By Peter Tchir of Academy Securities

Should I Stay or Should I Go?

Coming up for air after what was an intense week on the geopolitical and market side of things, I’m really being forced to reconsider my current recommendations (bearish bonds, stocks, and credit).

I keep thinking:

If I go, there will be trouble

And if I stay, it will be double

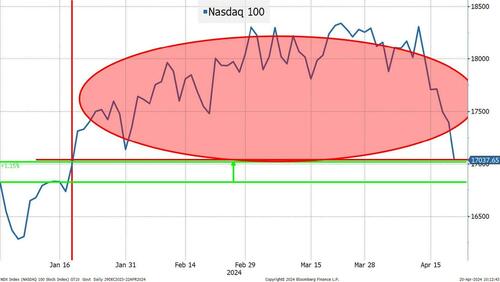

Bearish rates has worked well from the start. We turned negative on credit right near the lows, so that too has worked. On equities, by the time we turned bearish, it definitely moved against us. We had some drawdowns, and they seesawed back and forth between potentially making sense and looking very stupid (sometimes, on the same day). Well, the Nasdaq 100 (the main focus of our ire) is now down 7% since April 11th (6 trading days). We saw a rather nasty 2% drop on Friday (even after it had largely recovered from overnight Geopolitical concerns) and is now only up 1%. Our call had been that the market was highly susceptible to a rapid 5% to 10% decline, which we stretched to 10% as it continued to “defy” gravity. Remember, for all the hype about “all-time highs” and “tech is all you need”, the Nasdaq 100 closed above 18,300 all the way back on March 1st and barely got any higher than that in what is now almost 2 months.

We’ve updated this chart since we sent it around in an “informal” report, and the story is even more bleak, though not as bleak as it would have been had the markets closed at 3:45pm when this index was below 17,000.

Based on closing pricing, no one who bought the Nasdaq 100 since January 18th has made money. If you started the year long, you are now sitting on a relatively measly 1% gain – which just does not seem at all consistent with the hype.

In Thursday’s T-Report – We Can Drive it Home, With One Headlight, we reiterated our bearish views, while devoting much of the space to the section “AI valuations seem questionable.” There are some big stocks (some in the AI space) down around 10%. If you are keeping track at home, the leveraged single stock ETF that has caught my attention actually had net inflows on Friday, despite being down 20% - indicating that we haven’t seen a wipe out. I also distinctly remember headline after headline when we had record-setting market cap gains for individual companies, yet crickets on what had to be a historic drop in market cap. Another sign that we have not seen a washout.

But before we go through our analysis and recommendations coming into this week, I have to admit, “Should I Stay or Should I Go” isn’t close to being my favorite song by the Clash. But, I’ve already used “Magnificent Seven”, “Clampdown” seemed too harsh, “Lost in the Supermarket” would have made more sense when inflation was spiking, and “Death or Glory” sadly seems destined to pop up in a piece on geopolitics (the way the world is going). I did want to do I Fought the NDX and I Won, but the Clash cover stuck to the traditional title, and it was the Dead Kennedys who changed it to “I won” rather than “the law won.” But in the end it hasn’t been a resounding win, and I didn’t want to jinx myself too badly if I come out still bearish (spoiler alert, I am).

Equities

Today we will focus on what is “new” as the bear case was well covered in the previously referenced One Headlight piece.

The most bullish thing I can say is that equities are now 5% to 7% cheaper than a week or so ago. So, if you were planning on “backing up the truck” and loading up on stocks, you have that opportunity. You literally have missed nothing by not being massively overweight the Nasdaq 100 since the start of the year. Two issues fighting this come to mind:

- There have been multiple small dips this year, so how much dip buying capacity remains?

