By Mike Maharrey of MoneyMatals.com

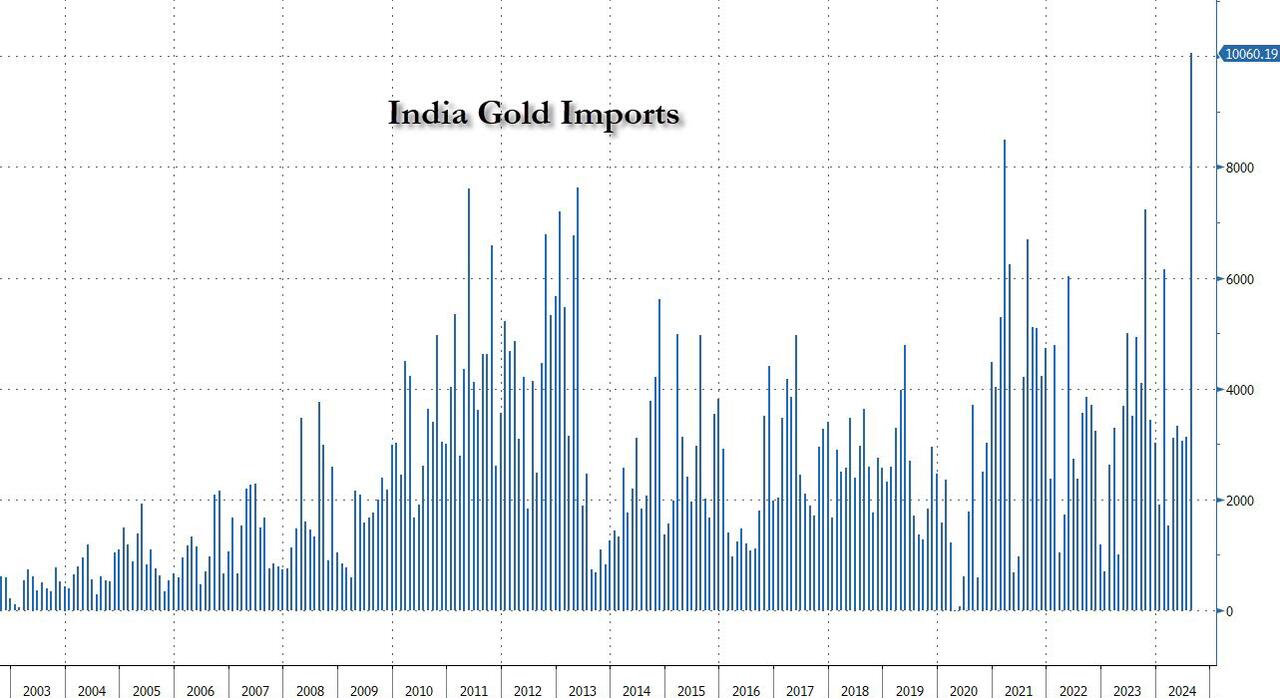

India reported record gold imports in August after the country slashed its import duty the month before. India ranks as the world's second-largest gold consumer behind China.

In July, the Indian government cut taxes on gold and silver imports by more than half, lowering duties from 15 percent to 6 percent. The domestic gold price fell 6 percent month-on-month after the lower duty went into effect, even as the dollar price of gold increased. As expected, the government's move spurred a big jump in gold demand.

India reported record gold imports in dollar terms, totaling $10 billion in August. It was over a three-fold increase over the previous month. The World Gold Council estimates the country imported 140 tons of gold, tripling July’s total.

So far, in 2024, Indian gold imports are up 30 percent.

After falling sharply after the import duty cut, the gold price in rupees stabilized and largely moved in tandem with the international price. Gold was up 3.9 percent in rupee terms in August.

Despite the August price gains, the domestic gold price remains about 2 percent lower than it was before the reduction in the import duty.

According to the World Gold Council, domestic demand for gold coins, bars, and jewelry surged after the duty cut and has since stabilized. Market reports indicate that buying momentum remains “healthy,” with an overall uptick before the import duty reduction.

“Purchases previously deferred are now materializing, and there is increased interest in heavier pieces of jewelry. Industry participants anticipate that this momentum will continue, though they are closely monitoring the crucial festive and wedding season sales that run through late August to December.”

Anecdotal evidence suggests that festival buying kicked off on a strong note.

The World Gold Council also reported that rural gold buying has shown improvement in recent months. A favorable monsoon season is expected to increase crop production, and additional income for farmers will likely boost gold demand in the fall months.

Evidencing strong investor interest in gold, Indian ETFs continue to report inflows of metal. According to World Gold Council estimates, India-based funds experienced the highest monthly inflows of gold on record in August.

So far, in 2024, Indian gold ETFs have added about 9.5 tons of gold.

According to the WGC, total assets under management by Indian gold ETFs have increased to INR374 billion (US$4.4 billion), an 8 percent month-on-month rise and a 54 percent year-on-year increase.

The Reserve Bank of India (RBI) continues to add gold to its reserves. Based on the latest figures, the Indian central bank has increased its gold holdings by 50 tons this year.

The RBI has been buying gold since 2017. Over that period, it has increased its gold holding by over 260 tons.

The Indian central bank now holds a record 853.6 tons of gold. The yellow metal makes up 9 percent of its foreign reserves, up from 7.5 percent a year ago.

An Indian economist told the Times of India that the push to accumulate gold was based on both political and economic factors. He said that the "reliability" of the U.S. dollar has "diminished." He noted the "noticeable decline" in the confidence in U.S. dollar assets.

