turmoil at OpenAI to launch a thinly veiled attack on Microsoft, the artificial intelligence company’s biggest investor. “Things are moving so fast [in AI] and in that type of environment the ability to adapt is the most valuable capability that you can have,” Selipsky, AWS chief executive, said at its annual developer conference in Las Vegas on Tuesday. “You don’t want a cloud provider that’s beholden primarily to one model provider, you need a real choice . . . The events of the past 10 days have made that very clear.” FT

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed after the choppy performance on Wall St where stocks wavered, Treasuries rallied and the Dollar dipped on dovish Fed rhetoric, while the region also digested the RBNZ’s hawkish hold where it kept rates unchanged but signalled risks of a hike. ASX 200 was positive with the index helped by encouraging data including better-than-expected Construction Work Done which feeds into next week’s GDP release and after softer monthly CPI all but guaranteed a pause at the December RBA meeting. Nikkei 225 swung between gains and losses with early pressure from a firmer currency before the index rebounded off lows, while there were also comments from BoJ Adachi who stuck to the dovish script as he noted it is appropriate to patiently maintain easy policy and if needed, the BoJ will take additional easing steps. Hang Seng and Shanghai Comp declined with underperformance in Hong Kong after the recent rises in domestic money market rates and with the PBoC’s open market operations resulting in a net daily drain.

Top Asian News

- China's Vice Foreign Minister recently met with the EU's external action service deputy secretary and said that China is ready to strengthen communication and coordination with the EU side and make preparations for a China-EU summit before the end of the year. Furthermore, it was stated that the two sides need to grasp the general direction of China-EU relations, uphold mutually beneficial and win-win cooperation, as well as fully respect each other's core interests, according to Reuters.

- Japan's Finance Ministry will raise the assumed interest rate paid on bonds in the government's annual budget proposal for the first time in 17 years in fiscal 2024, reflecting policy shifts by the BoJ that have allowed yields to rise, according to Nikkei.

- BoJ Board Member Adachi said Japan is yet to see a positive wage-inflation cycle become embedded enough and it is appropriate to patiently maintain easy policy. Adachi also stated that if needed, the BoJ will take additional easing steps, while he added that the steps the BoJ took in October to make YCC more flexible are not aimed at laying the groundwork for policy normalisation.

- RBNZ kept the OCR unchanged at 5.50% as expected, while it reiterated that interest rates will need to remain at a restrictive level for a sustained period of time and interest rates are restricting spending in the economy with consumer price inflation declining as is necessary to meet the committee's remit. RBNZ said inflation remains too high and the committee remains wary of ongoing inflationary pressures, as well as noted that demand growth has eased but by less than anticipated and if inflationary pressures were to be stronger than anticipated, the OCR would likely need to increase further. Furthermore, the committee is confident the current OCR level is restricting demand but slightly raised OCR and CPI forecasts with the OCR seen at 5.63% in March 2024 (prev. 5.58%), 5.66% in December 2024 (prev. 5.50%), and 5.56% (prev. 5.36%) in March 2025, while annual CPI is seen at 2.5% by December 2024 (prev. 2.4%).

- RBNZ Governor Orr said in the press conference that they've been adamant on holding rates through next year and noted that the projection shows upward bias to rates but it is not a done deal. Orr also stated the risk to inflation is still more to the upside, while he is nervous that inflation has been outside the band for so long and concerned that longer-term inflation expectations are creeping up.

- REUTERS POLL: Chinese New Home Prices Growth expects at +3.0% Y/Y 2023 (vs 0% in August poll); 1.1% Y/Y in 2024 (1.0% in August poll)

European equities, Euro Stoxx 50 +0.6% are extending gains, but with clear underperformance in the FTSE100 -0.2%, albeit the UK index is off lows. European sectors have a strong positive tilt; featuring strength in Autos & Parts whilst Energy lags but with both sectors underpinned by broker moves. US Futures are trading on the front foot, NQ & ES +0.4%, with clear outperformance in the RTY +0.8% as it pares back yesterday's losses.

Top European News

- The number of businesses set up in the UK in 2022 fell by 7% to 337k as UK business creation was hit by high borrowing costs and weaker demand, according to analysis by FT citing data released last week by the Office of National Statistics.

- Several ECB regulators are reportedly planning to push to ease bank payout stance, according to Bloomberg

- ECB's Stournaras says ECB April cut bets seem a bit optimistic, via Politico; says the first rate cut could come in the middle of 2024. Early PEPP winddown risks hurting ECB credibility

- OECD raises 2023 US growth forecast to 2.4% (prev. 2.2%), 1.5% in 2024 (prev. 1.3%), sees 1.7% 2025; Sees Chinese growth 5.2% (prev. 5.1%), 4.7% (prev. 4.6%), 4.2% in 2025; Raises UK growth forecast to 0.5% (prev. 0.3%), trims 2024 0.7% (prev. 0.8%), 1.2% in 2025.

FX

- DXY finds underlying bids just shy of 102.50 and aims for 103.00

- Kiwi outperforms after hawkish RBNZ hold and Aussie caught in AUD/NZD cross-fire with added downside pressure from soft inflation data

- NZD/USD elevated within 0.6208-0.6134 range, AUD/USD depressed between 0.6676-20 parameters

- Euro undermined by weaker than forecast German state and Spanish CPI metrics. EUR/USD sub-1.1000, but holding near decent option expiry interest and former Fib resistance/breakout area

- Yen retreats towards 148.00 from circa 146.68 after dovish guidance from BoJ's Adachi

- PBoC set USD/CNY mid-point at 7.1031 vs exp. 7.1340 (prev. 7.1132).

