Amid a relatively light event calendar, matters in the banking sector will continue to set the pace this week where, as DB's Jim Reid notes this morning, "in an age of social media, misinformation can spread like wildfire so you're never sure where the next incredulous story is going to come from alongside the genuine issues." One can see why Reid - who works for Deutsche Bank - may be somewhat concerned.

To be sure, it's not jost employees: investors in financials have also had their confidence knocked by recent events which has allowed those betting against the sector a free run, although we are seeing a bit of a squeeze this morning. If anything, some rampant fear on Friday morning allowed for an examination of the facts and fundamentals of the large banks and buyers stepped back in with European banks well off the lows by the end of Friday's session with the US bank index turning positive (+0.42%) just before the US close. With the worst of the irrational scare stories around European banks seemingly running out of momentum over the weekend, some reappraisals of the facts should continue this week. Indeed Euro Stoxx futures are up +1.1% in Asia trading with S&P and Nasdaq futures up around +0.5%.

Going back to the week's events, looking forward, the banking sector will clearly again set the scene this week as we approach month-end on Thursday. The data will be a bit secondary as it'll be too early to judge any impact from the mini crisis so far, however as Reid notes, there are some important releases with the PCE in the US (Friday), CPIs for Germany (Thursday), the Eurozone and Tokyo (both Friday) keeping inflation data top of mind for investors this week. They’ll probably care a little less than they did before the banking crisis hit though. In addition, an array of consumer and business confidence indicators in the US and Europe are also due and China PMIs on Friday will be important.

Perhaps more interesting with be hearing from a deluge of Fed officials as they were on blackout for the SVB crisis up until last week's FOMC. They are back in force this week and we'll therefore get a better idea of the deliberations around last week's 25bps hike and the future of this hiking cycle. See the day by day week ahead at the end for a list of the speaker and data highlights.

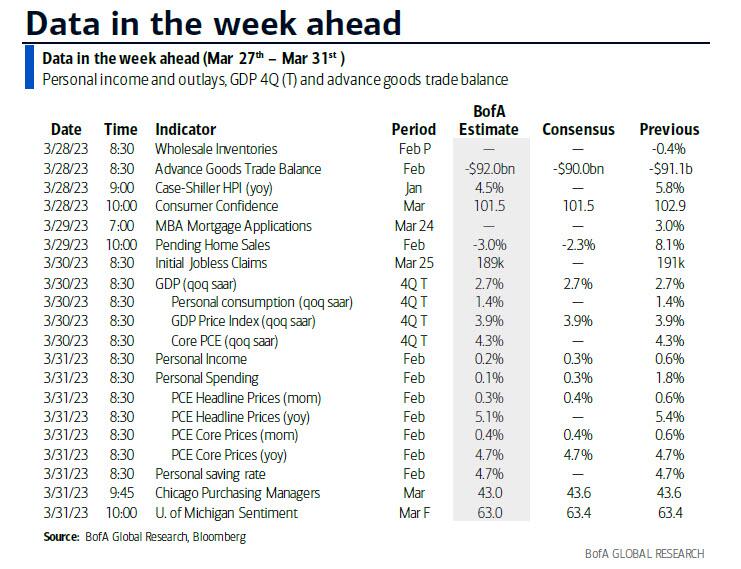

Let's expand on the main events below: we’ll have to wait until the end of the week for the most important datapoint and that’s the Fed's preferred inflation gauge, the PCE, on Friday. DB economists see a +0.36% advance for the core PCE in February (+0.57% in January) and MoM declines for both income (-0.1% vs +0.6% in January) and consumption (-0.6% vs +1.8%). Earlier in the week, a pulse check on the US consumer will come from Conference Board's consumer confidence measure on Wednesday (consensus estimates 101.0 vs 102.9 in February).

Over in Europe, all eyes will be on the preliminary inflation readings across the Eurozone. March data for Germany will be out on Thursday, followed by reports for the Eurozone and France on Friday, among others. In terms of forecasts, DB sees March headline at 7.1% (+1.1% MoM) and core at 5.8% (+1.4% MoM). As a reminder, the latest 5.6% core inflation reading is the highest on record. FWIW, DB's team don't expect it to peak until the 6.0% they expect in July.

