With the QRA, Fed and all megatech earnings now in the rearview mirror, the busiest week of the quarter comes to a merciful end tomorrow, but first we have to survive the January payrolls report. Here is what economists believe the report will show:

- Nonfarm payrolls are expected to grow by 185k, a drop from December's 216k,

- The unemployment rate is forecast to tick up to 3.8% from 3.7%.

- Average hourly earnings are seen rising 0.3% M/M in January, easing from the 0.4% pace in December; the Y/Y increase is expected to remain unchanged at 4.1%.

According to Newsquawk, labor market proxies have been leaning soft with a miss in ADP and a rise in Challenger layoffs (since ADP is always the polar opposite of the BLS print, expect the jobs number to be a multiple-sigma beat).

Elsewhere, the initial jobless claims data for the week that coincides with the usual BLS survey window saw a notable decline, although it was likely weather-related with more recent initial claims figures rising, whereas the continued claims data rose. However, the December JOLTS data rose above expectations while the quits rate was unchanged (this data, however, lags by a month). Analysts highlight the unchanged quits rate signals slower wage gains, which was also evident in the softer US Employment Cost Index report for Q4. Note, the BLS will also be releasing annual revisions to the establishment survey, but it will not provide revisions to the household survey despite adopting a new methodology for the January figures, thus, the January household survey data will not be directly comparable with data for December 2023 or earlier periods.

Regarding Fed implications, Fed Chair Powell stated the base case is not for a March rate cut but he did add that if the labour market saw an unexpected weakening, the Fed would be prepared to cut sooner. A dire report which takes the Fed off their base case would likely help put a March rate cut in play, providing the disinflation process continues, but there is still plenty of data due between now and March, including another NFP and PCE report, as well as two CPI reports.

Some more details on each of these:

EXPECTATIONS:

- Headline jobs added are expected to grow by 185k in January, down from the 216k gain in December although analyst forecasts are wide, ranging between 120-300k.

- Private payrolls are expected to rise by 170k, up from the 164k added in the prior month.

- Manufacturing payrolls are expected to add 5k jobs vs 6k in December.

- Private payrolls are expected to rise by 170k, up from the 164k added in the prior month.

- The unemployment rate is expected to tick up to 3.8% from 3.7%, with analysts forecasting between 3.7-3.9%.

- Note, in December the labour force participation saw a notable decline to 62.5% from 62.8%.

- On wages, average hourly earnings are seen rising 0.3%, easing from the prior 0.4%.

- The Y/Y earnings are expected to rise by 4.1%, maintaining the pace in January, although forecasts range between 4.0 and 4.2%.

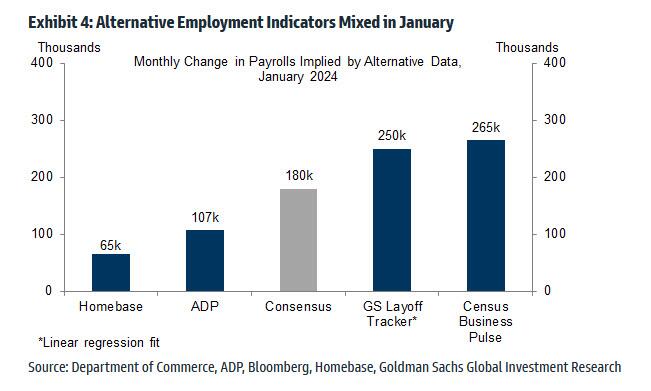

One of the notable upside outliers, is Goldman which in its preview writes that it expects "a strong report, with a large underlying gain in employment partially offset by weather effects... We estimate nonfarm payrolls rose by 250k in January (mom sa)—above consensus of +185k—reflecting below-normal end-of-year layoff rates that more than offset a roughly 50k drag from cold, snowy weather during the survey week. We see a wide range of outcomes for the weather drag and expect this headwind will be visible in the construction and leisure and hospitality categories. Big Data employment indicators were mixed in the month but are also broadly consistent with low layoff rates and a potentially large weather drag."

