It may come as a bit of a shock to those who have been following the creeping freeze in housing transactions as the bid-ask spread grows to monstrous proportions, leading to a record crash in pending home sales...

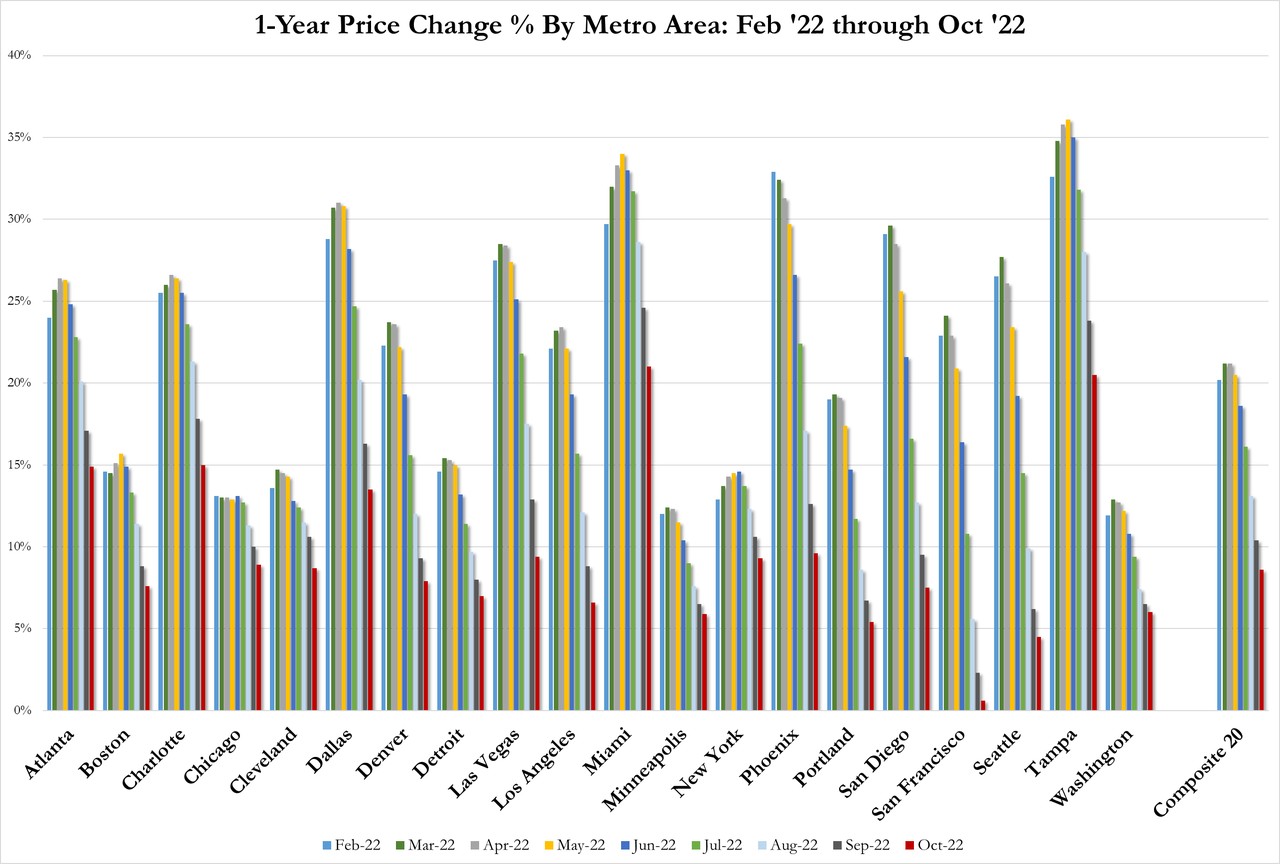

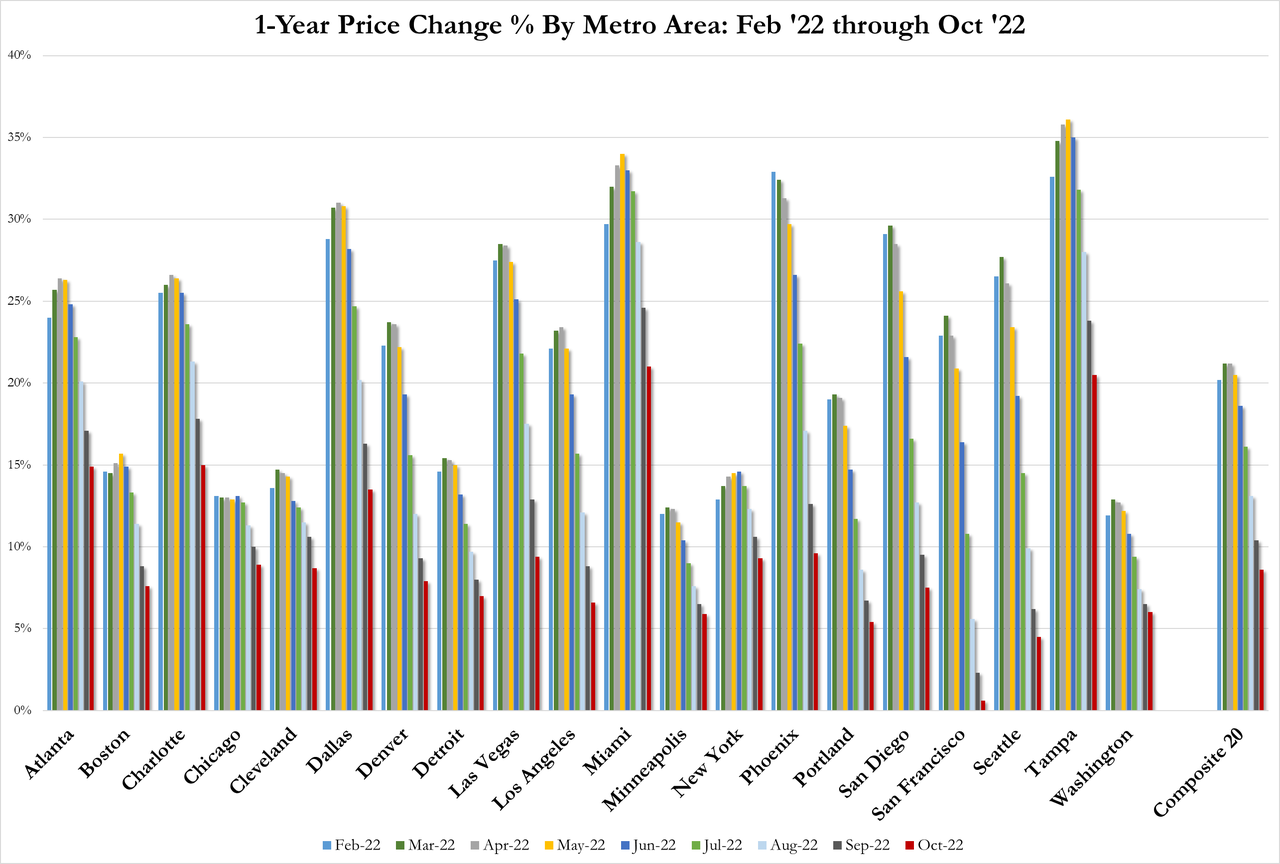

... and collapse in US home prices, especially on the West Coast...

... but even though mortgage rates ticked higher back to 6% in January, there is growing speculation that the housing market has bottomed. Why? Because as Goldman's Rich Provorotsky notes, "bet you didn’t know there were housing price futures…they bottomed in Q4 and have been rallying." Indeed, the Housing Composite Index traded on the CME is up decidedly in the past month after hitting a 16 month low in November.

