Authored by Mike Shedlock via MishTalk.com,

Jerome Powell and the St. Louis Fed are both concerned over inflation expectations. Let's investigate.

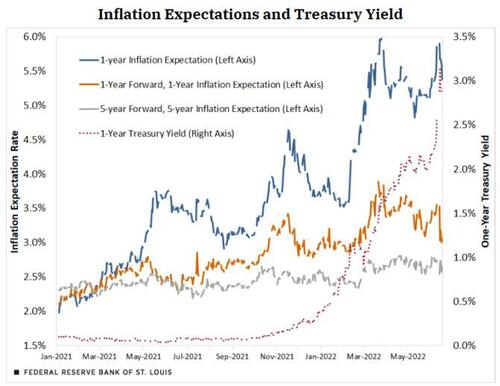

What Do Financial Markets Say about Future Inflation?

From the Federal Reserve Bank of St. Louis, please consider What Do Financial Markets Say about Future Inflation? by YiLi Chien and Julie Bennett.

The Importance of Inflation Expectation

The effectiveness of monetary policy hinges critically on inflation expectations. If economic agents, such as households and firms, expect higher inflation in the future, the rational reaction is to purchase goods and services right away in order to avoid higher future prices. As a result, the demand for goods and services immediately rises and so does the price level, which results in higher inflation right away. Hence, the Federal Reserve needs to anchor economic agents’ long-term inflation expectations close to the inflation target in order to effectively combat inflation. This blog post looks at the recent movements in so-called market-based inflation expectations for various time horizons.

....

Conclusion

In short, according to the inflation swap data, market participants believe the Federal Reserve can and will control the high inflation rate, despite price increases being more persistent than previously thought. The well-anchored longer-term inflation expectation provides additional supporting evidence of this.

I will rebut this nonsense again, but first let's consider another article on the alleged importance of inflation expectations.

The Strange Art of Asking People How Much Inflation They Expect

Please consider The Strange Art of Asking People How Much Inflation They Expect

“By about what percent do you expect prices to go up or down on the average, during the next 12 months?”

The answers people give to this question—this exact question—produce one of the most important numbers for the U.S. economy.

It’s the question the University of Michigan asks respondents to its Survey of Consumers. Because that survey is the longest-running such survey of consumer attitudes, dating back to 1946, its data about price increases have become the benchmark for economists who obsess over expectations of inflation.

When Federal Reserve Chairman Jerome Powell said last week that the Fed was raising interest rates by 0.75 percentage point, he cited an uptick in the responses people gave to the Michigan survey, saying, “It was quite eye-catching and we noticed that.”

Crucial Variable Says Gregory Mankiw

“Expected inflation is a crucial variable, but it’s probably one of the hardest of the crucial variables to measure,” said Harvard University economist Gregory Mankiw.

The first quirk is that many people have only a vague idea of how much prices will rise, and tend to respond with large (sometimes implausibly large) round numbers: 5%, 10%, 15%, even 50%. In other words, people don’t gravitate toward a common assessment—they disagree sharply about how much inflation to expect, as Mr. Mankiw puts it.

Second, partisanship colors people’s views. This is a well-known trend when assessing measures of consumer confidence: Democrats become extremely optimistic, and Republicans extremely pessimistic, the moment a Democratic president is elected. And vice versa. It has recently come to hang over inflation data, too.

The question “by about what percent per year do you expect prices to go (up/down) on the average, during the next 5 to 10 years?” is followed by a careful script to ensure that people are providing an estimate of annual increases, not cumulative.

Richard Curtin, former head of the University of Michigan survey, says the tendency to gravitate toward large, round numbers is a genuine reflection of how people think.

He sees a bit of condescension from economists who are skeptical that consumers could have well-formed views about inflation.

I Condemn the Surveys and the Economists

Q: Why?

A: The premise is ridiculous.

Q: What premise?

A: "If economic agents, such as households and firms, expect higher inflation in the future, the rational reaction is to purchase goods and services right away in order to avoid higher future prices."

That actually seems logical and to a meaningless degree it can temporarily happen.

Gasoline Example

Suppose a person thinks the price of gasoline will rise. That person then fills up his tank when it is half empty rather then three-quarters empty.

