Authored by Simon White, Bloomberg macro strategist,

Inflation may fall faster than most expect this year, but then surprise by beginning to rise again, potentially making new highs later in the cycle. Financial assets would have a reprieve due to a temporary easing in monetary policy, but face more downside as inflation began rising again.

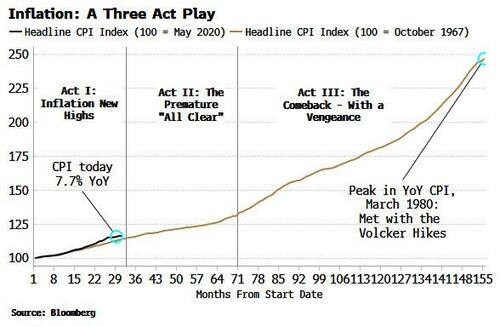

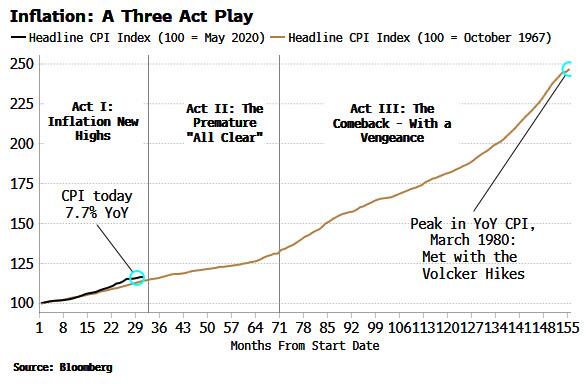

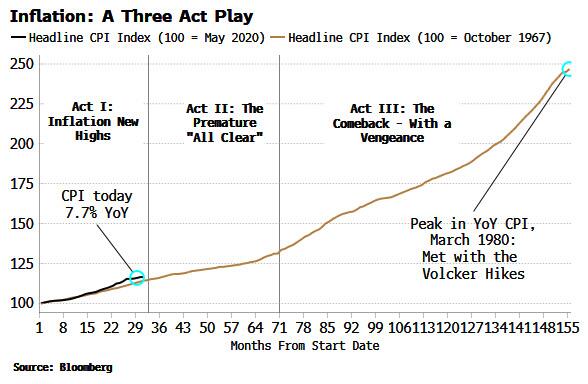

It helps to think of inflation as a play in three acts.

In the analogy, we are towards the end of the first act: inflation has peaked and is falling with greater momentum.

The second act sees the premature all-clear, where seemingly tamed inflation and a slowing economy eventually gives the Fed enough cover to begin easing policy.

However, the easing is likely to be too much too soon if the Fed really wants to stamp out inflation. It then starts to rise again, setting the stage for the third act, where inflation re-rears its head, potentially making new highs - as happened in the second half of the 1970s.

