Shares of Target jumped in premarket trading in New York after it reported adjusted earnings per share for the third quarter that beat Wall Street expectations. There were fewer markdowns and more efficiencies in inventory management following the big-box retailer's inventory buildups earlier this year.

Earnings per share for the quarter (ending Oct. 28) came in at $2.10 per share, beating Wall Street's estimate of $1.47. This was due primarily to a 14% reduction in inventory from a year ago. The company largely attributed the beat to "disciplined inventory and expense management."

However, comparable sales fell 4.9% for the second consecutive quarter as consumer spending on discretionary items weakened. That was the second-largest drop since 2009.

Here's a snapshot of the third quarter results:

-

Adjusted EPS $2.10 vs. $1.54 y/y, estimate $1.47 (Bloomberg Consensus)

-

Comparable sales -4.9% vs. +2.7% y/y, estimate -5.22%

-

Comp digital sales -6% vs. +0.3% y/y, estimate -10.3%

-

Sales $25.00 billion, -4.3% y/y, estimate $24.88 billion

-

Gross margin 27.4% vs. 24.7% y/y, estimate 26.3%

-

Ebit $1.34 billion, +30% y/y

-

Ebitda $2.06 billion, estimate $1.67 billion

-

Customer transactions -4.1% vs. +1.4% y/y

-

Average transaction amount -0.8% vs. +1.3% y/y, estimate -1.37%

-

Digital sales as share of total sales 16.8% vs. 17.1% y/y

-

Total stores 1,956, +0.8% y/y, estimate 1,965

-

Operating margin 5.2%, estimate 3.94%

-

SG&A expense $5.32 billion, +1.9% y/y, estimate $5.35 billion

-

Store comparable sales -4.6% vs. +3.2% y/y, estimate -4.91%

-

Stores originated sales 83.2% vs. 82.9% y/y, estimate 83.4%

-

Operating income $1.32 billion, +29% y/y, estimate $1 billion

For the fourth quarter, Target has adjusted EPS in a broad range, between $1.90 to $2.60, which the Bloomberg Consensus among Wall Street professionals is around $2.23.

- Sees adjusted EPS $1.90 to $2.60, estimate $2.23

Following the earnings report, Kate McShane, a retail analyst with Goldman Sachs, told clients:

"We expect the stock to track higher given the 3Q beat, noting the strong margin performance likely reinforces the longer term operating margin recovery opportunity to 6%+. On the call, we are interested in the cadence of SSS throughout 3Q; QTD trends by category; the relative impact of the gross margin drivers, including markdowns, mix, and shrink; the view of inflation; and the company's promotional."

McShane noted:

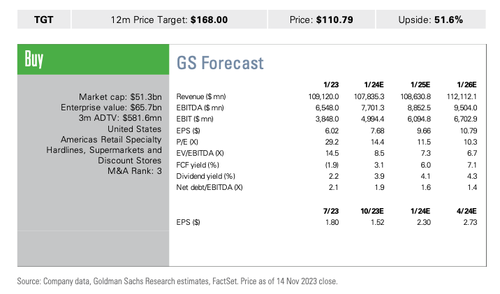

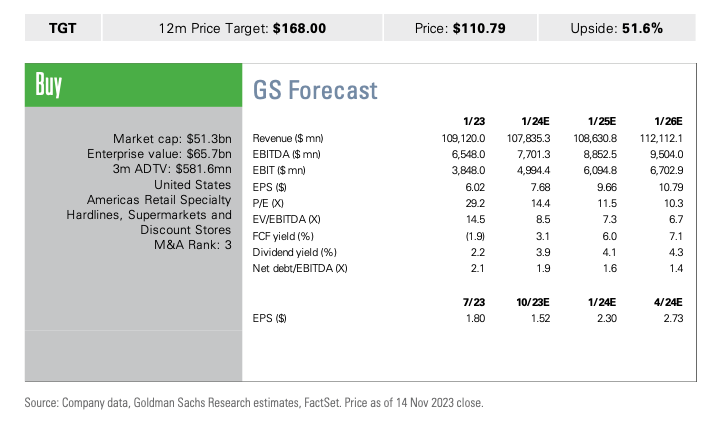

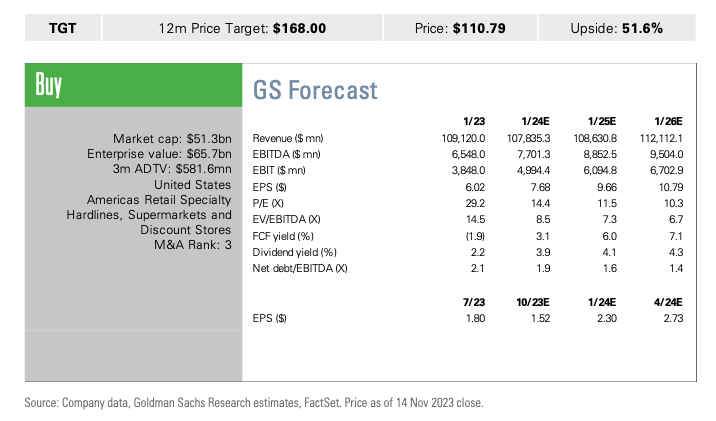

"We are Buy rated on TGT with a 12-month price target of $168, based on our risk-reward framework with downside/base/upside relative P/E multiples of 80%/90%/100%."

