By Ye Xie, Bloomberg markets live reporter and strategist

China’s stock rally has lost a bit of momentum. But Goldman Sachs, one of the most vocal bulls, says the pullback creates buying opportunities.

The CSI 300 benchmark has retreated about 3% since reaching a seven-month high on May 20, while Hong Kong’s Hang Seng Index has declined about 4%.

It seems the Chinese market is running out of good news. While Beijing announced its most forceful attempt yet to rescue the nation’s beleaguered property market, the funding support has so far been deemed insufficient. The earnings season didn’t provide anything to suggest a robust profit recovery is underway. And the US government’s new tariffs on Chinese imports didn’t help sentiment either.

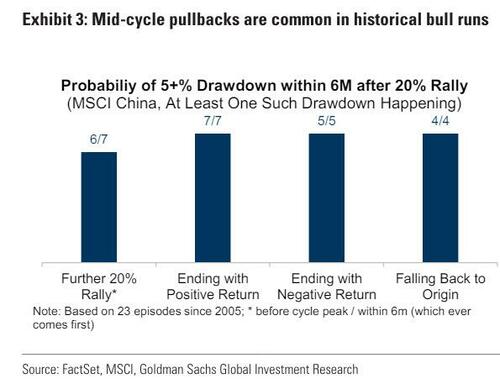

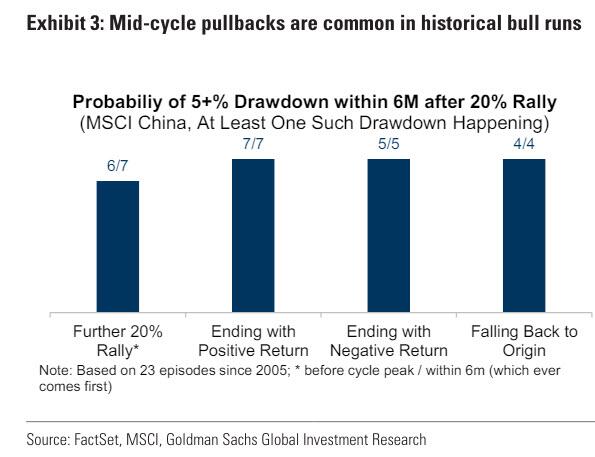

For Goldman Sachs strategists, the retreat isn’t particularly surprising after double-digit gains since February’s lows. They pointed out that the MSCI China Index almost inevitably declines at least 5% in about 20 trading days after reaching a technical bull market, which is defined as a 20% rally from the bottom.

It occurred in 22 out of 23 such episodes over the past two decades. But in about half of those cases, the market resumed the rally, gaining an additional 31% on average over the following three months, according to strategist Kinger Lau and his colleagues.

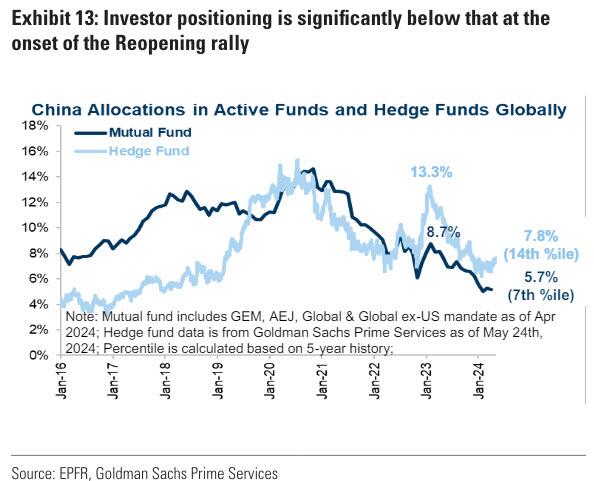

What’s more, the strategists said investors’ positioning in China’s equity market remains near historical lows, leaving room for them to add holdings.

In addition, while the government’s latest move to support the housing market isn’t forceful, it nonetheless signaled that that the prolonged property sector weakness has likely breached policymakers’ pain threshold, the strategists wrote. They summarized their market view as such:

The pullback hasn’t changed our core views/thesis on China equity, if anything, it provides a better entry point for investors to capitalize China’s rising portfolio value (i.e. diversification benefits), downside policy put underwritten by the government, and upside optionality on capital market reforms.

By Ye Xie, Bloomberg markets live reporter and strategist

China’s stock rally has lost a bit of momentum. But Goldman Sachs, one of the most vocal bulls, says the pullback creates buying opportunities.

The CSI 300 benchmark has retreated about 3% since reaching a seven-month high on May 20, while Hong Kong’s Hang Seng Index has declined about 4%.

It seems the Chinese market is running out of good news. While Beijing announced its most forceful attempt yet to rescue the nation’s beleaguered property market, the funding support has so far been deemed insufficient. The earnings season didn’t provide anything to suggest a robust profit recovery is underway. And the US government’s new tariffs on Chinese imports didn’t help sentiment either.

For Goldman Sachs strategists, the retreat isn’t particularly surprising after double-digit gains since February’s lows. They pointed out that the MSCI China Index almost inevitably declines at least 5% in about 20 trading days after reaching a technical bull market, which is defined as a 20% rally from the bottom.

It occurred in 22 out of 23 such episodes over the past two decades. But in about half of those cases, the market resumed the rally, gaining an additional 31% on average over the following three months, according to strategist Kinger Lau and his colleagues.

What’s more, the strategists said investors’ positioning in China’s equity market remains near historical lows, leaving room for them to add holdings.

In addition, while the government’s latest move to support the housing market isn’t forceful, it nonetheless signaled that that the prolonged property sector weakness has likely breached policymakers’ pain threshold, the strategists wrote. They summarized their market view as such:

The pullback hasn’t changed our core views/thesis on China equity, if anything, it provides a better entry point for investors to capitalize China’s rising portfolio value (i.e. diversification benefits), downside policy put underwritten by the government, and upside optionality on capital market reforms.

Loading…