Authored by Mike Shedlock via MishTalk.com,

On average, the economy looks OK. But averages are misleading. Several large groups of people are struggling. They all have one thing in common.

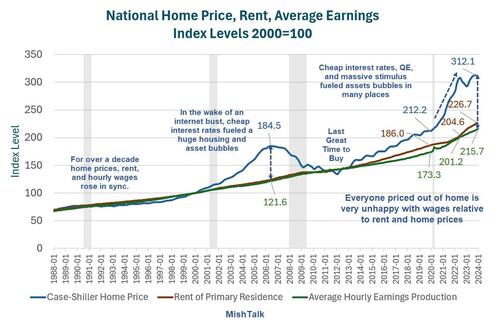

Case-Shiller home price index, CPI rent index, and the index of hourly earnings for production and nonsupervisory workers.

Who’s Unhappy?

Those looking to buy a home but cannot afford the record high prices, are not faring well in this economy.

The last great time to buy a home was in 2012. Over the next eight years, home prices moved further and further away from wages.

When the Covid pandemic hit in 2020, we had record QE, record fiscal stimulus, mortgage rates hit record lows, and inflation hit the highest levels in 40 years.

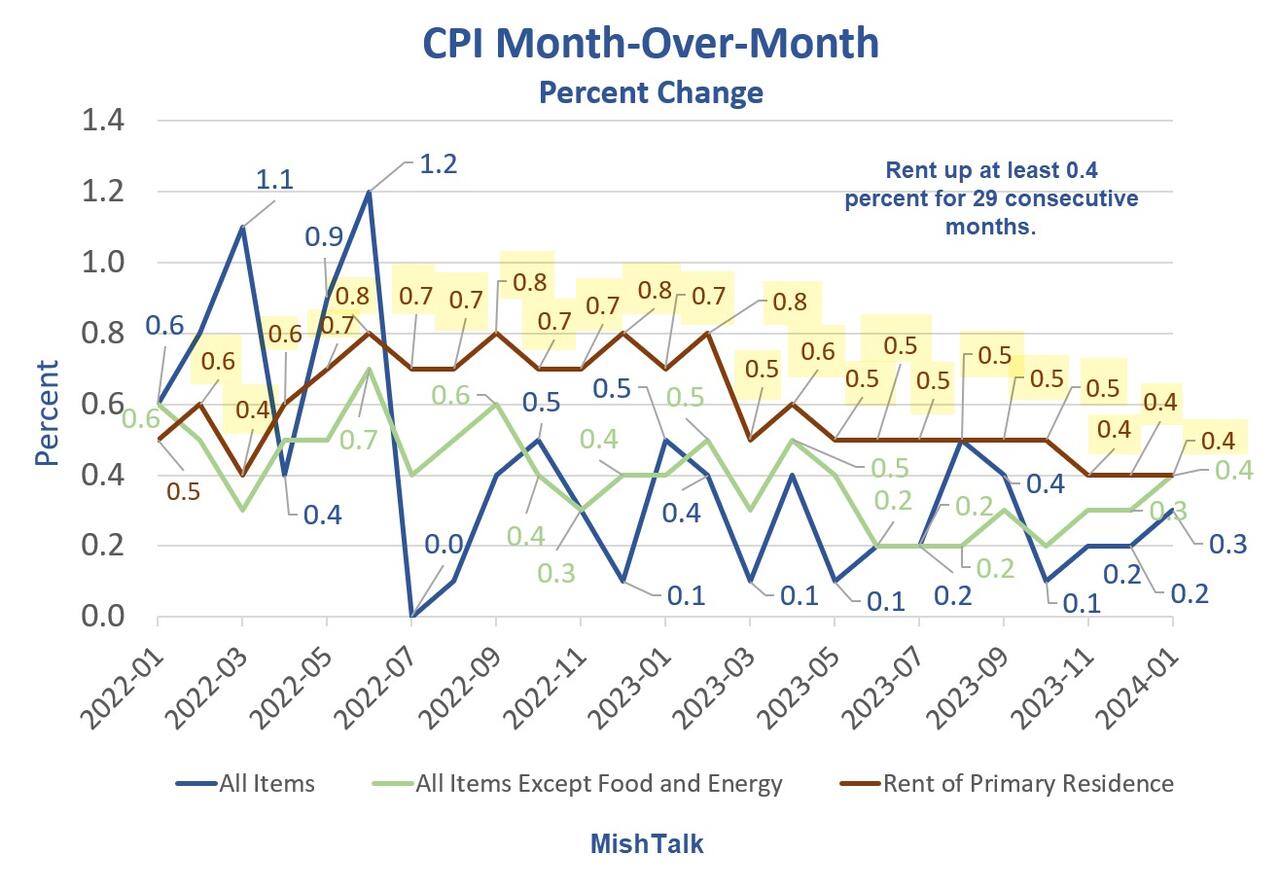

In response, home prices soared out of sight. Worse yet, the price of rent rose at least 0.4 percent for 28 straight months.

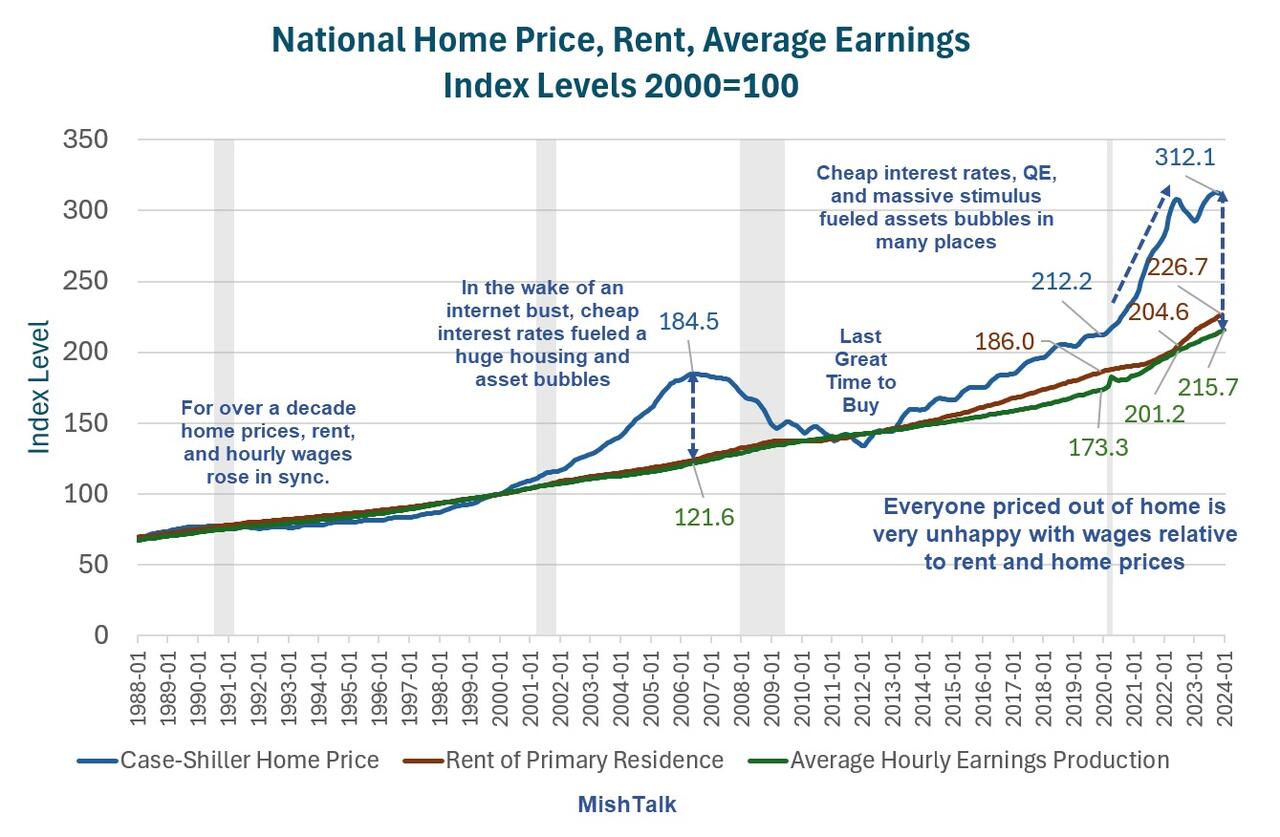

Rent of Primary Residence vs OER

Data from the BLS, chart by Mish

Rent vs OER Chart Notes

-

OER stands for Owners’ Equivalent Rent. It is the price one would pay to rent their own house, unfurnished without rent.