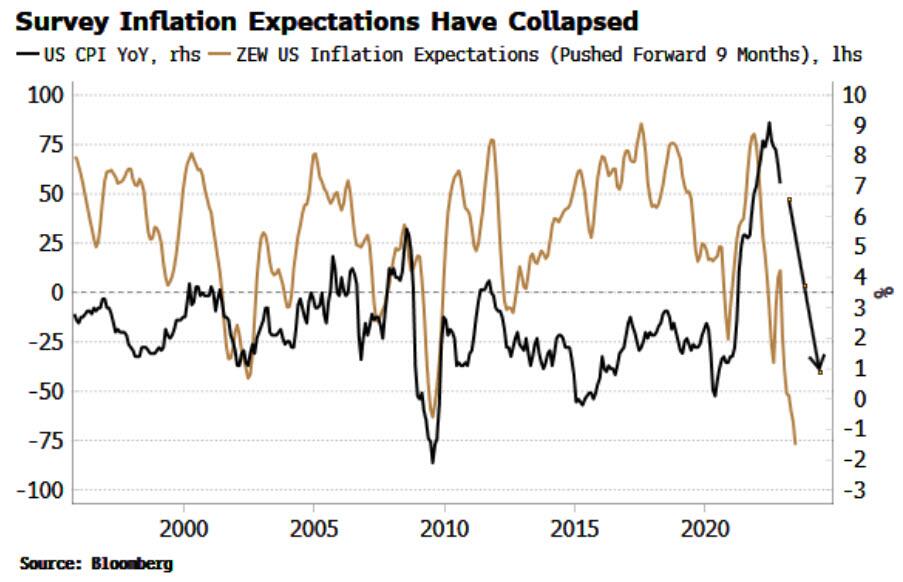

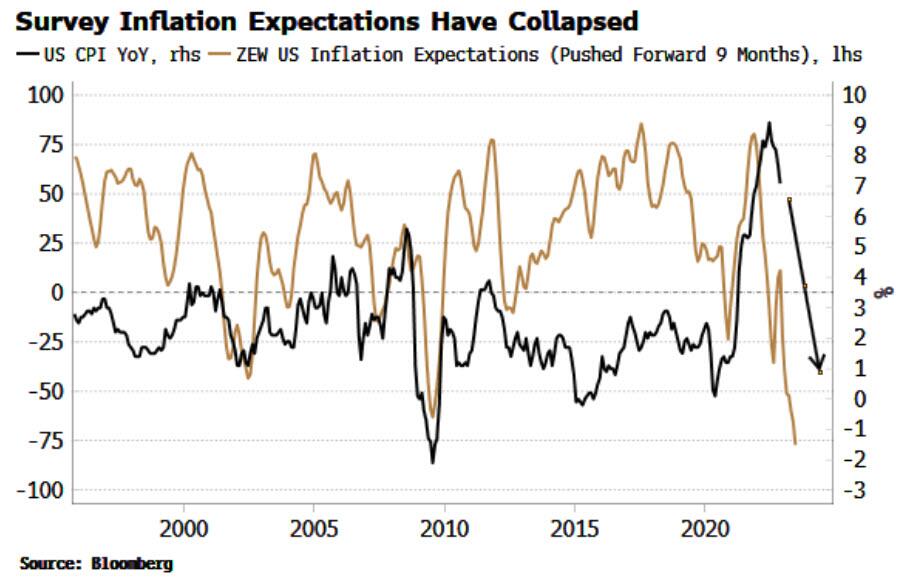

How long does the second act last? In the 70s, it took about 18 months to two years from inflation’s (initial) peak to its trough. But that timeline could be even shorter today. Some leading indicators, such as commodities, measures of supply-chain pressures, and survey-based inflation expectations, are showing a rapid fall in inflation over next six to nine months.

The economy is clearly slowing and, as in 1974, the US is likely to find itself in recession this year.