The person buys no more gas than he would otherwise, and perhaps even less by driving less. There is no place to store gas other the car.

Most people will not bother with the inconvenience of filling up twice as often to save a few cents, and it is meaningless if they do. No additional gas is purchased.

Toilet Paper Example

Similarly, we have seen a rush on toilet paper on fears of supply, causing temporary shortages, but what then?

Does the price of toilet paper keep rising forever? Or after some number of roll hoarding does the situation self-correct?

Medical Expense Example

If consumers think the cost of a heart surgery will rise dramatically next year, will they rush out and have two of them now to avoid the price hike?

Clearly the answer is no.

Rent Example

Rent gets to the heart of the matter. It is over 31 percent of the CPI.

What can consumers do about rising rent prices? Will they rush out and rent two houses if they expect an increase?

No, they won't do that, but they might rush to buy a home. Alas, neither the Fed nor economists see home price inflation as inflation.

Curiously, the rush to buy homes (asset prices in general) is the one place where expectations matter. But economists ignore that, focusing on what doesn't.

Please consider Why Do We Think That Inflation Expectations Matter for Inflation? (And Should We?) by Jeremy B. Rudd at the Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board.

Policy Errors

Economists and economic policymakers believe that households’ and firms’ expectations of future inflation are a key determinant of actual inflation. A review of the relevant theoretical and empirical literature suggests that this belief rests on extremely shaky foundations, and a case is made that adhering to it uncritically could easily lead to serious policy errors.

The study also debunked the highly touted Phillips Curve.

Here are a few direct quotes.

-

The direct evidence for an expected inflation channel was never very strong.

-

It is an irony of history that, when Phelps and Friedman sought to justify their proposed theoretical specifications, they were faced with the uncomfortable fact that empirical Phillips curves appeared to be remarkably stable.

-

These techniques are similar in spirit to those employed in the 1990s to estimate new-Keynesian models; hence, they suffer from the same sorts of problems—discussed below—that attend empirical estimates of those models.

-

Friedman’s derivation of the expectations-augmented Phillips curve implies that the real product wage should be strongly countercyclical (recall that in this model firms are always assumed to be on their labor demand curves). In particular, Friedman states as a matter of fact that “. . . selling prices of products typically respond to an unanticipated rise in demand faster than prices of factors of production,” which would in turn imply the empirical prediction that the price Phillips curve is steeper than the wage Phillips curve. However, in U.S. data this prediction is completely at odds with the evidence.

-

Most standard tests of the new-Keynesian Phillips curve suffer from such severe potential misspecification issues or such profound weak identification problems as to provide no evidence one way or the other regarding the importance of expectations (much the same statement applies to empirical tests that use survey measures of expected inflation).

-

What little we know about firms’ price-setting behavior suggests that many tend to respond to cost increases only when they actually show up and are visible to their customers, rather than in a preemptive fashion.

Common Sense and Practical Examples

Common sense and practical examples suggest that inflation expectations theory is ass backward.

So much of the CPI is nondiscretionary that it's difficult to impossible for CPI expectations to matter.

Yet, economists focus on expectations that don't matter and ignore the expectations that do matter, namely asset prices!

I have written about this several times previously, two of them before I even found the Fed study supporting my view.

Asset Irony

People will rush to buy stocks in a bubble if they think prices will rise. They will hold off buying stocks if they expect prices will go down.

People will buy houses to rent or fix up if they think home prices will rise. They will hold off housing speculation if they expect prices will drop.

The very things where expectations do matter are the very things the Fed ignores.