- My view is that when people say “I would load the boat if that stock drops 5%”, what they really mean is “I would load the boat if that stock drops 5% in otherwise calm markets, for no apparently good reason, basically letting me buy the same story, but 5% cheaper”. Well, the story and market dynamics have changed. Geopolitical risk has risen. Questions about valuation, easily dismissed when stocks seemed to be up every day (they weren’t but that was the narrative), are not so easily dismissed. As the chart highlights, anyone who bought this year is now likely under water on their new investments in this index (or ETFs like QQQ). Don’t get me started on ARKK, my “go to” proxy for “innovation” and “disruption,” which is down 20% on the year now. I will admit, Bitcoin might be a haven for some of the riskiest risk takers, as it is up strongly on the year, though it too has done very little (except cost buyers money) since the end of February. The “halving” is supposed to take it to the next level. How paying someone 50% less (for the same work that they did) helps the price is beyond me. I mean, I get the miners in particular are incentivized to jack up prices, but the “bitcoin always goes higher after the halving” arguments are based on such a small sample size, that I think it will not work this time as the entire crypto universe seems to think it will.

But anyways, I digress, I just think that enough has changed and enough dips have been bought, that there is no trove of “rescue” money about to flood the market with new buying liquidity.

Since AI remains too important, I will add one thing to the laundry list from Thursday:

-

Using Google trends, searches for things like ChatGPT are down and declining. Same for some broader themes on AI. You cannot have FOMO without the Fear of Missing Out and I don’t think we are ripe with Fear any longer. If anything, maybe it is the fear that valuations have gotten ahead of themselves.

Earnings will be important, and we will get several from very important companies this week.

-

Maybe it is my imagination (it could be, since there are few data points so far), but the “reaction function” to earnings seems to have changed. As we rallied late last year and at the start of this year, it seemed that the market focused on positives and dismissed negatives. It also seemed to rally on the “same” news, day after day. One stock in a sector would report positives and the market would take the sector significantly higher. A day or two later another company in the sector would give the market something to cheer about and the entire sector would pop again. Wasn’t some of that good news already priced in? I believe we have much higher hurdles this time and the markets are looking for excuses to sell, rather than to buy. I could be wrong on the reaction function or earnings could all beat by so much that we get a reversal, but I’m skeptical on that.

Think like an algo.

-

I tend to be a “profit” taker (and “double downer”). When things work, I like to take chips off the table. What I constantly need to remind myself of is that algos are often wired in the opposite direction. They press winners. They tend to follow momentum. They tend to be quick to stop themselves out. I believe algos/quantitative trading models have been exiting stocks. Are they out? Possibly, we have seen higher volumes on this down move. Have they turned from buyers to sellers and are happy to establish shorts and push those? That I don’t know, but my fear of “systematic” trading systems (often described simply as CTAs, but a universe much bigger than that) makes me want to stay bearish.

In the end, I’ve started to reduce shorts, but remain bearish, and think that the correct strategy is to sell bounces and keep reloading shorts, until something occurs that forces me to change my views.

Bond Yields

In the end, on equities, it turned out to be “more of the same” (maybe slightly less pounding on the table), but bonds are far more interesting in terms of “staying” or “going” from a bearish perspective.

We’ve been bearish on yields for most of this year and it has largely worked. Not a one-way street by any stretch of the imagination, but not bad. In fact, we’ve raised our range on the 10-year yield, from 4.2%-4.4% to 4.3%-4.5% and then from 4.4%-4.6%. I don’t think we’ve officially changed the band, but it is implicit that if 10-years are at 4.62% and I’m still bearish (though far less so than at 3.9% where we started the year), the band must be higher. Do we raise the range again? That is always a dangerous game, as many equity analysts, who felt compelled to raise price targets in the past few months, can tell you. Were we too low originally? Have things changed that significantly? Take the win? I’m not sure if repeatedly raising your bands is something that should be considered in current analysis, but it makes sense (at least for me).

Aside from many specific reasons to be bearish, we had the catch-all of “nothing that was in place to push 10s to 5% last fall has been resolved.” That is still true.

What is the bull case for bonds?

