After the unexpected rise in September, expectations were for October's Manufacturing surveys to hold their gains around 49-50 level - despite the recent collapse in 'hard' macro data.

Sure enough, S&P Global's US Manufacturing PMI printed 50.0 final for October (in line with the flash print and expectations and up slightly from September's 49.8). But, ISM's Manufacturing survey printed well below expectations (46.7 vs 49.0 exp vs 49.0 exp)...

Source: Bloomberg

The PMI survey highlighted that demand conditions were historically muted overall, with firms downwardly adjusting their output expectations for the year ahead and cutting employment for the first time since July 2020.

ISM warns that "the October reading (46.7 percent) corresponds to a change of minus -0.7 percent in real gross domestic product (GDP) on an annualized basis."

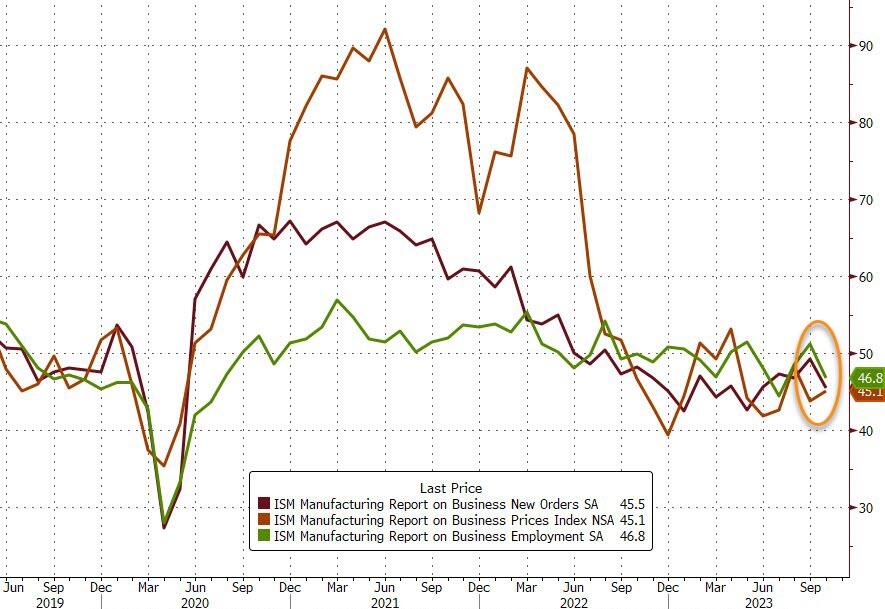

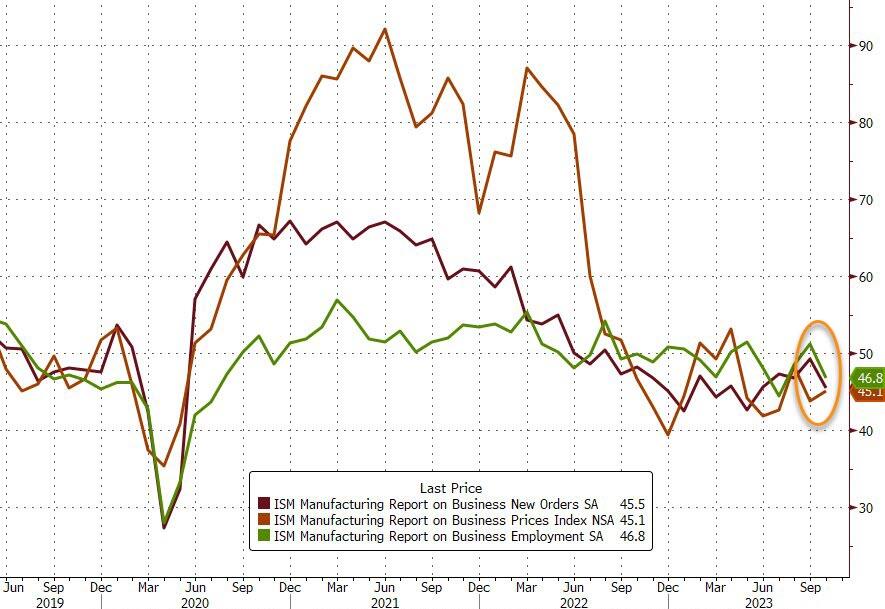

New orders and employment fell (second weakest since COVID lockdowns) as prices rose...