Apart from the inflation data, there will be an array of sentiment indicators across the bloc as well, with potential preliminary impact of the banking turmoil in focus. Among the gauges are the Ifo survey (today) and consumer confidence (Wednesday) in Germany, as well as manufacturing (tomorrow) and consumer confidence (Wednesday) in France.

Turning to Asia, this week will be a busy one for Japan as well, with one of the key releases being the Tokyo CPI on Friday. Elsewhere in the region, markets will be closely following China's PMI releases on Friday to assess the speed and magnitude of economic recovery. Current median estimates on Bloomberg are pointing to a slight deceleration in both manufacturing (51.8 vs 52.6 in February) and non-manufacturing (54.3 vs 56.3) indicators.

Courtesy of DB, here is a day-by-day calendar of events

Monday March 27

- Data: US March Dallas Fed manufacturing activity, China February industrial profits, Japan February PPI services, Germany March ifo survey, Eurozone February M3

- Central banks: Fed's Jefferson speaks, ECB's Centeno and Schnabel speak, BoE's Bailey speaks

Tuesday March 28

- Data: US March Conference Board consumer confidence, Richmond Fed manufacturing index, business conditions, Dallas Fed services activity, January FHFA house price index, February wholesale and retail inventories, advance goods trade balance, Italy March manufacturing and consumer confidence, economic sentiment, France March business and manufacturing confidence

- Central banks: BoE's Bailey testifies on Silicon Valley Bank, ECB's Muller speaks

- Earnings: BYD, Micron, Walgreens Boots Alliance, Lululemon

Wednesday March 29

- Data: US February pending home sales, UK February net consumer credit, mortgage approvals, M4, Germany April GfK consumer confidence, France March consumer confidence

- Central banks: ECB's Kazimir speaks, BoE's Mann speaks

- Earnings: CNOOC, China Construction Bank, PetroChina, Kuaishou Technology, Ganfeng Lithium

Thursday March 30

- Data: US initial jobless claims, Germany March CPI, Italy February PPI, unemployment rate, Eurozone March economic, industrial and services confidence Central banks: Fed's Barkin and Collins speak

- Earnings: H&M, Country Garden Holdings, Wynn Macau

Friday March 31

- Data: US March MNI Chicago PMI, February personal spending and income, PCE deflator, China March PMIs, UK March Lloyds business barometer, Q4 current account balance, Japan March Tokyo CPI, February retail sales, job-to-applicant ratio, jobless rate, industrial production, housing starts, department store sales, Italy March CPI, January industrial sales, Germany March unemployment change, February retail sales, import price index, France March CPI, February PPI, consumer spending, Eurozone March CPI, February unemployment rate, Canada January GDP Central banks: ECB's Lagarde and Kazaks speak, Fed's Williams, Waller and Cook speak

A somewhat more detailed day-by-day breakdown courtesy of Rabobank:

Monday: Eurozone M3 money supply figures are due out and the ECB’s Schnabel, Elderson and Centeno are speaking, along with the Bundesbank’s Nagel, BOE Governor Bailey and the Fed’s Jefferson. The challenge of balancing the inflation fight with the financial stability imperative is sure to feature prominently. Expect variations of ‘different tools for different challenges’, which points to the rate hikes + QE/acronyms paradigm that my colleague Michael Every has presaged in this Daily many times.

Tuesday: Australia February retail sales will be released with growth of 0.2% m-o-m expected vs 1.9% in January. Along with the monthly CPI figure due on Wednesday, retail sales is one of the four data points that Phil Lowe said the RBA will be watching closely to inform whether or not the RBA pauses in April. The other two were the February employment numbers and consumer confidence, both of which beat expectations.

- The ECB’s Muller is also speaking and we will hear again from BOE Governor Bailey on the SVB collapse. Over in the USA the Conference Board consumer confidence reading for March will be released (101 expected vs 102.9 prior) and we will also get the Richmond Fed March manufacturing index (-9 expected vs -16 prior). These will be worth keeping an eye on following Neel Kashkari’s comments over the weekend that the banking turmoil “definitely brings us closer” to the possibility of a US recession.

