By Garfield Reynolds, Bloomberg markets live reporter and strategist

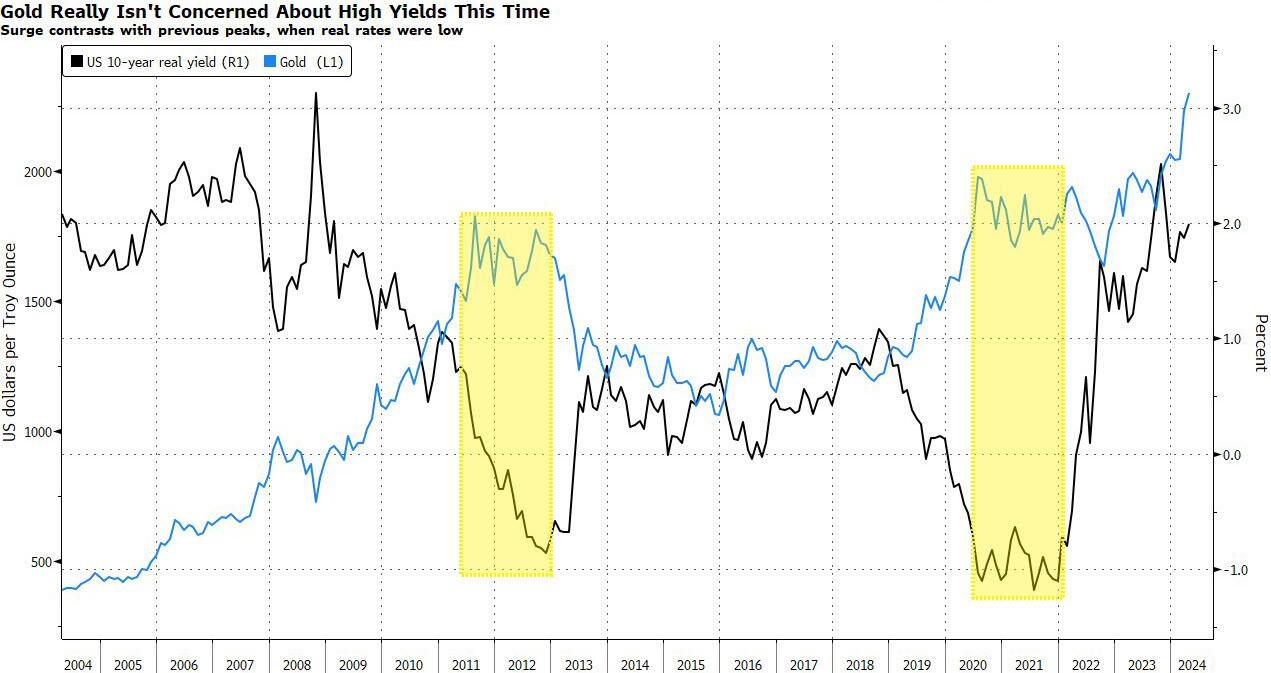

Gold’s surge to record highs is extraordinary — coming as it does in the face of elevated real yields that would normally bring it crashing down. That signals the metal is likely to rapidly reverse this year’s climb, unless risk assets collapse because of an economic or financial crisis.

The 10-year real yield is still around 2%, a level unseen since 2009. That should hurt a non-interest-bearing asset like gold, but it isn’t. The previous two times before the current surge when gold hit record highs were times of negative real yields — during the pandemic and in 2011-12 as Europe’s sovereign debt woes followed on the heels of the global financial crisis.

Back before the introduction of TIPS allowed the ready tracking of market expectations for real rates, the precious metal’s ascent to a record in 1980 came when 10-year nominal yields were well below the inflation rate.

That makes gold’s rally this year vulnerable, though it may also signal investors are becoming worried that major turmoil is coming. The surge that peaked in 2011 blew past gold’s 1980 high at the start of 2008, well before the collapse of Lehman Brothers.

It’s possible the real boon for the yellow metal is negative sentiment, rather than negative real yields.

By Garfield Reynolds, Bloomberg markets live reporter and strategist

Gold’s surge to record highs is extraordinary – coming as it does in the face of elevated real yields that would normally bring it crashing down.

That signals the metal is likely to rapidly reverse this year’s climb, unless risk assets collapse because of an economic or financial crisis.

The 10-year real yield is still around 2%, a level unseen since 2009.

That should hurt a non-interest-bearing asset like gold, but it isn’t.

The previous two times before the current surge when gold hit record highs were times of negative real yields — during the pandemic and in 2011-12 as Europe’s sovereign debt woes followed on the heels of the global financial crisis.

Back before the introduction of TIPS allowed the ready tracking of market expectations for real rates, the precious metal’s ascent to a record in 1980 came when 10-year nominal yields were well below the inflation rate.

That makes gold’s rally this year vulnerable, though it may also signal investors are becoming worried that major turmoil is coming.

The surge that peaked in 2011 blew past gold’s 1980 high at the start of 2008, well before the collapse of Lehman Brothers.

It’s possible the real boon for the yellow metal is negative sentiment, rather than negative real yields.

Loading…