Well, it's official: the inflation peak of the post-covid era is now behind us (that we will get another reflationary ascent is a question of when not if, but for now it's over the horizon), and as BBG's Chris Antsey writes, today's 0.2% reading for core monthly CPI takes us back to “old normal” for now. That was the most common figure for this indicator before the pandemic. In fact, for 53 straight months until Covid-19 hit in spring 2020, the median forecast in Bloomberg surveys was consistently 0.2%. More than four years. Furthermore, digging into the numbers shows that core CPI ex-shelter was actually a deflationary -0.13%, and since shelter/OER tracks market data with a real-time lag, the US is now in disinflation and Powell should be cutting rates tomorrow (spoiler alert: that won't happen, and instead the Fed will push the US economy into an even deeper recession).

Meanwhile, just as Goldman wrote in its CPI preview (which everyone should have read as it predicted today's move to a tee), the weakness was broad based, and not just food and energy (although there was a bizarre 0.2% M/M increase in apparel prices which makes no sense since online price data from Adobe shows a 15.5% decline in apparel prices over the course of November on a not-seasonally-adjusted basis).

Of course, the question now is what does Powell make of all of this, and until we get the answer in a little over 24 hours, here is a snapshot of kneejerk reactions from Wall Street's best and brightest.

Peter Tchir, chief strategist at Academy Securities

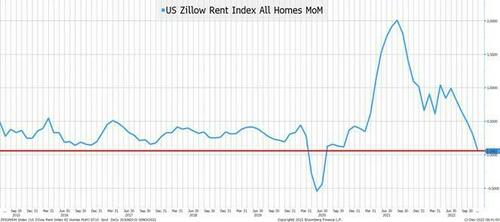

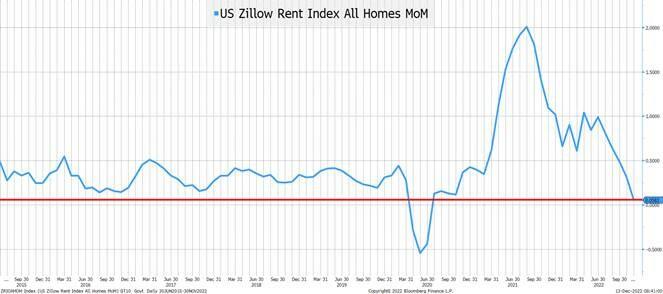

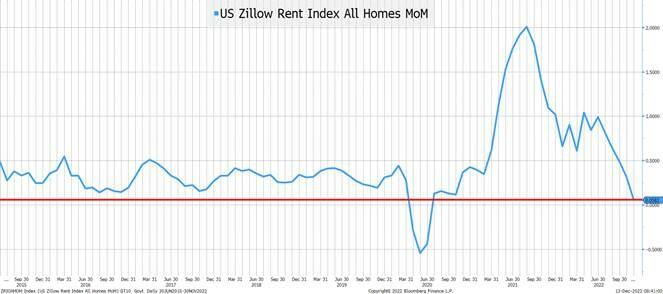

"Many say 50 for next meeting. I’m betting 0, but maybe it will be 25. I’m in the camp that tomorrow is the last hike in this cycle.... These low CPI prints were still too high based on the 0.6 increase in shelter (largely owners equivalent rent). OER was up 0.7, just off of last month’s allegedly record pace. Zillow, which publishes some data that I find more credible, had the lowest monthly rent increase, going back to 2015 (with the exception of the COVID lockdown). Just look at the chart! Zillow peaked in the summer of 2021 which is far more logical than peaking in October of 2022 (with November, apparently a close second)"

Omair Sharif, founder of Inflation Insights

“Today’s 0.2% core print might overstate the softness in core inflation modestly, but I’ll repeat what I said after the October CPI: This is not an outlier. In fact, today’s report showed a fairly broad-based slowdown, and core CPI ex-shelter was -0.13%.”