Wednesday: This ought to be key day of the week. In Australia February monthly CPI figures already mentioned are due out. Expectations are for a y-o-y read of 7.2% vs. 7.4% in January. Crucially, this data does not include the RBA’s preferred trimmed-mean measure. So, while it will be important, it may not be decisive.

- UK mortgage approvals numbers will also land. Surveyed economists expect 42,000 vs 39,600 in January. We will also hear from the BOE’s Catherine Mann and the ECB’s Isabel Schnabel (again) before the real highlight of the week, which should be the Fed’s Michael Barr appearing before the House Financial Services panel. Expect a post mortem on SVB and some thoughts on how financial stability may be improved into the future.

- The US Department of Energy also release updated fuel inventory figures. This could be an important number in the context of the almost 14% drop in crude prices since March 6, and comments from Energy Secretary Granholm on Thursday that it could take years to refill the USA’s strategic reserves.

Thursday: promises to be more sedate. Key releases are the New Zealand February building permits and business confidence numbers. No survey expectations are published for either, by both will be important inputs for the RBNZ’s thinking on the future path of the OCR.

- Later in the day US weekly jobless claims are expected to lift slightly to 196,000 and we will get the third reading of US Q4 GDP (2.7% expected).

Friday: will be an important day for Eurozone data. Preliminary March CPI is expected to lift to 1.1% m-o-m after coming in at 0.8% in February. On a y-o-y basis the headline number is expected to fall from 8.5% to 7.1% as March 2022 rolls off while the core reading is expected to lift by 1 tick to 5.7% y-o-y. We also get Eurozone unemployment figures where surveyed analysts expect the rate to fall 1 tick to 6.6%.

- Finally, China March PMIs also land. Expansion in manufacturing is seen slowing from 52.6 to 51.7 while the non-manufacturing sector’s breakneck expansion set off by China’s reopening is seen slowing from 56.3 to a still very healthy 54.9.

* * *

Finally, looking at just the US, Goldman writes that the key economic data release this week is the core PCE report on Friday. There are several speaking engagements from Fed officials this week, including congressional testimony by Vice Chair for Supervision Michael Barr on Tuesday and Wednesday and speeches by New York Fed President Williams and Fed Governor Waller on Friday.

Monday, March 27

- 10:30 AM Dallas Fed manufacturing index, March (consensus -10, last -13.5)

- 05:00 PM Fed Governor Jefferson speaks: Fed Governor Philip Jefferson will discuss the transmission and implementation of monetary policy at an event at Washington and Lee University in Virginia. Text and audience Q&A are expected. In a speech on February 24th, before the recent turmoil in the banking system, Governor Jefferson noted that “labor compensation has started to decelerate somewhat over the past year but is still running too high to be consistent with returning inflation to 2 percent in a timely and sustainable fashion.” Governor Jefferson also stressed that a key difference between the current inflationary episode and the Great Inflation of the late 1960s and 1970s was that the Fed was now “addressing the outbreak in inflation promptly and forcefully to maintain credibility and to preserve the "well anchored" property of long-term inflation expectations.”

Tuesday, March 28

- 08:30 AM Wholesale inventories, February preliminary (last -0.4%); Retail inventories, February (last +0.3%)

- 08:30 AM Advance goods trade balance, February (GS -$89.0bn, consensus -$90.0bn, last -$91.5bn); We estimate that the goods trade deficit narrowed by $2.5bn to $89.0bn in February compared to the final January report.

- 09:00 AM FHFA house price index, January (last -0.1%)

- 09:00 AM S&P/Case-Shiller 20-city home price index, January (GS -0.4%, consensus -0.5%, last -0.5%): We estimate that the S&P/Case-Shiller 20-city home price index declined 0.4% in January, following a 0.5% decline in December.

- 10:00 AM Conference Board consumer confidence, March (GS 101.5, consensus 101.5, last 102.9); We estimate that the Conference Board consumer confidence index decreased to 101.5 in March.

- 10:00 AM Richmond Fed manufacturing index, March (consensus -8, last -16)

- 10:00 AM Fed Vice Chair for Supervision Barr speaks: Fed Vice Chair for Supervision Michael Barr will testify before the Senate Banking Committee. On March 13th, the Fed announced that Vice Chair Barr was leading a review of the supervision and regulation of SVB following its failure. Vice Chair Barr stated that the Fed needs to have “humility and conduct a careful and thorough review of how we supervised and regulated this firm, and what we should learn from this experience.”