Fixed Income

- Bonds still well bid, but off new m-t-d highs

- Bunds hold comfortably above 132.00 within 132.72-131.95 range

- Gilts midway between 97.31-96.91 bounds and T-note a tad closer to 109-29 trough vs 110-14+ peak ahead of revised US Q3 GDP, Fed's Mester and Beige Book

- UK and German issuance less well covered after lack of concession

- UK sells GBP 4.25bln 3.5% 2025 Gilt: b/c 2.36x (prev. 2.61x), average yield 4.554% (prev. 4.964%) & tail 2.0bps (prev. 1.1bps)

- Italy sells EUR 6.5bln vs exp. EUR 5.5-6.5bln 4.10% 2029, 4.20% 2034 BTP & 0.75-1bln 2026 CCTeu: 4.10% 2029: b/c 1.45x (prev. 1.45x) & gross yield 3.61% (prev. 4.12%). 4.20% 2034: b/c 1.45x (prev. 1.33x) & gross yield 4.17% (prev. 4.76%). 2026 CCTeu: b/c 1.99x (prev. 2.0x) & gross yield 4.43% (prev. 4.12%)

- Germany sells EUR 2.82bln vs exp. EUR 3.5bln 2.60% 2033: b/c 1.74x (prev. 2.55x), average yield 2.45% (prev. 2.64%) & retention 19.4% (prev. 17.40%)

Commodities

- WTI and Brent, +1.3%, extend gains with the complex initially boosted by the recent weaker Dollar, and as the clock ticks down to the OPEC+ meeting tomorrow; though, the USD has since bounced but crude remains underpinned nonetheless.

- Spot gold briefly topped USD 2050/oz overnight to levels last seen in May, whilst base metals are flat/mixed taking a breather from yesterday’s Dollar-induced gains as the index lifts back towards 103.00.

- Strike at Las Bambas copper mine in Peru is limited to 48 hours after the labour authority declared the protest inappropriate.

- First Quantum (FM CA) said the Cobre Panama Mine suspended commercial production and is applying a programme of preservation and safe maintenance after the recent court ruling that its contract was unconstitutional.

- OPEC+ talks are ongoing continuing no fresh delays currently expected to tomorrow's meeting, according to Reuters sources

Geopolitics: Israel-Hamas

- Israeli negotiators are offering Hamas a further three days of ceasefire through to Sunday morning if the group releases all the remaining women and children they believe it is holding, according to sources close to talks in Qatar cited by The Times.

- G7 Foreign Ministers' joint statement on Israel and Gaza stated that they welcome the release of hostages and the pause in hostilities, while they support a further extension of the pause and future pauses as needed.

- White House's Kirby said they hope to see more Americans released by Hamas and will work to see if they can extend the pause.

- US paused drone flights over Gaza as part of the truce between Israel and Hamas, according to a Pentagon spokesperson.

- Source close to Hamas says group willing to extend truce by four more days, according to AFP.

- "Israeli vehicles fire their weapons at different areas northwest of Gaza City", according to Al Arabiya.

Geopolitics: NATO

- US State Department senior official said Turkey’s Foreign Minister told NATO he is working on the ratification of Sweden and gave the likely timeline of a 'few weeks'.

- Swedish Foreign Minister says Turkey's Foreign Minister said that ratification for Sweden's accession to NATO could occur within weeks

US Event Calendar

- 07:00: Nov. MBA Mortgage Applications, prior 3.0%

- 08:30: 3Q Core PCE Price Index QoQ, est. 2.4%, prior 2.4%

- 08:30: 3Q GDP Price Index, est. 3.5%, prior 3.5%

- 08:30: 3Q Personal Consumption, est. 4.0%, prior 4.0%

- 08:30: Oct. Retail Inventories MoM, est. 0.6%, prior 0.9%

- 08:30: Oct. Advance Goods Trade Balance, est. -$86.5b, prior -$85.8b, revised -$86.8b

- 08:30: Oct. Wholesale Inventories MoM, est. 0.2%, prior 0.2%

- 08:30: 3Q GDP Annualized QoQ, est. 5.0%, prior 4.9%

- 14:00: Federal Reserve Releases Beige Book

Central Bank speakers

- 13:45: Fed’s Mester Speaks on Financial Stability

DB's Jim Reid concludes the overnight wrap

As I fly over what are snowy Alpine peaks at the moment, the main highlight over the last 24 hours has been a further dovish pivot for rates with central bank speakers really impacting the market with 2yr Treasury yields leading the charge and down -11.8bps to a 4 month low and down another -4bps overnight. The next hurdles for markets are today's German CPI and the second reading of US Q3 GDP.

The main catalyst for this bond rally were comments from generally hawkish Fed Governor Waller, who said that he was “increasingly confident that policy is currently well positioned to slow the economy and get inflation back to 2%”. His off the cuff Q&A responses even suggested cuts were potentially possible in H1 if inflation behave as he thinks it could. So surprisinginly explicit. That was taken as another sign that the Fed were done hiking rates, and investors moved to price in a noticeably more dovish path for rates over the year ahead. For instance, the chance of a rate cut as soon as the March meeting rose from 16% to 35%, and the chance of a cut by May was up from 58% to 86%. And if you look at 2024 as a whole, the amount of cuts priced in was up from 89bps to 103bps following those comments. A reminder from our World Outlook that we expect 175bps of rate cuts in 2024 and a big rally down to 3.15% for 2 year yields. But this is more on the recession view rather than a soft landing one that markets are pricing.

To be fair, there were some hawkish lines from the Fed as well yesterday, it’s just that markets were focused on the dovish interpretation. One example came from Fed Governor Bowman, who said that her baseline outlook “continues to expect that we will need to increase the federal funds rate further”. However later New York Fed President Williams struck a more dovish tone again, saying that “encouragingly, the inflation trajectory has turned. ” This is the final week they can speak before the blackout period before the December meeting starts. We’ll get some further Fed speakers later in the week, including Chair Powell on Friday.

