By Ven Ram, Bloomberg markets live reporter and strategist

Japanese stocks can withstand a quick bounce in the yen, but will start to feel the pinch if the currency’s advance goes deeper and becomes more entrenched.

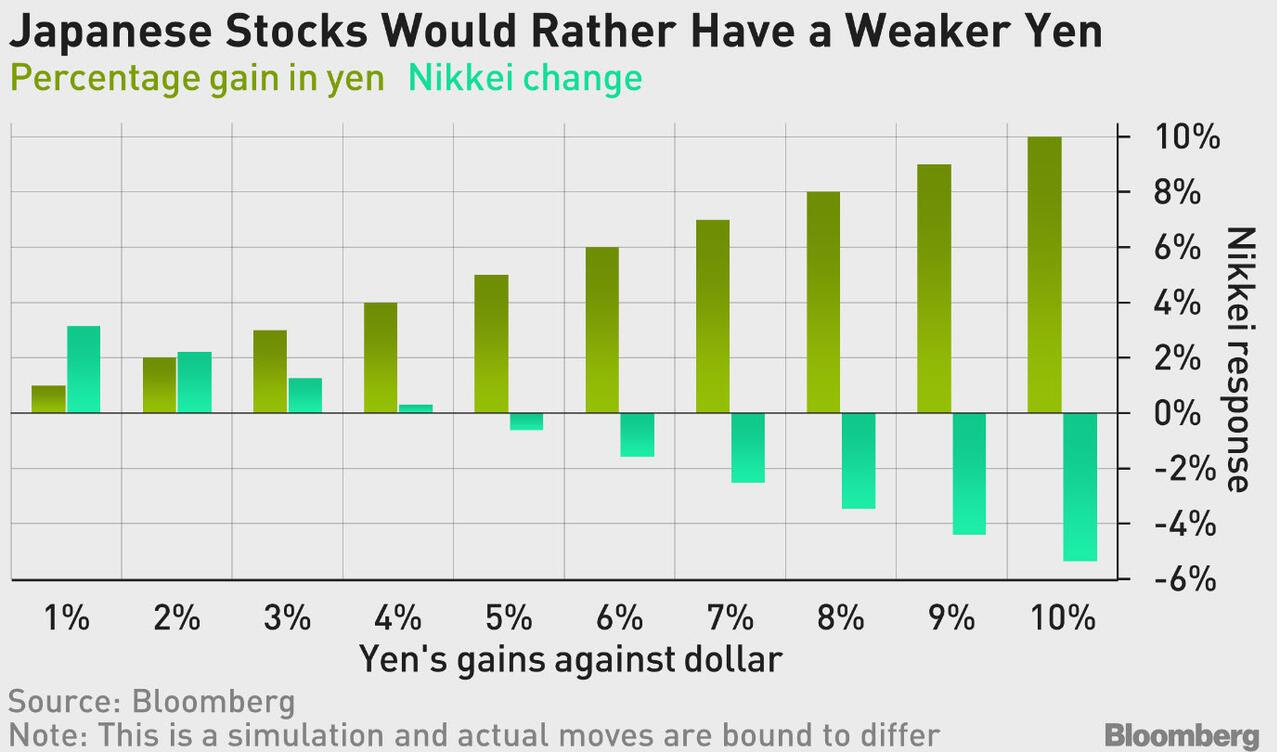

Gains in the Nikkei 225 Index will start slowing if the yen begins to advance sustainably against its major trading partners and in particular the dollar. That could turn into losses should the currency strengthen more than 5% this year.

The following chart shows how a strengthening of the yen against the dollar may affect the Nikkei’s fortunes, based on data going back almost a quarter of a century. The results are similar when the dollar is substituted with a trade-weighted basket of Japan’s major trading partners.

The Nikkei almost doubled in value over the past five years as Deutsche Bank’s trade-weighted yen slumped more than 20% over that period. A weaker yen is a tailwind for Japanese exporters, in particular automobile makers, whose overseas earnings morph into bigger gains after the currency translation.

