By Michael Every of Rabobank

The Most Beautiful Word in the Dictionary

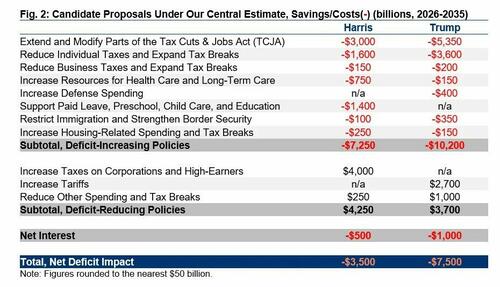

Donald Trump sat down for an hour long interview with Bloomberg Editor in Chief John Micklethwait yesterday. The conversation was mostly centerd on the economy, and Trump played the hits early by describing ‘tariff’ as “the most beautiful word in the dictionary”. Trump’s comment came in response to a question about the impact of his policies on the federal debt in light of analysis from the non-partisan Congressional Budget Office, which claimed that a second Trump Presidency would grow the debt by $7.5 trillion whereas Kamala Harris’ program would add $3.5 trillion.

Under Trump Mk II “we’re going to build a wall and Mexico is going to pay for it” has become “we’re going to build a tariff wall, and everyone else is going to pay for it”. Trump reprised the Laffer Curve by suggesting that he was the only candidate with a plan for growth and that stronger growth, alongside tariffs, would be sufficient to pay for sweeping tax cuts as companies seek to relocate production inside the United States.

Q. Your proposed policies would wreck the economy, and lead to higher inhalation and $7.5 trillion in debt. Even the conservative WSJ says it.

— Republicans against Trump (@RpsAgainstTrump) October 15, 2024

Trump: “What does the Wall Street Journal know? They've been wrong about everything. So have you.” pic.twitter.com/UPHb2LObaS

To illustrate his point on the beauty of tariffs, Trump recounted a conversation he had with an auto executive where he claimed that large-scale automotive factory projects in Mexico had been abandoned once it became clear that Trump was running and was competitive in the race for the White House. “If I run this country, I’m going to put a one-hundred, two-hundred, one-thousand per cent tariff. They’re not going to sell one car into the United States.” The Mexican Peso promptly slumped after his comments.

Europe also came in for criticism with Trump complaining that Europeans treat America “very badly”. He pointed to how few Chevrolets and Fords are sold in Germany, while “millions” of Volkswagens, BMWs and Mercedes Benzs are a feature on American roads. Trump contended that high tariffs would force European automakers to relocate production to the USA, which seems timely given the Empire Manufacturing Survey unexpectedly fell to a reading of -11.9 yesterday from +11.5 in September.

No doubt the specter of (further) forced deindustrialisation from mercantilist trade policies will send a shiver down the spine of European industrialists. Especially in light of news yesterday that Dutch tech giant ASML’s stock experienced the sharpest 1-day drop in 26 years after missing third quarter sales estimates by almost 50%. The sharp fall for ASML bled over into prices for US chipmakers, helping the S&P500 to finish 0.75% lower on the day while the NASDAQ dropped 1%.

While former President Trump was talking tariffs with Bloomberg, Vice President Harris gave an extended radio interview with Charlamagne Tha God. Polling data suggests the Harris campaign has been losing ground in recent days, particularly with male voters, and Nate Silver’s election outcome prediction model now sees the race as a 50-50 dead heat. Betting markets began pricing in Trump momentum somewhat earlier, and now indicate that Trump is most likely to be the next President.

Harris’s interview with Charlamagne Tha God was likely intended to target the important African American male demographic and covered off on issues like Harris’ support for the legalization of recreational marijuana, whether or not Donald Trump is a fascist (Harris says he is) and, sensationally, the concept of reparation payments for African Americans to which Harris says “it has to be studied. There’s no question.” Presumably the cost of reparations payments are not factored into the CBO’s $3.5trn estimate of the impact of Harris’ policies on the national debt.

Kamala says she’s open to taxpayer funded reparations for slavery. Every interview she does is a disaster. pic.twitter.com/kq51kHSlK2

— Clay Travis (@ClayTravis) October 15, 2024

As we approach the November 5th election date the Treasuries curve has trimmed the steepening that had been a feature in September as long yields jumped following the Fed’s 50bps rate cut. Recent flattening has been mainly due to the rising short end yields as exuberance over potential rate cuts collided with higher than expected payrolls and CPI figures over the last two weeks. Yields finished lower across the board yesterday with the short end continuing to outperform.

