Non-fungible tokens are a social currency, born from “a desire to do more with blockchain than just cryptocurrency,” according to Steven Schuchart, principal analyst at GlobalData.

Eve Thomas writes at Verdict that the first NFT is widely thought to have been created in 2014 – ‘Quantum’ was created on the Namecoin blockchain by Kevin McCoy. It is a kaleidoscopic, pulsing octagon, which was auctioned off through Sotheby’s for $1.47 million.

December 2017 saw the CryptoKitties craze boost the hype around NFTs as the game gripped the NFT community: it was so successful that Etherscan reported a sixfold increase in pending transactions on Ethereum within the first week.

The market exploded in 2021, with $17.6bn worth of NFTs sold, an increase of 21,000% on 2020’s $82m total, according to a report by nonfungible.com. Amongst an increasingly valuable market, Beeple’s sale of ‘Everydays’ for $69m in March 2021 became the most expensive NFT ever sold.

When a market grows, so does the number of opportunistic criminals targeting it.

The NFT market became a landscape of “rampant fraud, Ponzi schemes, currency washing (money laundering), and rug pulls,” according to Schuchart.

And, with investor apprehension came a reappraisal of the utility of NFTs.

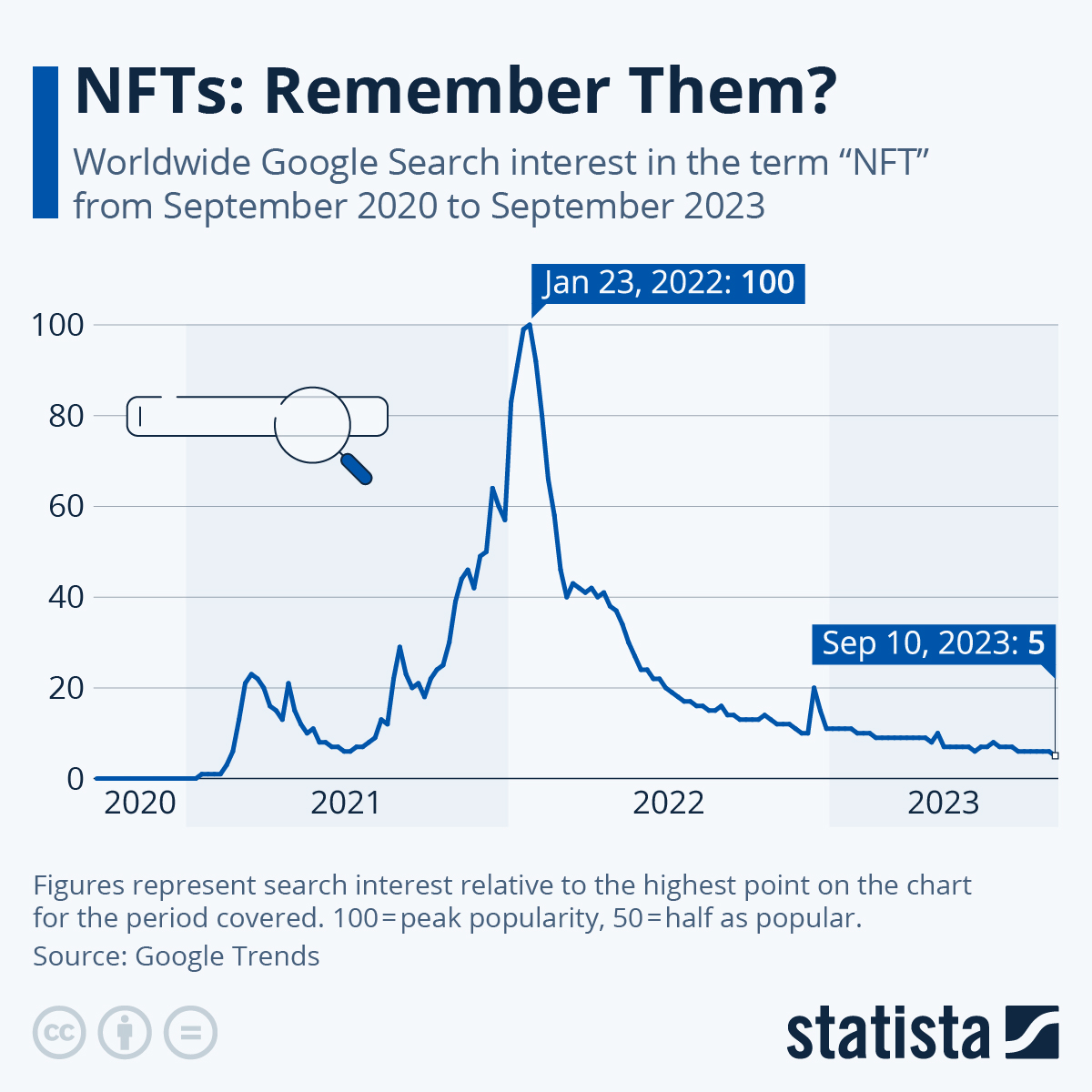

While many of us were forced to at least try to understand what an NFT is at some point in 2021 or 2022, the latest figures from Google Trends suggest that this research has not led to a sustained interest in the topic.

You will find more infographics at Statista

For those that didn't quite get around to it at the time, here's Wikipedia to the rescue:

"A non-fungible token (NFT) is a unique digital identifier that is recorded on a blockchain, and is used to certify ownership and authenticity. It cannot be copied, substituted, or subdivided. The ownership of an NFT is recorded in the blockchain and can be transferred by the owner, allowing NFTs to be sold and traded."

Still not clear?

Then have fun delving down this particular rabbit hole.

Though as Statista's Martin Armstrong notes, if the trend shown by Google's search data is anything to go by, combined with the countless NFT-based scams that have been uncovered, that might turn out to be a monumental waste of your time.

As Verdict's Eve Thomas concluded, for a while, it seemed that NFTs might revolutionise the world’s relationship with digital art. NFTs are still in use in some spheres: Neversea music festival is selling NFTs that provide exclusive access to parts of the festival, whilst Visa is running a Creator Program supporting NFT creators.

Nevertheless, the bubble has burst, and unless investors see a new reason to take interest, it looks as though it will be staying firmly popped.