However, she outlined several TGT downside risks:

Traffic and sales trends decelerate due to weakness in consumer spending;

Inflationary pressures related to product costs, freight/transportation, and/or wages;

The competitive environment forces TGT to compete more aggressively on price;

Margins come under pressure from omni-channel, supply chain investments, and mix shift.

More from the note:

Target shares have plunged more than 25% year-to-date. The company first warned about a consumer slowdown in May. Then, it was battered by a consumer boycott over selling 'woke' clothing to children. Shares in the premarket jumped as much as 15%.

Target earnings come as several large retailers, like Walmart, Macy's, and Gap, are expected to report earnings on Thursday. Also, comments from management teams will help investors gauge the strength of the consumer ahead of the holiday shopping season.

Shares of Target jumped in premarket trading in New York after it reported adjusted earnings per share for the third quarter that beat Wall Street expectations. There were fewer markdowns and more efficiencies in inventory management following the big-box retailer’s inventory buildups earlier this year.

Earnings per share for the quarter (ending Oct. 28) came in at $2.10 per share, beating Wall Street’s estimate of $1.47. This was due primarily to a 14% reduction in inventory from a year ago. The company largely attributed the beat to “disciplined inventory and expense management.”

However, comparable sales fell 4.9% for the second consecutive quarter as consumer spending on discretionary items weakened. That was the second-largest drop since 2009.

Here’s a snapshot of the third quarter results:

-

Adjusted EPS $2.10 vs. $1.54 y/y, estimate $1.47 (Bloomberg Consensus)

-

Comparable sales -4.9% vs. +2.7% y/y, estimate -5.22%

-

Comp digital sales -6% vs. +0.3% y/y, estimate -10.3%

-

Sales $25.00 billion, -4.3% y/y, estimate $24.88 billion

-

Gross margin 27.4% vs. 24.7% y/y, estimate 26.3%

-

Ebit $1.34 billion, +30% y/y

-

Ebitda $2.06 billion, estimate $1.67 billion

-

Customer transactions -4.1% vs. +1.4% y/y

-

Average transaction amount -0.8% vs. +1.3% y/y, estimate -1.37%

-

Digital sales as share of total sales 16.8% vs. 17.1% y/y

-

Total stores 1,956, +0.8% y/y, estimate 1,965

-

Operating margin 5.2%, estimate 3.94%

-

SG&A expense $5.32 billion, +1.9% y/y, estimate $5.35 billion

-

Store comparable sales -4.6% vs. +3.2% y/y, estimate -4.91%

-

Stores originated sales 83.2% vs. 82.9% y/y, estimate 83.4%

-

Operating income $1.32 billion, +29% y/y, estimate $1 billion

For the fourth quarter, Target has adjusted EPS in a broad range, between $1.90 to $2.60, which the Bloomberg Consensus among Wall Street professionals is around $2.23.

- Sees adjusted EPS $1.90 to $2.60, estimate $2.23

Following the earnings report, Kate McShane, a retail analyst with Goldman Sachs, told clients:

“We expect the stock to track higher given the 3Q beat, noting the strong margin performance likely reinforces the longer term operating margin recovery opportunity to 6%+. On the call, we are interested in the cadence of SSS throughout 3Q; QTD trends by category; the relative impact of the gross margin drivers, including markdowns, mix, and shrink; the view of inflation; and the company’s promotional.”

McShane noted:

“We are Buy rated on TGT with a 12-month price target of $168, based on our risk-reward framework with downside/base/upside relative P/E multiples of 80%/90%/100%.”

However, she outlined several TGT downside risks:

Traffic and sales trends decelerate due to weakness in consumer spending;

Inflationary pressures related to product costs, freight/transportation, and/or wages;

The competitive environment forces TGT to compete more aggressively on price;

Margins come under pressure from omni-channel, supply chain investments, and mix shift.

More from the note:

Target shares have plunged more than 25% year-to-date. The company first warned about a consumer slowdown in May. Then, it was battered by a consumer boycott over selling ‘woke’ clothing to children. Shares in the premarket jumped as much as 15%.

Target earnings come as several large retailers, like Walmart, Macy’s, and Gap, are expected to report earnings on Thursday. Also, comments from management teams will help investors gauge the strength of the consumer ahead of the holiday shopping season.

Loading…