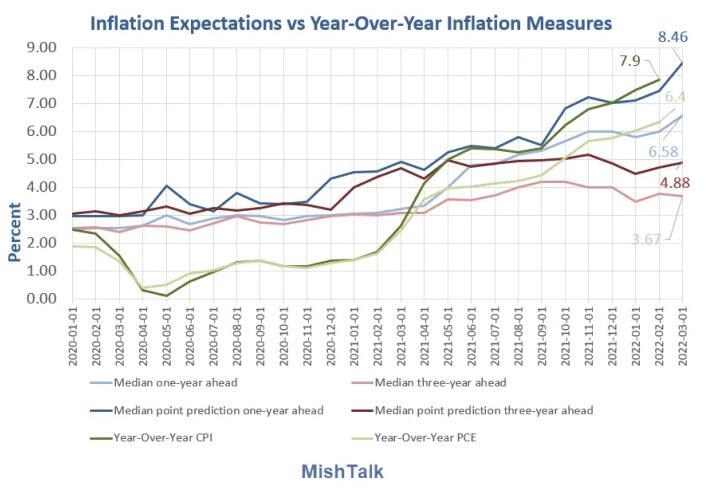

Hello Fed, Inflation Expectations Are Unglued, No Longer Well Anchored

Inflation Expectations data from New York Fed, chart by Mish

On April 11, I commented Hello Fed, Inflation Expectations Are Unglued, No Longer Well Anchored

The New York Fed survey already shows inflation expectations are not anchored.

Even the three-year median point projection is 4.88%, well over the Fed's target rate of 2.00%.

Powell was shocked that the University of Michigan survey showed the same thing.

I commented "It's a good thing that inflation expectations are a blatantly ridiculous concept. Even the Fed's own research papers make that conclusion."

It's a good thing inflation expectations are not self-fulfilling because expectations are now unglued.

Fed Studies Debunk the Phillips Curve

Both studies were done by Fed staffers.

Yet, Fed Chairs Janet Yellen and Jerome Powell did not believe the Fed's own study.

Stupidity Still Well Anchored

You have to be trained to believe in nonsense and stick with it despite all evidence to the contrary.

Yet, Powell and the St. Louis Fed trust their disproved inflation expectations models. It has led to policy errors already and will lead to more of them.

This is group think in action. There is no diversity of thought at the Fed.

Historical Perspective on CPI Deflations: How Damaging are They?

Regarding policy errors and the accurate warning by the Monetary Affairs Division of the Federal Reserve Board, please consider Historical Perspective on CPI Deflations: How Damaging are They?

A BIS study concluded "Deflation may actually boost output. Lower prices increase real incomes and wealth. And they may also make export goods more competitive."

Indeed, that must be the case as more goods for less money by default improves standards of living.

The Fed was hell bent on reducing standards of living via inflation. Now they struggle to undo the inflation and asset bubble consequences they created.

The Fed is the problem, not the solution.

* * *

Authored by Mike Shedlock via MishTalk.com,

Jerome Powell and the St. Louis Fed are both concerned over inflation expectations. Let’s investigate.

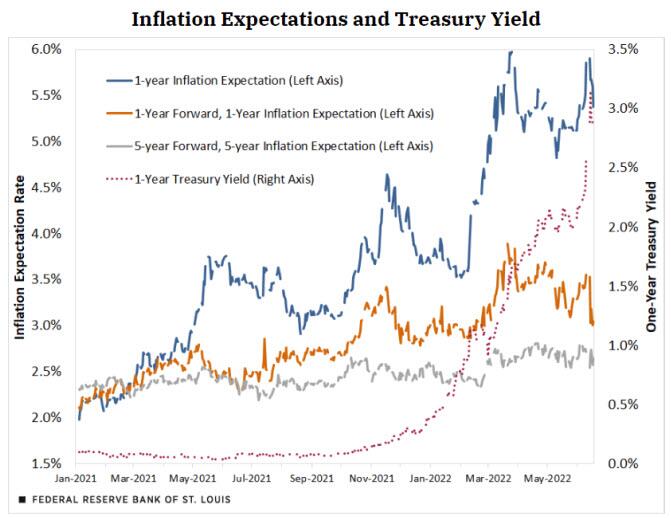

What Do Financial Markets Say about Future Inflation?

From the Federal Reserve Bank of St. Louis, please consider What Do Financial Markets Say about Future Inflation? by YiLi Chien and Julie Bennett.