-

Inflation. While I was never part of the “Super Users” group, I think I can relate to my understanding of the “gist” of the story – wanting more data to better understand what the heck the BLS actually comes up with for inflation. Let’s for the moment assume that inflation has “become sticky” around 2.5% (to pick a number). Then lets think about all the issues with measuring inflation. Hedonic quality adjustments. Substitution. Difficulty measuring. Flawed measurements (housing and rent, while ignoring the always “curious” use of Owners Equivalent Rent, have a lag effect built in, for gosh knows what “useful” reason). Last month, in at least one of the reports, it all came down to auto insurance. So, let’s assume that any given month is within 0.2% of being an accurate representation for that month (somehow, I feel I’m generous). Then it is at 2.4% annualized. So if we are centered around 2.5% (or 0.2% per month), then we could easily see a month with no inflation that annualizes to “problem solved.” While I believe on-shoring, near-shoring, geopolitical inflation, and the realization that we need to build out traditional and new energy sources, etc., will be inflationary, I would have to bet on seeing what would now be considered a surprise (a month where inflation data looks really good), especially given the current levels of expectations. One big fear I have about remaining bearish, is that not only would I not be surprised to see some good inflation data before the June meeting, but also I would be shocked if we didn’t. More about measurement and reporting than any real change in the underlying inflation rate.

-

Carry. Yes, the path to hell is paved with carry (or interest), but it is real. The back-up in yields provides more protection. While I’m constantly aware that selling can beget more selling (see my equity concerns), the case for “buying the dip” in bonds is stronger. More yield. Interest coming in every month that can be re-invested. Less inversion, making the decision between 2s and 10s more complicated even for “yield hogs” who focus more on yield than duration.

-

“No Bounce” and “American Exceptionalism” have become so consensus that it wouldn’t take much to tip the apple cart and put some level of fear about the state of the economy back on the table. I think earnings, and more importantly outlooks, may paint that picture for us.

I am worried about “faux” liquidity, even in the Treasury market. Electronic trading and a multitude of platforms tend to make liquidity appear more abundant than it really is. There aren’t 50 people sitting on the bid. There are 10, they just happen to all put them on 5 platforms, assuming they can yank the bid in time. There are really only 5 buyers, the other 5 just “see” them buying, so are along for the ride hoping to scalp some money and thinking they can pull their bids if necessary. That is why we get “air pockets” in pricing and will continue to do so. Positioning is better than it was (not everyone is long), but this “gap” risk is real – in both directions.

I like the 2-year at 5% and am “tolerant” of 10s at 4.6%.

Credit

Credit spreads for me are now largely just a proxy for equites. Yes CDX, credit spreads, and even high yield held their own on Friday amidst the debacle of an equity market, but that will be difficult to sustain.

I see no fundamental problems in credit, but it is difficult to remain bearish on equities and like credit. Also, the aforementioned “faux” liquidity is even more obvious in credit markets and creates far more gap risk. While that gap risk is usually somewhat symmetric, I think the gap risk to much wider is higher than the risk to a gap tighter. Still like 65-70 as range on CDX.

Geopolitical Base Case

Academy Securities has sent a lot out on the current situation in the Middle East. We’ve done what we can with our team of retired Generals and Admirals. Not just via written word (please see the “new” Daily Brief that we’ve been sending on Bloomberg), but also through more video calls than I can keep track of.

Even with their expertise, there is a range of “error” or “doubt” centered around “what has happened” let alone “what might happen.”

There have been some fast and furious discussions about deterrence and General (ret.) Ashley highlighted this Rand publication – Understanding Deterrence from 2018. Academy’s game theory centric piece – Geopolitical Chicken – is worth reading if you haven’t already.

Anyways, my base case is:

-

Iran’s attack on Israel was not just symbolic. They planned to cause damage and are really concerned that they didn’t. I’m agreeing with the argument that you send “a handful” of drones/missiles (all of the lowest quality) if you want to ensure that they don’t get through. Sending 100s with a range of capabilities, was an actual attack that failed. Others make the case that it was symbolic and designed to be destroyed en route. I find that argument less plausible, hence, not my base case.