LABOR MARKET PROXIES:

- The January ADP report, although not the best gauge for NFP, saw 107k jobs added in January, beneath the 145k forecast and prior 158k. However, Pantheon Macroeconomics highlight that the ADP measure has been close to the official estimate in the past three months. Meanwhile, within the ADP report, the wage metrics for job stayers eased to 5.2% from 5.4%, while for job changers it eased to 7.2% from 8.0%.

- The January Challenger Layoffs report saw a notable increase to 82k from 35k in December.

- The Initial Claims data for the week that coincides with the usual NFP survey window saw a notable decline to 189k from 203k, albeit the drop was likely related to the freezing weather in the US. The 4wk initial claims average over January rose to 208k from 203k in the prior week, but it does incorporate the steep weather-related drop, leaving it unchanged from the end of December 4wk average. The Continued Claims data for the NFP survey week, however, rose to 1.828mln from 1.806mln.

- The JOLTS data, albeit for December, was hotter than expected, rising to 9.026mln from 8.925mln (revised up from 8.79mln) although the quits rate was unchanged at 2.2%. Pantheon Macroeconomics writes the rebound in JOLTS does not matter as the data is volatile and subject to large revisions, however, the quits rate is more important as it signals slower wage gains.

- The Q4 Employment Costs Index eased to 0.9% from 1.1%, beneath the 1.0% forecast, also indicative of slowing wages. Employment wages within the report eased to 0.9% from 1.2%, while employment benefits eased to 0.7% from 0.9%.

ANNUAL REVISIONS: The report will see the incorporation of the 2023 revisions. Within the establishment survey, the BLS tells us that "nonfarm payroll employment, hours, and earnings data from the establishment survey will be revised to reflect the annual benchmark process and updated seasonal adjustment factors. Not seasonally adjusted data beginning with April 2022 and seasonally adjusted data beginning with January 2019 are subject to revision". Meanwhile, for the household survey, new population controls will be used in the estimation process which reflect the annual update of population estimates by the US Census Bureau. However, the BLS highlights, "In accordance with usual practice, historical data will not be revised to incorporate the new controls. Consequently, household survey data for January 2024 will not be directly comparable with data for December 2023 or earlier periods". Note, the US unemployment rate is derived from the household survey.

ARGUING FOR A STRONGER THAN EXPECTED REPORT:

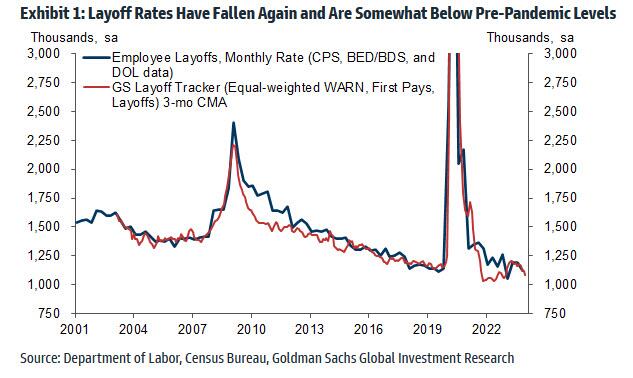

- Layoffs. Expect a boost from below-normal end-of-year layoffs on the order of 100k in tomorrow’s report. As shown in Exhibit 1, the Goldman layoff tracker indicates 1.1 million layoffs in January, a low level and a roughly 10% decline since mid-2023. The January payroll seasonals have started to evolve to reflect and offset the this post-pandemic trend, with a month-over-month hurdle for private payrolls of -2,584k in January 2023 compared to -2,773k in January 2019 (which was also a 4-week payroll month). However, even with this unfavorable evolution, nonfarm payrolls still rose by 436k month-over-month in January 2023—a 140k pickup relative to the 3-month average. Goldman's layoff tracker is 50k higher than it was last January, which would argue for a boost from low layoffs of around 90k this January, other things equal.

