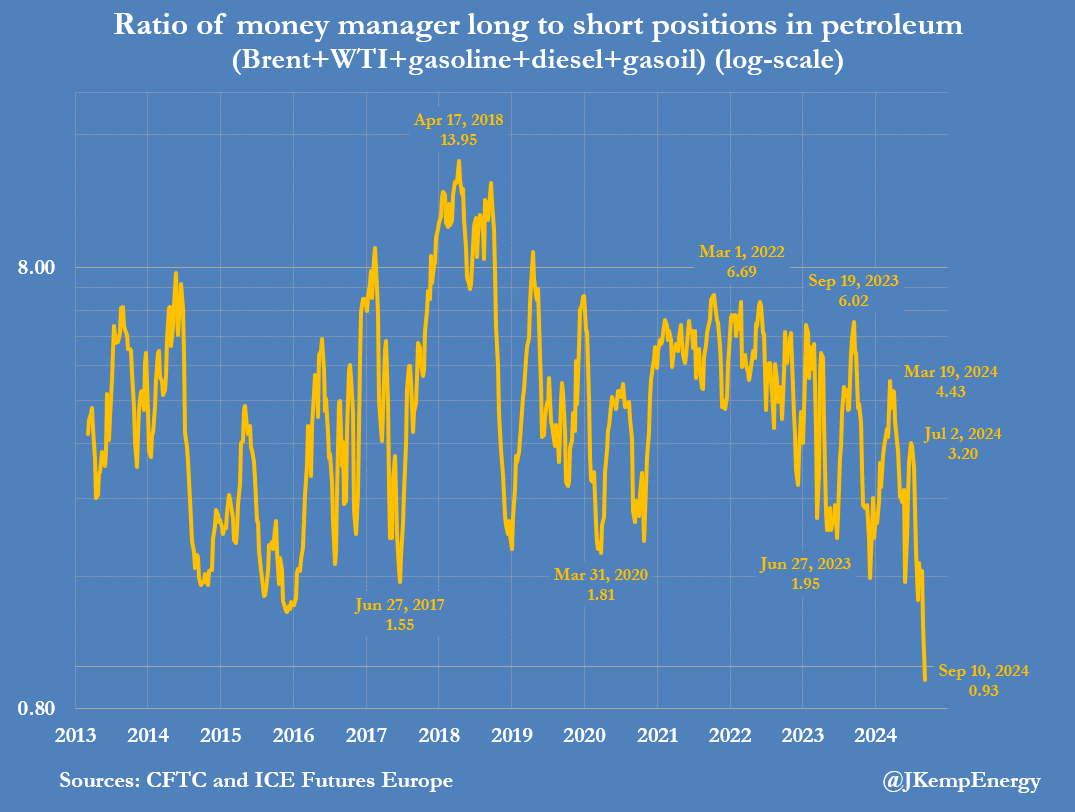

Hedge funds and other asset managers have never been more pessimistic about the outlook for petroleum prices, as signs multiply that the major industrial economies are losing momentum according to energy analyst John Kemp. Investors have also concluded Saudi Arabia and its OPEC+ allies have run out of options and either cannot or will not restrict their own production further to offset the slowdown in consumption growth and slide in prices.