-

Therefore, much like Russia, they have to recalculate their war effort. If the attack was somewhere between Fail and Epic Fail, you need to rethink your strategy. It is far too early for them to have understood what went wrong, let alone how to “correct” it, so of course they will downplay the Israeli attack on Iranian soil. You cannot afford to have a second failed attack. You might convince the world that you launched a “second symbolic” attack, but that’s a stretch of the imagination.

Therefore, my base case is that Iran is trying to figure out how to attack again, which may take some time, and a lot could change between now and then, but the current “quiet” is more about a failed attack than any meaningful de-escalation.

That may or may not be your base case, and even by working so closely with our Geopolitical Intelligence Group, you can find support for a range of “base cases,” but this is my working assumption. This means that I think possible shocks are still on the table. From Hedging Geopolitical Risk I think any shock will be bad for equities, temporarily good for bonds (but fade that quickly), and good for oil.

Bottom Line

There is very little I can find in equities. I’m not even “loving” long China (for a trade) versus short Nasdaq 100 (though I’d be remiss to point out for the past 3 months, FXI is up 10.8% while QQQ is down 1.4%). Remember, I think that as time goes by, more people will question whether slower sales into China are a function of problems with the Chinese economy or part of a broader strategy to suppress sales of Western brands in favor of domestic brands – The Threat of Made by China 2025.

- I still own energy and commodities but biased towards owning the equities (not the underlying commodities). It is interesting that the equities (looking at XLE) did so well on Friday. Maybe reduce some positions here, but this is my favorite sector. Iran seems unlikely to respond soon, given my base case, and my bet is that we see some signals of a slowing economy emerge from earnings calls.

- Neutral to mildly bullish Treasuries. There, I’ve done it. I’ve flipped. For now, buy some Treasuries. Stick to a 4.45% to 4.6% band on 10s. This is for a “trade” rather than a fundamental shift. If there is any market where deep out of the money options make sense, it could be here, as faux liquidity makes me fear a “flash crash” type of scenario. If this “bull case” sounds tepid, it is because it is tepid, but I’ve flip-flopped here to the bull side (again, for a trade, tepidly, and acknowledging the risk of a gap to much higher yields).

- Credit. Moderately bearish, based primarily on having a bearish outlook on equities. I don’t see fundamental issues, but that doesn’t matter for the next 10 bps on IG credit. Rising Treasury yields have helped credit spreads (got the higher yield on IG and even High Yield without having to demand wider spreads). If I’m correct and Treasuries bounce, then spreads are likely to feel a little bit of pain as you see a “flight to quality” (as opposed to a “flight to safety”).

Hopefully, by the time you read this report it is still relevant in a world where countries don’t adhere to a policy of attacking only during U.S. trading hours!

Good luck navigating this and please feel free to use Academy’s resources, as we as a firm are at your disposal!

By Peter Tchir of Academy Securities

Should I Stay or Should I Go?

Coming up for air after what was an intense week on the geopolitical and market side of things, I’m really being forced to reconsider my current recommendations (bearish bonds, stocks, and credit).

I keep thinking:

If I go, there will be trouble

And if I stay, it will be double

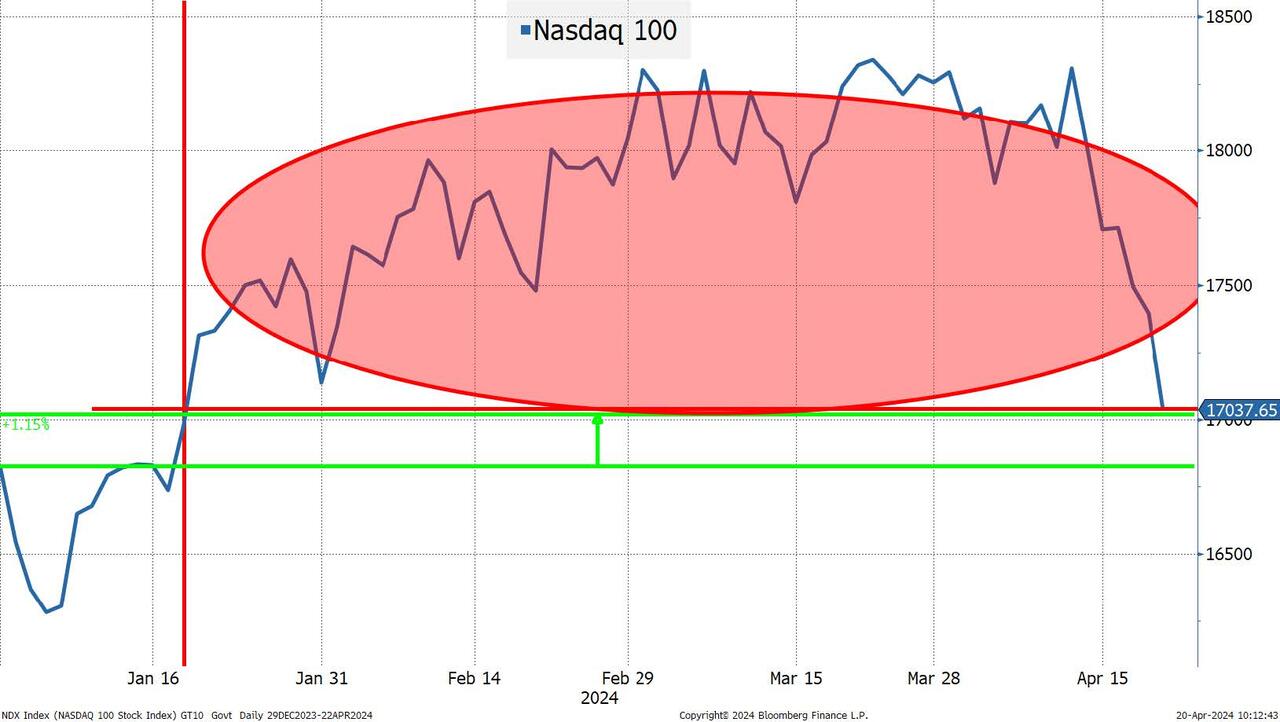

Bearish rates has worked well from the start. We turned negative on credit right near the lows, so that too has worked. On equities, by the time we turned bearish, it definitely moved against us. We had some drawdowns, and they seesawed back and forth between potentially making sense and looking very stupid (sometimes, on the same day). Well, the Nasdaq 100 (the main focus of our ire) is now down 7% since April 11th (6 trading days). We saw a rather nasty 2% drop on Friday (even after it had largely recovered from overnight Geopolitical concerns) and is now only up 1%. Our call had been that the market was highly susceptible to a rapid 5% to 10% decline, which we stretched to 10% as it continued to “defy” gravity. Remember, for all the hype about “all-time highs” and “tech is all you need”, the Nasdaq 100 closed above 18,300 all the way back on March 1st and barely got any higher than that in what is now almost 2 months.

We’ve updated this chart since we sent it around in an “informal” report, and the story is even more bleak, though not as bleak as it would have been had the markets closed at 3:45pm when this index was below 17,000.

Based on closing pricing, no one who bought the Nasdaq 100 since January 18th has made money. If you started the year long, you are now sitting on a relatively measly 1% gain – which just does not seem at all consistent with the hype.

In Thursday’s T-Report – We Can Drive it Home, With One Headlight, we reiterated our bearish views, while devoting much of the space to the section “AI valuations seem questionable.” There are some big stocks (some in the AI space) down around 10%. If you are keeping track at home, the leveraged single stock ETF that has caught my attention actually had net inflows on Friday, despite being down 20% – indicating that we haven’t seen a wipe out. I also distinctly remember headline after headline when we had record-setting market cap gains for individual companies, yet crickets on what had to be a historic drop in market cap. Another sign that we have not seen a washout.