Wednesday, March 29

- 10:00 AM Pending home sales, February (GS +3.0%, consensus -3.0%, last +8.1%); We estimate pending home sales increased 3.0% in February, following an 8.1% increase in January.

- 10:00 AM Fed Vice Chair for Supervision Barr speaks: Fed Vice Chair for Supervision Michael Barr will testify before the House Financial Services Committee.

Thursday, March 30

- 08:30 AM Initial jobless claims, week ended March 25 (GS 190k, consensus 195k, last 191k); Continuing jobless claims, week ended March 18 (consensus 1,697k, last 1,694k); We estimate that initial jobless claims edged down to 190k in the week ended March 25.

- 08:30 AM GDP (third), Q4 (GS +2.7%, consensus +2.7%, last +2.7%); Personal consumption, Q4 (GS +1.4%, consensus +1.5%, last +1.4%): We estimate no revision on net in the third vintage of the Q4 GDP report (previously reported at +2.7% qoq ar).

- 12:30 PM Richmond Fed President Barkin (FOMC non-voter) speaks: Richmond Fed President Thomas Barkin will speak at an event hosted by the Virginia Council of CEOs at the University of Richmond. Text and audience Q&A are expected. In an interview with CNN on March 24th, President Barkin stressed that “the case for raising [the federal funds rate by 25bp at the FOMC’s March meeting] was pretty clear,” because “inflation is high” and “demand hadn’t seemed to come down.” President Barkin also noted that the situation in the banking system “felt very stable” by the time the FOMC met.

- 12:45 PM Boston Fed President Collins (FOMC non-voter) speaks: Boston Fed President Susan Collins will deliver a speech at the annual NABE conference in Washington. Text and moderated Q&A are expected. On February 24th, before the recent stress in the banking system, President Collins argued that “now that policy is in restrictive territory, the process of realigning demand with supply is underway.”

Friday, March 31

- 08:30 AM Personal income, February (GS +0.4%, consensus +0.2%, last +0.6%); Personal spending, February (GS +0.2%, consensus +0.3%, last +1.8%); PCE price index, February (GS +0.30%, consensus +0.3%, last +0.6%); Core PCE price index, February (GS +0.34%, consensus +0.4%, last +0.6%): Based on details in the PPI, CPI, and import price reports, we forecast that the core PCE price index rose by 0.34% month-over-month in February, corresponding to a 4.67% increase from a year earlier. Additionally, we expect that the headline PCE price index increased by 0.30% in February, corresponding to a 5.07% increase from a year earlier. We expect that personal income increased by 0.4% and personal spending increased by 0.2% in February.

- 09:45 AM Chicago PMI, March (GS 41.6, consensus 43.9, last 43.6): We estimate that the Chicago PMI declined by 2pt to 41.6 in March, reflecting the lackluster rebound in East Asian manufacturing activity and a possible sentiment drag from US banking stress.

- 10:00 AM University of Michigan consumer sentiment, March final (GS 63.0, consensus 63.4, last 63.4); University of Michigan 5–10-year inflation expectations, March final (GS 2.8%, consensus 2.8%, last 2.8%): We expect the University of Michigan consumer sentiment index to decline by 0.4pt to 63.0 and expect the report’s measure of 5-10 year inflation expectations to remain unchanged in the final March reading.

- 03:00 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will deliver a speech on monetary policy and the economic outlook at Housatonic Community College in Connecticut. Text and moderated Q&A are expected. On February 14th, President Williams noted that “we have yet to see the gears turn for inflation of non-energy services excluding housing, which is still quite elevated, averaging 3-3/4 percent over the most recent six months.” President Williams said he expected “real GDP growth to come in around 1 percent for 2023” and the unemployment rate “to edge up over the next year to between 4 and 4½ percent.” His comments predated the recent turmoil in the banking system.

