The week after payrolls is usually quieter for data but this week's orientation of the calendar means we have the US CPI print this Thursday as an exception to this rule. And while it's hard to look much beyond this over the next few days, before we preview it, review a payrolls report on Friday that was much weaker under the surface than the headlines, and finally look back on a fascinating first week of the year, let's quickly summarize the rest of the global highlights for the week ahead.

In the US Friday's PPI is the next most important release but we also have consumer credit and the latest NY Fed 1yr inflation expectations survey today and the international trade balance tomorrow. There is a decent list of Fed speakers that you'll see in the week ahead diary at the end. We also have 3, 10 and 30-yr Treasury auctions Tuesday, Wednesday and Thursday which will be interesting given the first set back in bonds in a couple of months.

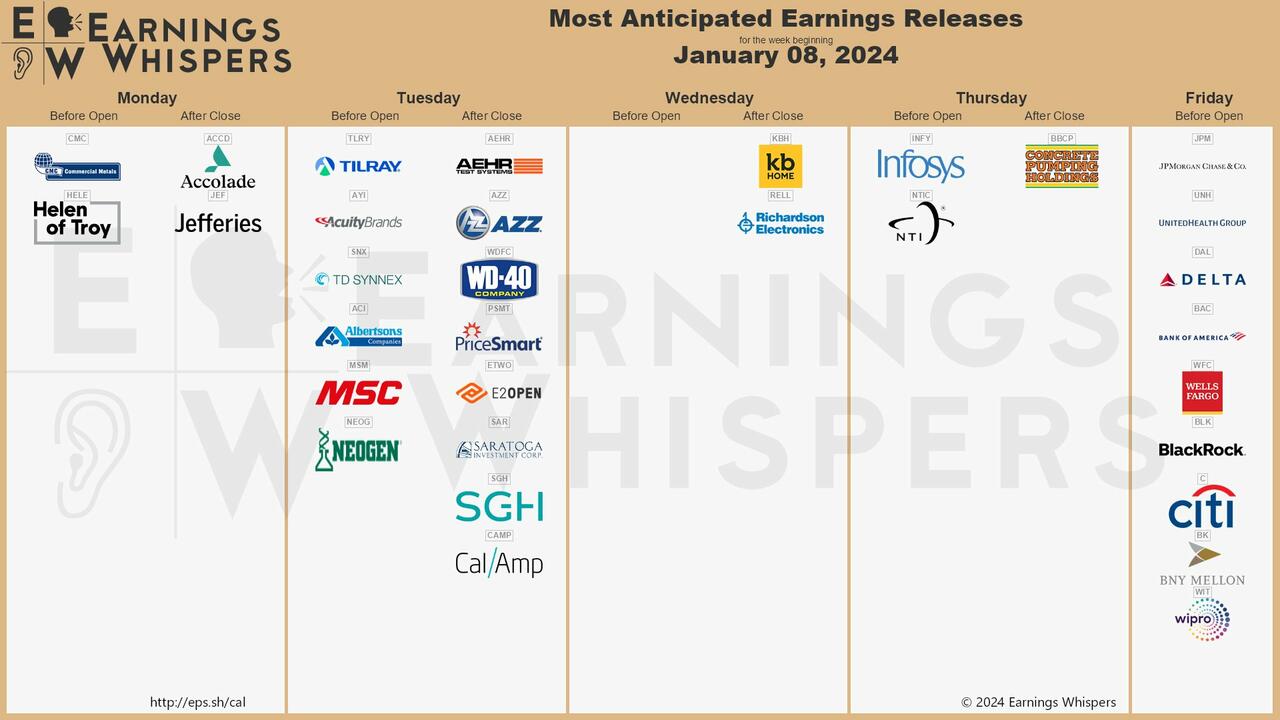

Before we leave the US, note that US earnings season unofficially starts on Friday with the release of several big financials' Q4 results (including JPM, Citi, BoA and Blackrock). Elsewhere, important inflation numbers are also released in China on Friday with the country still battling with deflation. Japanese wages and the Tokyo CPI tomorrow will also be of note.

In Europe it will be relatively quiet with the German trade balance and factory orders today and industrial production tomorrow. At the Eurozone level, there will be a number of sentiment indicators today as well. Otherwise, notable economic data includes industrial production (Thursday) and retail sales in Italy, as well as industrial production in France (both Wednesday). The UK monthly GDP report for November is also out on Friday.