As discussed at the top, the prospect of near-term rate cuts was great news for sovereign bonds, which rallied on both sides of the Atlantic. For example, US Treasuries saw a significant decline in yields across the curve, with the 2yr yield (-11.8bps) down to its lowest level since mid-July, before the big surge in yields over the summer. Similarly, the 10yr Treasury yield fell -6.6bps, taking it down to its lowest level since September at 4.32%. Yields across the curve have rallied further overnight by around -4bps. Bear in mind that it was only on October 23 that the 10yr yield moved above 5% on an intraday basis, so we’ve seen a sharp move lower in that time, to an extent we haven’t seen since the turmoil following SVB’s collapse in March.

$39bn 7-year bonds were issued yesterday, which is the third and last Treasury auction this week. It was a relatively weak auction with both direct and indirect bidders taking less of the auction than average over the last year with the largest primary dealer takedown since last November. 7yr yields were down nearly -7.8bps around noon local time before the poor auction saw yields rise 4bps before retracing its move by the close to finish down -9.1bps overall at 4.339% and further overnight as discussed above.

All those moves had significant implications across other asset classes too. In FX, growing anticipation about a Fed rate cut meant the dollar index (-0.44%) weakened for a third consecutive day, and the Euro surpassed $1.10 for the first time since August intraday before closing at $1.099. Meanwhile, gold (+1.33%) posted another very strong performance, hitting a new 6-month high. And in Europe there was a similar decline in sovereign bond yields, with those on 10yr bunds (-5.1bps), OATs (-4.5bps) and BTPs (-3.0bps) all moving lower .

Equities opened lower, rallied with the Fed speak and trading around unchanged through the US afternoon before the S&P 500 ended the day marginally (+0.10%) higher. That's up +8.61% in November, so barring a last minute slump over today and tomorrow, it’s firmly on track to be the best month for the S&P of 2023 so far. The S&P was led yesterday by autos (+3.9%), software (+0.7%), whilst healthcare (-0.5%) and Financials (-0.3%) lagged. With autos and software outperforming, the NASDAQ rose +0.29%. Europe was an underperformer however, with the STOXX 600 down -0.30% .

Asian equity markets are mixed this morning with the Hang Seng (-2.3%) leading losses and looking set for the lowest close in a year and continuing to buck the trend of the rest of the world. China risk is also weak on the mainland with the CSI (-0.67%) and the Shanghai Composite (-0.27%) also lower. Elsewhere, the KOSPI (+0.04%) and the Nikkei (+0.09%) are swinging between gains and losses this morning. S&P 500 (+0.15%) and NASDAQ 100 (+0.16%) futures are moving slightly higher.

Early morning data showed that the Australia’s inflation rate slowed more than expected, coming in at +4.9% y/y in Oct (v/s +5.2% expected) as against an increase of +5.6% recorded in the prior month. With the inflation data undershooting market expectations, it likely reduces the possibility of another rate hike by the Reserve Bank of Australia (RBA) when it meets next Tuesday for its final meeting of the year on interest rates. Our economists still think they'll hike though.

When it came to yesterday’s data, the US releases were pretty mixed, even though markets were anticipating a growing chance of rate cuts. On the bright side, the Conference Board’s consumer confidence indicator for November rose to 102.0 (vs. 101.0 expected), which was up from a revised 99.1 in October. That ended a run of three consecutive monthly declines, and the expectations measure also rose to 77.8. However, there were also some weaker numbers on the labour market, and the proportion saying that jobs were hard to get rose to 15.4%, which is the highest it’s been since March 2021, and adds to the recent indicators suggesting a weakening labour market. Otherwise, the Richmond Fed’s manufacturing index fell to a three-month low of -5 (vs. 1 expected).

To the day ahead now, and data releases include the preliminary German CPI reading for November, UK mortgage approvals for October, and in the US there’s the second estimate of Q3’s GDP. From central banks, we’ll hear from BoE Governor Bailey, Cleveland Fed President Mester, and the Fed will be releasing their Beige Book.