- Jobless claims. Initial jobless claims decreased to an average of 204k in the January payroll month, down from 212k in December and 225k on average in 2023. The JOLTS layoff rate was unchanged at low levels (1.0%) in December. Announced layoffs reported by Challenger, Gray & Christmas increased by 16k in January to 57k (SA by GS), compared to 54k on average in the second half of 2023.

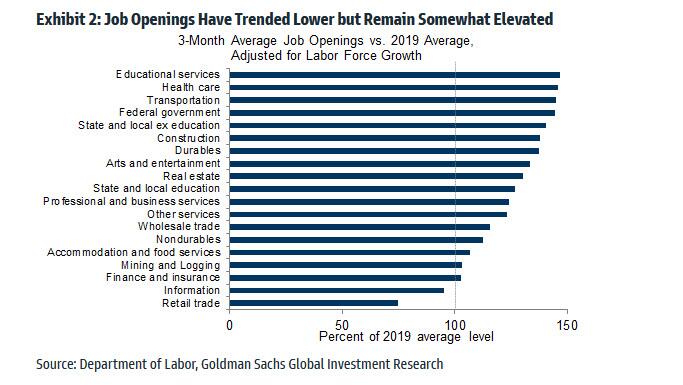

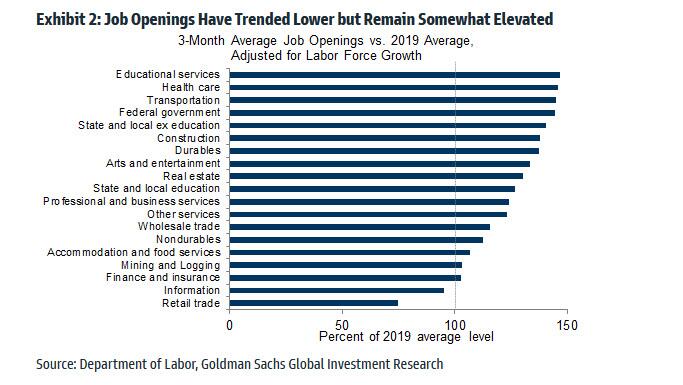

- Job availability. JOLTS job openings increased by 101k month-over-month to 9.0mn in December, well above consensus expectations, and online measures have declined slightly in recent months. While labor demand has fallen meaningfully on net, it remains elevated by 1-2 million relative to 2019 and represents a positive factor for job growth, in our view. Indeed, job openings remain above their 2019 levels in nearly every industry. Additionally, the Conference Board labor differential—the difference between the percent of respondents saying jobs are plentiful and those saying jobs are hard to get—increased by 8.4pt to +35.7 in January.

ARGUING FOR A WEAKER-THAN-EXPECTED REPORT

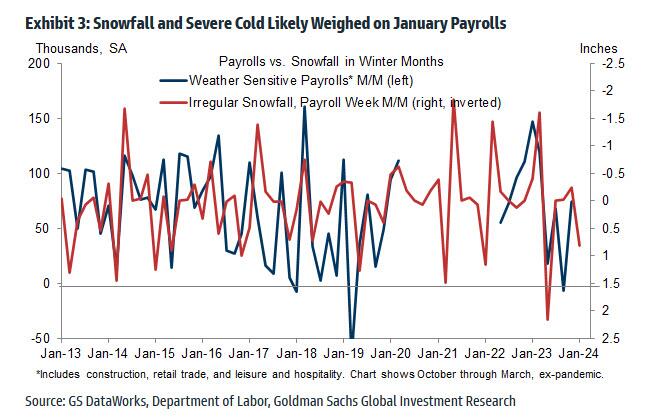

- Weather. Goldman assumes a 50k drag from cold, snowy weather during the survey week in the Midwest and Northeast. As shown below, the January increase in population-weighted snowfall (mom sa) argues for a drag in weather-sensitive industries such as construction, leisure, and retail—especially because good weather likely flattered the December employment report. While there are a wide range of outcomes for the weather drag, expect low layoff rates to offset or partially offset this headwind in the retail and leisure categories.

