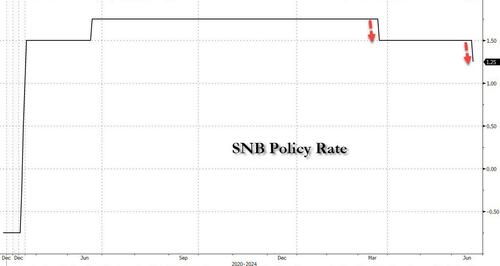

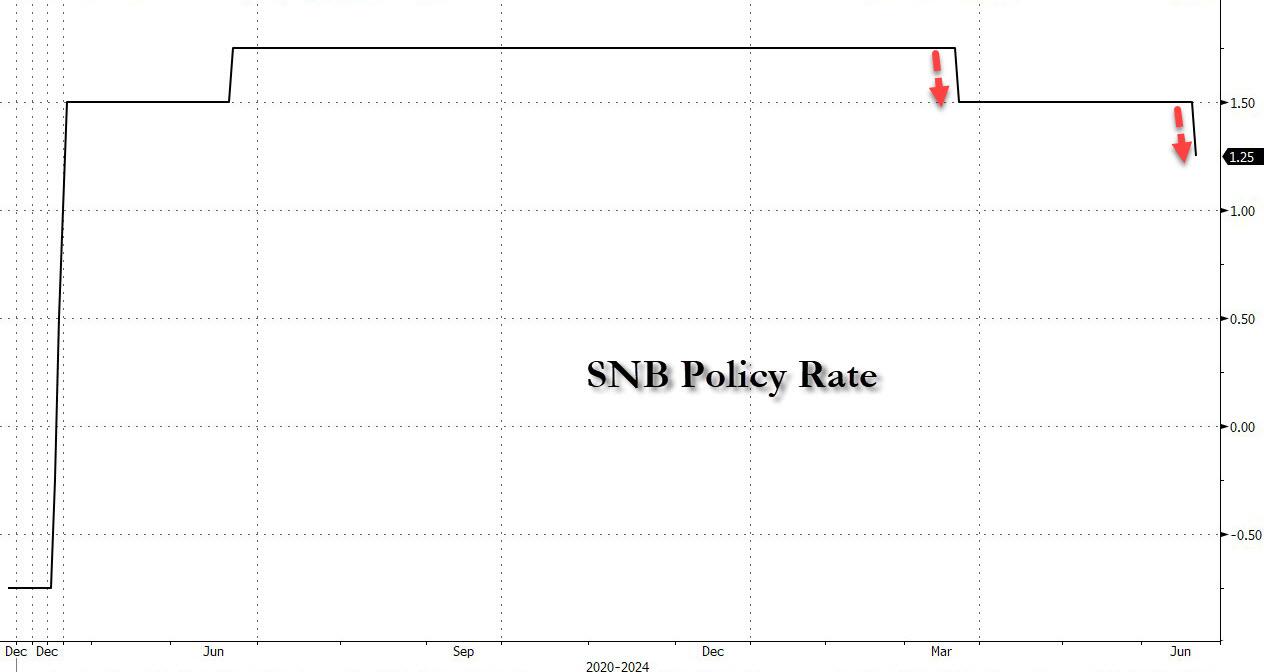

The Swiss National Bank unexpectedly cut interest rates on Thursday for the second time this year, pointing to easing price pressures that allowed it to maintain its position as the front-runner in the global policy easing cycle now underway.

The Swiss franc, which had soared in the past three weeks after the shocking result from the European parliament elections hammered the Euro, weakened against other currencies and stocks gained after the central bank cut its policy rate by 25 basis points to 1.25%, as expected by two-thirds of analysts polled by Bloomberg, following a quarter-point reduction in March.

The SNB's decision had been "finely balanced", similar to the BOE's decision to not cut rates, given a recent rebound in economic growth and a break in the trend of gently falling inflation in Switzerland.

"The underlying inflationary pressure has decreased again compared to the previous quarter," SNB Chairman Thomas Jordan said. "With today's lowering of the SNB policy rate, we are able to maintain appropriate monetary conditions."

Jordan pointed to the SNB's inflation forecasts, which were tweaked downwards and enabled the reduction in interest rates. While everyone knows how accurate central bank predictions are, even at the furthest end of its forecasts - covering the first quarter of 2027 - the SNB now expects inflation at 1.0%, well within its 0-2% target range.

With the updated language in the Monetary Policy Assessment, which states that "with today’s lowering of the SNB policy rate, the SNB is able to maintain appropriate monetary conditions" and an estimate of the neutral rate at around 1.25%, Goldman maintains its view that today's cut is likely to be the end of the SNB's easing cycle.

