By Russell Clark, author of the Capital Flows and Asset Market substack

Japan and Treasuries

My interest in Japan dates from 1991 when I was fresh faced high school exchange student in Kobe. There are no prizes for finding me in the above photo. I was the only “foreigner” in the school, and would go days without seeing anyone else that looked like me or even speaking English. I managed to combine my knowledge and experience in Japan with my other love, economics. I don’t think its too much of an exaggeration to say I owe my career and wealth through studying the Japan experience carefully and then applying those lessons to the rest of the world.

One of the most fascinating things about Japanese, economically speaking, is that almost its entire foreign reserves are made up of US treasuries, with almost no gold. As the right hand side column below shows, the share of gold as foreign exchange reserves is highest for the “old world”, while new powers such as China, Japan, Taiwan and Saudi Arabia have relatively low shares.

In absolute terms, China and Japan are by far the largest holders of foreign exchange reserves.

While China has larger foreign reserves than Japan now, Japan basically “invented” the idea of sovereign bonds as foreign exchange reserves. During the gold standard days, if a country like the US wanted to consume more than it produced, it would need to transfer gold overseas. With limited gold supply, this limited consumption. Moving to a treasury based financial system essentially removed this constraint. The only issue is whether other governments would accept treasuries or not.

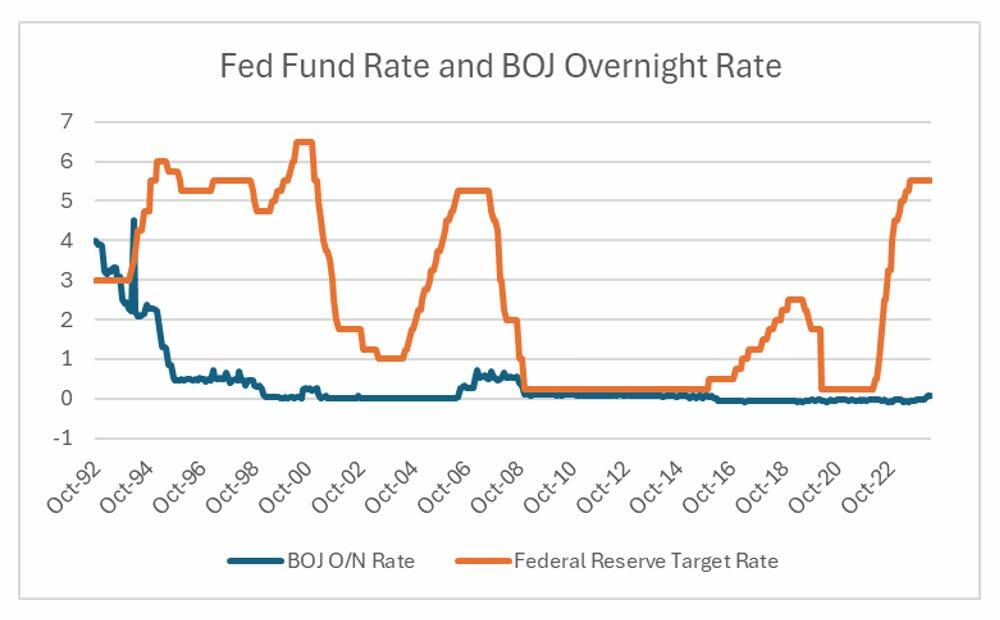

Why did Japan buy treasuries? Well when the bubble economy burst in the early 1990s, the BOJ cut rates to near zero, but the Yen did not collapse as expected.

In fact in the first stages of BOJ interest rates cuts, the Yen actually rallied. The failure of monetary policy to work as it should led the Ministry of Finance to intervene to try and help weaken the Yen, and official buying of US dollar assets took off.