-

Rent of primary residence is just what one would expect. It is measured price of rent, unfurnished, without utilities.

Mass Confusion Over OER

Contrary to widespread myth, OER is a measured price with very minor imputations that do not matter. OER is designed to track rent prices and it does. It is a measured price.

Much of the confusion comes from a misquoted BLS statement on OER, emphasis mine.

The expenditure weight in the CPI market basket for OER is based on the following question that the Consumer Expenditure Survey asks of consumers who own their primary residence: “If someone were to rent your home today, how much do you think it would rent for monthly, unfurnished and without utilities?”

Note that these responses are not used in estimating price change for the shelter categories, only the weight.

People quote that question as if that is how the BLS measures prices. It doesn’t. Prices, except for minor, irrelevant imputations, are based on actual measured rents.

No One Pays OER

The problem with OER is the weight not the measure. No one actually pays OER. Rather, people pay mortgages.

Yet, OER it is the single largest component of the CPI with a weight of 26.769 percent. Rent has a weight of 7.671 percent.

Many people conclude that the CPI is overstated because no one pays OER. The problem with this idea is home prices are at record highs and home prices are not in the CPI at all.

Homes are not in the CPI because economists consider them a capital expense not a personal expense.

But so what? Inflation matters not just consumer inflation. The Fed has made a big mess of things by ignoring obvious housing bubbles.