Florian Ielpo, head of macro research at Lombard Odier Asset Management

"This is the first time core inflation is showing a decline. This is consistent with a large cross-section of data in the US now: Inflation in the US is likely to be a problem of the past.”

Chris Antsey, Fed reporter at Bloomberg News

"This should give Powell some confidence tomorrow if he had planned on signaling a further step down in the magnitude of rate hikes to 25 basis points in February, after the 50 basis points that’s expected on Wednesday....The one proviso for the Fed is that this risk-asset rally undercuts the Fed’s tightening campaign. And indeed they’re not finished yet, with multiple rate hikes yet to come. To the extent that financial conditions ease up, that would be counterproductive."

Ira Jersey, Bloomberg Intelligence Chief US Rates Strategist

"The better-than-expected core CPI number gives the Fed the cover it needs to signal hikes will be coming to an end. However, we still think the Fed will signal it will maintain rates near the peak for longer than the market is pricing, which means the front-end knee-jerk rally may not have legs, while the long end may retest recent yield lows flattening the curve a bit further.”

Matthew Luzzetti, strategist at Deutsche Bank

"while the CPI print is cooler than expected, the Fed will still be careful. Inflation, after all, is still high. A big question is how PCE and CPI will converge a lot next year."

Dave Lutz, JonesTrading:

"The print says one thing: The worst of inflation has likely passed. This validates an anticipated slowing in the pace of Fed interest-rate hikes."

Seema Shah, global strategist at Principal Asset Management

“It also raises hopes that the inflation surge may actually be tamed within the next 12 months. Certainly, with important components such as shelter inflation and core goods inflation moving lower, it is reasonable to expect inflation to continue falling over coming months.”

April LaRusse, head of investment specialists at Insight Investments

“The slightly softer CPI numbers are almost entirely driven by the retracement we have seen in food and energy prices. With global growth decelerating it is not a surprise to see these components rolling over first. The key thing to watch is core service inflation which has yet to moderate. Without services and wages under control, we are not out of the woods yet on inflationary risks.”

Rubeela Farooqi, chief US economist at High Frequency Economics

"Overall, prices are moving in the right direction, although annual rates of change remain elevated, well above the 2% target. In terms of the upcoming rate decision, a deceleration will be welcome news and will support a slower pace of rate hikes going forward.We expect the FOMC to raise the target range by 50 basis points tomorrow. Further sustained improvement over coming months could see the Fed downshift further over coming meetings.”

Ellen Zentner, chief economist at Morgan Stanley

"From here on out the labor market may now become the key metric, rather than CPI: With the downtrend in inflation becoming entrenched, the FOMC can set its sights squarely on the labor market. In our forecasts, a slowdown in jobs growth over the coming months sets the stage for, first, a further step down to a 25 basis-point increase in the February meeting. As jobs growth trends towards the 100,000 mark, we expect no further interest rate hikes at the March FOMC, leaving the peak fed funds rate at 4.625%.”

Ian Lyngen, rates strategist at BMO Capital Markets

“The knee-jerk rally that has followed resonates with the peak-inflation narrative gaining steam. We’re on board with the steepening in 5s/30s as this print suggests a materially higher terminal rate may not be required, and from here this afternoon’s long bond auction will serve as a minor distraction ahead of the Fed tomorrow and the all-but-assured 50 bp hike.”

Katherine Judge, economist at CIBC Capital Markets

"The deceleration in price pressures was concentrated in a few components, and the labor market remains tight. The softer core reading was driven by an easing in core goods prices, specifically used cars, reflecting supply-chain improvements, and drops in medical care and transportation services. That masked price pressures in core services, with the shelter sub-index continuing to increase strongly, although the pace of monthly shelter increases subsided.”

Phillip Neuhart, economist at First Citizens Bank Wealth Management

“For the second consecutive month, inflation came in below expectations. This is good news for markets and the Federal Reserve. Should this downtrend persist, it allows the Fed to slow the pace of interest rate hikes and eventually pause in the first half of next year.”