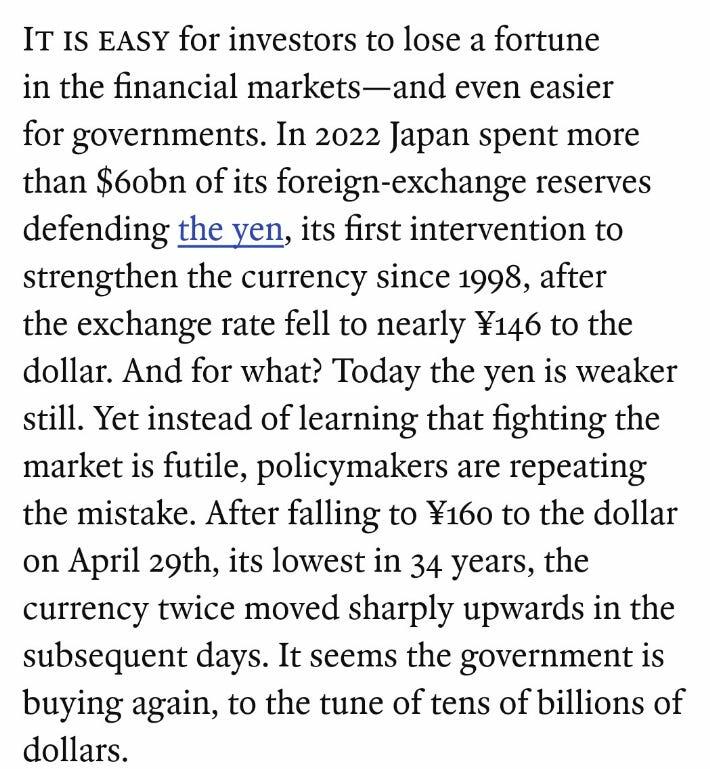

In pro-labor terms, when a government is pro-capital it wants to devalue to reduce the wages of its workers. This creates a trade surplus, which should cause the currency to appreciate, but if the government wants to keep the exchange rate competitive (i.e. keep real wages low), then it needs to buy more and more treasuries. A pro-labor government is happy to see its currency appreciate, and hence does not build foreign currency reserves. What is odd recently is that even as the BOJ remains extremely tardy in its monetary policy response, the Ministry of Finance in Japan has started using foreign reserves to “strengthen” the Yen. As the Economist points out, Japan is currently intervening in the currency market to try and strengthen the Yen.