Another economist told the Times, “It makes a lot of sense (to invest in gold), given the increased volatility in the FX market, elevated interest rates in the U.S., and, of course, also as the central banks in each economy would like to diversify the asset classes in which they are parking their reserves.”

Last spring, the RBI transported 100 tons of its gold from the UK back into India.

Indians have historically had an affinity for gold. Indian households own an estimated 25,000 tons of gold, and that likely understates the amount given the large black market in the country. Gold is deeply interwoven into the country’s marriage ceremonies and cultural rituals. Indians have long valued the yellow metal as a store of wealth, especially in poorer rural regions. Around two-thirds of India’s gold demand comes from beyond the urban centers, where large numbers of people operate outside the tax system.

Gold isn't considered a luxury in India. Even poor Indians buy gold. According to a 2018 ICE 360 survey, one in every two households in India had purchased gold within the last five years. Overall, 87 percent of Indian households own some gold. Even households at the lowest income levels in India hold some of the yellow metal. According to the survey, more than 75 percent of families in the bottom 10 percent of income managed to buy some gold.

The yellow metal was a lifeline for Indians buffeted by the economic storm caused by the government's response to COVID-19. After the Indian government locked down the country, banks tightened credit to mitigate the default risk. Unable to secure traditional loans, Indians used gold to secure financing. As Indians endured a second wave of lockdowns, many Indians resorted to selling gold outright to make ends meet.

By Mike Maharrey of MoneyMatals.com

India reported record gold imports in August after the country slashed its import duty the month before. India ranks as the world’s second-largest gold consumer behind China.

In July, the Indian government cut taxes on gold and silver imports by more than half, lowering duties from 15 percent to 6 percent. The domestic gold price fell 6 percent month-on-month after the lower duty went into effect, even as the dollar price of gold increased. As expected, the government’s move spurred a big jump in gold demand.

India reported record gold imports in dollar terms, totaling $10 billion in August. It was over a three-fold increase over the previous month. The World Gold Council estimates the country imported 140 tons of gold, tripling July’s total.

So far, in 2024, Indian gold imports are up 30 percent.

After falling sharply after the import duty cut, the gold price in rupees stabilized and largely moved in tandem with the international price. Gold was up 3.9 percent in rupee terms in August.

Despite the August price gains, the domestic gold price remains about 2 percent lower than it was before the reduction in the import duty.

According to the World Gold Council, domestic demand for gold coins, bars, and jewelry surged after the duty cut and has since stabilized. Market reports indicate that buying momentum remains “healthy,” with an overall uptick before the import duty reduction.

“Purchases previously deferred are now materializing, and there is increased interest in heavier pieces of jewelry. Industry participants anticipate that this momentum will continue, though they are closely monitoring the crucial festive and wedding season sales that run through late August to December.”

Anecdotal evidence suggests that festival buying kicked off on a strong note.

The World Gold Council also reported that rural gold buying has shown improvement in recent months. A favorable monsoon season is expected to increase crop production, and additional income for farmers will likely boost gold demand in the fall months.

Evidencing strong investor interest in gold, Indian ETFs continue to report inflows of metal. According to World Gold Council estimates, India-based funds experienced the highest monthly inflows of gold on record in August.

So far, in 2024, Indian gold ETFs have added about 9.5 tons of gold.

According to the WGC, total assets under management by Indian gold ETFs have increased to INR374 billion (US$4.4 billion), an 8 percent month-on-month rise and a 54 percent year-on-year increase.

The Reserve Bank of India (RBI) continues to add gold to its reserves. Based on the latest figures, the Indian central bank has increased its gold holdings by 50 tons this year.

The RBI has been buying gold since 2017. Over that period, it has increased its gold holding by over 260 tons.

The Indian central bank now holds a record 853.6 tons of gold. The yellow metal makes up 9 percent of its foreign reserves, up from 7.5 percent a year ago.

An Indian economist told the Times of India that the push to accumulate gold was based on both political and economic factors. He said that the “reliability” of the U.S. dollar has “diminished.” He noted the “noticeable decline” in the confidence in U.S. dollar assets.

Another economist told the Times, “It makes a lot of sense (to invest in gold), given the increased volatility in the FX market, elevated interest rates in the U.S., and, of course, also as the central banks in each economy would like to diversify the asset classes in which they are parking their reserves.”

Last spring, the RBI transported 100 tons of its gold from the UK back into India.

Indians have historically had an affinity for gold. Indian households own an estimated 25,000 tons of gold, and that likely understates the amount given the large black market in the country. Gold is deeply interwoven into the country’s marriage ceremonies and cultural rituals. Indians have long valued the yellow metal as a store of wealth, especially in poorer rural regions. Around two-thirds of India’s gold demand comes from beyond the urban centers, where large numbers of people operate outside the tax system.

Gold isn’t considered a luxury in India. Even poor Indians buy gold. According to a 2018 ICE 360 survey, one in every two households in India had purchased gold within the last five years. Overall, 87 percent of Indian households own some gold. Even households at the lowest income levels in India hold some of the yellow metal. According to the survey, more than 75 percent of families in the bottom 10 percent of income managed to buy some gold.

The yellow metal was a lifeline for Indians buffeted by the economic storm caused by the government’s response to COVID-19. After the Indian government locked down the country, banks tightened credit to mitigate the default risk. Unable to secure traditional loans, Indians used gold to secure financing. As Indians endured a second wave of lockdowns, many Indians resorted to selling gold outright to make ends meet.

Loading…