Authored by Brandon Smith via Alt-Market.us,

Several years ago I predicted that the U.S. would ultimately be confronted with the debilitating economic conundrum of stagflation, something which the nation had not seen since the 1970s. I suggested that stagflation would become a household word again and that the majority of American concerns would revolve around rising prices coupled with stagnant wages and falling production.

In 2018 in my article Stagflationary Crisis: U.S.A.’s Ongoing Collapse, Understanding the Cause, I noted:

Years ago there was a rather idiotic battle between financial analysts over what the end result of the Fed’s massive stimulus measures would be. One side argued that deflation would be the outcome and that no amount of Fed printing would overtake the vast black hole of debt conjured by the derivatives implosion. The other side argued that the Fed would continue to print perpetually, resorting to QE4 or possibly “QE infinity” and negative interest rates as a means to stave off a market crash for decades (like Japan) while at the same time initiating a Weimar-style inflationary bonanza.

Both sides were wrong because they refused to acknowledge the third option – stagflation.

Sleepwalking into stagflation

The process of stagflation is difficult to track because there are multiple paths that it can take, many of them largely dependent on the whims of the central bank and its policy decisions. All we can really do is look back at the limited number of historic examples simply and guess what will happen next. In the 1970s stagflation nearly crushed the country, with inflation rising by 7% to over 14% per year for a decade.

When I hear Zennials complain about being born into the “worst economy ever,” I have to laugh because they really have no clue. The 1970s was far worse in terms of erosion of buying power as well as overall poverty. If you look at film footage and photos of urban areas from Los Angeles to New York to Philadelphia during that time, many parts of these cities looked like bombed-out war zones.

The country was truly on the edge of disaster.

In the early 1980s, under Paul Volcker’s leadership the Federal Reserve jacked interest rates up to over 20%. This stopped the inflation crisis but triggered a deflationary plunge that would sit like a giant boulder on the chest of the American consumer and small business owners for years to come. My own grandfather lost millions in his trucking and freight company during the rate spike; many people lost their businesses and homes.

In other words, as bad as the situation is now, we haven’t seen anything yet. Of course, we are quickly moving towards similar conditions and there is one thing we have today that the 1970s didn’t: A massive (and growing) national debt.

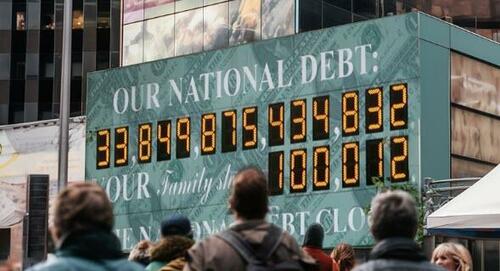

Currently, the U.S. national debt is $33.8 trillion and has a 120% debt-to-GDP ratio. In a single month, October 2023, the federal government added over $600 billion to the debt. At the current pace the total debt will breach $41 trillion in one year.

The speed of this accumulation is frightening. To put this in perspective, the Obama administration and the Federal Reserve added around $9 trillion to the debt in eight years with the corporate bailout spree of the Great Financial Crisis. Compared to the Biden administration, Obama’s spending looks absolutely miserly.

How is this possible?

The swirling debt spiral

As I have noted in the past, the U.S. economy rests on a foundation of intrinsically worthless currency – and so much debt that the slightest rise in interest rates causes huge ripple effects.

The 20% interest rate level of the early 1980s? Yes, it was worrisome, and led to not one but two grueling recessions. After 200 years of existence, the U.S. ended the decade of the 80s with just under $3 trillion in debt.

Today? Well, for comparison purposes, the Biden administration’s 2021 budget added $2.77 trillion to the national debt. In ONE YEAR! For comparison purposes, from 1776-1989, the federal government accumulated about $2.77 trillion in debt.

It’s impossible to overstate this point: The Biden regime saddled the nation with over 200 years’ worth of debt in just one year.

With a debt over $33 trillion, barely-above-historical-average 5.25% interest rates are catastrophic. Because of “compounding interest,” what Einstein called “the most powerful force in the Universe.” He called it one of the greatest “miracles” known to mankind – if you’re a creditor. If you’re a debtor, though? That miracle becomes a disaster…

Today, the U.S. government regularly borrows money just to make interest payments. The Treasury department also writes new IOUs to fund old IOUs that come due. Finally, the government borrows still more to fund all spending which exceeds tax collection (this is “deficit spending,” which increases the national debt – sometimes the two are conflated).

At higher interest-rate levels, borrowing enters a destructive spiral. There’s interest payments on debt, which was itself borrowed to make interest payments on debt. To put it in simple terms, it’s a bit like a broke person taking on a stack of new credit cards to make the interest payments on a stack of old credit cards. It’s financial suicide.

Eventually the avalanche of debt will stall inflation but it will also wreak havoc across the economy and trigger a deflationary crisis.

We’re seeing the beginning already… The crash across manufacturing and industrial sectors. Frozen wages. Layoffs and bankruptcies piling up in the freight sector.