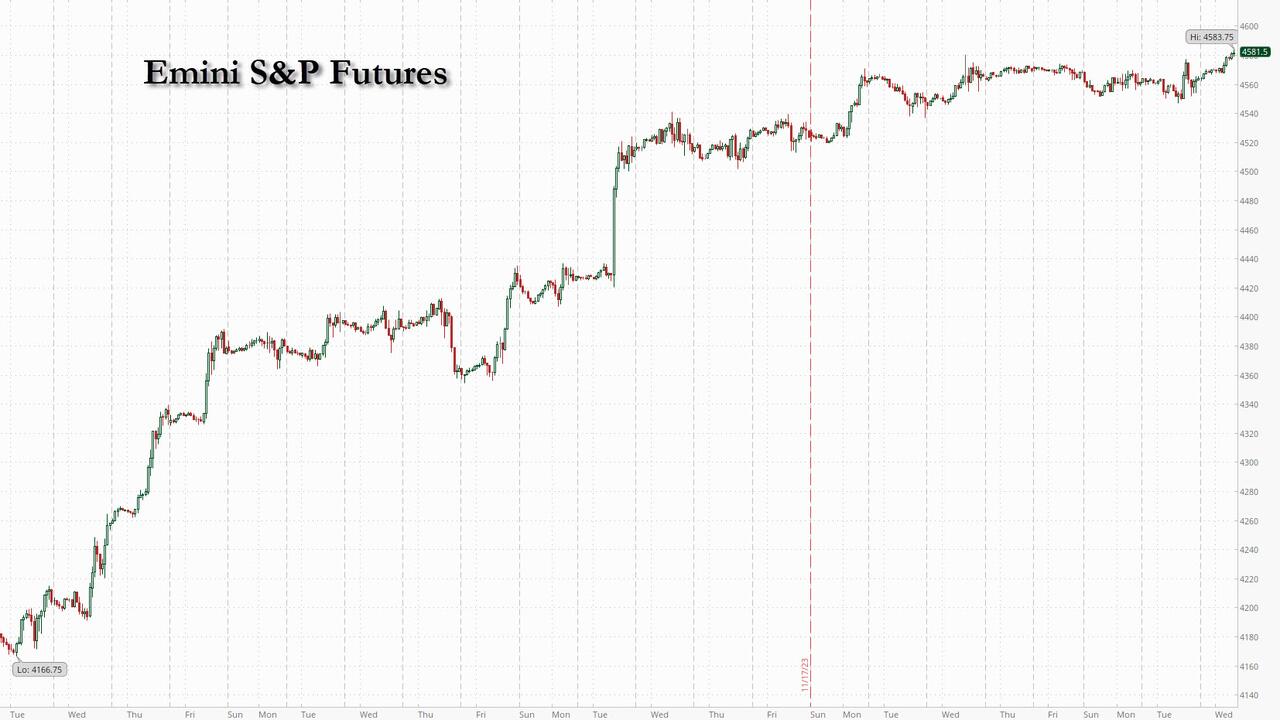

US equity futures, global markets and Treasuries extended their recent rallyall boosted by expectations that the Federal Reserve is not only done with hjking but will soon pivot and start cut rates early next year; in fact, according to Bill Ackman who has again flipflopped, the Fed will cut as soon as March (i.e., he is now long the same bonds he was so passionately shorting just a few months ago). This occurs as consumer confidence moved higher with holiday, retail sales numbers that illustrate a still strong consumer. As of 7:45am, US equity futures are up 0.4%, rising to the highest since Sept 1 and just shy of 2023 highs, while Nasdaq futures gained 0.6%; gold traded near record high, the dollar slide halted but is certainly not over, WTI oil futures rose 1.7% on the day, adding to Tuesday’s advance, while bitcoin traded just above $38K. The big question now is whether this rally can extend into December; the answer may be predicated on fundamentals rather than positioning/technicals. BBG reporting an uptick in corporate insider buying alongside stronger buyback activity. Today’s macro data focus includes 23Q3 GDP/Consumption/PCE, Beige Book, inventories, trade balance, and mtge applications.

In premarket trading, tech and small-caps are outperforming; megacap teach names are higher having added almost 14% MTD. General Motors jumped almost 6% in US premarket trading after announcing it will boost its dividend by 33% and implement a $10 billion share buyback program. Las Vegas Sands shares fell 5.6% as Miriam Adelson is selling $2 billion of stock in the casino company so the family can acquire a majority stake in the Dallas Mavericks NBA franchise from Mark Cuban. GameStop shares jump 12%, putting the stock on track to extend gains for a second consecutive session, ahead of its third-quarter results next week. Here are some other notable premarket movers:

- Airbnb shares slip 0.8% after Jefferies cut its recommendation on the short-term rental platform’s stock to hold from buy, citing a recent slowdown in bookings.

- CrowdStrike Holdings shares edged higher, rising 3.0%, after the security software company reported third-quarter results that beat expectations and raised its full-year revenue forecast.

- Fluence Energy shares jump 19% after the energy storage company’s results beat expectations, with analysts positive on its orders and prospects for 2024, especially against investors’ more sombre view on the renewables sector.

- NetApp shares jump 12% after the data storage company boosted its full-year adjusted earnings per share forecast above analyst expectations. Additionally, the company also reported second-quarter revenue that beat estimates. Analysts highlighted the traction in new products as well as strength in all-flash solutions.

- Okta shares fell 6.2% after the applications software company said it has found that hackers who had breached its network stole information on all users of its customer support system.

- Workday shares rise 8.92% after the application software company reported third-quarter results that beat expectations and raised its full-year forecast for subscription revenue.

- Foot Locker Inc surged as much as 13% after comparable sales beat the average analyst estimate.

The November stock party continues and the MSCI All Country World Index of stocks has gained 8.7% so far this month, the most since November 2020 amid a collapsing dollar (which however today paused a four-day retreat). It’s not just stocks that are soaring: in the latest rerun of the QE trade, bonds are climbing at the fastest monthly pace since 2008 as inflation continues to slow and Fed officials strike a dovish tone.

The latest leg higher for stocks and bonds came after the otherwise hawkish Fed Governor Christopher Waller suggested the central bank is well positioned to push inflation to a 2% target. And then overnight, Bill Ackman said he’s betting Fed cuts could come as soon as the first quarter, something we first said two weeks ago.

It takes 8 months on average from the last rate hike to the first rate cut. So March https://t.co/J9IULydqcA pic.twitter.com/SXFwn95DEA

— zerohedge (@zerohedge) November 14, 2023

“The market is hanging on to everything Fed speakers say,” said Justin Onuekwusi, chief investment officer at UK wealth manager St James Place. “It was only the end of October when we were talking of 5% yields on US Treasuries. It does feel like the market is being a bit complacent.”

Now, traders are looking ahead to data on Thursday that include the Fed’s preferred measure of underlying inflation, the core PCE, as well as a speech by Fed Chair Jerome Powell at the end of the week that could offer clues on potential policy easing. “I would expect some pushback on market rate expectations,” said Marc Ostwald, chief economist & global strategist at ADM Investor Services Int. Ltd. “Inflation will have to drop sharply in the coming months, and the labor market will need to loosen a lot more to justify a rate cut in the first half of 2024.”

European stocks are in the green after posting back-to-back losses for the first time in three weeks. The Stoxx 600 is up 0.6%, led by gains in real estate, auto and technology shares. The autos and real estate sectors are the best performers, with many property shares getting a boost from a renewed decline in yields. The energy and insurance sectors are the worst performers. Philips slumps on a new apnea machine safety issue. Here are some of the biggest movers on Wednesday:

- Vestas shares rise as much as 4% after Berenberg lifts recommendation on Danish wind turbine producer to buy from hold, citing rising momentum in margins over the last two quarters.

- BMW shares rise as much as 3.6%, with JPMorgan lauding a well balanced growth strategy at the German automaker and upgrading it to overweight from neutral.

- Musti shares gain as much as 29%, the most since the pet care firm went public in 2020, after the company’s board recommended a voluntary public cash tender offer from a group of investors that values the outstanding equity at €868m.