The Importance of Inflation Expectation

The effectiveness of monetary policy hinges critically on inflation expectations. If economic agents, such as households and firms, expect higher inflation in the future, the rational reaction is to purchase goods and services right away in order to avoid higher future prices. As a result, the demand for goods and services immediately rises and so does the price level, which results in higher inflation right away. Hence, the Federal Reserve needs to anchor economic agents’ long-term inflation expectations close to the inflation target in order to effectively combat inflation. This blog post looks at the recent movements in so-called market-based inflation expectations for various time horizons.

….

Conclusion

In short, according to the inflation swap data, market participants believe the Federal Reserve can and will control the high inflation rate, despite price increases being more persistent than previously thought. The well-anchored longer-term inflation expectation provides additional supporting evidence of this.

I will rebut this nonsense again, but first let’s consider another article on the alleged importance of inflation expectations.

The Strange Art of Asking People How Much Inflation They Expect

Please consider The Strange Art of Asking People How Much Inflation They Expect

“By about what percent do you expect prices to go up or down on the average, during the next 12 months?”

The answers people give to this question—this exact question—produce one of the most important numbers for the U.S. economy.

It’s the question the University of Michigan asks respondents to its Survey of Consumers. Because that survey is the longest-running such survey of consumer attitudes, dating back to 1946, its data about price increases have become the benchmark for economists who obsess over expectations of inflation.

When Federal Reserve Chairman Jerome Powell said last week that the Fed was raising interest rates by 0.75 percentage point, he cited an uptick in the responses people gave to the Michigan survey, saying, “It was quite eye-catching and we noticed that.”

Crucial Variable Says Gregory Mankiw

“Expected inflation is a crucial variable, but it’s probably one of the hardest of the crucial variables to measure,” said Harvard University economist Gregory Mankiw.

The first quirk is that many people have only a vague idea of how much prices will rise, and tend to respond with large (sometimes implausibly large) round numbers: 5%, 10%, 15%, even 50%. In other words, people don’t gravitate toward a common assessment—they disagree sharply about how much inflation to expect, as Mr. Mankiw puts it.

Second, partisanship colors people’s views. This is a well-known trend when assessing measures of consumer confidence: Democrats become extremely optimistic, and Republicans extremely pessimistic, the moment a Democratic president is elected. And vice versa. It has recently come to hang over inflation data, too.

The question “by about what percent per year do you expect prices to go (up/down) on the average, during the next 5 to 10 years?” is followed by a careful script to ensure that people are providing an estimate of annual increases, not cumulative.

Richard Curtin, former head of the University of Michigan survey, says the tendency to gravitate toward large, round numbers is a genuine reflection of how people think.

He sees a bit of condescension from economists who are skeptical that consumers could have well-formed views about inflation.

I Condemn the Surveys and the Economists

Q: Why?

A: The premise is ridiculous.

Q: What premise?

A: “If economic agents, such as households and firms, expect higher inflation in the future, the rational reaction is to purchase goods and services right away in order to avoid higher future prices.”

That actually seems logical and to a meaningless degree it can temporarily happen.

Gasoline Example

Suppose a person thinks the price of gasoline will rise. That person then fills up his tank when it is half empty rather then three-quarters empty.

The person buys no more gas than he would otherwise, and perhaps even less by driving less. There is no place to store gas other the car.

Most people will not bother with the inconvenience of filling up twice as often to save a few cents, and it is meaningless if they do. No additional gas is purchased.

Toilet Paper Example

Similarly, we have seen a rush on toilet paper on fears of supply, causing temporary shortages, but what then?

Does the price of toilet paper keep rising forever? Or after some number of roll hoarding does the situation self-correct?

Medical Expense Example

If consumers think the cost of a heart surgery will rise dramatically next year, will they rush out and have two of them now to avoid the price hike?

Clearly the answer is no.

Rent Example

Rent gets to the heart of the matter. It is over 31 percent of the CPI.

What can consumers do about rising rent prices? Will they rush out and rent two houses if they expect an increase?

No, they won’t do that, but they might rush to buy a home. Alas, neither the Fed nor economists see home price inflation as inflation.

Curiously, the rush to buy homes (asset prices in general) is the one place where expectations matter. But economists ignore that, focusing on what doesn’t.

Please consider Why Do We Think That Inflation Expectations Matter for Inflation? (And Should We?) by Jeremy B. Rudd at the Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board.