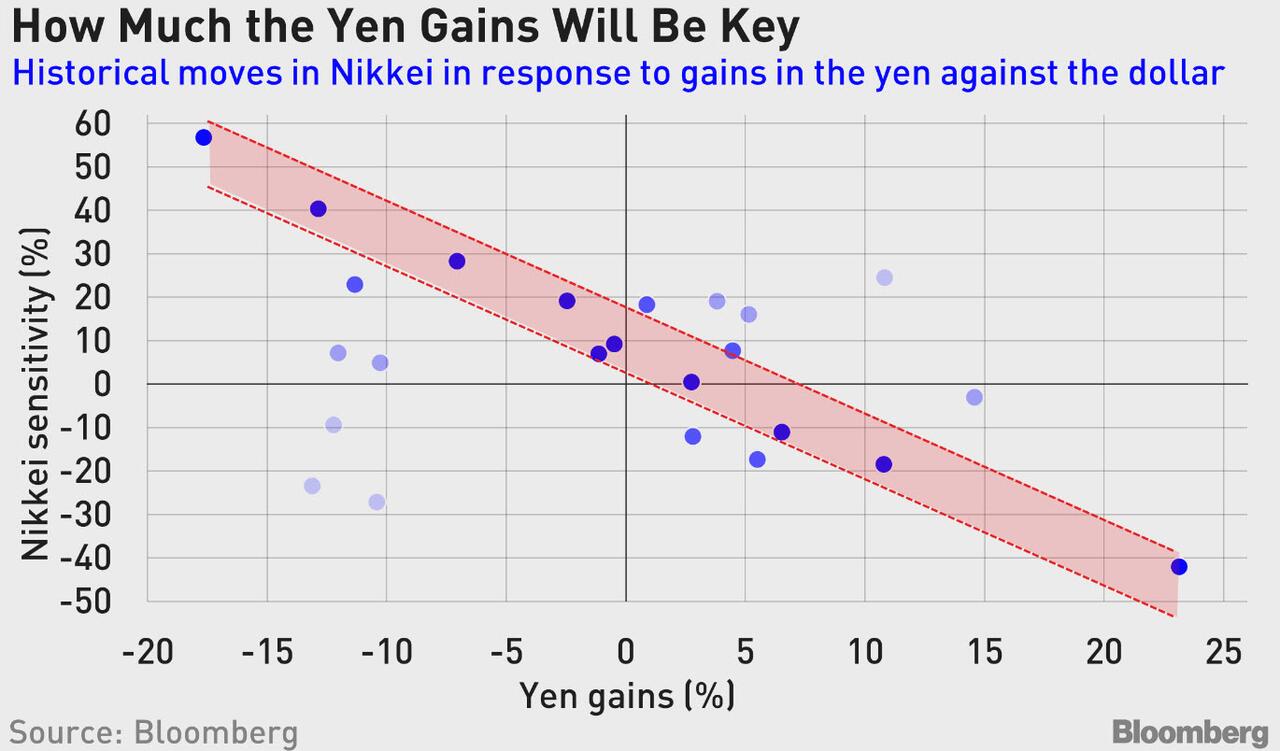

The yen and the Nikkei have generally moved in inverse directions, with the correlation significantly negative.

The analysis suggests that a short-lived gain in the yen would be less punitive for stocks than a currency that stays stronger — meaning a one-off bounce that is quickly reversed will have less of an overall impact.

A key reason for that is that major exporters typically assume a stronger yen level than we have been accustomed to in the past couple of years, shielding them from reporting poorer earnings stemming from fleeting gains in the currency.

The potential for a sustained appreciation in the yen can’t be overstated. Japan’s real effective exchange rate is more than two standard deviations below its historical average, a circumstance so rare as to occur less than 2% of the time.

That suggests the yen has considerable scope to appreciate in the months to come, especially if the Bank of Japan continues to raise interest rates beyond the zero-bound, and inflation in the US mellows sufficiently to allow the US to loosen policy as priced by the markets.

As of Monday, traders were pricing some 25 basis points of tightening from the BOJ this year and about 90 basis points of rate cuts from the Fed.

The median street forecast is for the yen to end the year at 139 per dollar, implying an appreciation of about 6% from current levels.

The Nikkei’s valuations also make the index vulnerable to a correction, independent of the yen. Japanese stocks rank among the worst in global markets given a low return on equity and demanding price-to-cash-flow metrics.

All told, the Nikkei’s stellar run-up over the past two years faces an acid test should the BOJ exit negative rates and spur gains in the yen.

By Ven Ram, Bloomberg markets live reporter and strategist

Japanese stocks can withstand a quick bounce in the yen, but will start to feel the pinch if the currency’s advance goes deeper and becomes more entrenched.