- Harbour Energy shares rise as much as 5.1% and is among leading gainers on the Stoxx 600 energy index on Wednesday, after delivering a nine-month update that analysts describe as solid.

- Ferrovial shares gain as much as 3.2% after Spanish construction firm agreed to sell its stake in the parent company of Heathrow Airport to Ardian and Saudi Arabia’s Public Investment Fund for a total of $3 billion.

- Saipem shares gain as much as 3% after the engineering company got two offshore contracts in Guyana and Brazil worth approximately $1.9b.

- Philips falls as much as 7.7% after the Food and Drug Administration warned about a new safety issue involving the company’s DreamStation 2 machines used to treat obstructive sleep apnea.

- Halfords shares slide as much as 23%, the biggest intraday decline since Jan. 12, after the motoring and cycling products retailer reported interim results. RBC Capital Markets said pretax profit was below their expectations due to a softer showing in the company’s retail business, while Peel Hunt noted that the wider market was “not playing ball.”

- Aroundtown shares slump as much as 11%, its second slump this month, after third quarter results showed deleveraging remains a major issue at the German real estate firm, according to Morgan Stanley.

- Kindred shares fall as much as 9.7%, the most since January, after the Stockholm-listed online gambling operator reported third-quarter earnings weighed down by poor margins in its sports betting segment. The outcome of a strategic review is, however, seen as positive due to cost savings.

The MSCI Asia Pacific gauge fell 0.3% erasing earlier gains, even as the US 10-year yield dropped below the closely watched 100-day average, as gains in Australia were tempered by heavy losses in Chinese technology shares. Meituan was the biggest drag on the regional gauge after the Chinese firm warned that growth in its main meal delivery business would slow this quarter. A measure of technology stocks in Hong Kong also dropped to its lowest level in two weeks.

- Hang Seng and Shanghai Comp declined with underperformance in Hong Kong after the recent rises in domestic money market rates and with the PBoC’s open market operations resulting in a net daily drain.

- Nikkei 225 swung between gains and losses with early pressure from a firmer currency before the index rebounded off lows, while there were also comments from BoJ Adachi who stuck to the dovish script as he noted it is appropriate to patiently maintain easy policy and if needed, the BoJ will take additional easing steps.

- Australian stocks climbed after inflation cooled more-than-expected in October, bolstering the case for the Reserve Bank to resume pausing interest rates next week. New Zealand stocks also rose after its central bank kept rates unchanged.

- Indian stocks rallied, with the NSE Nifty 50 Index reclaiming the psychological 20,000 mark for the first time since dropping below it in September. The S&P BSE Sensex rose 1.1% to 66,901.91 at the 3:30 p.m. close in Mumbai, while the Nifty finished 1% higher at 20,096.60. The Nifty has logged similar or greater gains eight times in the past year. The gauge rose further the next day on six occasions, posting an average 0.4% gain, according to data compiled by Bloomberg. Wednesday’s gains were driven by automobiles and banks, which rose over 1.5% each. The laggards were media and realty, which ended in the red.

In FX, the Bloomberg Dollar Spot Index is unchanged after falling as much 0.2% to 1228,70, its lowest since early August amid growing bets that the Federal Reserve may start cutting interest rates next year, after two hawkish Fed officials signaled they could be comfortable holding rates steady for now. The kiwi is the best performer among the G-10’s, rising 0.2% versus the greenback after a hawkish hold from the RBNZ. The Aussie lags after CPI slowed in October. Oil prices advance, with WTI rising 1.4% to trade near $77.40. Spot gold falls 0.2%.

In rates, treasuries were richer by 4bps-5bps across the curve amid bigger gains in core European rates following bullish German state CPI readings ahead of the national print at 8am New York time. Two-year Treasury yields dropped four basis points to 4.69% after shedding 15 basis points Tuesday. Fed swaps are anticipating over 100 basis points of rate cuts by the end of 2024. Meanwhile, 10-year TSY yields are around 4.28%, richer by 4bp vs Tuesday close while trailing bunds and gilts in the sector by 1.5bp and 1bp on the day; new 2-year note auctioned Monday traded as rich as 4.664%, lowest for a current issue since mid-July and approaching 200-day moving average. Swaps market looks for deeper rate cuts next year, with May contracts priced for 23bp of cuts, or 92% chance of a 25bp move. German bonds rallied for a third day, the longest stretch in a month, after regional and state inflation data showed that inflation continued to slow. German 10-year yields fall 4bps to 2.45%.

“Attention will now move to Chair Powell’s speech on Friday to see if the tone points to a clear pivot towards easing,” Daragh Maher, head of FX strategy for the US at HSBC, wrote in a research note. “If it materializes, this would clearly be a challenge to our bullish US dollar view”

In commodities, oil climbed for a second day as traders awaited a high-stakes OPEC+ meeting on supply. WTI rose 1.4% to trade near $77.40. Gold extended gains to its highest level since May, also buoyed by hopes of a Fed policy shift.

To the day ahead now, and data releases include the preliminary German CPI reading for November, UK mortgage approvals for October, and in the US there’s the second estimate of Q3’s GDP (median est. 5% vs 4.9% initial). From central banks, we’ll hear from BoE Governor Bailey, Cleveland Fed President Mester, and the Fed will be releasing their Beige Book.