These are all clear indicators of impending recession. Meanwhile, U.S. home sales have plunged to a 13 year low as prices continue to rise.

These are all red flags of an impending deflation event that is certain to cause massive unemployment, likely within the next year. It would seem the magic of the Covid-era money-printing spree is finally fading away – and we’re seeing the real economy underneath.

The expectation among investors is that the Fed is poised to cut rates or return swiftly to QE. This is not going to happen, at least not anytime soon. The Fed, I believe, wants a crash. After addicting markets to easy money for over a decade, the central bankers know exactly what will happen as they continue to cut off the drug supply.

I suspect we are about to see a major change in the behavior of the economy going into 2024. The stagflation phase is nearly over. The discussion around dinner tables across America will turn to the exploding national debt, and debt in general. The big debate will once again turn to this: Will the Fed keep rates steady, risking deflationary implosion and debt default, or, will they cut rates, return to stimulus to pay the debt, and risk double digit inflation? These are the two choices in front of the U.S. government – and either way, we lose.

That’s why it’s more urgent than ever to own financial assets that aren’t based on debt, that aren’t IOUs but actual, tangible things you can see and touch. There are only a few left in this globally-financialized world – and of them, only physical precious metals are also private, safe haven stores of value. If you don’t own real physical gold and silver soon, your financial future will be tied to the U.S. government’s financial future.

The U.S. economy will fail. Those who don’t ensure their financial independence will sink with the ship. You can take steps now to protect yourself and your family, but the opportunity won’t last forever. Once it’s obvious that the ship is sinking, it’s too late – the lifeboats will already be full.

Don’t go down with the ship.

* * *

As the world moves away from dollars and toward Central Bank Digital Currencies (CBDCs), is your 401(k) or IRA really safe? A smart and conservative move is to diversify into a physical gold IRA. That way your savings will be in something solid and enduring. Get your FREE info kit on Gold IRAs from Birch Gold Group. No strings attached, just peace of mind. Click here to secure your future today.

Authored by Brandon Smith via Alt-Market.us,

Several years ago I predicted that the U.S. would ultimately be confronted with the debilitating economic conundrum of stagflation, something which the nation had not seen since the 1970s. I suggested that stagflation would become a household word again and that the majority of American concerns would revolve around rising prices coupled with stagnant wages and falling production.

In 2018 in my article Stagflationary Crisis: U.S.A.’s Ongoing Collapse, Understanding the Cause, I noted:

Years ago there was a rather idiotic battle between financial analysts over what the end result of the Fed’s massive stimulus measures would be. One side argued that deflation would be the outcome and that no amount of Fed printing would overtake the vast black hole of debt conjured by the derivatives implosion. The other side argued that the Fed would continue to print perpetually, resorting to QE4 or possibly “QE infinity” and negative interest rates as a means to stave off a market crash for decades (like Japan) while at the same time initiating a Weimar-style inflationary bonanza.

Both sides were wrong because they refused to acknowledge the third option – stagflation.

Sleepwalking into stagflation

The process of stagflation is difficult to track because there are multiple paths that it can take, many of them largely dependent on the whims of the central bank and its policy decisions. All we can really do is look back at the limited number of historic examples simply and guess what will happen next. In the 1970s stagflation nearly crushed the country, with inflation rising by 7% to over 14% per year for a decade.

When I hear Zennials complain about being born into the “worst economy ever,” I have to laugh because they really have no clue. The 1970s was far worse in terms of erosion of buying power as well as overall poverty. If you look at film footage and photos of urban areas from Los Angeles to New York to Philadelphia during that time, many parts of these cities looked like bombed-out war zones.

The country was truly on the edge of disaster.

In the early 1980s, under Paul Volcker’s leadership the Federal Reserve jacked interest rates up to over 20%. This stopped the inflation crisis but triggered a deflationary plunge that would sit like a giant boulder on the chest of the American consumer and small business owners for years to come. My own grandfather lost millions in his trucking and freight company during the rate spike; many people lost their businesses and homes.

In other words, as bad as the situation is now, we haven’t seen anything yet. Of course, we are quickly moving towards similar conditions and there is one thing we have today that the 1970s didn’t: A massive (and growing) national debt.