Why this surprising bounce? A big reason for the unexpected rebound may be a recent report from real estate company Redfin which last Wednesday reported that "the housing market has begun to recover from a trough in the second week of November with buyers returning at a faster pace than sellers. The number of Redfin customers asking for first tours has improved by 17 percentage points from the November low, and the number of clients contacting."

Furthermore, according to the report, Redfin agents to begin the home-buying process has improved by 13 points: "I've seen more homes go under contract this month than in the entire fourth quarter," Angela Langone, a San Jose, California, agent, said in the report.

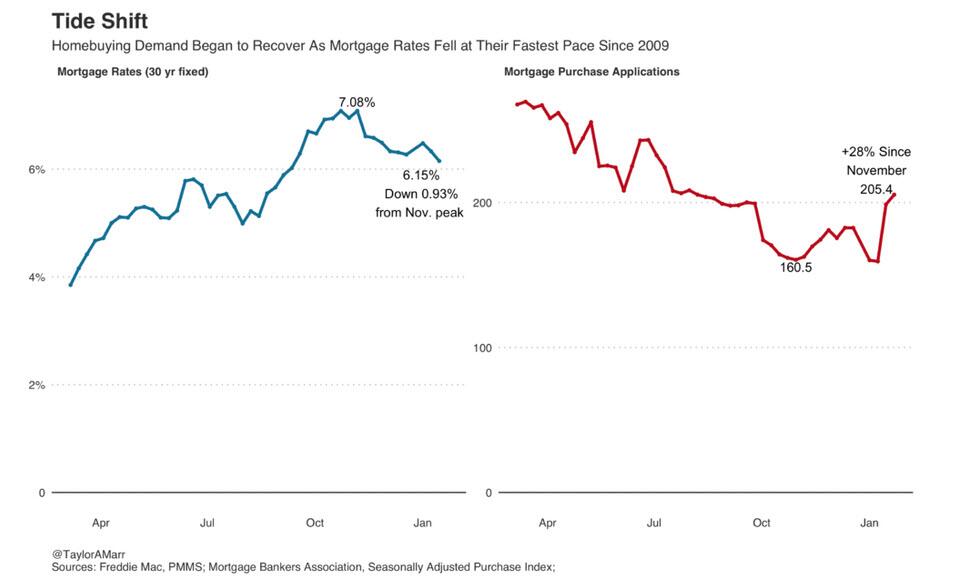

Among notable market moves, Redfin points to mortgage applications which are up 28% from early November as the average 30-year-fixed mortgage rate has dropped to 6.15% from its peak of 7.08% in November, the biggest decline since 2009. Pending home sales rose 3% in December from November.

Preliminary data on the share of Redfin agents’ offers facing bidding wars points to small upticks in the Seattle and Tampa markets this month (however, since this is an uneven trend, expect it to take some time before bidding wars nationally show an upward trend).

“Bidding wars are back in Seattle,” said local Redfin real estate agent Shoshana Godwin. “One of our Issaquah listings got 12 offers and is under contract for $155,000 over the $1.4 million list price. The buyer waived every contingency, handed over $300,000 of earnest money and is letting the seller stay for free for two months after closing. Another home in Seattle’s popular Ballard neighborhood was recently delisted after sitting on the market for over three months. The seller relisted it last week and it went pending in under a day.”

Eric Auciello, Redfin’s team manager in Tampa, has seen three modest single-family homes priced around $300,000 wind up in bidding wars in central Florida this month, with 16, 17 and 23 competing offers, respectively.

More in the full report here.