- 04:00 PM Fed Governor Waller speaks: Fed Governor Christopher Waller will deliver a speech titled “The Unstable Phillips Curve” at a conference hosted by the San Francisco Fed. Text is expected. On March 2nd, Governor Waller noted that the recent data had challenged his view “that the FOMC was making significant progress in … reducing inflation.”

- 05:45 PM Fed Governor Cook speaks: Fed Governor Lisa Cook will deliver a speech on the US economy and monetary policy to the Midwest Economics Association in Cleveland, Ohio. Text is expected. In a speech delivered on January 6th, Governor Cook noted that the inflation outlook for core non-housing services “partly depends on whether growth in nominal labor costs comes back down, and recent data suggest that labor-compensation growth has indeed started to decelerate somewhat over the past year.”

Source: DB, Goldman, Rabobank, BofA

Amid a relatively light event calendar, matters in the banking sector will continue to set the pace this week where, as DB’s Jim Reid notes this morning, “in an age of social media, misinformation can spread like wildfire so you’re never sure where the next incredulous story is going to come from alongside the genuine issues.” One can see why Reid – who works for Deutsche Bank – may be somewhat concerned.

To be sure, it’s not jost employees: investors in financials have also had their confidence knocked by recent events which has allowed those betting against the sector a free run, although we are seeing a bit of a squeeze this morning. If anything, some rampant fear on Friday morning allowed for an examination of the facts and fundamentals of the large banks and buyers stepped back in with European banks well off the lows by the end of Friday’s session with the US bank index turning positive (+0.42%) just before the US close. With the worst of the irrational scare stories around European banks seemingly running out of momentum over the weekend, some reappraisals of the facts should continue this week. Indeed Euro Stoxx futures are up +1.1% in Asia trading with S&P and Nasdaq futures up around +0.5%.

Going back to the week’s events, looking forward, the banking sector will clearly again set the scene this week as we approach month-end on Thursday. The data will be a bit secondary as it’ll be too early to judge any impact from the mini crisis so far, however as Reid notes, there are some important releases with the PCE in the US (Friday), CPIs for Germany (Thursday), the Eurozone and Tokyo (both Friday) keeping inflation data top of mind for investors this week. They’ll probably care a little less than they did before the banking crisis hit though. In addition, an array of consumer and business confidence indicators in the US and Europe are also due and China PMIs on Friday will be important.

Perhaps more interesting with be hearing from a deluge of Fed officials as they were on blackout for the SVB crisis up until last week’s FOMC. They are back in force this week and we’ll therefore get a better idea of the deliberations around last week’s 25bps hike and the future of this hiking cycle. See the day by day week ahead at the end for a list of the speaker and data highlights.

Let’s expand on the main events below: we’ll have to wait until the end of the week for the most important datapoint and that’s the Fed’s preferred inflation gauge, the PCE, on Friday. DB economists see a +0.36% advance for the core PCE in February (+0.57% in January) and MoM declines for both income (-0.1% vs +0.6% in January) and consumption (-0.6% vs +1.8%). Earlier in the week, a pulse check on the US consumer will come from Conference Board’s consumer confidence measure on Wednesday (consensus estimates 101.0 vs 102.9 in February).

Over in Europe, all eyes will be on the preliminary inflation readings across the Eurozone. March data for Germany will be out on Thursday, followed by reports for the Eurozone and France on Friday, among others. In terms of forecasts, DB sees March headline at 7.1% (+1.1% MoM) and core at 5.8% (+1.4% MoM). As a reminder, the latest 5.6% core inflation reading is the highest on record. FWIW, DB’s team don’t expect it to peak until the 6.0% they expect in July.

Apart from the inflation data, there will be an array of sentiment indicators across the bloc as well, with potential preliminary impact of the banking turmoil in focus. Among the gauges are the Ifo survey (today) and consumer confidence (Wednesday) in Germany, as well as manufacturing (tomorrow) and consumer confidence (Wednesday) in France.

Turning to Asia, this week will be a busy one for Japan as well, with one of the key releases being the Tokyo CPI on Friday. Elsewhere in the region, markets will be closely following China’s PMI releases on Friday to assess the speed and magnitude of economic recovery. Current median estimates on Bloomberg are pointing to a slight deceleration in both manufacturing (51.8 vs 52.6 in February) and non-manufacturing (54.3 vs 56.3) indicators.