UBS, however, disagrees and points out that the SNB said that without this rate cut, the inflation forecasts would have been lower: "That suggests by the time of the next meeting, inflation forecasts will be lower without another cut; there was no change in the language to suggest a pause is coming up. Before this decision, UBS Economics had expected a cut in June and one more in September, to lower the base rate to 1%."

The recent rise of the Swiss franc, driven by rising political uncertainty in Europe pushing investors towards the safe haven currency, was also highlighted by Jordan. The franc has gained 4.5% against the euro in the past month on political concerns, including the upcoming French elections, which could see the far right win power. The SNB was paying close attention, Jordan said.

"We are ready to be active on the foreign exchange market and that can go in both directions," he told reporters.

According to Reuters, various factors lie behind Switzerland's low price pressures, including an energy mix that makes the country less exposed to oil and gas costs, wage restraint, and protection against imported price inflation from the strong franc.

Here are the three main points on the rate cut according to Goldman:

- The Swiss National Bank (SNB) surprised consensus expectations again and delivered another 25bp cut to 1.25%, in line with our forecast. The language around FX interventions was left unchanged, with the Monetary Policy Assessment (MPA) noting that the SNB remains willing to be active in FX market "as necessary".

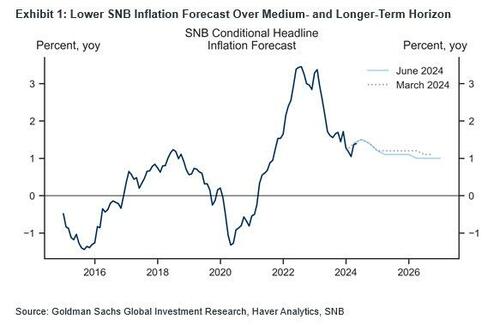

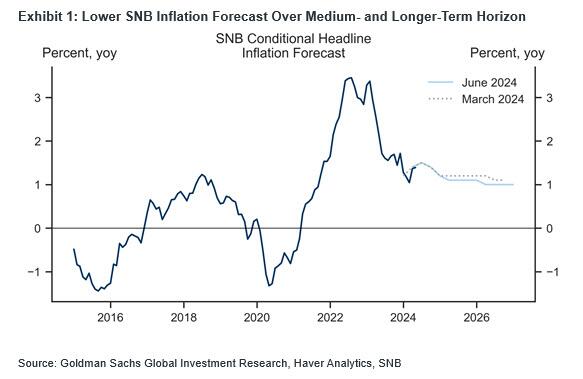

- Exhibit 1 shows the new conditional inflation forecast, which was revised down slightly on account of weaker second-round effects (-0.1pp to 1.3% in 2024, -0.1pp to 1.1% in 2025, -0.1pp to 1.0% in 2026). The SNB reiterated its GDP growth forecast of "around 1%" for 2024 in the latest MPA. Looking ahead, the SNB expects unemployment to continue to rise gradually and capacity utilisation to decline somewhat further.

- With the new inflation projections, the stress on underlying inflationary pressure, and updated language in the MPA, which states that "with today’s lowering of the SNB policy rate, the SNB is able to maintain appropriate monetary conditions", we see today's cut as the end of the SNB's easing cycle. Given our estimate of the neutral rate at around 1.25%, we continue to expect them to remain on hold at the upcoming meetings, barring any unforeseen developments at home or abroad.

ING economist Peter Vanden Houte said the rate cut was not a big surprise given the recent strengthening of the franc.

"With decent Swiss GDP growth in the first quarter there was no real urgency for the SNB to cut rates, but given the still benign inflation outlook the SNB saw a window to ease," said Vanden Houte. "For the SNB it was more a rate cut because it could, not because it should."

Thomas Gitzel, chief economist at VP Bank Group, said the SNB had done the right thing by lowering rates again. Had it not, "it could have created the impression the SNB was unsure about its key interest rate reduction in March."

All aboard the cutting train

Cooling inflation allowed the SNB to become the first major central bank to lower rates at its last meeting. It has since been followed by the ECB, which last week cut rates for the first time in five years. Canadian and Swedish central banks have also started to bring down borrowing costs that were lifted to tackle the post-pandemic inflation surge. The U.S. Federal Reserve last week, however, held rates steady and pushed out the start of rate cuts to later this year.

Economists said that Thursday's cut narrowed the scope for more easing for the Swiss central bank, with one more quarter-point move in September a possibility, but not a given.

"With the latest rate cut, the policy rate is now closer to its terminal value, which we estimate at 1.00%," said Maxime Botteron, economist at UBS in Zurich, referring to a potential end point of the current easing cycle. "This means that the potential for additional cuts is limited."

The Swiss National Bank unexpectedly cut interest rates on Thursday for the second time this year, pointing to easing price pressures that allowed it to maintain its position as the front-runner in the global policy easing cycle now underway.