Now onto US CPI on Thursday. We will have a more extended preview later tin the week, but DB's economists expect headline CPI (+0.26% forecast vs. +0.10% previously. Consensus at 0.2%) to come in roughly in line with core (+0.28% vs. +0.28%. Consensus at +0.3%). This would equate to 3.9% and 3.3% YoY, a tenth ahead of consensus. The bank was at 4.0% and 3.1% last month. So core is not yet breaking through 3% on the downside and the 3 and 6m annualised rates are also likely to stay slightly above this mark.

Courtesy of DB, here is a day-by-day calendar of events

Monday January 8

- Data: US November consumer credit, December NY Fed 1-yr inflation expectations, Japan December Tokyo CPI, November household spending, Germany November trade balance, factory orders, Eurozone November retail sales, December services, industrial and economic confidence

- Central banks: Fed's Bostic speaks

- Earnings: Jefferies

Tuesday January 9

- Data: US November trade balance, December NFIB small business optimism, Japan November labour cash earnings, Italy November unemployment rate, Germany November industrial production, France November trade balance, current account balance, Eurozone November unemployment rate, Canada November international merchandise trade, building permits

- Central banks: Fed's Barr speaks, ECB's Villeroy speaks

- Earnings: Samsung, Albertsons

- Auctions: US 3-yr Notes ($52bn)

Wednesday January 10

- Data: US November wholesale trade sales, Italy November retail sales, France November manufacturing production, industrial production

- Central banks: Fed's Williams speaks

- Auctions: US 10-yr Notes (reopening, $37bn)

Thursday January 11

- Data: US December CPI, monthly budget statement, initial jobless claims, Japan November trade balance, current account balance, leading index, coincident index, December bank lending, Italy November industrial production, Germany November current account balance

- Central banks: ECB's Vujcic speaks, ECB's Economic Bulletin

- Auctions: US 30-yr Bond (reopening, $21bn)

Friday January 12

- Data: US December PPI, China December CPI, PPI, trade balance, UK November monthly GDP, trade balance, manufacturing production, industrial production, index of services, construction output, Japan December Economy Watchers survey, France November consumer spending

- Central banks: Fed's Kashkari speaks, ECB's Lane speaks

- Earnings: JPMorgan Chase, BlackRock, Citigroup, Bank of America, Wells Fargo, UnitedHealth, Delta Air Lines

Focusing on just the US, Goldman notes that the key economic data releases this week are the CPI report on Thursday and the PPI report on Friday. There are several speaking engagements by Fed officials this week, including Vice Chair for Supervision Barr and Presidents Bostic, Williams, and Kashkari.

Monday, January 8

- 12:30 PM Atlanta Fed President Bostic (FOMC voter) speaks: Atlanta Fed President Raphael Bostic will speak to the Atlanta Rotary Club about the 2024 economic outlook. A Q&A is expected. On December 19th, Bostic said “inflation is going to come down relatively slowly in the next six months, which means that there's not going to be urgency for us to start to pull off of our restrictive stance."

Tuesday, January 9

- 06:00 AM NFIB Small business optimism, December (consensus 90.8, last 90.6)

- 08:30 AM Trade balance, November (GS -$64.5bn, consensus -$64.8bn, last -$64.3bn)

- 12:00 PM Vice Chair for Supervision Barr speaks: Vice Chair for Supervision Michael Barr will speak on bank regulation at a moderated discussion with Women in Housing and Finance.

Wednesday, January 10

- 08:30 AM Wholesale inventories, November final (consensus -0.2%, last -0.2%)

- 03:15 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will give a speech on the 2024 economic outlook at an event in White Plains, NY hosted by several organizations including the Bronx Economic Development Corporation. Speech text and Q&A are expected. On December 15th, Williams said “we aren't really talking about rate cuts right now, I just think it's just premature to be even thinking about that."

Thursday, January 11

- 08:30 AM CPI (mom), December (GS +0.29%, consensus +0.2%, last +0.1%)

- Core CPI (mom), December (GS +0.27%, consensus +0.3%, last +0.3%)

- CPI (yoy), December (GS +3.30%, consensus +3.2%, last +3.1%)

- Core CPI (yoy), December (GS +3.87%, consensus +3.8%, last +4.0%): We estimate a 0.27% increase in December core CPI (mom sa), which would lower the year-on-year rate by one tenth to 3.9%. Our forecast reflects a 5% rise in airfares (mom sa) offset by declines in auto prices (new -0.2%, used -1.1%) based on the further rebound in incentives and the decline in auction prices. We also assume another decline in apparel prices (-0.3%) on elevated holiday promotionality, and we assume further deceleration in car insurance rates (we assume +0.6%), as premiums have nearly caught up to repair and replacement costs. We forecast a slowdown in shelter categories (we estimate +0.45% for both rent and OER), reflecting the slowdown in rent growth. We estimate a 0.29% rise in headline CPI, reflecting higher energy (+0.4%) and food (+0.4%) prices.