- Employer surveys. The employment components of business surveys were net weaker in January. The employment component of the GS manufacturing survey tracker declined 1.3pt to 47.5 while the employment component of the services survey tracker increased 0.2pt to 49.8. Both trackers remain below their 2018-2019 average levels of 55.3 and 56.6, respectively.

NEUTRAL/MIXED FACTORS:

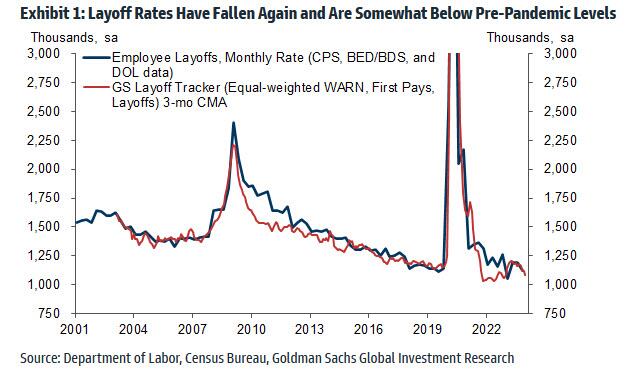

- Big Data. Big Data employment indicators were mixed in January, with an average pace of +179k across the four indicators tracked by Goldman economists. This compares to the +150k median of these measures in December.

- Worker strikes. The return of 3k striking workers will boost payroll growth by that amount in tomorrow’s report. This compares to the 8k boost in last month’s report and a 38k boost in November.

FED IMPLICATIONS: The FOMC on Wednesday saw rates left unchanged and removed its tightening bias in the statement as expected, it also played down the prospects of near-term rate cuts with Powell explicitly saying a March cut is not likely. Money markets have pared back their implied probability of a rate cut for the March meeting to c. 35% from the 50%+ pricing pre-FOMC. The NFP report will help shape those expectations, where a surprise downside report for the labour market would support the case for a March cut but it is seen as increasingly unlikely. Barclays and Goldman Sachs have both pushed back their March rate cut calls since the FOMC to May, while BofA pushed back their rate cut call to June from March. Nonetheless, Fed Chair Powell said many times in his post-FOMC Presser/Q&A that the labor market remains strong, but he did warn of earlier rate cuts than expected if that were to change, "If we saw an unexpected weakening [in the labour market] that would certainly weigh on cutting sooner", how sooner remains to be seen, but March would still appear a possibility, providing the data supported it. When questioned on a March cut, Powell said, "I don’t think that’s...what we would call the base case", but he also didn't rule out the possibility. Powell pointed to the December SEPs - which saw three rate cuts in 2024 - "as good evidence of where people are", whilst saying that the "base case" assumes that "we have a strong labor market, we have inflation coming down, that’s what people are writing their SEP around". So, if the base case assumes continued disinflation progress and a strong labor market leading to three rate cuts this year - with March being too early for the first cut in that scenario - a weak labour market report that takes the Fed off that base case could be the key to putting March back in play for the Fed and a deeper cutting cycle than the Dec SEPs median forecast of three 25bp cuts, assuming disinflation continues as expected.

DATES AHEAD: The next FOMC is on March 19-20th. The January & February CPI reports are due on February 13th and March 12th, respectively, as well as the February jobs report due March 8th and the January PCE due February 29th. All will be key in determining the timing of the Fed's first rate cut and extrapolating the depth of cuts over the year, with the market still priced for nearly six 25bps cuts across the year.

MARKET REACTION: According to Goldman, while the S&P is less than 1% below ATHs, markets should still like a miss since it raises the chance of a cut (Reminder March Cut probability stands at 40%). The reaction should prove out to be more so asymmetric for equities as Powell was pretty unconcerned about upside growth, but acknowledged they will be quick to cut in a downside surprise scenario. Given that the market isn't really concerned about a bad growth outcome anymore, bad news tomorrow should be good for the market.