Market Snapshot

- S&P 500 futures up 0.3% to 4,576.75

- STOXX Europe 600 up 0.5% to 459.11

- MXAP down 0.3% to 161.59

- MXAPJ down 0.3% to 504.05

- Nikkei down 0.3% to 33,321.22

- Topix down 0.5% to 2,364.50

- Hang Seng Index down 2.1% to 16,993.44

- Shanghai Composite down 0.6% to 3,021.69

- Sensex up 1.1% to 66,881.45

- Australia S&P/ASX 200 up 0.3% to 7,035.35

- Kospi little changed at 2,519.81

- German 10Y yield little changed at 2.47%

- Euro down 0.1% to $1.0979

- Brent Futures up 0.4% to $82.01/bbl

- Gold spot down 0.3% to $2,035.68

- U.S. Dollar Index up 0.11% to 102.86

Top Overnight News

- Jack Ma has urged Alibaba to “change and reform” as the ecommerce giant he founded tries to find a new path after abandoning parts of its ambitious restructuring plan and its main Chinese rival gains ground. FT

- Australia’s inflation cools, with the CPI rising 4.9% in Oct (down from +5.6% in Sept and below the Street’s +5.2% forecast). BBG

- Spanish inflation unexpectedly eased, retreating for the first time since June thanks to drops in the costs of fuel and tourism. Consumer prices rose 3.2% from a year earlier in November, data Wednesday showed. That compares with 3.5% the previous month and defied the median estimate in a Bloomberg survey of economists for an acceleration to 3.7%. BBG

- German regional inflation cools in Nov, including Baden Wuerttemberg +3.4% (down from +4.4% in Oct), Bavaria +2.8% (down from +3.7% in Oct), Brandenburg +4.1% (down from +4.6% in Oct), Hesse +2.9% (down from +3.6% in Oct), North Rhine Westphalia +3% (down from +3.1% in Oct), and Saxony +3.9% (down from +4.5% in Oct). BBG

- Russian President Vladimir Putin will not make peace in Ukraine before he knows the results of the November 2024 U.S. election, a senior U.S. State Department official said on Tuesday, amid concerns that a potential victory for former President Donald Trump could upend Western support for Kyiv. RTRS

- Bill Ackman is betting the Federal Reserve will begin cutting interest rates sooner than markets are predicting. The Pershing Square Capital Management founder said such a move could happen as soon as the first quarter. Traders are fully pricing in a rate cut in June, with the chance of a cut happening in May priced at about 80%, according to swaps market data. BBG

- WDAY shares rose more than 8% premarket after the cloud enterprise company raised its outlook for the year and reported higher-than-expected revenue in the third quarter. WSJ

- OpenAI’s revamped board of directors doesn’t plan to include representatives from outside investors, according to a person familiar with the situation. It’s a sign that the board will prioritize safety practices ahead of investor returns. The Information

- The head of Amazon’s cloud division has used recent turmoil at OpenAI to launch a thinly veiled attack on Microsoft, the artificial intelligence company’s biggest investor. “Things are moving so fast [in AI] and in that type of environment the ability to adapt is the most valuable capability that you can have,” Selipsky, AWS chief executive, said at its annual developer conference in Las Vegas on Tuesday. “You don’t want a cloud provider that’s beholden primarily to one model provider, you need a real choice . . . The events of the past 10 days have made that very clear.” FT

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed after the choppy performance on Wall St where stocks wavered, Treasuries rallied and the Dollar dipped on dovish Fed rhetoric, while the region also digested the RBNZ’s hawkish hold where it kept rates unchanged but signalled risks of a hike. ASX 200 was positive with the index helped by encouraging data including better-than-expected Construction Work Done which feeds into next week’s GDP release and after softer monthly CPI all but guaranteed a pause at the December RBA meeting. Nikkei 225 swung between gains and losses with early pressure from a firmer currency before the index rebounded off lows, while there were also comments from BoJ Adachi who stuck to the dovish script as he noted it is appropriate to patiently maintain easy policy and if needed, the BoJ will take additional easing steps. Hang Seng and Shanghai Comp declined with underperformance in Hong Kong after the recent rises in domestic money market rates and with the PBoC’s open market operations resulting in a net daily drain.

Top Asian News

- China’s Vice Foreign Minister recently met with the EU’s external action service deputy secretary and said that China is ready to strengthen communication and coordination with the EU side and make preparations for a China-EU summit before the end of the year. Furthermore, it was stated that the two sides need to grasp the general direction of China-EU relations, uphold mutually beneficial and win-win cooperation, as well as fully respect each other’s core interests, according to Reuters.

- Japan’s Finance Ministry will raise the assumed interest rate paid on bonds in the government’s annual budget proposal for the first time in 17 years in fiscal 2024, reflecting policy shifts by the BoJ that have allowed yields to rise, according to Nikkei.

- BoJ Board Member Adachi said Japan is yet to see a positive wage-inflation cycle become embedded enough and it is appropriate to patiently maintain easy policy. Adachi also stated that if needed, the BoJ will take additional easing steps, while he added that the steps the BoJ took in October to make YCC more flexible are not aimed at laying the groundwork for policy normalisation.

- RBNZ kept the OCR unchanged at 5.50% as expected, while it reiterated that interest rates will need to remain at a restrictive level for a sustained period of time and interest rates are restricting spending in the economy with consumer price inflation declining as is necessary to meet the committee’s remit. RBNZ said inflation remains too high and the committee remains wary of ongoing inflationary pressures, as well as noted that demand growth has eased but by less than anticipated and if inflationary pressures were to be stronger than anticipated, the OCR would likely need to increase further. Furthermore, the committee is confident the current OCR level is restricting demand but slightly raised OCR and CPI forecasts with the OCR seen at 5.63% in March 2024 (prev. 5.58%), 5.66% in December 2024 (prev. 5.50%), and 5.56% (prev. 5.36%) in March 2025, while annual CPI is seen at 2.5% by December 2024 (prev. 2.4%).

- RBNZ Governor Orr said in the press conference that they’ve been adamant on holding rates through next year and noted that the projection shows upward bias to rates but it is not a done deal. Orr also stated the risk to inflation is still more to the upside, while he is nervous that inflation has been outside the band for so long and concerned that longer-term inflation expectations are creeping up.

- REUTERS POLL: Chinese New Home Prices Growth expects at +3.0% Y/Y 2023 (vs 0% in August poll); 1.1% Y/Y in 2024 (1.0% in August poll)

European equities, Euro Stoxx 50 +0.6% are extending gains, but with clear underperformance in the FTSE100 -0.2%, albeit the UK index is off lows. European sectors have a strong positive tilt; featuring strength in Autos & Parts whilst Energy lags but with both sectors underpinned by broker moves. US Futures are trading on the front foot, NQ & ES +0.4%, with clear outperformance in the RTY +0.8% as it pares back yesterday’s losses.