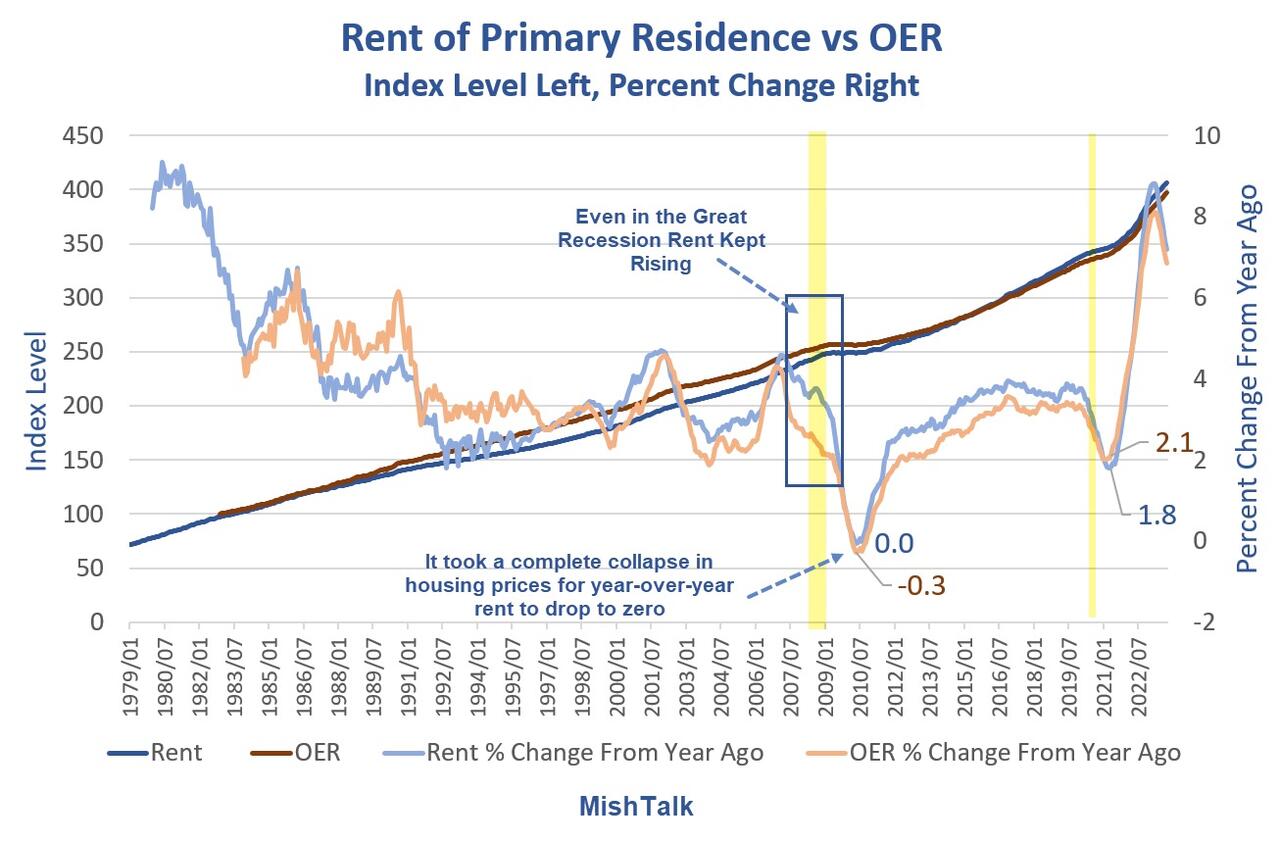

30-year mortgage Rates

Mortgage rates courtesy of Mortgage News Daily, annotations by Mish

When the Fed slashed interest rates to zero, mortgage rates fell below 3.0% for an extended period allowing everyone to refinance at 3.0 percent or below. Most did.

OER rose from 332 to 403 between January of 2020 and January of 2024. That’s a gain of 21.4 percent.

Rent rose from 338 to 412. That’s a gain of 21.9 percent.

Whereas the renter is struggling, the homeowner refinanced lower putting extra money in his pocket every month.

Home owners also benefitted from rising wages, rising value of their home and a stable, not rising mortgage payment.

Winners and Losers

-

The homeowners are generally doing OK. The home ownership rate is 65.7 percent.

-

The 34.3 percent who rent are generally not doing OK.

The study did not break things down by home owners vs renters, but I suspect most of the use is by renters.

According to the latest CPI report, rent was up at least 0.4 percent for the 29th straight month. Shelter, a broader category, rose 0.6 percent. Food rose 0.4 percent.

CPI data from the BLS, chart by Mish

Whereas home owners have a fixed payment, likely refinanced lower than their initial mortgage, renters faces huge increases, not every month, but once a year, big bang.

For discussion please see Another Hotter Than Expected CPI Led by Shelter, Up Another 0.6 Percent

The stress is easy to spot by demographics.

Credit Card and Auto Delinquencies Soar

![]()

Credit card debt surged to a record high in the fourth quarter. Even more troubling is a steep climb in 90 day or longer delinquencies.

Record High Credit Card Debt

Credit card debt rose to a new record high of $1.13 trillion, up $50 billion in the quarter. Even more troubling is the surge in serious delinquencies, defined as 90 days or more past due.

For nearly all age groups, serious delinquencies are the highest since 2011 at best.

Auto Loan Delinquencies

![]()

Serious delinquencies on auto loans have jumped from under 3 percent in mid-2021 to to 5 percent at the end of 2023 for age group 18-29.

Age group 30-39 is also troubling. Serious delinquencies for age groups 18-29 and 30-39 are at the highest levels since 2010.

For further discussion please see Credit Card and Auto Delinquencies Soar, Especially Age Group 18 to 39