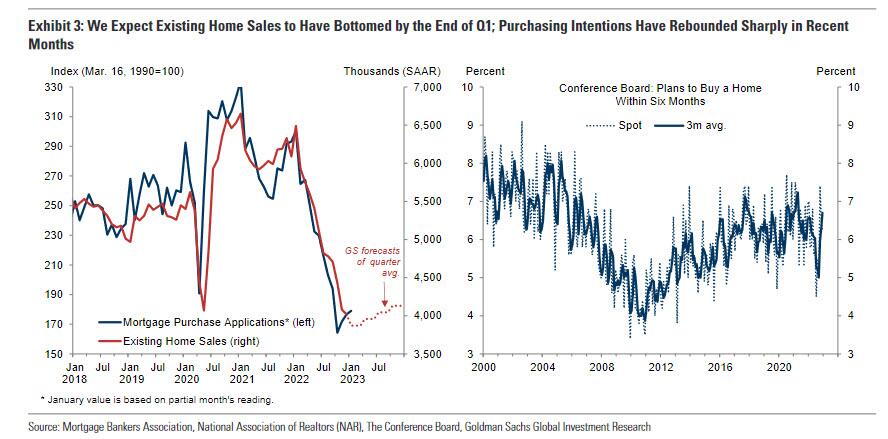

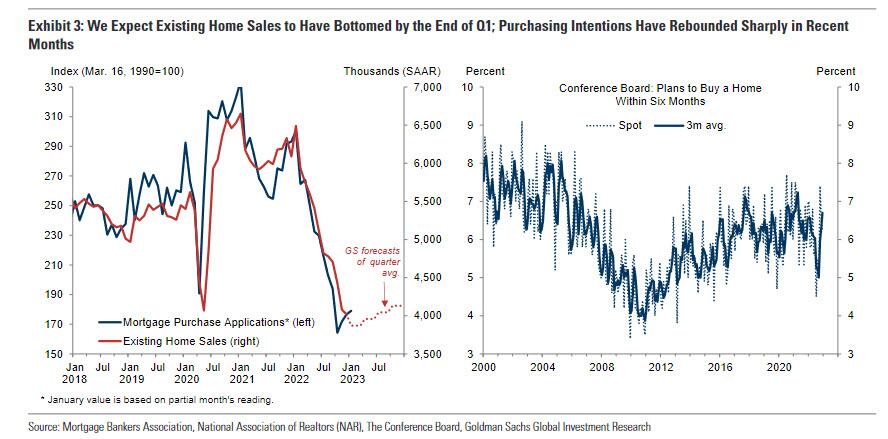

But while one can accuse Redfin of bias - after all the company recently laid off some 13% of its employees due to the housing market collapse so it is certainly interested in sparking some animal spirits in the sector - it is not alone in predicting a housing recovery. One week ago, Goldman's Jan Hatzius published the bank's Housing Outlook for 2023 in which he predicted that "home sales appear set to turn higher." That's because "mortgage purchase applications have averaged 9% above their October trough so far in January and survey-based measures of purchasing intentions have rebounded sharply" and while Goldman expects that existing home sales could decline slightly further "but will likely bottom in Q1 (GS forecast: Q1 average of 3.85mn saar vs. 4.02mn in December) before rebounding modestly by year-end (GS forecast: Q4 average of 4.1mn)."

Here are some more observations from the Goldman note (full report available to pro subs):

We forecast that housing starts will take longer to stabilize, declining to a trough pace of 1¼mn in 2023Q4 (vs. 1.4mn in 2022Q4) before recovering next year. We expect completions to total 1½mn this year, the most since 2007, which will help to clear the backlog of homes under construction and contribute to a modest increase in the homeowner vacancy rate (GS forecast of 1.2% in 2023Q4 vs. 0.9% now and 1.4% in 2019Q4).