Courtesy of DB, here is a day-by-day calendar of events

Monday March 27

- Data: US March Dallas Fed manufacturing activity, China February industrial profits, Japan February PPI services, Germany March ifo survey, Eurozone February M3

- Central banks: Fed’s Jefferson speaks, ECB’s Centeno and Schnabel speak, BoE’s Bailey speaks

Tuesday March 28

- Data: US March Conference Board consumer confidence, Richmond Fed manufacturing index, business conditions, Dallas Fed services activity, January FHFA house price index, February wholesale and retail inventories, advance goods trade balance, Italy March manufacturing and consumer confidence, economic sentiment, France March business and manufacturing confidence

- Central banks: BoE’s Bailey testifies on Silicon Valley Bank, ECB’s Muller speaks

- Earnings: BYD, Micron, Walgreens Boots Alliance, Lululemon

Wednesday March 29

- Data: US February pending home sales, UK February net consumer credit, mortgage approvals, M4, Germany April GfK consumer confidence, France March consumer confidence

- Central banks: ECB’s Kazimir speaks, BoE’s Mann speaks

- Earnings: CNOOC, China Construction Bank, PetroChina, Kuaishou Technology, Ganfeng Lithium

Thursday March 30

- Data: US initial jobless claims, Germany March CPI, Italy February PPI, unemployment rate, Eurozone March economic, industrial and services confidence Central banks: Fed’s Barkin and Collins speak

- Earnings: H&M, Country Garden Holdings, Wynn Macau

Friday March 31

- Data: US March MNI Chicago PMI, February personal spending and income, PCE deflator, China March PMIs, UK March Lloyds business barometer, Q4 current account balance, Japan March Tokyo CPI, February retail sales, job-to-applicant ratio, jobless rate, industrial production, housing starts, department store sales, Italy March CPI, January industrial sales, Germany March unemployment change, February retail sales, import price index, France March CPI, February PPI, consumer spending, Eurozone March CPI, February unemployment rate, Canada January GDP Central banks: ECB’s Lagarde and Kazaks speak, Fed’s Williams, Waller and Cook speak

A somewhat more detailed day-by-day breakdown courtesy of Rabobank:

Monday: Eurozone M3 money supply figures are due out and the ECB’s Schnabel, Elderson and Centeno are speaking, along with the Bundesbank’s Nagel, BOE Governor Bailey and the Fed’s Jefferson. The challenge of balancing the inflation fight with the financial stability imperative is sure to feature prominently. Expect variations of ‘different tools for different challenges’, which points to the rate hikes + QE/acronyms paradigm that my colleague Michael Every has presaged in this Daily many times.

Tuesday: Australia February retail sales will be released with growth of 0.2% m-o-m expected vs 1.9% in January. Along with the monthly CPI figure due on Wednesday, retail sales is one of the four data points that Phil Lowe said the RBA will be watching closely to inform whether or not the RBA pauses in April. The other two were the February employment numbers and consumer confidence, both of which beat expectations.

- The ECB’s Muller is also speaking and we will hear again from BOE Governor Bailey on the SVB collapse. Over in the USA the Conference Board consumer confidence reading for March will be released (101 expected vs 102.9 prior) and we will also get the Richmond Fed March manufacturing index (-9 expected vs -16 prior). These will be worth keeping an eye on following Neel Kashkari’s comments over the weekend that the banking turmoil “definitely brings us closer” to the possibility of a US recession.

Wednesday: This ought to be key day of the week. In Australia February monthly CPI figures already mentioned are due out. Expectations are for a y-o-y read of 7.2% vs. 7.4% in January. Crucially, this data does not include the RBA’s preferred trimmed-mean measure. So, while it will be important, it may not be decisive.

- UK mortgage approvals numbers will also land. Surveyed economists expect 42,000 vs 39,600 in January. We will also hear from the BOE’s Catherine Mann and the ECB’s Isabel Schnabel (again) before the real highlight of the week, which should be the Fed’s Michael Barr appearing before the House Financial Services panel. Expect a post mortem on SVB and some thoughts on how financial stability may be improved into the future.