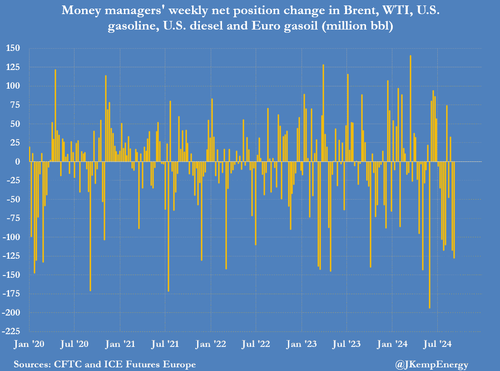

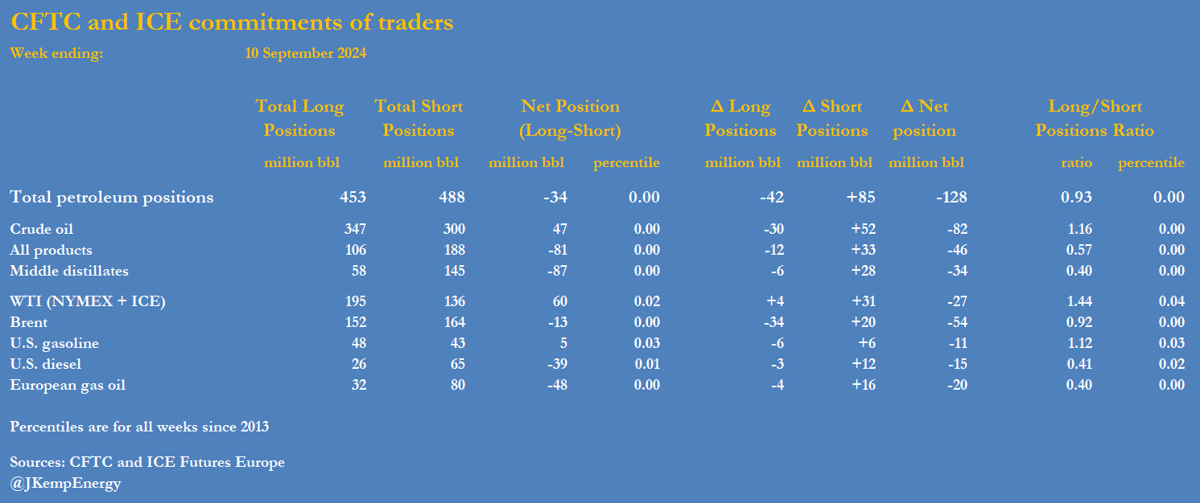

Hedge funds and other money managers sold the equivalent of 128 million barrels in the six most important futures and options contracts over the seven days ending on September 10. Fund managers have sold petroleum in eight of the most recent ten weeks, cutting their combined position by a total of 558 million barrels since the start of July.