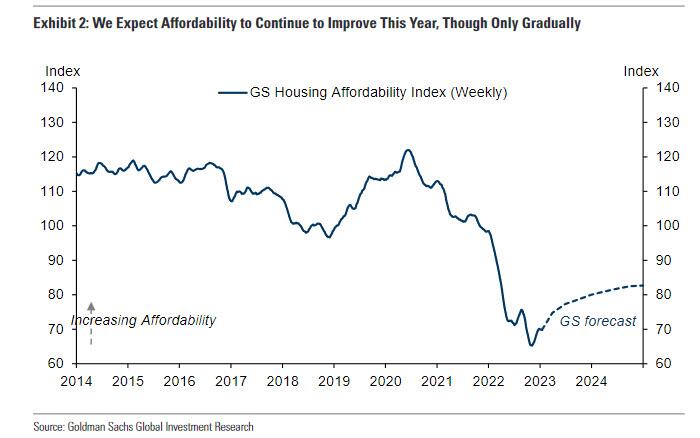

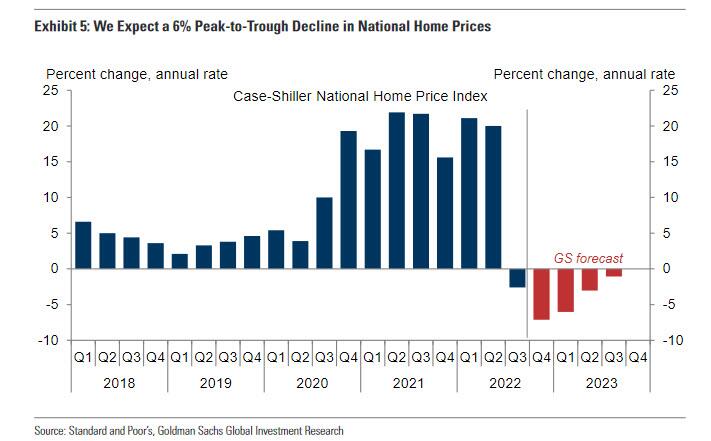

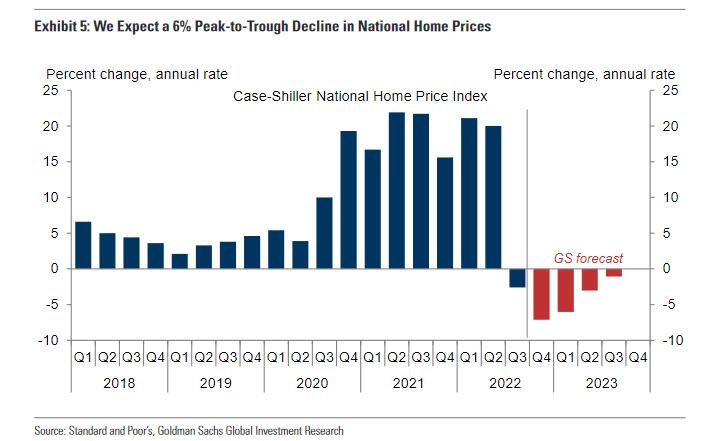

We expect a peak-to-trough decline in national home prices of roughly 6% and for prices to stop declining around mid-year.