- 250k+ S&P sells off at least 50-75bps

- 200k – 250k S&P + / - 40bps

- 150k – 200 S&P +75bps-100bps

- 50 – 150k S&P -25bps / +50bps

The question, however, is what does Biden want: does he still believe that if he manipulates the data long and strong enough, the average American will finally give him credit for "Bidenomics." Alternatively, has Biden given up on the economy, and is he more focused on levitating stocks as a shortcut to gaining votes. The answer to those two questions will determine what number we get tomorrow.

More in the full payrolls preview folder available to pro subscribers.

With the QRA, Fed and all megatech earnings now in the rearview mirror, the busiest week of the quarter comes to a merciful end tomorrow, but first we have to survive the January payrolls report. Here is what economists believe the report will show:

- Nonfarm payrolls are expected to grow by 185k, a drop from December’s 216k,

- The unemployment rate is forecast to tick up to 3.8% from 3.7%.

- Average hourly earnings are seen rising 0.3% M/M in January, easing from the 0.4% pace in December; the Y/Y increase is expected to remain unchanged at 4.1%.

According to Newsquawk, labor market proxies have been leaning soft with a miss in ADP and a rise in Challenger layoffs (since ADP is always the polar opposite of the BLS print, expect the jobs number to be a multiple-sigma beat).

Elsewhere, the initial jobless claims data for the week that coincides with the usual BLS survey window saw a notable decline, although it was likely weather-related with more recent initial claims figures rising, whereas the continued claims data rose. However, the December JOLTS data rose above expectations while the quits rate was unchanged (this data, however, lags by a month). Analysts highlight the unchanged quits rate signals slower wage gains, which was also evident in the softer US Employment Cost Index report for Q4. Note, the BLS will also be releasing annual revisions to the establishment survey, but it will not provide revisions to the household survey despite adopting a new methodology for the January figures, thus, the January household survey data will not be directly comparable with data for December 2023 or earlier periods.

Regarding Fed implications, Fed Chair Powell stated the base case is not for a March rate cut but he did add that if the labour market saw an unexpected weakening, the Fed would be prepared to cut sooner. A dire report which takes the Fed off their base case would likely help put a March rate cut in play, providing the disinflation process continues, but there is still plenty of data due between now and March, including another NFP and PCE report, as well as two CPI reports.

Some more details on each of these:

EXPECTATIONS:

- Headline jobs added are expected to grow by 185k in January, down from the 216k gain in December although analyst forecasts are wide, ranging between 120-300k.

- Private payrolls are expected to rise by 170k, up from the 164k added in the prior month.

- Manufacturing payrolls are expected to add 5k jobs vs 6k in December.

- Private payrolls are expected to rise by 170k, up from the 164k added in the prior month.

- The unemployment rate is expected to tick up to 3.8% from 3.7%, with analysts forecasting between 3.7-3.9%.

- Note, in December the labour force participation saw a notable decline to 62.5% from 62.8%.

- On wages, average hourly earnings are seen rising 0.3%, easing from the prior 0.4%.

- The Y/Y earnings are expected to rise by 4.1%, maintaining the pace in January, although forecasts range between 4.0 and 4.2%.

One of the notable upside outliers, is Goldman which in its preview writes that it expects “a strong report, with a large underlying gain in employment partially offset by weather effects… We estimate nonfarm payrolls rose by 250k in January (mom sa)—above consensus of +185k—reflecting below-normal end-of-year layoff rates that more than offset a roughly 50k drag from cold, snowy weather during the survey week. We see a wide range of outcomes for the weather drag and expect this headwind will be visible in the construction and leisure and hospitality categories. Big Data employment indicators were mixed in the month but are also broadly consistent with low layoff rates and a potentially large weather drag.”