- The US Department of Energy also release updated fuel inventory figures. This could be an important number in the context of the almost 14% drop in crude prices since March 6, and comments from Energy Secretary Granholm on Thursday that it could take years to refill the USA’s strategic reserves.

Thursday: promises to be more sedate. Key releases are the New Zealand February building permits and business confidence numbers. No survey expectations are published for either, by both will be important inputs for the RBNZ’s thinking on the future path of the OCR.

- Later in the day US weekly jobless claims are expected to lift slightly to 196,000 and we will get the third reading of US Q4 GDP (2.7% expected).

Friday: will be an important day for Eurozone data. Preliminary March CPI is expected to lift to 1.1% m-o-m after coming in at 0.8% in February. On a y-o-y basis the headline number is expected to fall from 8.5% to 7.1% as March 2022 rolls off while the core reading is expected to lift by 1 tick to 5.7% y-o-y. We also get Eurozone unemployment figures where surveyed analysts expect the rate to fall 1 tick to 6.6%.

- Finally, China March PMIs also land. Expansion in manufacturing is seen slowing from 52.6 to 51.7 while the non-manufacturing sector’s breakneck expansion set off by China’s reopening is seen slowing from 56.3 to a still very healthy 54.9.

* * *

Finally, looking at just the US, Goldman writes that the key economic data release this week is the core PCE report on Friday. There are several speaking engagements from Fed officials this week, including congressional testimony by Vice Chair for Supervision Michael Barr on Tuesday and Wednesday and speeches by New York Fed President Williams and Fed Governor Waller on Friday.

Monday, March 27

- 10:30 AM Dallas Fed manufacturing index, March (consensus -10, last -13.5)

- 05:00 PM Fed Governor Jefferson speaks: Fed Governor Philip Jefferson will discuss the transmission and implementation of monetary policy at an event at Washington and Lee University in Virginia. Text and audience Q&A are expected. In a speech on February 24th, before the recent turmoil in the banking system, Governor Jefferson noted that “labor compensation has started to decelerate somewhat over the past year but is still running too high to be consistent with returning inflation to 2 percent in a timely and sustainable fashion.” Governor Jefferson also stressed that a key difference between the current inflationary episode and the Great Inflation of the late 1960s and 1970s was that the Fed was now “addressing the outbreak in inflation promptly and forcefully to maintain credibility and to preserve the “well anchored” property of long-term inflation expectations.”

Tuesday, March 28

- 08:30 AM Wholesale inventories, February preliminary (last -0.4%); Retail inventories, February (last +0.3%)

- 08:30 AM Advance goods trade balance, February (GS -$89.0bn, consensus -$90.0bn, last -$91.5bn); We estimate that the goods trade deficit narrowed by $2.5bn to $89.0bn in February compared to the final January report.

- 09:00 AM FHFA house price index, January (last -0.1%)

- 09:00 AM S&P/Case-Shiller 20-city home price index, January (GS -0.4%, consensus -0.5%, last -0.5%): We estimate that the S&P/Case-Shiller 20-city home price index declined 0.4% in January, following a 0.5% decline in December.

- 10:00 AM Conference Board consumer confidence, March (GS 101.5, consensus 101.5, last 102.9); We estimate that the Conference Board consumer confidence index decreased to 101.5 in March.

- 10:00 AM Richmond Fed manufacturing index, March (consensus -8, last -16)

- 10:00 AM Fed Vice Chair for Supervision Barr speaks: Fed Vice Chair for Supervision Michael Barr will testify before the Senate Banking Committee. On March 13th, the Fed announced that Vice Chair Barr was leading a review of the supervision and regulation of SVB following its failure. Vice Chair Barr stated that the Fed needs to have “humility and conduct a careful and thorough review of how we supervised and regulated this firm, and what we should learn from this experience.”

Wednesday, March 29

- 10:00 AM Pending home sales, February (GS +3.0%, consensus -3.0%, last +8.1%); We estimate pending home sales increased 3.0% in February, following an 8.1% increase in January.

- 10:00 AM Fed Vice Chair for Supervision Barr speaks: Fed Vice Chair for Supervision Michael Barr will testify before the House Financial Services Committee.