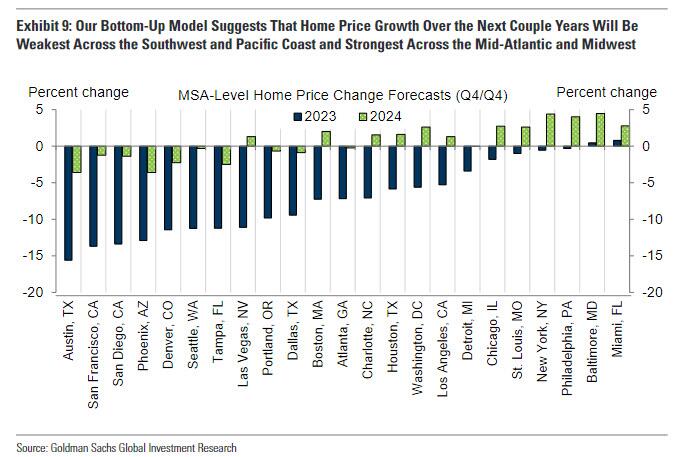

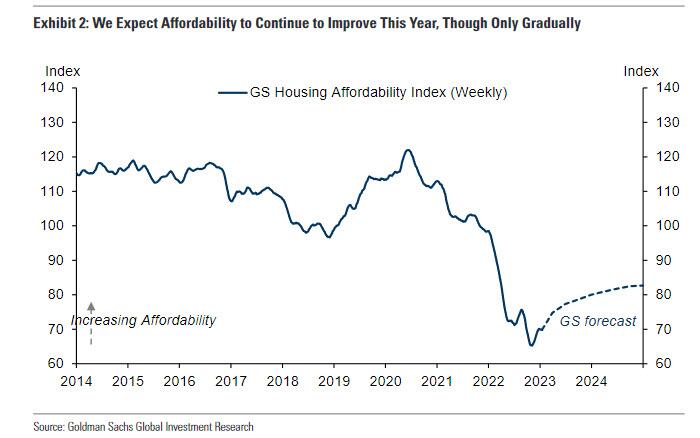

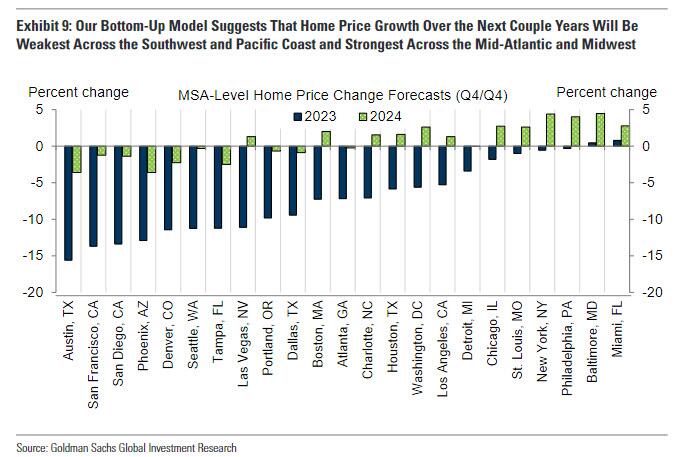

On a regional basis, we project larger declines across the Pacific Coast and Southwest regions—which have seen the largest increases in inventory on average—and more modest declines across the Mid-Atlantic and Midwest—which have maintained greater affordability over the past couple years.