Policy Errors

Economists and economic policymakers believe that households’ and firms’ expectations of future inflation are a key determinant of actual inflation. A review of the relevant theoretical and empirical literature suggests that this belief rests on extremely shaky foundations, and a case is made that adhering to it uncritically could easily lead to serious policy errors.

The study also debunked the highly touted Phillips Curve.

Here are a few direct quotes.

-

The direct evidence for an expected inflation channel was never very strong.

-

It is an irony of history that, when Phelps and Friedman sought to justify their proposed theoretical specifications, they were faced with the uncomfortable fact that empirical Phillips curves appeared to be remarkably stable.

-

These techniques are similar in spirit to those employed in the 1990s to estimate new-Keynesian models; hence, they suffer from the same sorts of problems—discussed below—that attend empirical estimates of those models.

-

Friedman’s derivation of the expectations-augmented Phillips curve implies that the real product wage should be strongly countercyclical (recall that in this model firms are always assumed to be on their labor demand curves). In particular, Friedman states as a matter of fact that “. . . selling prices of products typically respond to an unanticipated rise in demand faster than prices of factors of production,” which would in turn imply the empirical prediction that the price Phillips curve is steeper than the wage Phillips curve. However, in U.S. data this prediction is completely at odds with the evidence.

-

Most standard tests of the new-Keynesian Phillips curve suffer from such severe potential misspecification issues or such profound weak identification problems as to provide no evidence one way or the other regarding the importance of expectations (much the same statement applies to empirical tests that use survey measures of expected inflation).

-

What little we know about firms’ price-setting behavior suggests that many tend to respond to cost increases only when they actually show up and are visible to their customers, rather than in a preemptive fashion.

Common Sense and Practical Examples

Common sense and practical examples suggest that inflation expectations theory is ass backward.

So much of the CPI is nondiscretionary that it’s difficult to impossible for CPI expectations to matter.

Yet, economists focus on expectations that don’t matter and ignore the expectations that do matter, namely asset prices!

I have written about this several times previously, two of them before I even found the Fed study supporting my view.

Asset Irony

People will rush to buy stocks in a bubble if they think prices will rise. They will hold off buying stocks if they expect prices will go down.

People will buy houses to rent or fix up if they think home prices will rise. They will hold off housing speculation if they expect prices will drop.

The very things where expectations do matter are the very things the Fed ignores.

Hello Fed, Inflation Expectations Are Unglued, No Longer Well Anchored

Inflation Expectations data from New York Fed, chart by Mish

On April 11, I commented Hello Fed, Inflation Expectations Are Unglued, No Longer Well Anchored

The New York Fed survey already shows inflation expectations are not anchored.

Even the three-year median point projection is 4.88%, well over the Fed’s target rate of 2.00%.

Powell was shocked that the University of Michigan survey showed the same thing.

I commented “It’s a good thing that inflation expectations are a blatantly ridiculous concept. Even the Fed’s own research papers make that conclusion.”

It’s a good thing inflation expectations are not self-fulfilling because expectations are now unglued.

Fed Studies Debunk the Phillips Curve

Both studies were done by Fed staffers.

Yet, Fed Chairs Janet Yellen and Jerome Powell did not believe the Fed’s own study.

Stupidity Still Well Anchored

You have to be trained to believe in nonsense and stick with it despite all evidence to the contrary.

Yet, Powell and the St. Louis Fed trust their disproved inflation expectations models. It has led to policy errors already and will lead to more of them.

This is group think in action. There is no diversity of thought at the Fed.

Historical Perspective on CPI Deflations: How Damaging are They?

Regarding policy errors and the accurate warning by the Monetary Affairs Division of the Federal Reserve Board, please consider Historical Perspective on CPI Deflations: How Damaging are They?

A BIS study concluded “Deflation may actually boost output. Lower prices increase real incomes and wealth. And they may also make export goods more competitive.“

Indeed, that must be the case as more goods for less money by default improves standards of living.

The Fed was hell bent on reducing standards of living via inflation. Now they struggle to undo the inflation and asset bubble consequences they created.

The Fed is the problem, not the solution.

* * *