By Stephen Byrd, Head of North American Equity Research, Power/Utilities and Clean Tech at Morgan Stanley

Debate among investors is growing about whether to focus on stocks which are ESG ‘enablers’ with best-in-class ESG metrics, or on ‘ESG improvers’. We see merit in both approaches but believe the benefits of owning ‘ESG rate of change’ stocks and engaging with companies in transition are underappreciated. In a recent report, Morgan Stanley's Sustainability Research team, in collaboration with industry analysts, our Quantitative Investment Strategies (QIS) team, and AlphaWise, show that focusing on names with improving ESG metrics can deliver both alpha and positive ESG impacts.

Our work is distinctive on multiple fronts. First, in collaboration with our analysts, we developed a forward-looking framework to analyze ESG rate of change at the stock level. We think it provides a better gauge of the likely future rate of change than typical data services, which are often backward looking and/or not informed by in-depth, sector-specific analyses. In addition, our analysts focused on companies with an opportunity to improve their financial performance thanks to ESG rate of change, a key difference from typical ESG analyses.

From a quant perspective, our QIS team assessed the impact on stock returns of ESG criteria such as carbon efficiency, exclusions driven by environmental harm, percentages of revenues linked to fossil fuels, and non-climate ESG concerns. The team found little evidence of a significant positive or negative effect on performance from screening on such broad ESG criteria. This underscores the need to marry ESG capabilities with strong sector expertise in order to generate alpha, tailoring ESG criteria and strategies to industry dynamics. We developed a robust set of sector-specific ESG rate of change criteria.

We were surprised how often deflationary technologies are driving simultaneous improvement in both ESG and financial metrics. An usually broad range of innovations are dropping in cost so much that they offer significant net benefits on both fronts. These include solar/wind/clean hydrogen, green ammonia, precision agriculture, improved molecular plastics recycling technology, more efficient electric motors, energy storage cost reductions, ‘green steel’, more durable vehicle tires, recycling technologies, electrification of many products/industrial processes, carbon capture tech, and waste-to-energy/waste-to-plastics technologies.

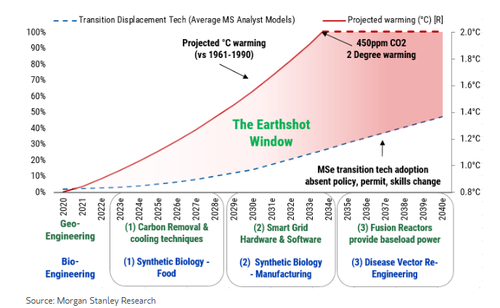

We reject a dichotomy between investing in ESG ‘enablers’ versus ‘improvers’. We would highlight a recent Morgan Stanley report on Earthshots led by Ed Stanley that identified a number of important emerging ‘enabling’ technologies – radical decarbonization accelerants or global warming mitigants. With the help of our global analysts, the team reviewed 40 promising technologies but zeroed in on six of the most game-changing. Given a growing mismatch between the pace of climate technology adoption and the planet's need for these solutions, we believe these Earthshots are likely to be a key secular trade of the 2020s.

In evaluating ‘improvers’, we reiterate the need to marry ESG investing principles and deep sector expertise. Applying ESG metrics without such knowledge can lead to suboptimal results. For example, in the US utilities sector, management teams are shutting down expensive coal-fired power plants and building renewables, energy storage, and transmission, which drives superior EPS growth. Our quantitative research team showed the superior stock returns for companies leading the way on this ‘carbon rate of change’ strategy, but many of these stocks would screen negatively on classic ESG metrics such as carbon intensity.

By Stephen Byrd, Head of North American Equity Research, Power/Utilities and Clean Tech at Morgan Stanley

Debate among investors is growing about whether to focus on stocks which are ESG ‘enablers’ with best-in-class ESG metrics, or on ‘ESG improvers’. We see merit in both approaches but believe the benefits of owning ‘ESG rate of change’ stocks and engaging with companies in transition are underappreciated. In a recent report, Morgan Stanley’s Sustainability Research team, in collaboration with industry analysts, our Quantitative Investment Strategies (QIS) team, and AlphaWise, show that focusing on names with improving ESG metrics can deliver both alpha and positive ESG impacts.

Our work is distinctive on multiple fronts. First, in collaboration with our analysts, we developed a forward-looking framework to analyze ESG rate of change at the stock level. We think it provides a better gauge of the likely future rate of change than typical data services, which are often backward looking and/or not informed by in-depth, sector-specific analyses. In addition, our analysts focused on companies with an opportunity to improve their financial performance thanks to ESG rate of change, a key difference from typical ESG analyses.

From a quant perspective, our QIS team assessed the impact on stock returns of ESG criteria such as carbon efficiency, exclusions driven by environmental harm, percentages of revenues linked to fossil fuels, and non-climate ESG concerns. The team found little evidence of a significant positive or negative effect on performance from screening on such broad ESG criteria. This underscores the need to marry ESG capabilities with strong sector expertise in order to generate alpha, tailoring ESG criteria and strategies to industry dynamics. We developed a robust set of sector-specific ESG rate of change criteria.

We were surprised how often deflationary technologies are driving simultaneous improvement in both ESG and financial metrics. An usually broad range of innovations are dropping in cost so much that they offer significant net benefits on both fronts. These include solar/wind/clean hydrogen, green ammonia, precision agriculture, improved molecular plastics recycling technology, more efficient electric motors, energy storage cost reductions, ‘green steel’, more durable vehicle tires, recycling technologies, electrification of many products/industrial processes, carbon capture tech, and waste-to-energy/waste-to-plastics technologies.

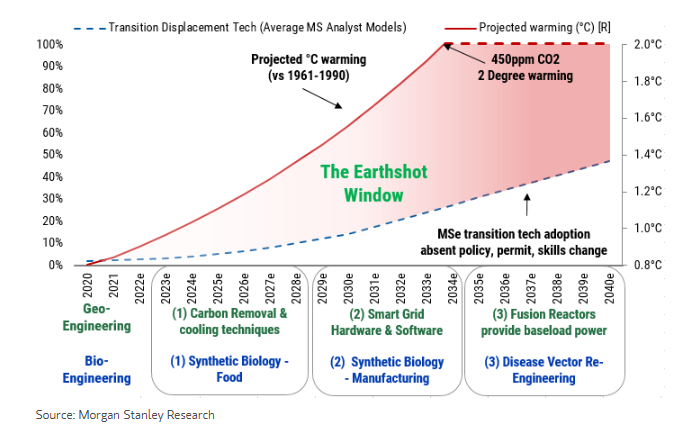

We reject a dichotomy between investing in ESG ‘enablers’ versus ‘improvers’. We would highlight a recent Morgan Stanley report on Earthshots led by Ed Stanley that identified a number of important emerging ‘enabling’ technologies – radical decarbonization accelerants or global warming mitigants. With the help of our global analysts, the team reviewed 40 promising technologies but zeroed in on six of the most game-changing. Given a growing mismatch between the pace of climate technology adoption and the planet’s need for these solutions, we believe these Earthshots are likely to be a key secular trade of the 2020s.

In evaluating ‘improvers’, we reiterate the need to marry ESG investing principles and deep sector expertise. Applying ESG metrics without such knowledge can lead to suboptimal results. For example, in the US utilities sector, management teams are shutting down expensive coal-fired power plants and building renewables, energy storage, and transmission, which drives superior EPS growth. Our quantitative research team showed the superior stock returns for companies leading the way on this ‘carbon rate of change’ strategy, but many of these stocks would screen negatively on classic ESG metrics such as carbon intensity.

Loading…