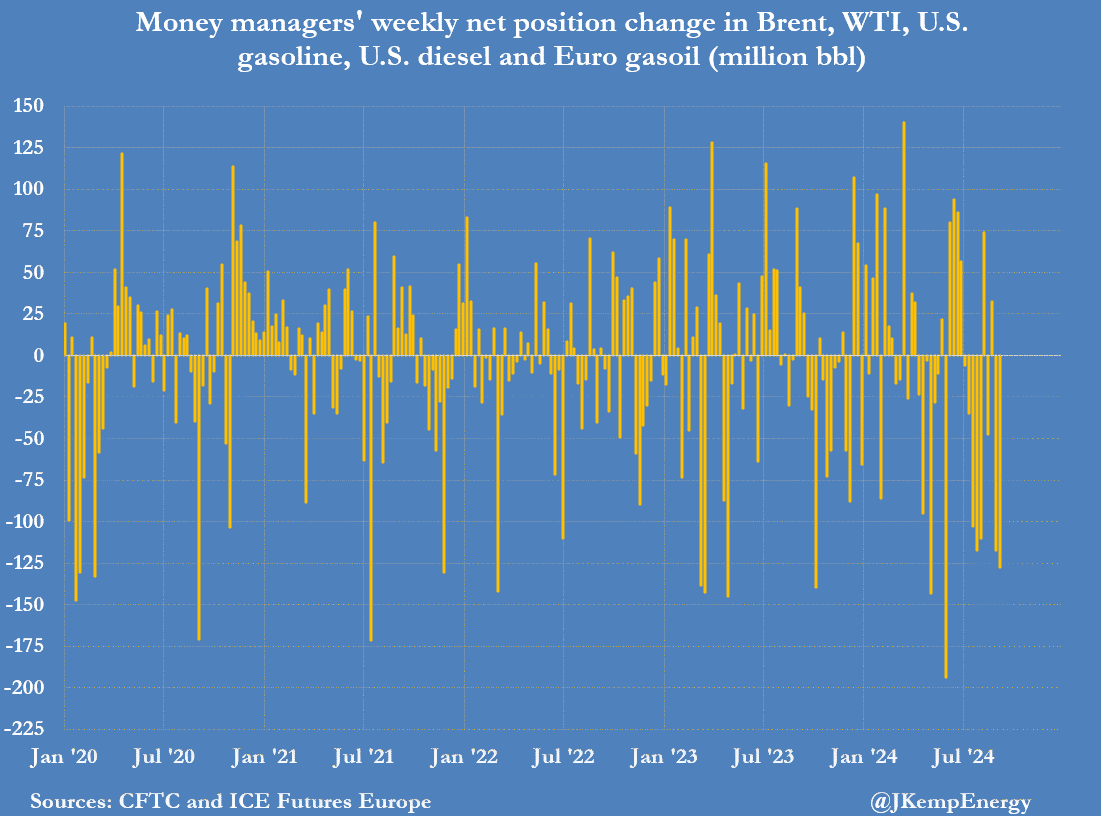

And for the first time on record, funds held a net short position of 34 million barrels down from a net long position of 524 million barrels on July 2.