Siân Jones, Principal Economist at S&P Global Market Intelligence, said:

"October PMI data signalled a stabilisation of US manufacturing conditions amid a renewed rise in new order inflows and firmer output growth. Demand conditions reportedly showed signs of improvement as customer interest revived, but this was once again largely focused on the domestic market as new export orders fell at a quicker rate.

However, it was not all good news at all - backlogs down, jobs down, output expectations down, inflation up:

"Of concern were reports of dwindling backlogs of work, previously used to help support production, as firms also revised down their expectations for future output to the lowest in 2023 so far."

"At the same time, manufacturers cut employment for the first time in over three years as workloads were reportedly insufficient to warrant additional hiring or the replacement of voluntary leavers. "

"On the price front, manufacturers saw sharper increases in costs and output charges, as inflation regained some momentum in the sector. Higher oil and oil-derived input prices again spurred hikes, as rates of inflation accelerated for the third month running."

Finally, we note that, with a 6-month lag or so, US Manufacturing surveys have been following the path of financial conditions. Six months after financial conditions began to ease late last year, US Manufacturing surveys started to pick up...

Source: Bloomberg

...but as the chart shows, the recent aggressive tightening of financial conditions suggest the sentiment surveys are about to run out of their upside steam.

Will that slower growth be accompanied by slowing inflation? For now, inflation expectations are on the rise once again...

After the unexpected rise in September, expectations were for October’s Manufacturing surveys to hold their gains around 49-50 level – despite the recent collapse in ‘hard’ macro data.

Sure enough, S&P Global’s US Manufacturing PMI printed 50.0 final for October (in line with the flash print and expectations and up slightly from September’s 49.8). But, ISM’s Manufacturing survey printed well below expectations (46.7 vs 49.0 exp vs 49.0 exp)…

Source: Bloomberg

The PMI survey highlighted that demand conditions were historically muted overall, with firms downwardly adjusting their output expectations for the year ahead and cutting employment for the first time since July 2020.

ISM warns that “the October reading (46.7 percent) corresponds to a change of minus -0.7 percent in real gross domestic product (GDP) on an annualized basis.”

New orders and employment fell (second weakest since COVID lockdowns) as prices rose…

Siân Jones, Principal Economist at S&P Global Market Intelligence, said:

“October PMI data signalled a stabilisation of US manufacturing conditions amid a renewed rise in new order inflows and firmer output growth. Demand conditions reportedly showed signs of improvement as customer interest revived, but this was once again largely focused on the domestic market as new export orders fell at a quicker rate.

However, it was not all good news at all – backlogs down, jobs down, output expectations down, inflation up:

“Of concern were reports of dwindling backlogs of work, previously used to help support production, as firms also revised down their expectations for future output to the lowest in 2023 so far.”

“At the same time, manufacturers cut employment for the first time in over three years as workloads were reportedly insufficient to warrant additional hiring or the replacement of voluntary leavers. “

“On the price front, manufacturers saw sharper increases in costs and output charges, as inflation regained some momentum in the sector. Higher oil and oil-derived input prices again spurred hikes, as rates of inflation accelerated for the third month running.“

Finally, we note that, with a 6-month lag or so, US Manufacturing surveys have been following the path of financial conditions. Six months after financial conditions began to ease late last year, US Manufacturing surveys started to pick up…

Source: Bloomberg

…but as the chart shows, the recent aggressive tightening of financial conditions suggest the sentiment surveys are about to run out of their upside steam.

Will that slower growth be accompanied by slowing inflation? For now, inflation expectations are on the rise once again…

Loading…