LABOR MARKET PROXIES:

- The January ADP report, although not the best gauge for NFP, saw 107k jobs added in January, beneath the 145k forecast and prior 158k. However, Pantheon Macroeconomics highlight that the ADP measure has been close to the official estimate in the past three months. Meanwhile, within the ADP report, the wage metrics for job stayers eased to 5.2% from 5.4%, while for job changers it eased to 7.2% from 8.0%.

- The January Challenger Layoffs report saw a notable increase to 82k from 35k in December.

- The Initial Claims data for the week that coincides with the usual NFP survey window saw a notable decline to 189k from 203k, albeit the drop was likely related to the freezing weather in the US. The 4wk initial claims average over January rose to 208k from 203k in the prior week, but it does incorporate the steep weather-related drop, leaving it unchanged from the end of December 4wk average. The Continued Claims data for the NFP survey week, however, rose to 1.828mln from 1.806mln.

- The JOLTS data, albeit for December, was hotter than expected, rising to 9.026mln from 8.925mln (revised up from 8.79mln) although the quits rate was unchanged at 2.2%. Pantheon Macroeconomics writes the rebound in JOLTS does not matter as the data is volatile and subject to large revisions, however, the quits rate is more important as it signals slower wage gains.

- The Q4 Employment Costs Index eased to 0.9% from 1.1%, beneath the 1.0% forecast, also indicative of slowing wages. Employment wages within the report eased to 0.9% from 1.2%, while employment benefits eased to 0.7% from 0.9%.

ANNUAL REVISIONS: The report will see the incorporation of the 2023 revisions. Within the establishment survey, the BLS tells us that “nonfarm payroll employment, hours, and earnings data from the establishment survey will be revised to reflect the annual benchmark process and updated seasonal adjustment factors. Not seasonally adjusted data beginning with April 2022 and seasonally adjusted data beginning with January 2019 are subject to revision“. Meanwhile, for the household survey, new population controls will be used in the estimation process which reflect the annual update of population estimates by the US Census Bureau. However, the BLS highlights, “In accordance with usual practice, historical data will not be revised to incorporate the new controls. Consequently, household survey data for January 2024 will not be directly comparable with data for December 2023 or earlier periods“. Note, the US unemployment rate is derived from the household survey.

ARGUING FOR A STRONGER THAN EXPECTED REPORT:

- Layoffs. Expect a boost from below-normal end-of-year layoffs on the order of 100k in tomorrow’s report. As shown in Exhibit 1, the Goldman layoff tracker indicates 1.1 million layoffs in January, a low level and a roughly 10% decline since mid-2023. The January payroll seasonals have started to evolve to reflect and offset the this post-pandemic trend, with a month-over-month hurdle for private payrolls of -2,584k in January 2023 compared to -2,773k in January 2019 (which was also a 4-week payroll month). However, even with this unfavorable evolution, nonfarm payrolls still rose by 436k month-over-month in January 2023—a 140k pickup relative to the 3-month average. Goldman’s layoff tracker is 50k higher than it was last January, which would argue for a boost from low layoffs of around 90k this January, other things equal.

- Jobless claims. Initial jobless claims decreased to an average of 204k in the January payroll month, down from 212k in December and 225k on average in 2023. The JOLTS layoff rate was unchanged at low levels (1.0%) in December. Announced layoffs reported by Challenger, Gray & Christmas increased by 16k in January to 57k (SA by GS), compared to 54k on average in the second half of 2023.

- Job availability. JOLTS job openings increased by 101k month-over-month to 9.0mn in December, well above consensus expectations, and online measures have declined slightly in recent months. While labor demand has fallen meaningfully on net, it remains elevated by 1-2 million relative to 2019 and represents a positive factor for job growth, in our view. Indeed, job openings remain above their 2019 levels in nearly every industry. Additionally, the Conference Board labor differential—the difference between the percent of respondents saying jobs are plentiful and those saying jobs are hard to get—increased by 8.4pt to +35.7 in January.

