Authored by Peter Reagan via Birch Gold Group,

After almost 15 years of Fed-fueled cheap money offered at near-zero rates that was leveraged into overinflated speculative bubbles, the lights are on, the crowd is dispersing – and the party might finally be over.

At an actual party, it’s easy to know when it’s time to say your goodbyes. The hosts turn the music off, start looking at their watches and taking away the snacks.

In this metaphorical party, though, how do you know when it’s over?

Analysts describe the end as a “Minsky Moment,” defined as:

the onset of a market collapse brought on by the reckless speculative activity that defines an unsustainable bullish period. Minsky Moment is named after economist Hyman Minsky and defines the point in time where the sudden decline in market sentiment inevitably leads to a market crash. [emphasis added]

The two most important words there, I think, are “sudden” and “inevitably.”

Experts from JP Morgan think the moment is now:

Bank failures, market turmoil and ongoing economic uncertainty as central banks battle high inflation have increased the chances of a “Minsky moment,” according to JPMorgan Chase & Co.’s Marko Kolanovic.

In the past week, investors have contended with several U.S. bank bailouts, market volatility, the collapse of Credit Suisse and the European Central Bank’s 50 basis-point rate hike.

The Fed’s decision to increase rates this week will likely provide yet another concern to Kolanovic and his team.

Obviously, this isn’t the first time that a Minsky Moment has happened in the U.S. The U.S. has experienced a handful in the past, some of which you’ll remember if there’s enough gray in your hair:

In 1998, following the bursting of asset bubbles in Asia, Russia defaulted on its domestic debt and devalued the ruble. (It was during that crisis that Paul McCulley, then an economist at Pacific Investment Management Co., coined the term “Minsky moment.”)

The global financial crisis of 2007-2008 is considered another Minsky moment, since it was caused by the implosion of the U.S. subprime mortgage market.

Since 2008, we’ve talked a lot about a “Lehman moment” – referring to the collapse of white-shoe Wall Street investment bank Lehman Brothers, which notably wasn’t bailed out by the Fed or the Treasury Department. It’s the same thing.

It doesn’t matter what we call that tipping point, that event or that day when everyone finally recognizes the party’s really over, tries to leave at the same time and gets jammed at the exits.

When you read the context above, take note of the common elements in both prior Minsky Moments; debt and bubbles. It looks as though both of those elements are making a return appearance right now.

All Minsky Moments have one thing in common

I discussed the “everything bubble” and its consequences in May of last year. (It didn’t really take a crystal ball to see it coming, though – all you need is a grasp of how financial markets work and a little history).

Like those before and, presumably, future Minsky Moments, the one thing they have in common is debt:

Massive borrowing around the world since the financial crisis – much of it in response to the coronavirus pandemic and its aftermath – has prompted warnings of another Minsky moment to come. The surge was made possible by ultra-easy monetary policy – central banks slashing interest rates – and governments turning on the spending taps. Rising interest rates over the past year as the Federal Reserve and European Central Bank battled inflation have made debt burdens heavier. [emphasis added]

(If you’re a regular reader, you know all this already.)

When ultra-easy monetary policy makes credit and borrowing overabundant, a bubble forms. Instead of being incentivized to save money, the combination of inflation and rising asset prices sends money flooding into increasingly speculative gambles.

When rates go up, like they are right now, all the debt generated to fuel that asset price bubble becomes an anchor that drags economic activity down.

Again, if you pay attention, you already know all this – and you aren’t alone. There’s been no lack of reporting on Wall Street’s mismanaged debt. Comparisons to 2008 only point out jus how much bigger the bubble is this time around:

The financial system has lent with abandon even as U.S. equity valuations jumped to nose-bleed levels experienced only once over the past 100 years and as U.S. housing prices adjusted for inflation exceeded their 2006 pre crisis peak. Fueling this lending spree was the approximately $5 trillion in Federal Reserve bond purchases in response to the pandemic that induced investors to stretch for yield.

One indication of excessive lending is the more than $1 trillion that has been loaned to highly leveraged U.S. companies and the skyrocketing of global debt to a level well in excess of its precrash 2008 peak. According to the International Institute for Finance, global debt reached almost $300 trillion by the second quarter of 2021. In relation to GDP, this was some 350%, above the 280% before September 2008 Lehman bankruptcy.

When the bubble pops, asset prices generally decline – and that puts a heavy dent in our savings.

To make matters worse, failing banks often escape the consequences of their disastrous decisions – thanks to government bailouts. If you think about it, banks are basically the only corporations in the U.S. that simply aren’t allowed to fail. Banks have the federal government convinced that they’re so important that the entire nation is bound by a suicide pact. We can’t afford to let banks fail, the feds will tell us – so we’re going to save them – and you’re going to pay for it.

That’s right.

To add insult to injury, we, you and I, the taxpayers, ultimately pay the bill. And not in just one way, but in several!