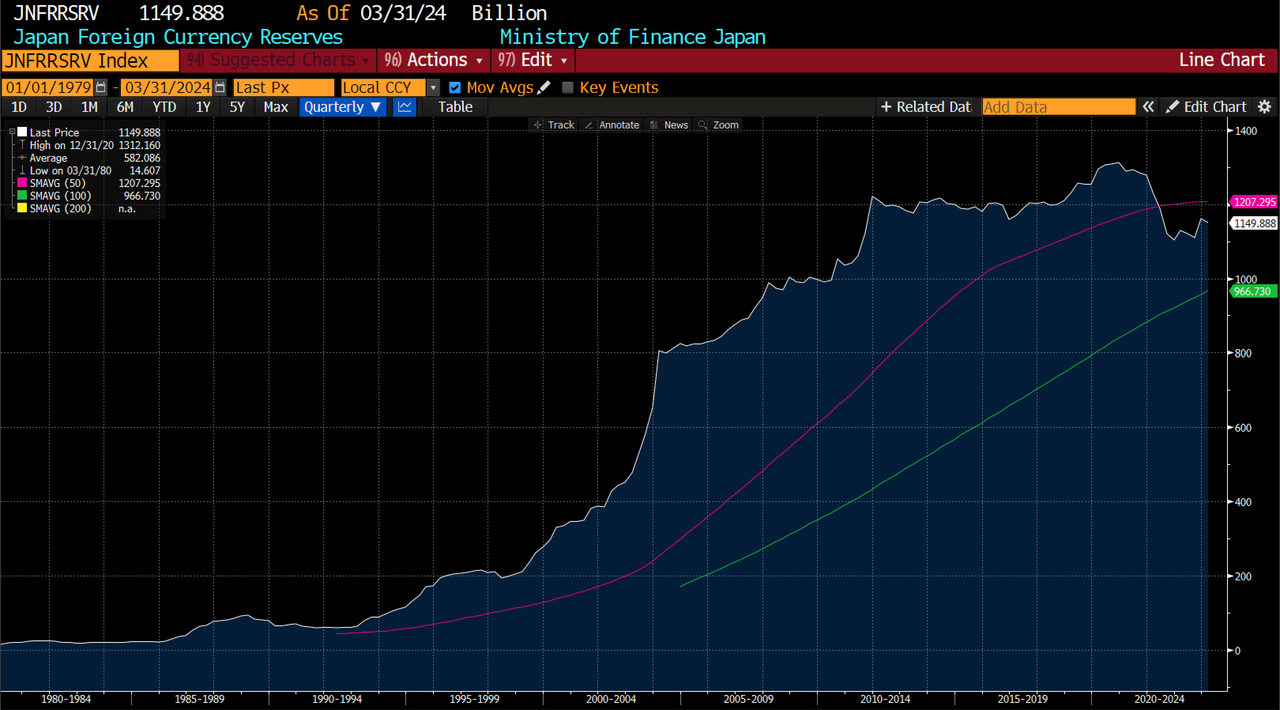

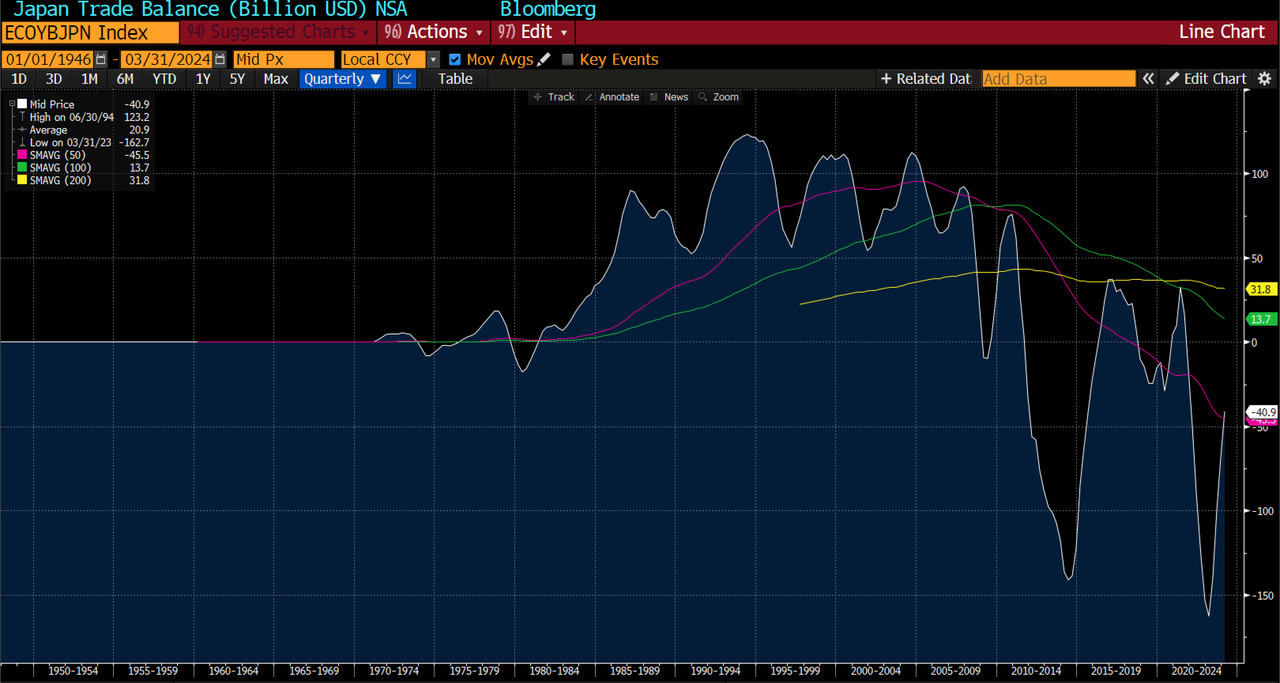

We don’t know the cost of the foreign exchange intervention at the moment [ZH: we do, it was $59BN], but as can be seen above, Japanese foreign exchange reserves have not been rebuilt since the last intervention in 2022. Japan also does not run the structural trade surplus that it did from 1980 to 2010.

With falling foreign exchange reserves, trade deficit, and the likely increase in defence spending that the Russian-Ukrainian war implies, BOJ policy looks increasingly wrong. Markets seem to agree, with 10 year JGB yields at 13 year highs.