San Francisco Fed President Mary Daly picked up on recent strong data by intimating that the Fed could skip a cut at one of the two remaining policy meetings this year. That stands in contrast to clear forward guidance from Jerome Powell at the NABE Conference in late September, where he suggested that the Fed was likely to cut by 25bps at each meeting. Trump remains unimpressed with the Fed Chair’s command of monetary policy, telling Bloomberg that “it’s the greatest job in government. You show up to the office once a month and you say ‘let’s say flip a coin’ and everybody talks about you like you’re a God.”

While bets on the pace of cuts in the US are pared back, the inflation pulse seems to be fading fast almost everywhere else. The final read of September CPI in France saw the year-on-year EU harmonized figure revised down 1-tick to 1.4%, Canadian September CPI undershot expectations by two-ticks to sit at 1.6% y-o-y (lifting the odds of a 50bp cut from the BOC next week) and New Zealand’s Q3 CPI also printed a little softer than expected to take the annual headline rate to just 2.2%.

When asked whether the soft CPI figures could prompt the RBNZ to cut by 75bps in November, Assistant Governor Karen Silk studiously avoided answering the question.

‘Tariff’ might be the most beautiful word in the dictionary, but in financial markets the most beautiful words are still ‘rate cuts!’

By Michael Every of Rabobank

The Most Beautiful Word in the Dictionary

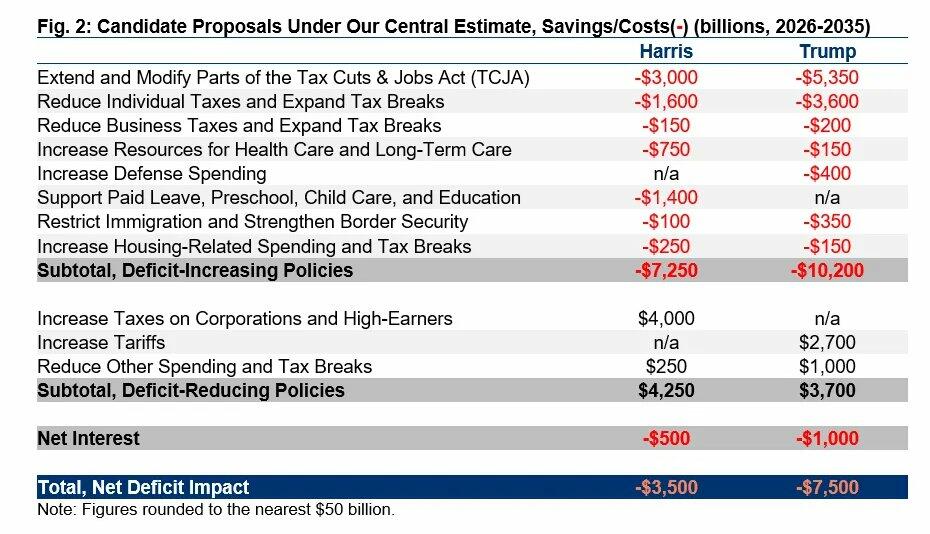

Donald Trump sat down for an hour long interview with Bloomberg Editor in Chief John Micklethwait yesterday. The conversation was mostly centerd on the economy, and Trump played the hits early by describing ‘tariff’ as “the most beautiful word in the dictionary”. Trump’s comment came in response to a question about the impact of his policies on the federal debt in light of analysis from the non-partisan Congressional Budget Office, which claimed that a second Trump Presidency would grow the debt by $7.5 trillion whereas Kamala Harris’ program would add $3.5 trillion.

Under Trump Mk II “we’re going to build a wall and Mexico is going to pay for it” has become “we’re going to build a tariff wall, and everyone else is going to pay for it”. Trump reprised the Laffer Curve by suggesting that he was the only candidate with a plan for growth and that stronger growth, alongside tariffs, would be sufficient to pay for sweeping tax cuts as companies seek to relocate production inside the United States.