But before we go through our analysis and recommendations coming into this week, I have to admit, “Should I Stay or Should I Go” isn’t close to being my favorite song by the Clash. But, I’ve already used “Magnificent Seven”, “Clampdown” seemed too harsh, “Lost in the Supermarket” would have made more sense when inflation was spiking, and “Death or Glory” sadly seems destined to pop up in a piece on geopolitics (the way the world is going). I did want to do I Fought the NDX and I Won, but the Clash cover stuck to the traditional title, and it was the Dead Kennedys who changed it to “I won” rather than “the law won.” But in the end it hasn’t been a resounding win, and I didn’t want to jinx myself too badly if I come out still bearish (spoiler alert, I am).

Equities

Today we will focus on what is “new” as the bear case was well covered in the previously referenced One Headlight piece.

The most bullish thing I can say is that equities are now 5% to 7% cheaper than a week or so ago. So, if you were planning on “backing up the truck” and loading up on stocks, you have that opportunity. You literally have missed nothing by not being massively overweight the Nasdaq 100 since the start of the year. Two issues fighting this come to mind:

- There have been multiple small dips this year, so how much dip buying capacity remains?

- My view is that when people say “I would load the boat if that stock drops 5%”, what they really mean is “I would load the boat if that stock drops 5% in otherwise calm markets, for no apparently good reason, basically letting me buy the same story, but 5% cheaper”. Well, the story and market dynamics have changed. Geopolitical risk has risen. Questions about valuation, easily dismissed when stocks seemed to be up every day (they weren’t but that was the narrative), are not so easily dismissed. As the chart highlights, anyone who bought this year is now likely under water on their new investments in this index (or ETFs like QQQ). Don’t get me started on ARKK, my “go to” proxy for “innovation” and “disruption,” which is down 20% on the year now. I will admit, Bitcoin might be a haven for some of the riskiest risk takers, as it is up strongly on the year, though it too has done very little (except cost buyers money) since the end of February. The “halving” is supposed to take it to the next level. How paying someone 50% less (for the same work that they did) helps the price is beyond me. I mean, I get the miners in particular are incentivized to jack up prices, but the “bitcoin always goes higher after the halving” arguments are based on such a small sample size, that I think it will not work this time as the entire crypto universe seems to think it will.

But anyways, I digress, I just think that enough has changed and enough dips have been bought, that there is no trove of “rescue” money about to flood the market with new buying liquidity.

Since AI remains too important, I will add one thing to the laundry list from Thursday:

-

Using Google trends, searches for things like ChatGPT are down and declining. Same for some broader themes on AI. You cannot have FOMO without the Fear of Missing Out and I don’t think we are ripe with Fear any longer. If anything, maybe it is the fear that valuations have gotten ahead of themselves.

Earnings will be important, and we will get several from very important companies this week.

-

Maybe it is my imagination (it could be, since there are few data points so far), but the “reaction function” to earnings seems to have changed. As we rallied late last year and at the start of this year, it seemed that the market focused on positives and dismissed negatives. It also seemed to rally on the “same” news, day after day. One stock in a sector would report positives and the market would take the sector significantly higher. A day or two later another company in the sector would give the market something to cheer about and the entire sector would pop again. Wasn’t some of that good news already priced in? I believe we have much higher hurdles this time and the markets are looking for excuses to sell, rather than to buy. I could be wrong on the reaction function or earnings could all beat by so much that we get a reversal, but I’m skeptical on that.

Think like an algo.

-

I tend to be a “profit” taker (and “double downer”). When things work, I like to take chips off the table. What I constantly need to remind myself of is that algos are often wired in the opposite direction. They press winners. They tend to follow momentum. They tend to be quick to stop themselves out. I believe algos/quantitative trading models have been exiting stocks. Are they out? Possibly, we have seen higher volumes on this down move. Have they turned from buyers to sellers and are happy to establish shorts and push those? That I don’t know, but my fear of “systematic” trading systems (often described simply as CTAs, but a universe much bigger than that) makes me want to stay bearish.

In the end, I’ve started to reduce shorts, but remain bearish, and think that the correct strategy is to sell bounces and keep reloading shorts, until something occurs that forces me to change my views.