With either a Biden or Trump presidency in 2025, the chances of an austerity driven fiscal policy or a change in trade policy looks unlikely to me. The Japanese may well be caught in a doom loop, where they need to sell more foreign reserves to prop up the currency, which cause US yields to rise, which causes the Yen to weaken further and so on.

Until and unless the BOJ becomes more aggressive, Treasuries look like to have a systematic buyer turn into a systematic seller. China is likely a seller of treasuries and buyer of gold for political and strategic reasons, and Japan is a seller of treasuries for economic reasons. I am still baffled to why retail investors prefer treasuries to gold.

Japan was the key to understanding why treasuries did so well form 1980 to 2020. I think it is now the key to understanding why treasuries are going to do poorly from 2020 onwards.

By Russell Clark, author of the Capital Flows and Asset Market substack

Japan and Treasuries

My interest in Japan dates from 1991 when I was fresh faced high school exchange student in Kobe. There are no prizes for finding me in the above photo. I was the only “foreigner” in the school, and would go days without seeing anyone else that looked like me or even speaking English. I managed to combine my knowledge and experience in Japan with my other love, economics. I don’t think its too much of an exaggeration to say I owe my career and wealth through studying the Japan experience carefully and then applying those lessons to the rest of the world.

One of the most fascinating things about Japanese, economically speaking, is that almost its entire foreign reserves are made up of US treasuries, with almost no gold. As the right hand side column below shows, the share of gold as foreign exchange reserves is highest for the “old world”, while new powers such as China, Japan, Taiwan and Saudi Arabia have relatively low shares.

In absolute terms, China and Japan are by far the largest holders of foreign exchange reserves.

While China has larger foreign reserves than Japan now, Japan basically “invented” the idea of sovereign bonds as foreign exchange reserves. During the gold standard days, if a country like the US wanted to consume more than it produced, it would need to transfer gold overseas. With limited gold supply, this limited consumption. Moving to a treasury based financial system essentially removed this constraint. The only issue is whether other governments would accept treasuries or not.

Why did Japan buy treasuries? Well when the bubble economy burst in the early 1990s, the BOJ cut rates to near zero, but the Yen did not collapse as expected.

In fact in the first stages of BOJ interest rates cuts, the Yen actually rallied. The failure of monetary policy to work as it should led the Ministry of Finance to intervene to try and help weaken the Yen, and official buying of US dollar assets took off.

In pro-labor terms, when a government is pro-capital it wants to devalue to reduce the wages of its workers. This creates a trade surplus, which should cause the currency to appreciate, but if the government wants to keep the exchange rate competitive (i.e. keep real wages low), then it needs to buy more and more treasuries. A pro-labor government is happy to see its currency appreciate, and hence does not build foreign currency reserves. What is odd recently is that even as the BOJ remains extremely tardy in its monetary policy response, the Ministry of Finance in Japan has started using foreign reserves to “strengthen” the Yen. As the Economist points out, Japan is currently intervening in the currency market to try and strengthen the Yen.

We don’t know the cost of the foreign exchange intervention at the moment [ZH: we do, it was $59BN], but as can be seen above, Japanese foreign exchange reserves have not been rebuilt since the last intervention in 2022. Japan also does not run the structural trade surplus that it did from 1980 to 2010.

With falling foreign exchange reserves, trade deficit, and the likely increase in defence spending that the Russian-Ukrainian war implies, BOJ policy looks increasingly wrong. Markets seem to agree, with 10 year JGB yields at 13 year highs.

With either a Biden or Trump presidency in 2025, the chances of an austerity driven fiscal policy or a change in trade policy looks unlikely to me. The Japanese may well be caught in a doom loop, where they need to sell more foreign reserves to prop up the currency, which cause US yields to rise, which causes the Yen to weaken further and so on.

Until and unless the BOJ becomes more aggressive, Treasuries look like to have a systematic buyer turn into a systematic seller. China is likely a seller of treasuries and buyer of gold for political and strategic reasons, and Japan is a seller of treasuries for economic reasons. I am still baffled to why retail investors prefer treasuries to gold.

Japan was the key to understanding why treasuries did so well form 1980 to 2020. I think it is now the key to understanding why treasuries are going to do poorly from 2020 onwards.

Loading…