The Swiss franc, which had soared in the past three weeks after the shocking result from the European parliament elections hammered the Euro, weakened against other currencies and stocks gained after the central bank cut its policy rate by 25 basis points to 1.25%, as expected by two-thirds of analysts polled by Bloomberg, following a quarter-point reduction in March.

The SNB’s decision had been “finely balanced”, similar to the BOE’s decision to not cut rates, given a recent rebound in economic growth and a break in the trend of gently falling inflation in Switzerland.

“The underlying inflationary pressure has decreased again compared to the previous quarter,” SNB Chairman Thomas Jordan said. “With today’s lowering of the SNB policy rate, we are able to maintain appropriate monetary conditions.”

Jordan pointed to the SNB’s inflation forecasts, which were tweaked downwards and enabled the reduction in interest rates. While everyone knows how accurate central bank predictions are, even at the furthest end of its forecasts – covering the first quarter of 2027 – the SNB now expects inflation at 1.0%, well within its 0-2% target range.

With the updated language in the Monetary Policy Assessment, which states that “with today’s lowering of the SNB policy rate, the SNB is able to maintain appropriate monetary conditions” and an estimate of the neutral rate at around 1.25%, Goldman maintains its view that today’s cut is likely to be the end of the SNB’s easing cycle.

UBS, however, disagrees and points out that the SNB said that without this rate cut, the inflation forecasts would have been lower: “That suggests by the time of the next meeting, inflation forecasts will be lower without another cut; there was no change in the language to suggest a pause is coming up. Before this decision, UBS Economics had expected a cut in June and one more in September, to lower the base rate to 1%.“

The recent rise of the Swiss franc, driven by rising political uncertainty in Europe pushing investors towards the safe haven currency, was also highlighted by Jordan. The franc has gained 4.5% against the euro in the past month on political concerns, including the upcoming French elections, which could see the far right win power. The SNB was paying close attention, Jordan said.

“We are ready to be active on the foreign exchange market and that can go in both directions,” he told reporters.

According to Reuters, various factors lie behind Switzerland’s low price pressures, including an energy mix that makes the country less exposed to oil and gas costs, wage restraint, and protection against imported price inflation from the strong franc.

Here are the three main points on the rate cut according to Goldman:

- The Swiss National Bank (SNB) surprised consensus expectations again and delivered another 25bp cut to 1.25%, in line with our forecast. The language around FX interventions was left unchanged, with the Monetary Policy Assessment (MPA) noting that the SNB remains willing to be active in FX market “as necessary”.

- Exhibit 1 shows the new conditional inflation forecast, which was revised down slightly on account of weaker second-round effects (-0.1pp to 1.3% in 2024, -0.1pp to 1.1% in 2025, -0.1pp to 1.0% in 2026). The SNB reiterated its GDP growth forecast of “around 1%” for 2024 in the latest MPA. Looking ahead, the SNB expects unemployment to continue to rise gradually and capacity utilisation to decline somewhat further.

- With the new inflation projections, the stress on underlying inflationary pressure, and updated language in the MPA, which states that “with today’s lowering of the SNB policy rate, the SNB is able to maintain appropriate monetary conditions”, we see today’s cut as the end of the SNB’s easing cycle. Given our estimate of the neutral rate at around 1.25%, we continue to expect them to remain on hold at the upcoming meetings, barring any unforeseen developments at home or abroad.

ING economist Peter Vanden Houte said the rate cut was not a big surprise given the recent strengthening of the franc.

“With decent Swiss GDP growth in the first quarter there was no real urgency for the SNB to cut rates, but given the still benign inflation outlook the SNB saw a window to ease,” said Vanden Houte. “For the SNB it was more a rate cut because it could, not because it should.”

Thomas Gitzel, chief economist at VP Bank Group, said the SNB had done the right thing by lowering rates again. Had it not, “it could have created the impression the SNB was unsure about its key interest rate reduction in March.”

All aboard the cutting train

Cooling inflation allowed the SNB to become the first major central bank to lower rates at its last meeting. It has since been followed by the ECB, which last week cut rates for the first time in five years. Canadian and Swedish central banks have also started to bring down borrowing costs that were lifted to tackle the post-pandemic inflation surge. The U.S. Federal Reserve last week, however, held rates steady and pushed out the start of rate cuts to later this year.

Economists said that Thursday’s cut narrowed the scope for more easing for the Swiss central bank, with one more quarter-point move in September a possibility, but not a given.

“With the latest rate cut, the policy rate is now closer to its terminal value, which we estimate at 1.00%,” said Maxime Botteron, economist at UBS in Zurich, referring to a potential end point of the current easing cycle. “This means that the potential for additional cuts is limited.”

Loading…