-

Higher interest rates on everything from mortgages to credit cards

-

Losses on investments (equities, housing and so on)

-

Lost purchasing power (thanks to the inevitable “quantitative easing” aka money-printing we’re told is “necessary” to stimulate economic recovery)

The problem with identifying any Minsky Moment in real time is, well, you can’t.

Even the sharpest and most seasoned Wall Street veteran can only identify the moment a bubble stops deflating and starts popping in hindsight.

Since we can’t know the future, what can we learn from the past?

No one’s going to bail us out

In the end, we all have to look out for ourselves. If you’ve been persisting in the delusion that financial analysts can help, allow me to present you with two facts:

-

Silicon Valley Bank had an investment-grade credit ratings from the major ratings companies on the day it collapsed.

-

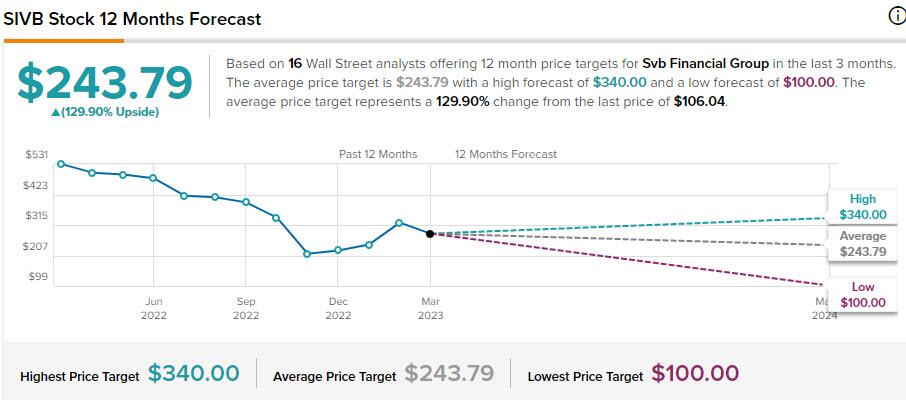

Analyst reports on SVB were overwhelmingly positive (in fact, most of them haven’t been updated) with an average price target of $243!

via TipRanks

Let me reiterate: no one but you is looking out for your best interests.

During times of crisis, whether it’s the next Minsky Moment, bank failure or whatever other black swan event manifests, there’s a coordinated rush to safe haven assets. As the Wall Street proverb goes, no one wants to try to catch a falling knife.

Among safe haven assets, physical precious metals (especially gold and silver) are the gold standard safe haven, as they have been for centuries. Demand is closely tied to price – because no one can print more gold bullion…

Is this a Minsky Moment or not? I don’t know, but what I can tell you is the price of physical gold has risen 8.34% since March 7th.

I strongly recommend you take a minute and educate yourself on the benefits of diversifying with safe haven assets like physical gold and silver (the information is free, and there’s no obligation). Here at Birch Gold, we sincerely believe that education is your best defense against bubbles and panics, market volatility and Federal Reserve shenanigans. You can learn more here.

Authored by Peter Reagan via Birch Gold Group,

After almost 15 years of Fed-fueled cheap money offered at near-zero rates that was leveraged into overinflated speculative bubbles, the lights are on, the crowd is dispersing – and the party might finally be over.

At an actual party, it’s easy to know when it’s time to say your goodbyes. The hosts turn the music off, start looking at their watches and taking away the snacks.

In this metaphorical party, though, how do you know when it’s over?

Analysts describe the end as a “Minsky Moment,” defined as:

the onset of a market collapse brought on by the reckless speculative activity that defines an unsustainable bullish period. Minsky Moment is named after economist Hyman Minsky and defines the point in time where the sudden decline in market sentiment inevitably leads to a market crash. [emphasis added]

The two most important words there, I think, are “sudden” and “inevitably.”

Experts from JP Morgan think the moment is now:

Bank failures, market turmoil and ongoing economic uncertainty as central banks battle high inflation have increased the chances of a “Minsky moment,” according to JPMorgan Chase & Co.’s Marko Kolanovic.

In the past week, investors have contended with several U.S. bank bailouts, market volatility, the collapse of Credit Suisse and the European Central Bank’s 50 basis-point rate hike.

The Fed’s decision to increase rates this week will likely provide yet another concern to Kolanovic and his team.

Obviously, this isn’t the first time that a Minsky Moment has happened in the U.S. The U.S. has experienced a handful in the past, some of which you’ll remember if there’s enough gray in your hair:

In 1998, following the bursting of asset bubbles in Asia, Russia defaulted on its domestic debt and devalued the ruble. (It was during that crisis that Paul McCulley, then an economist at Pacific Investment Management Co., coined the term “Minsky moment.”)

The global financial crisis of 2007-2008 is considered another Minsky moment, since it was caused by the implosion of the U.S. subprime mortgage market.