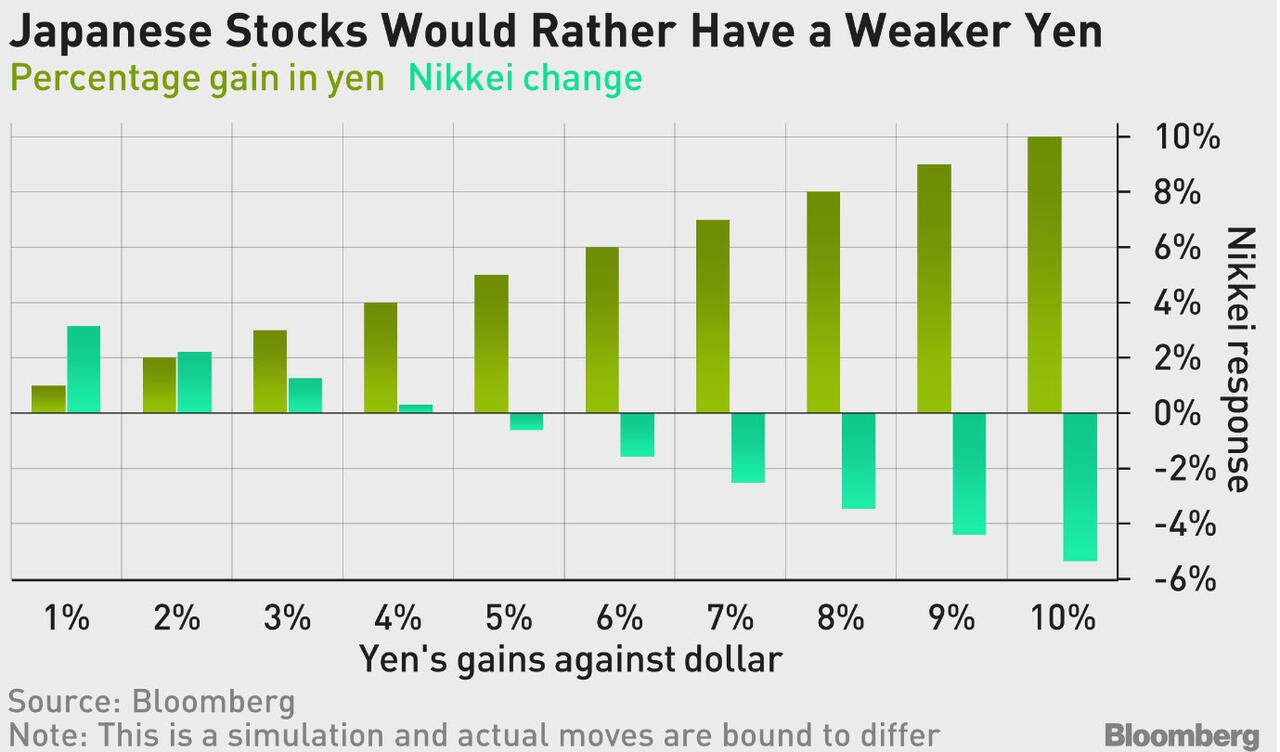

Gains in the Nikkei 225 Index will start slowing if the yen begins to advance sustainably against its major trading partners and in particular the dollar. That could turn into losses should the currency strengthen more than 5% this year.

The following chart shows how a strengthening of the yen against the dollar may affect the Nikkei’s fortunes, based on data going back almost a quarter of a century. The results are similar when the dollar is substituted with a trade-weighted basket of Japan’s major trading partners.

The Nikkei almost doubled in value over the past five years as Deutsche Bank’s trade-weighted yen slumped more than 20% over that period. A weaker yen is a tailwind for Japanese exporters, in particular automobile makers, whose overseas earnings morph into bigger gains after the currency translation.

The yen and the Nikkei have generally moved in inverse directions, with the correlation significantly negative.

The analysis suggests that a short-lived gain in the yen would be less punitive for stocks than a currency that stays stronger — meaning a one-off bounce that is quickly reversed will have less of an overall impact.

A key reason for that is that major exporters typically assume a stronger yen level than we have been accustomed to in the past couple of years, shielding them from reporting poorer earnings stemming from fleeting gains in the currency.

The potential for a sustained appreciation in the yen can’t be overstated. Japan’s real effective exchange rate is more than two standard deviations below its historical average, a circumstance so rare as to occur less than 2% of the time.

That suggests the yen has considerable scope to appreciate in the months to come, especially if the Bank of Japan continues to raise interest rates beyond the zero-bound, and inflation in the US mellows sufficiently to allow the US to loosen policy as priced by the markets.

As of Monday, traders were pricing some 25 basis points of tightening from the BOJ this year and about 90 basis points of rate cuts from the Fed.

The median street forecast is for the yen to end the year at 139 per dollar, implying an appreciation of about 6% from current levels.

The Nikkei’s valuations also make the index vulnerable to a correction, independent of the yen. Japanese stocks rank among the worst in global markets given a low return on equity and demanding price-to-cash-flow metrics.

All told, the Nikkei’s stellar run-up over the past two years faces an acid test should the BOJ exit negative rates and spur gains in the yen.

Loading…