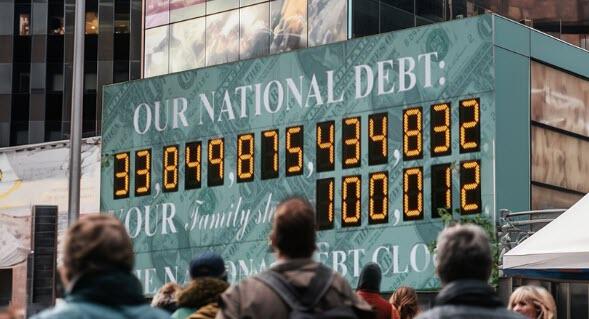

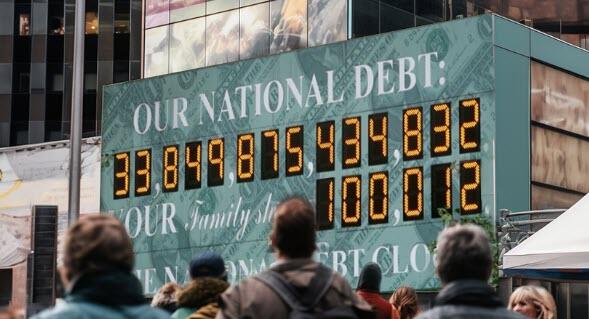

Currently, the U.S. national debt is $33.8 trillion and has a 120% debt-to-GDP ratio. In a single month, October 2023, the federal government added over $600 billion to the debt. At the current pace the total debt will breach $41 trillion in one year.

The speed of this accumulation is frightening. To put this in perspective, the Obama administration and the Federal Reserve added around $9 trillion to the debt in eight years with the corporate bailout spree of the Great Financial Crisis. Compared to the Biden administration, Obama’s spending looks absolutely miserly.

How is this possible?

The swirling debt spiral

As I have noted in the past, the U.S. economy rests on a foundation of intrinsically worthless currency – and so much debt that the slightest rise in interest rates causes huge ripple effects.

The 20% interest rate level of the early 1980s? Yes, it was worrisome, and led to not one but two grueling recessions. After 200 years of existence, the U.S. ended the decade of the 80s with just under $3 trillion in debt.

Today? Well, for comparison purposes, the Biden administration’s 2021 budget added $2.77 trillion to the national debt. In ONE YEAR! For comparison purposes, from 1776-1989, the federal government accumulated about $2.77 trillion in debt.

It’s impossible to overstate this point: The Biden regime saddled the nation with over 200 years’ worth of debt in just one year.

With a debt over $33 trillion, barely-above-historical-average 5.25% interest rates are catastrophic. Because of “compounding interest,” what Einstein called “the most powerful force in the Universe.” He called it one of the greatest “miracles” known to mankind – if you’re a creditor. If you’re a debtor, though? That miracle becomes a disaster…

Today, the U.S. government regularly borrows money just to make interest payments. The Treasury department also writes new IOUs to fund old IOUs that come due. Finally, the government borrows still more to fund all spending which exceeds tax collection (this is “deficit spending,” which increases the national debt – sometimes the two are conflated).

At higher interest-rate levels, borrowing enters a destructive spiral. There’s interest payments on debt, which was itself borrowed to make interest payments on debt. To put it in simple terms, it’s a bit like a broke person taking on a stack of new credit cards to make the interest payments on a stack of old credit cards. It’s financial suicide.

Eventually the avalanche of debt will stall inflation but it will also wreak havoc across the economy and trigger a deflationary crisis.

We’re seeing the beginning already… The crash across manufacturing and industrial sectors. Frozen wages. Layoffs and bankruptcies piling up in the freight sector.

These are all clear indicators of impending recession. Meanwhile, U.S. home sales have plunged to a 13 year low as prices continue to rise.

These are all red flags of an impending deflation event that is certain to cause massive unemployment, likely within the next year. It would seem the magic of the Covid-era money-printing spree is finally fading away – and we’re seeing the real economy underneath.

The expectation among investors is that the Fed is poised to cut rates or return swiftly to QE. This is not going to happen, at least not anytime soon. The Fed, I believe, wants a crash. After addicting markets to easy money for over a decade, the central bankers know exactly what will happen as they continue to cut off the drug supply.

I suspect we are about to see a major change in the behavior of the economy going into 2024. The stagflation phase is nearly over. The discussion around dinner tables across America will turn to the exploding national debt, and debt in general. The big debate will once again turn to this: Will the Fed keep rates steady, risking deflationary implosion and debt default, or, will they cut rates, return to stimulus to pay the debt, and risk double digit inflation? These are the two choices in front of the U.S. government – and either way, we lose.

That’s why it’s more urgent than ever to own financial assets that aren’t based on debt, that aren’t IOUs but actual, tangible things you can see and touch. There are only a few left in this globally-financialized world – and of them, only physical precious metals are also private, safe haven stores of value. If you don’t own real physical gold and silver soon, your financial future will be tied to the U.S. government’s financial future.

The U.S. economy will fail. Those who don’t ensure their financial independence will sink with the ship. You can take steps now to protect yourself and your family, but the opportunity won’t last forever. Once it’s obvious that the ship is sinking, it’s too late – the lifeboats will already be full.

Don’t go down with the ship.

* * *

As the world moves away from dollars and toward Central Bank Digital Currencies (CBDCs), is your 401(k) or IRA really safe? A smart and conservative move is to diversify into a physical gold IRA. That way your savings will be in something solid and enduring. Get your FREE info kit on Gold IRAs from Birch Gold Group. No strings attached, just peace of mind. Click here to secure your future today.

Loading…