- 08:30 AM Initial jobless claims, week ending January 6 (GS 205k, consensus 210k, last 202k): Continuing claims, week ending December 30 (GS 1,885k, consensus 1,875k, last 1,855k)

Friday, January 12

- 08:30 AM PPI final demand, December (GS +0.1%, consensus +0.1%, last flat); PPI ex-food and energy, December (GS +0.2%, consensus +0.2%, last flat); PPI ex-food, energy, and trade, December (GS +0.2%, consensus +0.2%, last +0.1%)

- 10:00 AM Minneapolis Fed President Kashkari (FOMC non-voter) speaks: Minneapolis Fed President Neel Kashkari will deliver welcoming remarks and participate in a fireside chat at the bank's annual Regional Economic Conditions Conference. On November 6th, Kashkari said “undertightening will not get us back to 2% in a reasonable time… the economy has proven resilient, [but I am concerned about inflation] ticking up again [and] settling somewhere north of 2%, and that would be very concerning to me.”

Source: DB, Goldman, BofA

The week after payrolls is usually quieter for data but this week’s orientation of the calendar means we have the US CPI print this Thursday as an exception to this rule. And while it’s hard to look much beyond this over the next few days, before we preview it, review a payrolls report on Friday that was much weaker under the surface than the headlines, and finally look back on a fascinating first week of the year, let’s quickly summarize the rest of the global highlights for the week ahead.

In the US Friday’s PPI is the next most important release but we also have consumer credit and the latest NY Fed 1yr inflation expectations survey today and the international trade balance tomorrow. There is a decent list of Fed speakers that you’ll see in the week ahead diary at the end. We also have 3, 10 and 30-yr Treasury auctions Tuesday, Wednesday and Thursday which will be interesting given the first set back in bonds in a couple of months.

Before we leave the US, note that US earnings season unofficially starts on Friday with the release of several big financials’ Q4 results (including JPM, Citi, BoA and Blackrock). Elsewhere, important inflation numbers are also released in China on Friday with the country still battling with deflation. Japanese wages and the Tokyo CPI tomorrow will also be of note.

In Europe it will be relatively quiet with the German trade balance and factory orders today and industrial production tomorrow. At the Eurozone level, there will be a number of sentiment indicators today as well. Otherwise, notable economic data includes industrial production (Thursday) and retail sales in Italy, as well as industrial production in France (both Wednesday). The UK monthly GDP report for November is also out on Friday.

Now onto US CPI on Thursday. We will have a more extended preview later tin the week, but DB’s economists expect headline CPI (+0.26% forecast vs. +0.10% previously. Consensus at 0.2%) to come in roughly in line with core (+0.28% vs. +0.28%. Consensus at +0.3%). This would equate to 3.9% and 3.3% YoY, a tenth ahead of consensus. The bank was at 4.0% and 3.1% last month. So core is not yet breaking through 3% on the downside and the 3 and 6m annualised rates are also likely to stay slightly above this mark.

Courtesy of DB, here is a day-by-day calendar of events

Monday January 8

- Data: US November consumer credit, December NY Fed 1-yr inflation expectations, Japan December Tokyo CPI, November household spending, Germany November trade balance, factory orders, Eurozone November retail sales, December services, industrial and economic confidence

- Central banks: Fed’s Bostic speaks

- Earnings: Jefferies

Tuesday January 9

- Data: US November trade balance, December NFIB small business optimism, Japan November labour cash earnings, Italy November unemployment rate, Germany November industrial production, France November trade balance, current account balance, Eurozone November unemployment rate, Canada November international merchandise trade, building permits

- Central banks: Fed’s Barr speaks, ECB’s Villeroy speaks

- Earnings: Samsung, Albertsons

- Auctions: US 3-yr Notes ($52bn)

Wednesday January 10

- Data: US November wholesale trade sales, Italy November retail sales, France November manufacturing production, industrial production

- Central banks: Fed’s Williams speaks

- Auctions: US 10-yr Notes (reopening, $37bn)