Bond Yields

In the end, on equities, it turned out to be “more of the same” (maybe slightly less pounding on the table), but bonds are far more interesting in terms of “staying” or “going” from a bearish perspective.

We’ve been bearish on yields for most of this year and it has largely worked. Not a one-way street by any stretch of the imagination, but not bad. In fact, we’ve raised our range on the 10-year yield, from 4.2%-4.4% to 4.3%-4.5% and then from 4.4%-4.6%. I don’t think we’ve officially changed the band, but it is implicit that if 10-years are at 4.62% and I’m still bearish (though far less so than at 3.9% where we started the year), the band must be higher. Do we raise the range again? That is always a dangerous game, as many equity analysts, who felt compelled to raise price targets in the past few months, can tell you. Were we too low originally? Have things changed that significantly? Take the win? I’m not sure if repeatedly raising your bands is something that should be considered in current analysis, but it makes sense (at least for me).

Aside from many specific reasons to be bearish, we had the catch-all of “nothing that was in place to push 10s to 5% last fall has been resolved.” That is still true.

What is the bull case for bonds?

-

Inflation. While I was never part of the “Super Users” group, I think I can relate to my understanding of the “gist” of the story – wanting more data to better understand what the heck the BLS actually comes up with for inflation. Let’s for the moment assume that inflation has “become sticky” around 2.5% (to pick a number). Then lets think about all the issues with measuring inflation. Hedonic quality adjustments. Substitution. Difficulty measuring. Flawed measurements (housing and rent, while ignoring the always “curious” use of Owners Equivalent Rent, have a lag effect built in, for gosh knows what “useful” reason). Last month, in at least one of the reports, it all came down to auto insurance. So, let’s assume that any given month is within 0.2% of being an accurate representation for that month (somehow, I feel I’m generous). Then it is at 2.4% annualized. So if we are centered around 2.5% (or 0.2% per month), then we could easily see a month with no inflation that annualizes to “problem solved.” While I believe on-shoring, near-shoring, geopolitical inflation, and the realization that we need to build out traditional and new energy sources, etc., will be inflationary, I would have to bet on seeing what would now be considered a surprise (a month where inflation data looks really good), especially given the current levels of expectations. One big fear I have about remaining bearish, is that not only would I not be surprised to see some good inflation data before the June meeting, but also I would be shocked if we didn’t. More about measurement and reporting than any real change in the underlying inflation rate.

-

Carry. Yes, the path to hell is paved with carry (or interest), but it is real. The back-up in yields provides more protection. While I’m constantly aware that selling can beget more selling (see my equity concerns), the case for “buying the dip” in bonds is stronger. More yield. Interest coming in every month that can be re-invested. Less inversion, making the decision between 2s and 10s more complicated even for “yield hogs” who focus more on yield than duration.

-

“No Bounce” and “American Exceptionalism” have become so consensus that it wouldn’t take much to tip the apple cart and put some level of fear about the state of the economy back on the table. I think earnings, and more importantly outlooks, may paint that picture for us.

I am worried about “faux” liquidity, even in the Treasury market. Electronic trading and a multitude of platforms tend to make liquidity appear more abundant than it really is. There aren’t 50 people sitting on the bid. There are 10, they just happen to all put them on 5 platforms, assuming they can yank the bid in time. There are really only 5 buyers, the other 5 just “see” them buying, so are along for the ride hoping to scalp some money and thinking they can pull their bids if necessary. That is why we get “air pockets” in pricing and will continue to do so. Positioning is better than it was (not everyone is long), but this “gap” risk is real – in both directions.

I like the 2-year at 5% and am “tolerant” of 10s at 4.6%.

Credit

Credit spreads for me are now largely just a proxy for equites. Yes CDX, credit spreads, and even high yield held their own on Friday amidst the debacle of an equity market, but that will be difficult to sustain.

I see no fundamental problems in credit, but it is difficult to remain bearish on equities and like credit. Also, the aforementioned “faux” liquidity is even more obvious in credit markets and creates far more gap risk. While that gap risk is usually somewhat symmetric, I think the gap risk to much wider is higher than the risk to a gap tighter. Still like 65-70 as range on CDX.