Non-fungible tokens are a social currency, born from “a desire to do more with blockchain than just cryptocurrency,” according to Steven Schuchart, principal analyst at GlobalData.

Eve Thomas writes at Verdict that the first NFT is widely thought to have been created in 2014 – ‘Quantum’ was created on the Namecoin blockchain by Kevin McCoy. It is a kaleidoscopic, pulsing octagon, which was auctioned off through Sotheby’s for $1.47 million.

December 2017 saw the CryptoKitties craze boost the hype around NFTs as the game gripped the NFT community: it was so successful that Etherscan reported a sixfold increase in pending transactions on Ethereum within the first week.

The market exploded in 2021, with $17.6bn worth of NFTs sold, an increase of 21,000% on 2020’s $82m total, according to a report by nonfungible.com. Amongst an increasingly valuable market, Beeple’s sale of ‘Everydays’ for $69m in March 2021 became the most expensive NFT ever sold.

When a market grows, so does the number of opportunistic criminals targeting it.

The NFT market became a landscape of “rampant fraud, Ponzi schemes, currency washing (money laundering), and rug pulls,” according to Schuchart.

And, with investor apprehension came a reappraisal of the utility of NFTs.

While many of us were forced to at least try to understand what an NFT is at some point in 2021 or 2022, the latest figures from Google Trends suggest that this research has not led to a sustained interest in the topic.

You will find more infographics at Statista

For those that didn’t quite get around to it at the time, here’s Wikipedia to the rescue:

“A non-fungible token (NFT) is a unique digital identifier that is recorded on a blockchain, and is used to certify ownership and authenticity. It cannot be copied, substituted, or subdivided. The ownership of an NFT is recorded in the blockchain and can be transferred by the owner, allowing NFTs to be sold and traded.”

Still not clear?

Then have fun delving down this particular rabbit hole.

Though as Statista’s Martin Armstrong notes, if the trend shown by Google’s search data is anything to go by, combined with the countless NFT-based scams that have been uncovered, that might turn out to be a monumental waste of your time.

As Verdict’s Eve Thomas concluded, for a while, it seemed that NFTs might revolutionise the world’s relationship with digital art. NFTs are still in use in some spheres: Neversea music festival is selling NFTs that provide exclusive access to parts of the festival, whilst Visa is running a Creator Program supporting NFT creators.

Nevertheless, the bubble has burst, and unless investors see a new reason to take interest, it looks as though it will be staying firmly popped.

Loading…