Since 2008, we’ve talked a lot about a “Lehman moment” – referring to the collapse of white-shoe Wall Street investment bank Lehman Brothers, which notably wasn’t bailed out by the Fed or the Treasury Department. It’s the same thing.

It doesn’t matter what we call that tipping point, that event or that day when everyone finally recognizes the party’s really over, tries to leave at the same time and gets jammed at the exits.

When you read the context above, take note of the common elements in both prior Minsky Moments; debt and bubbles. It looks as though both of those elements are making a return appearance right now.

All Minsky Moments have one thing in common

I discussed the “everything bubble” and its consequences in May of last year. (It didn’t really take a crystal ball to see it coming, though – all you need is a grasp of how financial markets work and a little history).

Like those before and, presumably, future Minsky Moments, the one thing they have in common is debt:

Massive borrowing around the world since the financial crisis – much of it in response to the coronavirus pandemic and its aftermath – has prompted warnings of another Minsky moment to come. The surge was made possible by ultra-easy monetary policy – central banks slashing interest rates – and governments turning on the spending taps. Rising interest rates over the past year as the Federal Reserve and European Central Bank battled inflation have made debt burdens heavier. [emphasis added]

(If you’re a regular reader, you know all this already.)

When ultra-easy monetary policy makes credit and borrowing overabundant, a bubble forms. Instead of being incentivized to save money, the combination of inflation and rising asset prices sends money flooding into increasingly speculative gambles.

When rates go up, like they are right now, all the debt generated to fuel that asset price bubble becomes an anchor that drags economic activity down.

Again, if you pay attention, you already know all this – and you aren’t alone. There’s been no lack of reporting on Wall Street’s mismanaged debt. Comparisons to 2008 only point out jus how much bigger the bubble is this time around:

The financial system has lent with abandon even as U.S. equity valuations jumped to nose-bleed levels experienced only once over the past 100 years and as U.S. housing prices adjusted for inflation exceeded their 2006 pre crisis peak. Fueling this lending spree was the approximately $5 trillion in Federal Reserve bond purchases in response to the pandemic that induced investors to stretch for yield.

One indication of excessive lending is the more than $1 trillion that has been loaned to highly leveraged U.S. companies and the skyrocketing of global debt to a level well in excess of its precrash 2008 peak. According to the International Institute for Finance, global debt reached almost $300 trillion by the second quarter of 2021. In relation to GDP, this was some 350%, above the 280% before September 2008 Lehman bankruptcy.

When the bubble pops, asset prices generally decline – and that puts a heavy dent in our savings.

To make matters worse, failing banks often escape the consequences of their disastrous decisions – thanks to government bailouts. If you think about it, banks are basically the only corporations in the U.S. that simply aren’t allowed to fail. Banks have the federal government convinced that they’re so important that the entire nation is bound by a suicide pact. We can’t afford to let banks fail, the feds will tell us – so we’re going to save them – and you’re going to pay for it.

That’s right.

To add insult to injury, we, you and I, the taxpayers, ultimately pay the bill. And not in just one way, but in several!

-

Higher interest rates on everything from mortgages to credit cards

-

Losses on investments (equities, housing and so on)

-

Lost purchasing power (thanks to the inevitable “quantitative easing” aka money-printing we’re told is “necessary” to stimulate economic recovery)

The problem with identifying any Minsky Moment in real time is, well, you can’t.

Even the sharpest and most seasoned Wall Street veteran can only identify the moment a bubble stops deflating and starts popping in hindsight.

Since we can’t know the future, what can we learn from the past?

No one’s going to bail us out

In the end, we all have to look out for ourselves. If you’ve been persisting in the delusion that financial analysts can help, allow me to present you with two facts:

-

Silicon Valley Bank had an investment-grade credit ratings from the major ratings companies on the day it collapsed.

-

Analyst reports on SVB were overwhelmingly positive (in fact, most of them haven’t been updated) with an average price target of $243!

via TipRanks

Let me reiterate: no one but you is looking out for your best interests.

During times of crisis, whether it’s the next Minsky Moment, bank failure or whatever other black swan event manifests, there’s a coordinated rush to safe haven assets. As the Wall Street proverb goes, no one wants to try to catch a falling knife.

Among safe haven assets, physical precious metals (especially gold and silver) are the gold standard safe haven, as they have been for centuries. Demand is closely tied to price – because no one can print more gold bullion…

Is this a Minsky Moment or not? I don’t know, but what I can tell you is the price of physical gold has risen 8.34% since March 7th.

I strongly recommend you take a minute and educate yourself on the benefits of diversifying with safe haven assets like physical gold and silver (the information is free, and there’s no obligation). Here at Birch Gold, we sincerely believe that education is your best defense against bubbles and panics, market volatility and Federal Reserve shenanigans. You can learn more here.

Loading…