Geopolitical Base Case

Academy Securities has sent a lot out on the current situation in the Middle East. We’ve done what we can with our team of retired Generals and Admirals. Not just via written word (please see the “new” Daily Brief that we’ve been sending on Bloomberg), but also through more video calls than I can keep track of.

Even with their expertise, there is a range of “error” or “doubt” centered around “what has happened” let alone “what might happen.”

There have been some fast and furious discussions about deterrence and General (ret.) Ashley highlighted this Rand publication – Understanding Deterrence from 2018. Academy’s game theory centric piece – Geopolitical Chicken – is worth reading if you haven’t already.

Anyways, my base case is:

-

Iran’s attack on Israel was not just symbolic. They planned to cause damage and are really concerned that they didn’t. I’m agreeing with the argument that you send “a handful” of drones/missiles (all of the lowest quality) if you want to ensure that they don’t get through. Sending 100s with a range of capabilities, was an actual attack that failed. Others make the case that it was symbolic and designed to be destroyed en route. I find that argument less plausible, hence, not my base case.

-

Therefore, much like Russia, they have to recalculate their war effort. If the attack was somewhere between Fail and Epic Fail, you need to rethink your strategy. It is far too early for them to have understood what went wrong, let alone how to “correct” it, so of course they will downplay the Israeli attack on Iranian soil. You cannot afford to have a second failed attack. You might convince the world that you launched a “second symbolic” attack, but that’s a stretch of the imagination.

Therefore, my base case is that Iran is trying to figure out how to attack again, which may take some time, and a lot could change between now and then, but the current “quiet” is more about a failed attack than any meaningful de-escalation.

That may or may not be your base case, and even by working so closely with our Geopolitical Intelligence Group, you can find support for a range of “base cases,” but this is my working assumption. This means that I think possible shocks are still on the table. From Hedging Geopolitical Risk I think any shock will be bad for equities, temporarily good for bonds (but fade that quickly), and good for oil.

Bottom Line

There is very little I can find in equities. I’m not even “loving” long China (for a trade) versus short Nasdaq 100 (though I’d be remiss to point out for the past 3 months, FXI is up 10.8% while QQQ is down 1.4%). Remember, I think that as time goes by, more people will question whether slower sales into China are a function of problems with the Chinese economy or part of a broader strategy to suppress sales of Western brands in favor of domestic brands – The Threat of Made by China 2025.

- I still own energy and commodities but biased towards owning the equities (not the underlying commodities). It is interesting that the equities (looking at XLE) did so well on Friday. Maybe reduce some positions here, but this is my favorite sector. Iran seems unlikely to respond soon, given my base case, and my bet is that we see some signals of a slowing economy emerge from earnings calls.

- Neutral to mildly bullish Treasuries. There, I’ve done it. I’ve flipped. For now, buy some Treasuries. Stick to a 4.45% to 4.6% band on 10s. This is for a “trade” rather than a fundamental shift. If there is any market where deep out of the money options make sense, it could be here, as faux liquidity makes me fear a “flash crash” type of scenario. If this “bull case” sounds tepid, it is because it is tepid, but I’ve flip-flopped here to the bull side (again, for a trade, tepidly, and acknowledging the risk of a gap to much higher yields).

- Credit. Moderately bearish, based primarily on having a bearish outlook on equities. I don’t see fundamental issues, but that doesn’t matter for the next 10 bps on IG credit. Rising Treasury yields have helped credit spreads (got the higher yield on IG and even High Yield without having to demand wider spreads). If I’m correct and Treasuries bounce, then spreads are likely to feel a little bit of pain as you see a “flight to quality” (as opposed to a “flight to safety”).

Hopefully, by the time you read this report it is still relevant in a world where countries don’t adhere to a policy of attacking only during U.S. trading hours!

Good luck navigating this and please feel free to use Academy’s resources, as we as a firm are at your disposal!

Loading…