Top European News

- The number of businesses set up in the UK in 2022 fell by 7% to 337k as UK business creation was hit by high borrowing costs and weaker demand, according to analysis by FT citing data released last week by the Office of National Statistics.

- Several ECB regulators are reportedly planning to push to ease bank payout stance, according to Bloomberg

- ECB’s Stournaras says ECB April cut bets seem a bit optimistic, via Politico; says the first rate cut could come in the middle of 2024. Early PEPP winddown risks hurting ECB credibility

- OECD raises 2023 US growth forecast to 2.4% (prev. 2.2%), 1.5% in 2024 (prev. 1.3%), sees 1.7% 2025; Sees Chinese growth 5.2% (prev. 5.1%), 4.7% (prev. 4.6%), 4.2% in 2025; Raises UK growth forecast to 0.5% (prev. 0.3%), trims 2024 0.7% (prev. 0.8%), 1.2% in 2025.

FX

- DXY finds underlying bids just shy of 102.50 and aims for 103.00

- Kiwi outperforms after hawkish RBNZ hold and Aussie caught in AUD/NZD cross-fire with added downside pressure from soft inflation data

- NZD/USD elevated within 0.6208-0.6134 range, AUD/USD depressed between 0.6676-20 parameters

- Euro undermined by weaker than forecast German state and Spanish CPI metrics. EUR/USD sub-1.1000, but holding near decent option expiry interest and former Fib resistance/breakout area

- Yen retreats towards 148.00 from circa 146.68 after dovish guidance from BoJ’s Adachi

- PBoC set USD/CNY mid-point at 7.1031 vs exp. 7.1340 (prev. 7.1132).

Fixed Income

- Bonds still well bid, but off new m-t-d highs

- Bunds hold comfortably above 132.00 within 132.72-131.95 range

- Gilts midway between 97.31-96.91 bounds and T-note a tad closer to 109-29 trough vs 110-14+ peak ahead of revised US Q3 GDP, Fed’s Mester and Beige Book

- UK and German issuance less well covered after lack of concession

- UK sells GBP 4.25bln 3.5% 2025 Gilt: b/c 2.36x (prev. 2.61x), average yield 4.554% (prev. 4.964%) & tail 2.0bps (prev. 1.1bps)

- Italy sells EUR 6.5bln vs exp. EUR 5.5-6.5bln 4.10% 2029, 4.20% 2034 BTP & 0.75-1bln 2026 CCTeu: 4.10% 2029: b/c 1.45x (prev. 1.45x) & gross yield 3.61% (prev. 4.12%). 4.20% 2034: b/c 1.45x (prev. 1.33x) & gross yield 4.17% (prev. 4.76%). 2026 CCTeu: b/c 1.99x (prev. 2.0x) & gross yield 4.43% (prev. 4.12%)

- Germany sells EUR 2.82bln vs exp. EUR 3.5bln 2.60% 2033: b/c 1.74x (prev. 2.55x), average yield 2.45% (prev. 2.64%) & retention 19.4% (prev. 17.40%)

Commodities

- WTI and Brent, +1.3%, extend gains with the complex initially boosted by the recent weaker Dollar, and as the clock ticks down to the OPEC+ meeting tomorrow; though, the USD has since bounced but crude remains underpinned nonetheless.

- Spot gold briefly topped USD 2050/oz overnight to levels last seen in May, whilst base metals are flat/mixed taking a breather from yesterday’s Dollar-induced gains as the index lifts back towards 103.00.

- Strike at Las Bambas copper mine in Peru is limited to 48 hours after the labour authority declared the protest inappropriate.

- First Quantum (FM CA) said the Cobre Panama Mine suspended commercial production and is applying a programme of preservation and safe maintenance after the recent court ruling that its contract was unconstitutional.

- OPEC+ talks are ongoing continuing no fresh delays currently expected to tomorrow’s meeting, according to Reuters sources

Geopolitics: Israel-Hamas

- Israeli negotiators are offering Hamas a further three days of ceasefire through to Sunday morning if the group releases all the remaining women and children they believe it is holding, according to sources close to talks in Qatar cited by The Times.

- G7 Foreign Ministers’ joint statement on Israel and Gaza stated that they welcome the release of hostages and the pause in hostilities, while they support a further extension of the pause and future pauses as needed.

- White House’s Kirby said they hope to see more Americans released by Hamas and will work to see if they can extend the pause.

- US paused drone flights over Gaza as part of the truce between Israel and Hamas, according to a Pentagon spokesperson.

- Source close to Hamas says group willing to extend truce by four more days, according to AFP.

- “Israeli vehicles fire their weapons at different areas northwest of Gaza City”, according to Al Arabiya.

Geopolitics: NATO

- US State Department senior official said Turkey’s Foreign Minister told NATO he is working on the ratification of Sweden and gave the likely timeline of a ‘few weeks’.

- Swedish Foreign Minister says Turkey’s Foreign Minister said that ratification for Sweden’s accession to NATO could occur within weeks

US Event Calendar

- 07:00: Nov. MBA Mortgage Applications, prior 3.0%

- 08:30: 3Q Core PCE Price Index QoQ, est. 2.4%, prior 2.4%

- 08:30: 3Q GDP Price Index, est. 3.5%, prior 3.5%

- 08:30: 3Q Personal Consumption, est. 4.0%, prior 4.0%

- 08:30: Oct. Retail Inventories MoM, est. 0.6%, prior 0.9%

- 08:30: Oct. Advance Goods Trade Balance, est. -$86.5b, prior -$85.8b, revised -$86.8b

- 08:30: Oct. Wholesale Inventories MoM, est. 0.2%, prior 0.2%

- 08:30: 3Q GDP Annualized QoQ, est. 5.0%, prior 4.9%

- 14:00: Federal Reserve Releases Beige Book

Central Bank speakers

- 13:45: Fed’s Mester Speaks on Financial Stability

DB’s Jim Reid concludes the overnight wrap

As I fly over what are snowy Alpine peaks at the moment, the main highlight over the last 24 hours has been a further dovish pivot for rates with central bank speakers really impacting the market with 2yr Treasury yields leading the charge and down -11.8bps to a 4 month low and down another -4bps overnight. The next hurdles for markets are today’s German CPI and the second reading of US Q3 GDP.