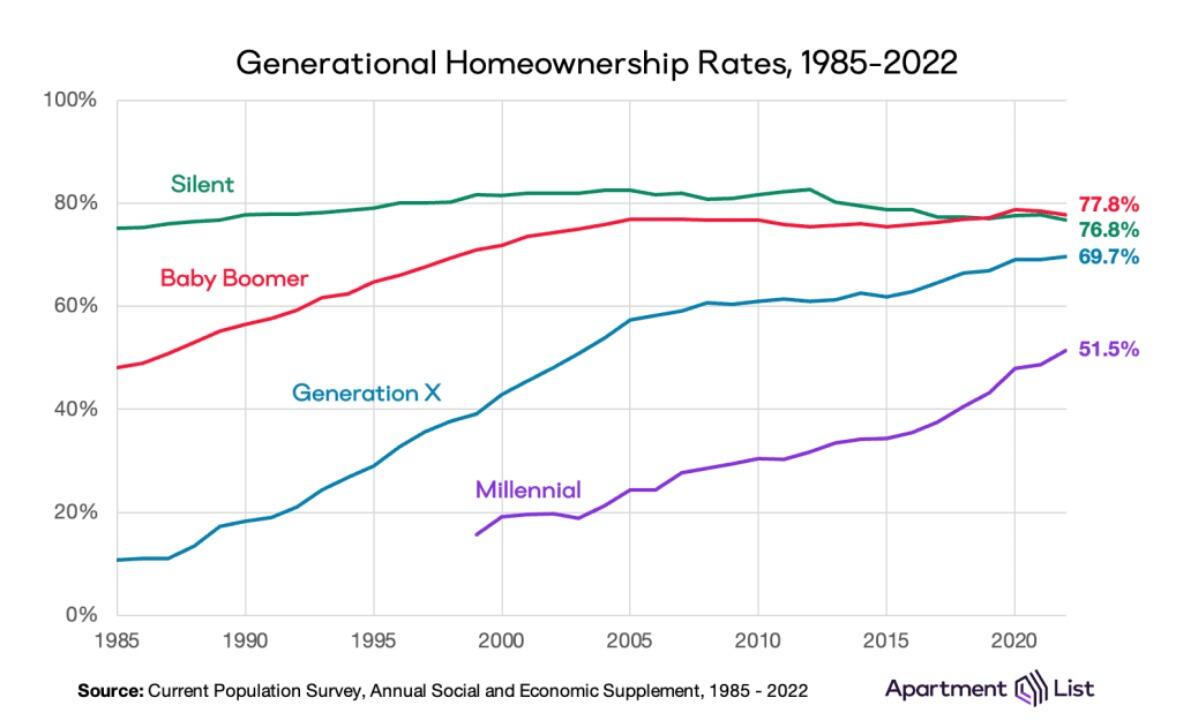

Generational Homeownership Rates

Home ownership rates courtesy of Apartment List

The above chart is from the Apartment List’s 2023 Millennial Homeownership Report

Those struggling with rent are more likely to Millennials and Zoomers than Generation X, Baby Boomers, or members of the Silent Generation.

The same age groups struggling with credit card and auto delinquencies.

On Average Everything is Great

Average it up as Fed and all the clueless economic and political writers do, and things look great.

This is why we have seen countless stories attempting to explain why people should be happy.

Krugman Blames Partisanship

With the recent rise in consumer sentiment, time to revisit this excellent Briefing Book paper. On reflection, I'd do it a bit differently; same basic conclusion, but I think partisan asymmetry explains even more of the remaining low numbers 1/ https://t.co/4lqm7X4472

— Paul Krugman (@paulkrugman) February 17, 2024

OK, there is a fair amount of partisanship in the polls.

However, Biden isn’t struggling from partisanship alone. If that was the reason, Biden would not be polling so miserably with Democrats in general, blacks, and younger voters.

In addition to Biden’s Age and Senility, this allegedly booming economy left behind the renters and everyone under the age of 40 struggling to make ends meet.

Powell Pleads Patience

In Jerome Powell’s Interview with 60 Minutes, the Fed Chairman Tells 60 Minutes US Fiscal Path is Unsustainable

Powell: When high inflation really threatens to become persistent, we use our tools to bring down inflation. It’s very important for that young couple — and particularly for younger couples starting out who may not have great financial means, that we succeed in this effort.

60 Minutes: You’re asking the American people for patience?

Powell: Yes. And I think people have been patient and have been through a pretty difficult time. And I think now we’re coming through that time and starting to feel a little bit better about things.

Powell, Krugman, and most of the economic writers, even at the Wall Street Journal have not managed to figure out over a third of the nation is struggling.