Jason Pride, Glenmede

“Investors should be careful not to over-extrapolate these results and temper their expectations for a premature pivot from the Fed. Consumer inflation is still far from the Fed’s price stability goals, and the 1970s provide case-in-point as to the risks of claiming victory on inflation too early.”

Chris Zaccarelli, chief investment officer at Independent Advisor Alliance

“The market was clearly offside with bearish positioning leaving many shorts vulnerable to a downside surprise on inflation, which we now have. Stocks are going to rally and the path of least resistance will be higher with so many people forecasting an imminent recession. Just as inflation has remained higher for longer, it is also possible that the economy remains resilient for longer.”

Paul Ashworth, Capital Economics:

“Stick a fork in it, inflation is done. The 0.2% m/m increase in core consumer prices in November provides strong support to our long-held view that mounting disinflation will soon persuade the Fed to move to the side line after one 25 basis-point hike in early February.”

Source: Bloomberg

Well, it’s official: the inflation peak of the post-covid era is now behind us (that we will get another reflationary ascent is a question of when not if, but for now it’s over the horizon), and as BBG’s Chris Antsey writes, today’s 0.2% reading for core monthly CPI takes us back to “old normal” for now. That was the most common figure for this indicator before the pandemic. In fact, for 53 straight months until Covid-19 hit in spring 2020, the median forecast in Bloomberg surveys was consistently 0.2%. More than four years. Furthermore, digging into the numbers shows that core CPI ex-shelter was actually a deflationary -0.13%, and since shelter/OER tracks market data with a real-time lag, the US is now in disinflation and Powell should be cutting rates tomorrow (spoiler alert: that won’t happen, and instead the Fed will push the US economy into an even deeper recession).

Meanwhile, just as Goldman wrote in its CPI preview (which everyone should have read as it predicted today’s move to a tee), the weakness was broad based, and not just food and energy (although there was a bizarre 0.2% M/M increase in apparel prices which makes no sense since online price data from Adobe shows a 15.5% decline in apparel prices over the course of November on a not-seasonally-adjusted basis).

Of course, the question now is what does Powell make of all of this, and until we get the answer in a little over 24 hours, here is a snapshot of kneejerk reactions from Wall Street’s best and brightest.

Peter Tchir, chief strategist at Academy Securities

“Many say 50 for next meeting. I’m betting 0, but maybe it will be 25. I’m in the camp that tomorrow is the last hike in this cycle…. These low CPI prints were still too high based on the 0.6 increase in shelter (largely owners equivalent rent). OER was up 0.7, just off of last month’s allegedly record pace. Zillow, which publishes some data that I find more credible, had the lowest monthly rent increase, going back to 2015 (with the exception of the COVID lockdown). Just look at the chart! Zillow peaked in the summer of 2021 which is far more logical than peaking in October of 2022 (with November, apparently a close second)”

Omair Sharif, founder of Inflation Insights

“Today’s 0.2% core print might overstate the softness in core inflation modestly, but I’ll repeat what I said after the October CPI: This is not an outlier. In fact, today’s report showed a fairly broad-based slowdown, and core CPI ex-shelter was -0.13%.”

Florian Ielpo, head of macro research at Lombard Odier Asset Management

“This is the first time core inflation is showing a decline. This is consistent with a large cross-section of data in the US now: Inflation in the US is likely to be a problem of the past.”

Chris Antsey, Fed reporter at Bloomberg News

“This should give Powell some confidence tomorrow if he had planned on signaling a further step down in the magnitude of rate hikes to 25 basis points in February, after the 50 basis points that’s expected on Wednesday….The one proviso for the Fed is that this risk-asset rally undercuts the Fed’s tightening campaign. And indeed they’re not finished yet, with multiple rate hikes yet to come. To the extent that financial conditions ease up, that would be counterproductive.”

Ira Jersey, Bloomberg Intelligence Chief US Rates Strategist

“The better-than-expected core CPI number gives the Fed the cover it needs to signal hikes will be coming to an end. However, we still think the Fed will signal it will maintain rates near the peak for longer than the market is pricing, which means the front-end knee-jerk rally may not have legs, while the long end may retest recent yield lows flattening the curve a bit further.”