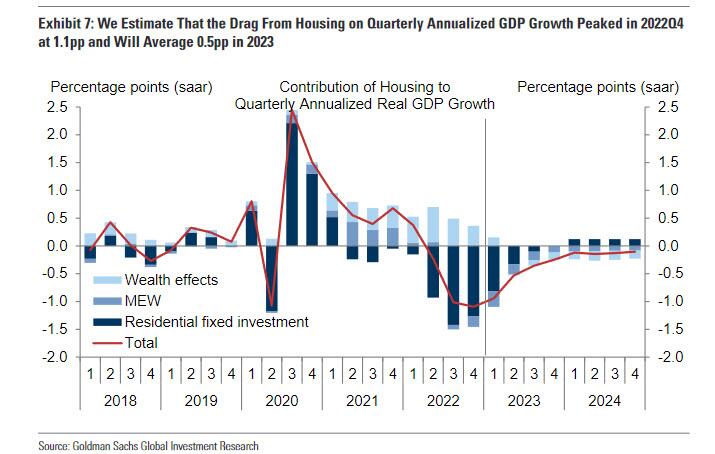

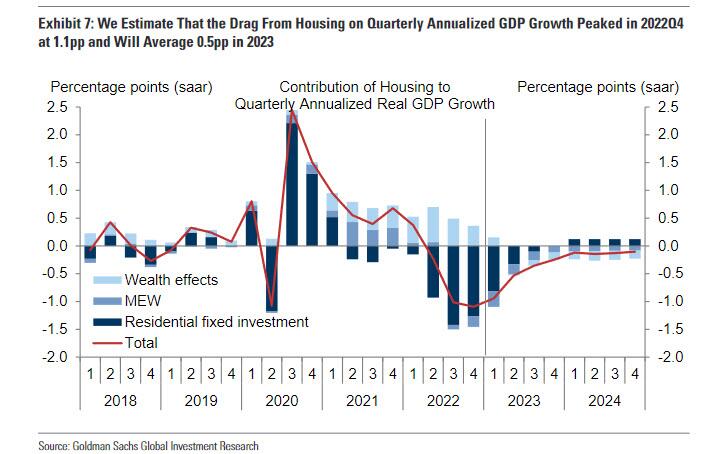

Higher rates and lower home prices will increase the drag on GDP growth from negative wealth effects and declining mortgage equity withdrawal, but we believe that the aggregate drag on GDP growth from the housing sector peaked in 2022Q4 at 1.1pp and will moderate to just 0.25pp by 2023Q4.

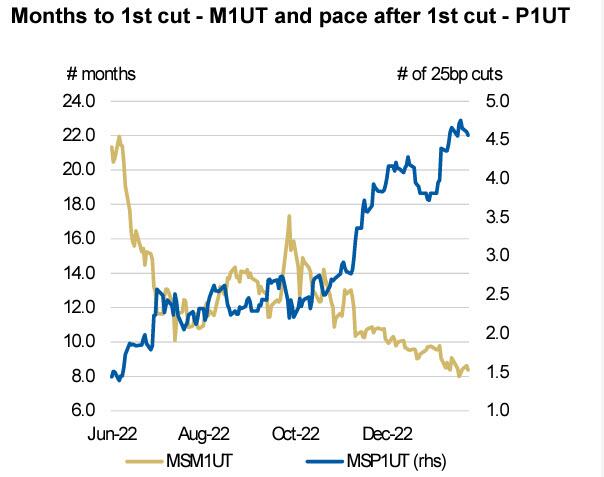

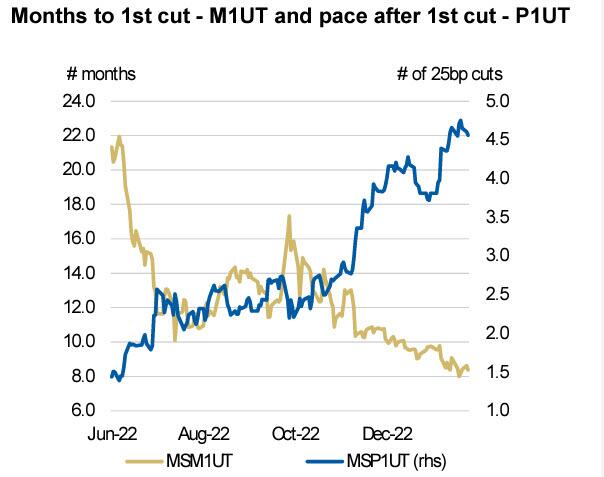

If the housing price futures market - and Goldman - is right in pricing in a housing trough than the consequences could confound markets: on one hand, a stabilization in housing will likely make any coming recession less severe; on the other, since housing is the primary channel by which the Fed can slowdown the economy, any failure to cripple this key US asset, could mean that Powell will be stuck in a "higher for longer" mode for, well, longer than the market expects. As a reminder, as the following Morgan Stanley chart shows, consensus is that the Fed is about 8 months away from its first rate cut, which will be promptly followed by ~4.5 25bps rate cuts.

More in the full Goldman note available to pro subs.

It may come as a bit of a shock to those who have been following the creeping freeze in housing transactions as the bid-ask spread grows to monstrous proportions, leading to a record crash in pending home sales…

… and collapse in US home prices, especially on the West Coast…

… but even though mortgage rates ticked higher back to 6% in January, there is growing speculation that the housing market has bottomed. Why? Because as Goldman’s Rich Provorotsky notes, “bet you didn’t know there were housing price futures…they bottomed in Q4 and have been rallying.” Indeed, the Housing Composite Index traded on the CME is up decidedly in the past month after hitting a 16 month low in November.