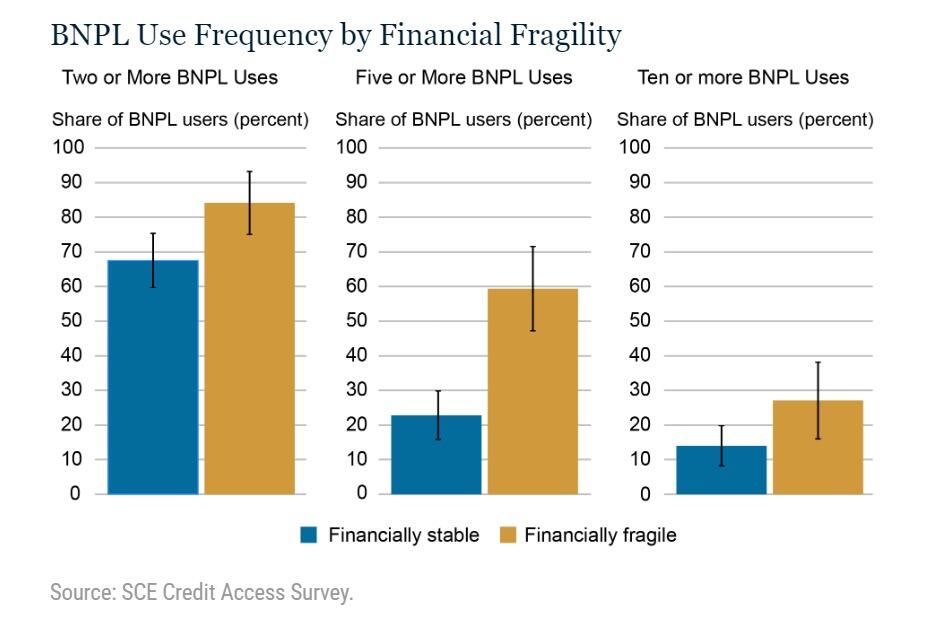

Many Are Addicted to “Buy Now, Pay Later” Plans

Buy Now Pay Later, BNPL, plans are increasingly popular. It’s another sign of consumer credit stress.

For discussion, please see Many Are Addicted to “Buy Now, Pay Later” Plans, It’s a Big Trap

The study did not break things down by home owners vs renters, but I strongly suspect most of the BNPL use is by renters.

What About Jobs?