Thursday, March 30

- 08:30 AM Initial jobless claims, week ended March 25 (GS 190k, consensus 195k, last 191k); Continuing jobless claims, week ended March 18 (consensus 1,697k, last 1,694k); We estimate that initial jobless claims edged down to 190k in the week ended March 25.

- 08:30 AM GDP (third), Q4 (GS +2.7%, consensus +2.7%, last +2.7%); Personal consumption, Q4 (GS +1.4%, consensus +1.5%, last +1.4%): We estimate no revision on net in the third vintage of the Q4 GDP report (previously reported at +2.7% qoq ar).

- 12:30 PM Richmond Fed President Barkin (FOMC non-voter) speaks: Richmond Fed President Thomas Barkin will speak at an event hosted by the Virginia Council of CEOs at the University of Richmond. Text and audience Q&A are expected. In an interview with CNN on March 24th, President Barkin stressed that “the case for raising [the federal funds rate by 25bp at the FOMC’s March meeting] was pretty clear,” because “inflation is high” and “demand hadn’t seemed to come down.” President Barkin also noted that the situation in the banking system “felt very stable” by the time the FOMC met.

- 12:45 PM Boston Fed President Collins (FOMC non-voter) speaks: Boston Fed President Susan Collins will deliver a speech at the annual NABE conference in Washington. Text and moderated Q&A are expected. On February 24th, before the recent stress in the banking system, President Collins argued that “now that policy is in restrictive territory, the process of realigning demand with supply is underway.”

Friday, March 31

- 08:30 AM Personal income, February (GS +0.4%, consensus +0.2%, last +0.6%); Personal spending, February (GS +0.2%, consensus +0.3%, last +1.8%); PCE price index, February (GS +0.30%, consensus +0.3%, last +0.6%); Core PCE price index, February (GS +0.34%, consensus +0.4%, last +0.6%): Based on details in the PPI, CPI, and import price reports, we forecast that the core PCE price index rose by 0.34% month-over-month in February, corresponding to a 4.67% increase from a year earlier. Additionally, we expect that the headline PCE price index increased by 0.30% in February, corresponding to a 5.07% increase from a year earlier. We expect that personal income increased by 0.4% and personal spending increased by 0.2% in February.

- 09:45 AM Chicago PMI, March (GS 41.6, consensus 43.9, last 43.6): We estimate that the Chicago PMI declined by 2pt to 41.6 in March, reflecting the lackluster rebound in East Asian manufacturing activity and a possible sentiment drag from US banking stress.

- 10:00 AM University of Michigan consumer sentiment, March final (GS 63.0, consensus 63.4, last 63.4); University of Michigan 5–10-year inflation expectations, March final (GS 2.8%, consensus 2.8%, last 2.8%): We expect the University of Michigan consumer sentiment index to decline by 0.4pt to 63.0 and expect the report’s measure of 5-10 year inflation expectations to remain unchanged in the final March reading.

- 03:00 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will deliver a speech on monetary policy and the economic outlook at Housatonic Community College in Connecticut. Text and moderated Q&A are expected. On February 14th, President Williams noted that “we have yet to see the gears turn for inflation of non-energy services excluding housing, which is still quite elevated, averaging 3-3/4 percent over the most recent six months.” President Williams said he expected “real GDP growth to come in around 1 percent for 2023” and the unemployment rate “to edge up over the next year to between 4 and 4½ percent.” His comments predated the recent turmoil in the banking system.

- 04:00 PM Fed Governor Waller speaks: Fed Governor Christopher Waller will deliver a speech titled “The Unstable Phillips Curve” at a conference hosted by the San Francisco Fed. Text is expected. On March 2nd, Governor Waller noted that the recent data had challenged his view “that the FOMC was making significant progress in … reducing inflation.”

- 05:45 PM Fed Governor Cook speaks: Fed Governor Lisa Cook will deliver a speech on the US economy and monetary policy to the Midwest Economics Association in Cleveland, Ohio. Text is expected. In a speech delivered on January 6th, Governor Cook noted that the inflation outlook for core non-housing services “partly depends on whether growth in nominal labor costs comes back down, and recent data suggest that labor-compensation growth has indeed started to decelerate somewhat over the past year.”

Source: DB, Goldman, Rabobank, BofA

Loading…