Q. Your proposed policies would wreck the economy, and lead to higher inhalation and $7.5 trillion in debt. Even the conservative WSJ says it.

Trump: “What does the Wall Street Journal know? They’ve been wrong about everything. So have you.” pic.twitter.com/UPHb2LObaS

— Republicans against Trump (@RpsAgainstTrump) October 15, 2024

To illustrate his point on the beauty of tariffs, Trump recounted a conversation he had with an auto executive where he claimed that large-scale automotive factory projects in Mexico had been abandoned once it became clear that Trump was running and was competitive in the race for the White House. “If I run this country, I’m going to put a one-hundred, two-hundred, one-thousand per cent tariff. They’re not going to sell one car into the United States.” The Mexican Peso promptly slumped after his comments.

Europe also came in for criticism with Trump complaining that Europeans treat America “very badly”. He pointed to how few Chevrolets and Fords are sold in Germany, while “millions” of Volkswagens, BMWs and Mercedes Benzs are a feature on American roads. Trump contended that high tariffs would force European automakers to relocate production to the USA, which seems timely given the Empire Manufacturing Survey unexpectedly fell to a reading of -11.9 yesterday from +11.5 in September.

No doubt the specter of (further) forced deindustrialisation from mercantilist trade policies will send a shiver down the spine of European industrialists. Especially in light of news yesterday that Dutch tech giant ASML’s stock experienced the sharpest 1-day drop in 26 years after missing third quarter sales estimates by almost 50%. The sharp fall for ASML bled over into prices for US chipmakers, helping the S&P500 to finish 0.75% lower on the day while the NASDAQ dropped 1%.

While former President Trump was talking tariffs with Bloomberg, Vice President Harris gave an extended radio interview with Charlamagne Tha God. Polling data suggests the Harris campaign has been losing ground in recent days, particularly with male voters, and Nate Silver’s election outcome prediction model now sees the race as a 50-50 dead heat. Betting markets began pricing in Trump momentum somewhat earlier, and now indicate that Trump is most likely to be the next President.

Harris’s interview with Charlamagne Tha God was likely intended to target the important African American male demographic and covered off on issues like Harris’ support for the legalization of recreational marijuana, whether or not Donald Trump is a fascist (Harris says he is) and, sensationally, the concept of reparation payments for African Americans to which Harris says “it has to be studied. There’s no question.” Presumably the cost of reparations payments are not factored into the CBO’s $3.5trn estimate of the impact of Harris’ policies on the national debt.

Kamala says she’s open to taxpayer funded reparations for slavery. Every interview she does is a disaster. pic.twitter.com/kq51kHSlK2

— Clay Travis (@ClayTravis) October 15, 2024

As we approach the November 5th election date the Treasuries curve has trimmed the steepening that had been a feature in September as long yields jumped following the Fed’s 50bps rate cut. Recent flattening has been mainly due to the rising short end yields as exuberance over potential rate cuts collided with higher than expected payrolls and CPI figures over the last two weeks. Yields finished lower across the board yesterday with the short end continuing to outperform.

San Francisco Fed President Mary Daly picked up on recent strong data by intimating that the Fed could skip a cut at one of the two remaining policy meetings this year. That stands in contrast to clear forward guidance from Jerome Powell at the NABE Conference in late September, where he suggested that the Fed was likely to cut by 25bps at each meeting. Trump remains unimpressed with the Fed Chair’s command of monetary policy, telling Bloomberg that “it’s the greatest job in government. You show up to the office once a month and you say ‘let’s say flip a coin’ and everybody talks about you like you’re a God.”

While bets on the pace of cuts in the US are pared back, the inflation pulse seems to be fading fast almost everywhere else. The final read of September CPI in France saw the year-on-year EU harmonized figure revised down 1-tick to 1.4%, Canadian September CPI undershot expectations by two-ticks to sit at 1.6% y-o-y (lifting the odds of a 50bp cut from the BOC next week) and New Zealand’s Q3 CPI also printed a little softer than expected to take the annual headline rate to just 2.2%.

When asked whether the soft CPI figures could prompt the RBNZ to cut by 75bps in November, Assistant Governor Karen Silk studiously avoided answering the question.

‘Tariff’ might be the most beautiful word in the dictionary, but in financial markets the most beautiful words are still ‘rate cuts!’

Loading…