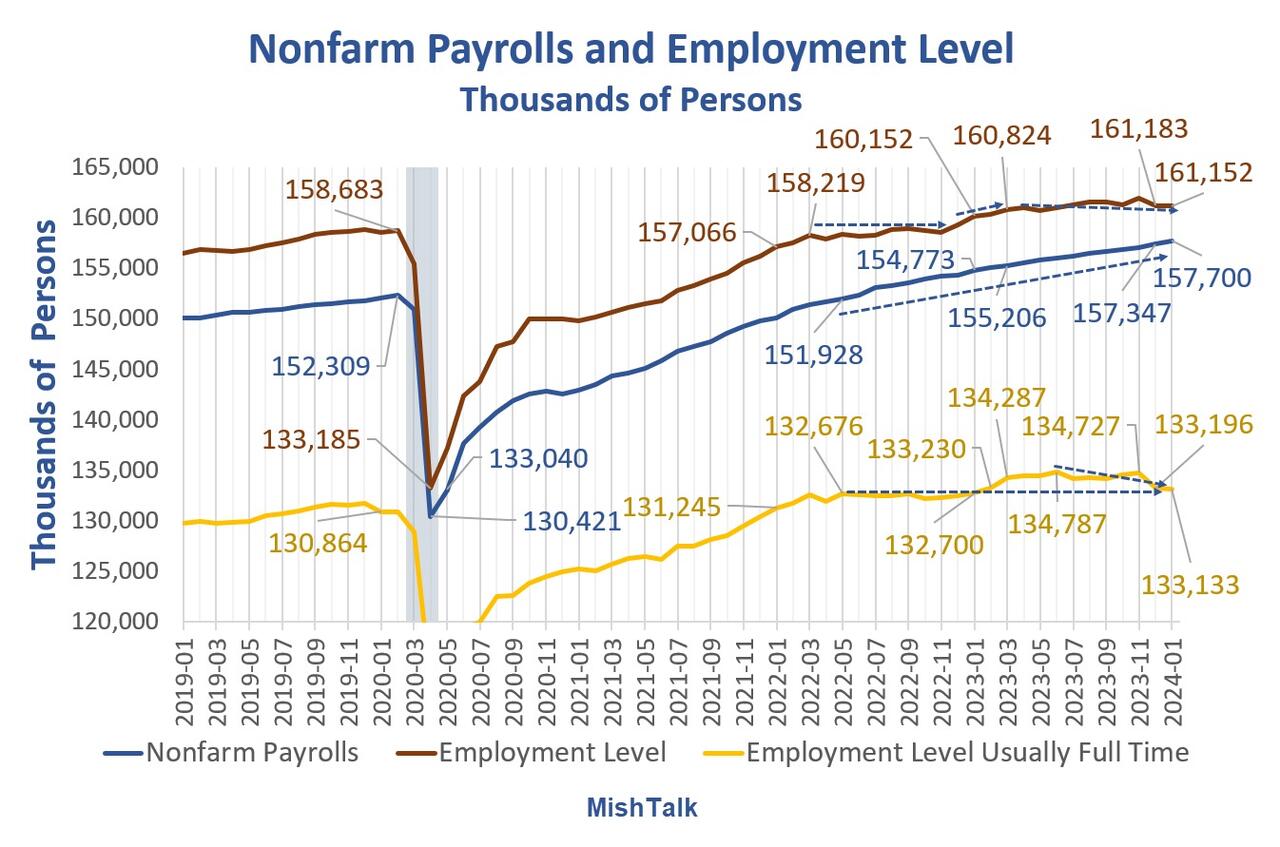

Jobs Soar but Full Time Employment Is Barely Changed Since May 2022

Nonfarm payrolls and employment levels from the BLS, chart by Mish.

-

February 5, 2024: Big Explosion of Government and Social Assistance Jobs in 2023 to Help Migrants

-

February 16, 2024: Over 100% of the Increase in Employment Since 2020 is Foreign Born

-

February 2, 2024: Jobs Soar but Full Time Employment Is Barely Changed Since May 2022

But hey, that’s OK because on average, the economy is great. Or do we really mean, on average the stock market is great, and the average homeowner is fine?

Hello Mr. Powell

There are two economies (the homeowners/asset holders and everyone else). However, there is only one interest rate. Patience please says Powell.

Lowering rates risks risks fueling the housing bubble and the most expensive stock market in history.

Hello Mr. Powell, it’s your move.

Authored by Mike Shedlock via MishTalk.com,

On average, the economy looks OK. But averages are misleading. Several large groups of people are struggling. They all have one thing in common.

Case-Shiller home price index, CPI rent index, and the index of hourly earnings for production and nonsupervisory workers.

Who’s Unhappy?

Those looking to buy a home but cannot afford the record high prices, are not faring well in this economy.

The last great time to buy a home was in 2012. Over the next eight years, home prices moved further and further away from wages.

When the Covid pandemic hit in 2020, we had record QE, record fiscal stimulus, mortgage rates hit record lows, and inflation hit the highest levels in 40 years.

In response, home prices soared out of sight. Worse yet, the price of rent rose at least 0.4 percent for 28 straight months.

Rent of Primary Residence vs OER

Data from the BLS, chart by Mish

Rent vs OER Chart Notes

-

OER stands for Owners’ Equivalent Rent. It is the price one would pay to rent their own house, unfurnished without rent.

-

Rent of primary residence is just what one would expect. It is measured price of rent, unfurnished, without utilities.

Mass Confusion Over OER

Contrary to widespread myth, OER is a measured price with very minor imputations that do not matter. OER is designed to track rent prices and it does. It is a measured price.

Much of the confusion comes from a misquoted BLS statement on OER, emphasis mine.

The expenditure weight in the CPI market basket for OER is based on the following question that the Consumer Expenditure Survey asks of consumers who own their primary residence: “If someone were to rent your home today, how much do you think it would rent for monthly, unfurnished and without utilities?”

Note that these responses are not used in estimating price change for the shelter categories, only the weight.

People quote that question as if that is how the BLS measures prices. It doesn’t. Prices, except for minor, irrelevant imputations, are based on actual measured rents.

No One Pays OER

The problem with OER is the weight not the measure. No one actually pays OER. Rather, people pay mortgages.

Yet, OER it is the single largest component of the CPI with a weight of 26.769 percent. Rent has a weight of 7.671 percent.

Many people conclude that the CPI is overstated because no one pays OER. The problem with this idea is home prices are at record highs and home prices are not in the CPI at all.

Homes are not in the CPI because economists consider them a capital expense not a personal expense.

But so what? Inflation matters not just consumer inflation. The Fed has made a big mess of things by ignoring obvious housing bubbles.

30-year mortgage Rates

Mortgage rates courtesy of Mortgage News Daily, annotations by Mish

When the Fed slashed interest rates to zero, mortgage rates fell below 3.0% for an extended period allowing everyone to refinance at 3.0 percent or below. Most did.

OER rose from 332 to 403 between January of 2020 and January of 2024. That’s a gain of 21.4 percent.

Rent rose from 338 to 412. That’s a gain of 21.9 percent.

Whereas the renter is struggling, the homeowner refinanced lower putting extra money in his pocket every month.