Matthew Luzzetti, strategist at Deutsche Bank

“while the CPI print is cooler than expected, the Fed will still be careful. Inflation, after all, is still high. A big question is how PCE and CPI will converge a lot next year.”

Dave Lutz, JonesTrading:

“The print says one thing: The worst of inflation has likely passed. This validates an anticipated slowing in the pace of Fed interest-rate hikes.”

Seema Shah, global strategist at Principal Asset Management

“It also raises hopes that the inflation surge may actually be tamed within the next 12 months. Certainly, with important components such as shelter inflation and core goods inflation moving lower, it is reasonable to expect inflation to continue falling over coming months.”

April LaRusse, head of investment specialists at Insight Investments

“The slightly softer CPI numbers are almost entirely driven by the retracement we have seen in food and energy prices. With global growth decelerating it is not a surprise to see these components rolling over first. The key thing to watch is core service inflation which has yet to moderate. Without services and wages under control, we are not out of the woods yet on inflationary risks.”

Rubeela Farooqi, chief US economist at High Frequency Economics

“Overall, prices are moving in the right direction, although annual rates of change remain elevated, well above the 2% target. In terms of the upcoming rate decision, a deceleration will be welcome news and will support a slower pace of rate hikes going forward.We expect the FOMC to raise the target range by 50 basis points tomorrow. Further sustained improvement over coming months could see the Fed downshift further over coming meetings.”

Ellen Zentner, chief economist at Morgan Stanley

“From here on out the labor market may now become the key metric, rather than CPI: With the downtrend in inflation becoming entrenched, the FOMC can set its sights squarely on the labor market. In our forecasts, a slowdown in jobs growth over the coming months sets the stage for, first, a further step down to a 25 basis-point increase in the February meeting. As jobs growth trends towards the 100,000 mark, we expect no further interest rate hikes at the March FOMC, leaving the peak fed funds rate at 4.625%.”

Ian Lyngen, rates strategist at BMO Capital Markets

“The knee-jerk rally that has followed resonates with the peak-inflation narrative gaining steam. We’re on board with the steepening in 5s/30s as this print suggests a materially higher terminal rate may not be required, and from here this afternoon’s long bond auction will serve as a minor distraction ahead of the Fed tomorrow and the all-but-assured 50 bp hike.”

Katherine Judge, economist at CIBC Capital Markets

“The deceleration in price pressures was concentrated in a few components, and the labor market remains tight. The softer core reading was driven by an easing in core goods prices, specifically used cars, reflecting supply-chain improvements, and drops in medical care and transportation services. That masked price pressures in core services, with the shelter sub-index continuing to increase strongly, although the pace of monthly shelter increases subsided.”

Phillip Neuhart, economist at First Citizens Bank Wealth Management

“For the second consecutive month, inflation came in below expectations. This is good news for markets and the Federal Reserve. Should this downtrend persist, it allows the Fed to slow the pace of interest rate hikes and eventually pause in the first half of next year.”

Jason Pride, Glenmede

“Investors should be careful not to over-extrapolate these results and temper their expectations for a premature pivot from the Fed. Consumer inflation is still far from the Fed’s price stability goals, and the 1970s provide case-in-point as to the risks of claiming victory on inflation too early.”

Chris Zaccarelli, chief investment officer at Independent Advisor Alliance

“The market was clearly offside with bearish positioning leaving many shorts vulnerable to a downside surprise on inflation, which we now have. Stocks are going to rally and the path of least resistance will be higher with so many people forecasting an imminent recession. Just as inflation has remained higher for longer, it is also possible that the economy remains resilient for longer.”

Paul Ashworth, Capital Economics:

“Stick a fork in it, inflation is done. The 0.2% m/m increase in core consumer prices in November provides strong support to our long-held view that mounting disinflation will soon persuade the Fed to move to the side line after one 25 basis-point hike in early February.”

Source: Bloomberg

Loading…