ARGUING FOR A WEAKER-THAN-EXPECTED REPORT

- Weather. Goldman assumes a 50k drag from cold, snowy weather during the survey week in the Midwest and Northeast. As shown below, the January increase in population-weighted snowfall (mom sa) argues for a drag in weather-sensitive industries such as construction, leisure, and retail—especially because good weather likely flattered the December employment report. While there are a wide range of outcomes for the weather drag, expect low layoff rates to offset or partially offset this headwind in the retail and leisure categories.

- Employer surveys. The employment components of business surveys were net weaker in January. The employment component of the GS manufacturing survey tracker declined 1.3pt to 47.5 while the employment component of the services survey tracker increased 0.2pt to 49.8. Both trackers remain below their 2018-2019 average levels of 55.3 and 56.6, respectively.

NEUTRAL/MIXED FACTORS:

- Big Data. Big Data employment indicators were mixed in January, with an average pace of +179k across the four indicators tracked by Goldman economists. This compares to the +150k median of these measures in December.

- Worker strikes. The return of 3k striking workers will boost payroll growth by that amount in tomorrow’s report. This compares to the 8k boost in last month’s report and a 38k boost in November.

FED IMPLICATIONS: The FOMC on Wednesday saw rates left unchanged and removed its tightening bias in the statement as expected, it also played down the prospects of near-term rate cuts with Powell explicitly saying a March cut is not likely. Money markets have pared back their implied probability of a rate cut for the March meeting to c. 35% from the 50%+ pricing pre-FOMC. The NFP report will help shape those expectations, where a surprise downside report for the labour market would support the case for a March cut but it is seen as increasingly unlikely. Barclays and Goldman Sachs have both pushed back their March rate cut calls since the FOMC to May, while BofA pushed back their rate cut call to June from March. Nonetheless, Fed Chair Powell said many times in his post-FOMC Presser/Q&A that the labor market remains strong, but he did warn of earlier rate cuts than expected if that were to change, “If we saw an unexpected weakening [in the labour market] that would certainly weigh on cutting sooner”, how sooner remains to be seen, but March would still appear a possibility, providing the data supported it. When questioned on a March cut, Powell said, “I don’t think that’s…what we would call the base case”, but he also didn’t rule out the possibility. Powell pointed to the December SEPs – which saw three rate cuts in 2024 – “as good evidence of where people are”, whilst saying that the “base case” assumes that “we have a strong labor market, we have inflation coming down, that’s what people are writing their SEP around”. So, if the base case assumes continued disinflation progress and a strong labor market leading to three rate cuts this year – with March being too early for the first cut in that scenario – a weak labour market report that takes the Fed off that base case could be the key to putting March back in play for the Fed and a deeper cutting cycle than the Dec SEPs median forecast of three 25bp cuts, assuming disinflation continues as expected.

DATES AHEAD: The next FOMC is on March 19-20th. The January & February CPI reports are due on February 13th and March 12th, respectively, as well as the February jobs report due March 8th and the January PCE due February 29th. All will be key in determining the timing of the Fed’s first rate cut and extrapolating the depth of cuts over the year, with the market still priced for nearly six 25bps cuts across the year.

MARKET REACTION: According to Goldman, while the S&P is less than 1% below ATHs, markets should still like a miss since it raises the chance of a cut (Reminder March Cut probability stands at 40%). The reaction should prove out to be more so asymmetric for equities as Powell was pretty unconcerned about upside growth, but acknowledged they will be quick to cut in a downside surprise scenario. Given that the market isn’t really concerned about a bad growth outcome anymore, bad news tomorrow should be good for the market.

- 250k+ S&P sells off at least 50-75bps

- 200k – 250k S&P + / – 40bps

- 150k – 200 S&P +75bps-100bps

- 50 – 150k S&P -25bps / +50bps

The question, however, is what does Biden want: does he still believe that if he manipulates the data long and strong enough, the average American will finally give him credit for “Bidenomics.” Alternatively, has Biden given up on the economy, and is he more focused on levitating stocks as a shortcut to gaining votes. The answer to those two questions will determine what number we get tomorrow.

More in the full payrolls preview folder available to pro subscribers.

Loading…