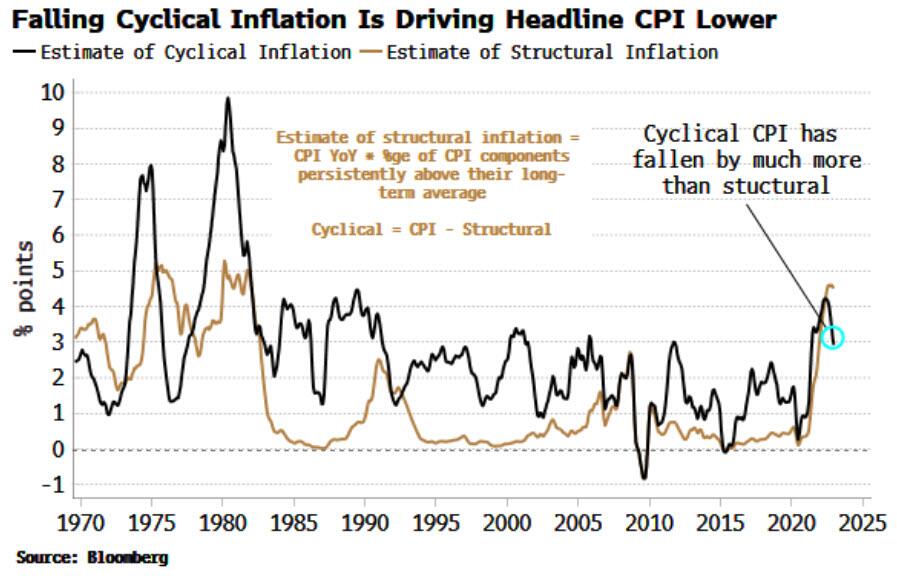

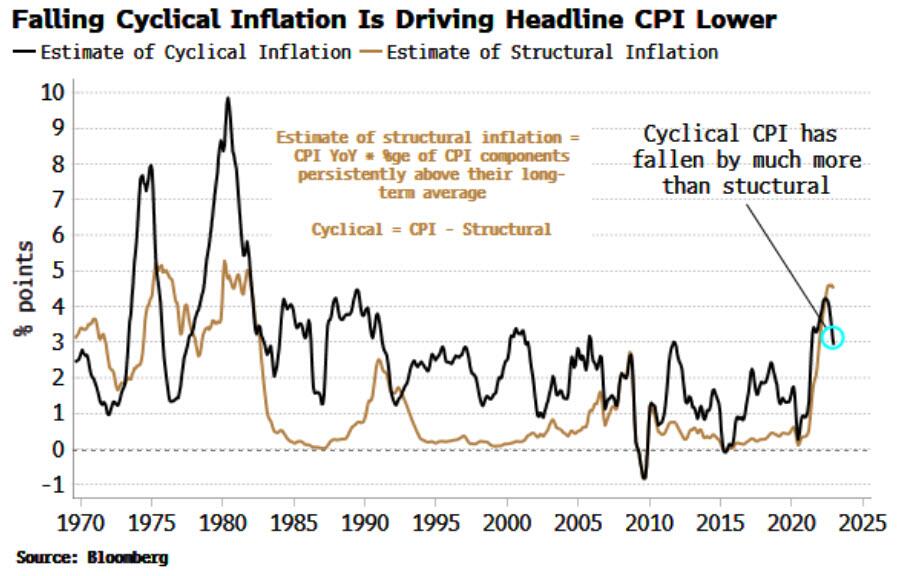

What, then, would drive inflation higher? To answer this it helps to split inflation into structural and cyclical components.

The fall in inflation this year is being driven by a decline in cyclical inflation. Structural inflation – now higher than it’s been since the 1970s – will fall too, but remain much stickier. Inflation overall will make a higher low. But then cyclical inflation will start rising again, adding to structural inflation that is unlikely to ease by much.

Thus inflation unexpectedly starts rising again from a higher base, potentially leading to it making new highs.

A tangible interpretation of this is as goods inflation (more cyclical) falls, the extra income goes into services inflation (more structural).

The inflation path means investment agility is key, as any window where the Fed eases is likely to be short-lived (one to two years). As the Volcker era reminds us, the final inflation act is a wrecking ball for financial assets.

Authored by Simon White, Bloomberg macro strategist,

Inflation may fall faster than most expect this year, but then surprise by beginning to rise again, potentially making new highs later in the cycle. Financial assets would have a reprieve due to a temporary easing in monetary policy, but face more downside as inflation began rising again.

It helps to think of inflation as a play in three acts.

In the analogy, we are towards the end of the first act: inflation has peaked and is falling with greater momentum.

The second act sees the premature all-clear, where seemingly tamed inflation and a slowing economy eventually gives the Fed enough cover to begin easing policy.

However, the easing is likely to be too much too soon if the Fed really wants to stamp out inflation. It then starts to rise again, setting the stage for the third act, where inflation re-rears its head, potentially making new highs – as happened in the second half of the 1970s.

How long does the second act last? In the 70s, it took about 18 months to two years from inflation’s (initial) peak to its trough. But that timeline could be even shorter today. Some leading indicators, such as commodities, measures of supply-chain pressures, and survey-based inflation expectations, are showing a rapid fall in inflation over next six to nine months.

The economy is clearly slowing and, as in 1974, the US is likely to find itself in recession this year.

What, then, would drive inflation higher? To answer this it helps to split inflation into structural and cyclical components.

The fall in inflation this year is being driven by a decline in cyclical inflation. Structural inflation – now higher than it’s been since the 1970s – will fall too, but remain much stickier. Inflation overall will make a higher low. But then cyclical inflation will start rising again, adding to structural inflation that is unlikely to ease by much.

Thus inflation unexpectedly starts rising again from a higher base, potentially leading to it making new highs.

A tangible interpretation of this is as goods inflation (more cyclical) falls, the extra income goes into services inflation (more structural).

The inflation path means investment agility is key, as any window where the Fed eases is likely to be short-lived (one to two years). As the Volcker era reminds us, the final inflation act is a wrecking ball for financial assets.

Loading…