Thursday January 11

- Data: US December CPI, monthly budget statement, initial jobless claims, Japan November trade balance, current account balance, leading index, coincident index, December bank lending, Italy November industrial production, Germany November current account balance

- Central banks: ECB’s Vujcic speaks, ECB’s Economic Bulletin

- Auctions: US 30-yr Bond (reopening, $21bn)

Friday January 12

- Data: US December PPI, China December CPI, PPI, trade balance, UK November monthly GDP, trade balance, manufacturing production, industrial production, index of services, construction output, Japan December Economy Watchers survey, France November consumer spending

- Central banks: Fed’s Kashkari speaks, ECB’s Lane speaks

- Earnings: JPMorgan Chase, BlackRock, Citigroup, Bank of America, Wells Fargo, UnitedHealth, Delta Air Lines

Focusing on just the US, Goldman notes that the key economic data releases this week are the CPI report on Thursday and the PPI report on Friday. There are several speaking engagements by Fed officials this week, including Vice Chair for Supervision Barr and Presidents Bostic, Williams, and Kashkari.

Monday, January 8

- 12:30 PM Atlanta Fed President Bostic (FOMC voter) speaks: Atlanta Fed President Raphael Bostic will speak to the Atlanta Rotary Club about the 2024 economic outlook. A Q&A is expected. On December 19th, Bostic said “inflation is going to come down relatively slowly in the next six months, which means that there’s not going to be urgency for us to start to pull off of our restrictive stance.”

Tuesday, January 9

- 06:00 AM NFIB Small business optimism, December (consensus 90.8, last 90.6)

- 08:30 AM Trade balance, November (GS -$64.5bn, consensus -$64.8bn, last -$64.3bn)

- 12:00 PM Vice Chair for Supervision Barr speaks: Vice Chair for Supervision Michael Barr will speak on bank regulation at a moderated discussion with Women in Housing and Finance.

Wednesday, January 10

- 08:30 AM Wholesale inventories, November final (consensus -0.2%, last -0.2%)

- 03:15 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will give a speech on the 2024 economic outlook at an event in White Plains, NY hosted by several organizations including the Bronx Economic Development Corporation. Speech text and Q&A are expected. On December 15th, Williams said “we aren’t really talking about rate cuts right now, I just think it’s just premature to be even thinking about that.”

Thursday, January 11

- 08:30 AM CPI (mom), December (GS +0.29%, consensus +0.2%, last +0.1%)

- Core CPI (mom), December (GS +0.27%, consensus +0.3%, last +0.3%)

- CPI (yoy), December (GS +3.30%, consensus +3.2%, last +3.1%)

- Core CPI (yoy), December (GS +3.87%, consensus +3.8%, last +4.0%): We estimate a 0.27% increase in December core CPI (mom sa), which would lower the year-on-year rate by one tenth to 3.9%. Our forecast reflects a 5% rise in airfares (mom sa) offset by declines in auto prices (new -0.2%, used -1.1%) based on the further rebound in incentives and the decline in auction prices. We also assume another decline in apparel prices (-0.3%) on elevated holiday promotionality, and we assume further deceleration in car insurance rates (we assume +0.6%), as premiums have nearly caught up to repair and replacement costs. We forecast a slowdown in shelter categories (we estimate +0.45% for both rent and OER), reflecting the slowdown in rent growth. We estimate a 0.29% rise in headline CPI, reflecting higher energy (+0.4%) and food (+0.4%) prices.

- 08:30 AM Initial jobless claims, week ending January 6 (GS 205k, consensus 210k, last 202k): Continuing claims, week ending December 30 (GS 1,885k, consensus 1,875k, last 1,855k)

Friday, January 12

- 08:30 AM PPI final demand, December (GS +0.1%, consensus +0.1%, last flat); PPI ex-food and energy, December (GS +0.2%, consensus +0.2%, last flat); PPI ex-food, energy, and trade, December (GS +0.2%, consensus +0.2%, last +0.1%)

- 10:00 AM Minneapolis Fed President Kashkari (FOMC non-voter) speaks: Minneapolis Fed President Neel Kashkari will deliver welcoming remarks and participate in a fireside chat at the bank’s annual Regional Economic Conditions Conference. On November 6th, Kashkari said “undertightening will not get us back to 2% in a reasonable time… the economy has proven resilient, [but I am concerned about inflation] ticking up again [and] settling somewhere north of 2%, and that would be very concerning to me.”

Source: DB, Goldman, BofA

Loading…