Home owners also benefitted from rising wages, rising value of their home and a stable, not rising mortgage payment.

Winners and Losers

The study did not break things down by home owners vs renters, but I suspect most of the use is by renters.

According to the latest CPI report, rent was up at least 0.4 percent for the 29th straight month. Shelter, a broader category, rose 0.6 percent. Food rose 0.4 percent.

CPI data from the BLS, chart by Mish

Whereas home owners have a fixed payment, likely refinanced lower than their initial mortgage, renters faces huge increases, not every month, but once a year, big bang.

For discussion please see Another Hotter Than Expected CPI Led by Shelter, Up Another 0.6 Percent

The stress is easy to spot by demographics.

Credit Card and Auto Delinquencies Soar

![]()

Credit card debt surged to a record high in the fourth quarter. Even more troubling is a steep climb in 90 day or longer delinquencies.

Record High Credit Card Debt

Credit card debt rose to a new record high of $1.13 trillion, up $50 billion in the quarter. Even more troubling is the surge in serious delinquencies, defined as 90 days or more past due.

For nearly all age groups, serious delinquencies are the highest since 2011 at best.

Auto Loan Delinquencies

![]()

Serious delinquencies on auto loans have jumped from under 3 percent in mid-2021 to to 5 percent at the end of 2023 for age group 18-29.

Age group 30-39 is also troubling. Serious delinquencies for age groups 18-29 and 30-39 are at the highest levels since 2010.

For further discussion please see Credit Card and Auto Delinquencies Soar, Especially Age Group 18 to 39

Generational Homeownership Rates

Home ownership rates courtesy of Apartment List

The above chart is from the Apartment List’s 2023 Millennial Homeownership Report

Those struggling with rent are more likely to Millennials and Zoomers than Generation X, Baby Boomers, or members of the Silent Generation.

The same age groups struggling with credit card and auto delinquencies.

On Average Everything is Great

Average it up as Fed and all the clueless economic and political writers do, and things look great.

This is why we have seen countless stories attempting to explain why people should be happy.

Krugman Blames Partisanship

With the recent rise in consumer sentiment, time to revisit this excellent Briefing Book paper. On reflection, I’d do it a bit differently; same basic conclusion, but I think partisan asymmetry explains even more of the remaining low numbers 1/ https://t.co/4lqm7X4472

— Paul Krugman (@paulkrugman) February 17, 2024

OK, there is a fair amount of partisanship in the polls.

However, Biden isn’t struggling from partisanship alone. If that was the reason, Biden would not be polling so miserably with Democrats in general, blacks, and younger voters.

In addition to Biden’s Age and Senility, this allegedly booming economy left behind the renters and everyone under the age of 40 struggling to make ends meet.

Powell Pleads Patience

In Jerome Powell’s Interview with 60 Minutes, the Fed Chairman Tells 60 Minutes US Fiscal Path is Unsustainable

Powell: When high inflation really threatens to become persistent, we use our tools to bring down inflation. It’s very important for that young couple — and particularly for younger couples starting out who may not have great financial means, that we succeed in this effort.

60 Minutes: You’re asking the American people for patience?

Powell: Yes. And I think people have been patient and have been through a pretty difficult time. And I think now we’re coming through that time and starting to feel a little bit better about things.

Powell, Krugman, and most of the economic writers, even at the Wall Street Journal have not managed to figure out over a third of the nation is struggling.

Many Are Addicted to “Buy Now, Pay Later” Plans

Buy Now Pay Later, BNPL, plans are increasingly popular. It’s another sign of consumer credit stress.

For discussion, please see Many Are Addicted to “Buy Now, Pay Later” Plans, It’s a Big Trap

The study did not break things down by home owners vs renters, but I strongly suspect most of the BNPL use is by renters.

What About Jobs?

Jobs Soar but Full Time Employment Is Barely Changed Since May 2022

Nonfarm payrolls and employment levels from the BLS, chart by Mish.

But hey, that’s OK because on average, the economy is great. Or do we really mean, on average the stock market is great, and the average homeowner is fine?

Hello Mr. Powell

There are two economies (the homeowners/asset holders and everyone else). However, there is only one interest rate. Patience please says Powell.

Lowering rates risks risks fueling the housing bubble and the most expensive stock market in history.

Hello Mr. Powell, it’s your move.

Loading…