Why this surprising bounce? A big reason for the unexpected rebound may be a recent report from real estate company Redfin which last Wednesday reported that “the housing market has begun to recover from a trough in the second week of November with buyers returning at a faster pace than sellers. The number of Redfin customers asking for first tours has improved by 17 percentage points from the November low, and the number of clients contacting.”

Furthermore, according to the report, Redfin agents to begin the home-buying process has improved by 13 points: “I’ve seen more homes go under contract this month than in the entire fourth quarter,” Angela Langone, a San Jose, California, agent, said in the report.

Among notable market moves, Redfin points to mortgage applications which are up 28% from early November as the average 30-year-fixed mortgage rate has dropped to 6.15% from its peak of 7.08% in November, the biggest decline since 2009. Pending home sales rose 3% in December from November.

Preliminary data on the share of Redfin agents’ offers facing bidding wars points to small upticks in the Seattle and Tampa markets this month (however, since this is an uneven trend, expect it to take some time before bidding wars nationally show an upward trend).

“Bidding wars are back in Seattle,” said local Redfin real estate agent Shoshana Godwin. “One of our Issaquah listings got 12 offers and is under contract for $155,000 over the $1.4 million list price. The buyer waived every contingency, handed over $300,000 of earnest money and is letting the seller stay for free for two months after closing. Another home in Seattle’s popular Ballard neighborhood was recently delisted after sitting on the market for over three months. The seller relisted it last week and it went pending in under a day.”

Eric Auciello, Redfin’s team manager in Tampa, has seen three modest single-family homes priced around $300,000 wind up in bidding wars in central Florida this month, with 16, 17 and 23 competing offers, respectively.

More in the full report here.

But while one can accuse Redfin of bias – after all the company recently laid off some 13% of its employees due to the housing market collapse so it is certainly interested in sparking some animal spirits in the sector – it is not alone in predicting a housing recovery. One week ago, Goldman’s Jan Hatzius published the bank’s Housing Outlook for 2023 in which he predicted that “home sales appear set to turn higher.” That’s because “mortgage purchase applications have averaged 9% above their October trough so far in January and survey-based measures of purchasing intentions have rebounded sharply” and while Goldman expects that existing home sales could decline slightly further “but will likely bottom in Q1 (GS forecast: Q1 average of 3.85mn saar vs. 4.02mn in December) before rebounding modestly by year-end (GS forecast: Q4 average of 4.1mn).”

Here are some more observations from the Goldman note (full report available to pro subs):

We forecast that housing starts will take longer to stabilize, declining to a trough pace of 1¼mn in 2023Q4 (vs. 1.4mn in 2022Q4) before recovering next year. We expect completions to total 1½mn this year, the most since 2007, which will help to clear the backlog of homes under construction and contribute to a modest increase in the homeowner vacancy rate (GS forecast of 1.2% in 2023Q4 vs. 0.9% now and 1.4% in 2019Q4).

We expect a peak-to-trough decline in national home prices of roughly 6% and for prices to stop declining around mid-year.

On a regional basis, we project larger declines across the Pacific Coast and Southwest regions—which have seen the largest increases in inventory on average—and more modest declines across the Mid-Atlantic and Midwest—which have maintained greater affordability over the past couple years.

Higher rates and lower home prices will increase the drag on GDP growth from negative wealth effects and declining mortgage equity withdrawal, but we believe that the aggregate drag on GDP growth from the housing sector peaked in 2022Q4 at 1.1pp and will moderate to just 0.25pp by 2023Q4.

If the housing price futures market – and Goldman – is right in pricing in a housing trough than the consequences could confound markets: on one hand, a stabilization in housing will likely make any coming recession less severe; on the other, since housing is the primary channel by which the Fed can slowdown the economy, any failure to cripple this key US asset, could mean that Powell will be stuck in a “higher for longer” mode for, well, longer than the market expects. As a reminder, as the following Morgan Stanley chart shows, consensus is that the Fed is about 8 months away from its first rate cut, which will be promptly followed by ~4.5 25bps rate cuts.

More in the full Goldman note available to pro subs.

Loading…