The main catalyst for this bond rally were comments from generally hawkish Fed Governor Waller, who said that he was “increasingly confident that policy is currently well positioned to slow the economy and get inflation back to 2%”. His off the cuff Q&A responses even suggested cuts were potentially possible in H1 if inflation behave as he thinks it could. So surprisinginly explicit. That was taken as another sign that the Fed were done hiking rates, and investors moved to price in a noticeably more dovish path for rates over the year ahead. For instance, the chance of a rate cut as soon as the March meeting rose from 16% to 35%, and the chance of a cut by May was up from 58% to 86%. And if you look at 2024 as a whole, the amount of cuts priced in was up from 89bps to 103bps following those comments. A reminder from our World Outlook that we expect 175bps of rate cuts in 2024 and a big rally down to 3.15% for 2 year yields. But this is more on the recession view rather than a soft landing one that markets are pricing.

To be fair, there were some hawkish lines from the Fed as well yesterday, it’s just that markets were focused on the dovish interpretation. One example came from Fed Governor Bowman, who said that her baseline outlook “continues to expect that we will need to increase the federal funds rate further”. However later New York Fed President Williams struck a more dovish tone again, saying that “encouragingly, the inflation trajectory has turned. ” This is the final week they can speak before the blackout period before the December meeting starts. We’ll get some further Fed speakers later in the week, including Chair Powell on Friday.

As discussed at the top, the prospect of near-term rate cuts was great news for sovereign bonds, which rallied on both sides of the Atlantic. For example, US Treasuries saw a significant decline in yields across the curve, with the 2yr yield (-11.8bps) down to its lowest level since mid-July, before the big surge in yields over the summer. Similarly, the 10yr Treasury yield fell -6.6bps, taking it down to its lowest level since September at 4.32%. Yields across the curve have rallied further overnight by around -4bps. Bear in mind that it was only on October 23 that the 10yr yield moved above 5% on an intraday basis, so we’ve seen a sharp move lower in that time, to an extent we haven’t seen since the turmoil following SVB’s collapse in March.

$39bn 7-year bonds were issued yesterday, which is the third and last Treasury auction this week. It was a relatively weak auction with both direct and indirect bidders taking less of the auction than average over the last year with the largest primary dealer takedown since last November. 7yr yields were down nearly -7.8bps around noon local time before the poor auction saw yields rise 4bps before retracing its move by the close to finish down -9.1bps overall at 4.339% and further overnight as discussed above.

All those moves had significant implications across other asset classes too. In FX, growing anticipation about a Fed rate cut meant the dollar index (-0.44%) weakened for a third consecutive day, and the Euro surpassed $1.10 for the first time since August intraday before closing at $1.099. Meanwhile, gold (+1.33%) posted another very strong performance, hitting a new 6-month high. And in Europe there was a similar decline in sovereign bond yields, with those on 10yr bunds (-5.1bps), OATs (-4.5bps) and BTPs (-3.0bps) all moving lower .

Equities opened lower, rallied with the Fed speak and trading around unchanged through the US afternoon before the S&P 500 ended the day marginally (+0.10%) higher. That’s up +8.61% in November, so barring a last minute slump over today and tomorrow, it’s firmly on track to be the best month for the S&P of 2023 so far. The S&P was led yesterday by autos (+3.9%), software (+0.7%), whilst healthcare (-0.5%) and Financials (-0.3%) lagged. With autos and software outperforming, the NASDAQ rose +0.29%. Europe was an underperformer however, with the STOXX 600 down -0.30% .

Asian equity markets are mixed this morning with the Hang Seng (-2.3%) leading losses and looking set for the lowest close in a year and continuing to buck the trend of the rest of the world. China risk is also weak on the mainland with the CSI (-0.67%) and the Shanghai Composite (-0.27%) also lower. Elsewhere, the KOSPI (+0.04%) and the Nikkei (+0.09%) are swinging between gains and losses this morning. S&P 500 (+0.15%) and NASDAQ 100 (+0.16%) futures are moving slightly higher.

Early morning data showed that the Australia’s inflation rate slowed more than expected, coming in at +4.9% y/y in Oct (v/s +5.2% expected) as against an increase of +5.6% recorded in the prior month. With the inflation data undershooting market expectations, it likely reduces the possibility of another rate hike by the Reserve Bank of Australia (RBA) when it meets next Tuesday for its final meeting of the year on interest rates. Our economists still think they’ll hike though.

When it came to yesterday’s data, the US releases were pretty mixed, even though markets were anticipating a growing chance of rate cuts. On the bright side, the Conference Board’s consumer confidence indicator for November rose to 102.0 (vs. 101.0 expected), which was up from a revised 99.1 in October. That ended a run of three consecutive monthly declines, and the expectations measure also rose to 77.8. However, there were also some weaker numbers on the labour market, and the proportion saying that jobs were hard to get rose to 15.4%, which is the highest it’s been since March 2021, and adds to the recent indicators suggesting a weakening labour market. Otherwise, the Richmond Fed’s manufacturing index fell to a three-month low of -5 (vs. 1 expected).

To the day ahead now, and data releases include the preliminary German CPI reading for November, UK mortgage approvals for October, and in the US there’s the second estimate of Q3’s GDP. From central banks, we’ll hear from BoE Governor Bailey, Cleveland Fed President Mester, and the Fed will be releasing their Beige Book.

Loading…