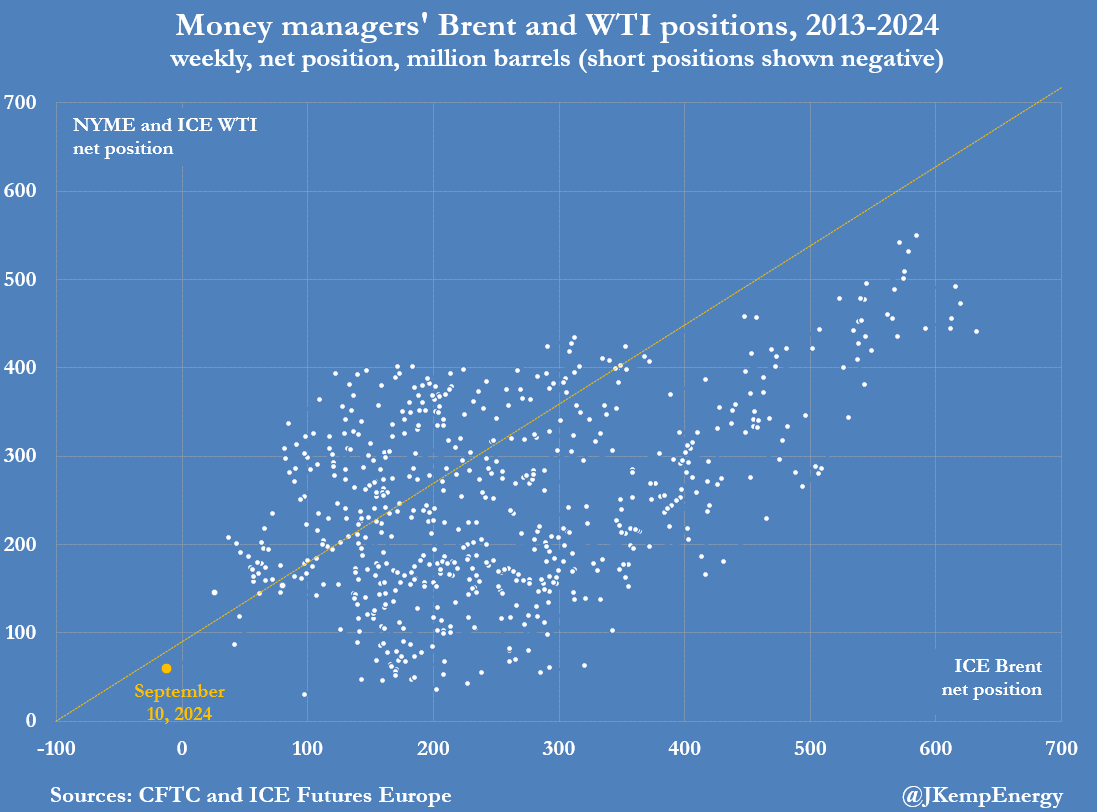

The most recent week saw heavy sales across the board, led by Brent (-54 million barrels), but including NYMEX and ICE WTI (-27 million), European gas oil (-20 million), U.S. diesel (-15 million) and U.S. gasoline (-11 million).

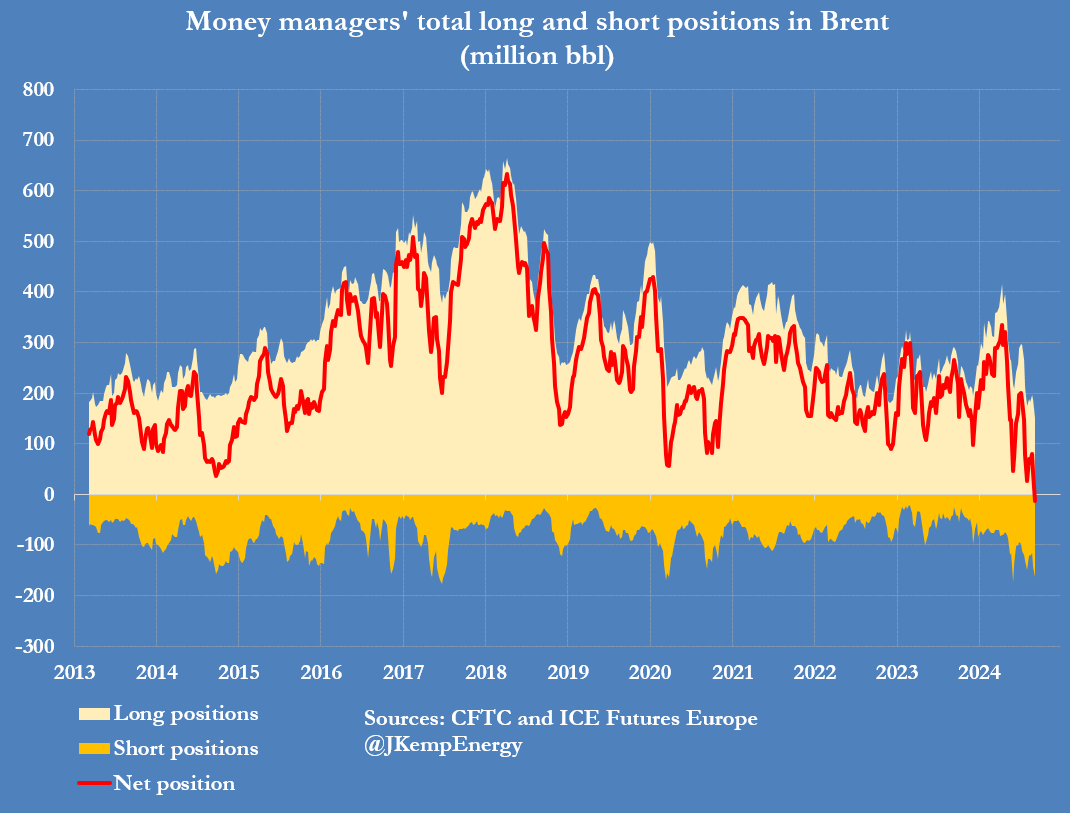

Fund managers have sold Brent in seven of the most recent nine weeks, slashing their position by a total of 213 million barrels since July 9. For the first time on record, funds held a net short position in Brent of 13 million barrels down from a net long position of 200 million nine weeks earlier.

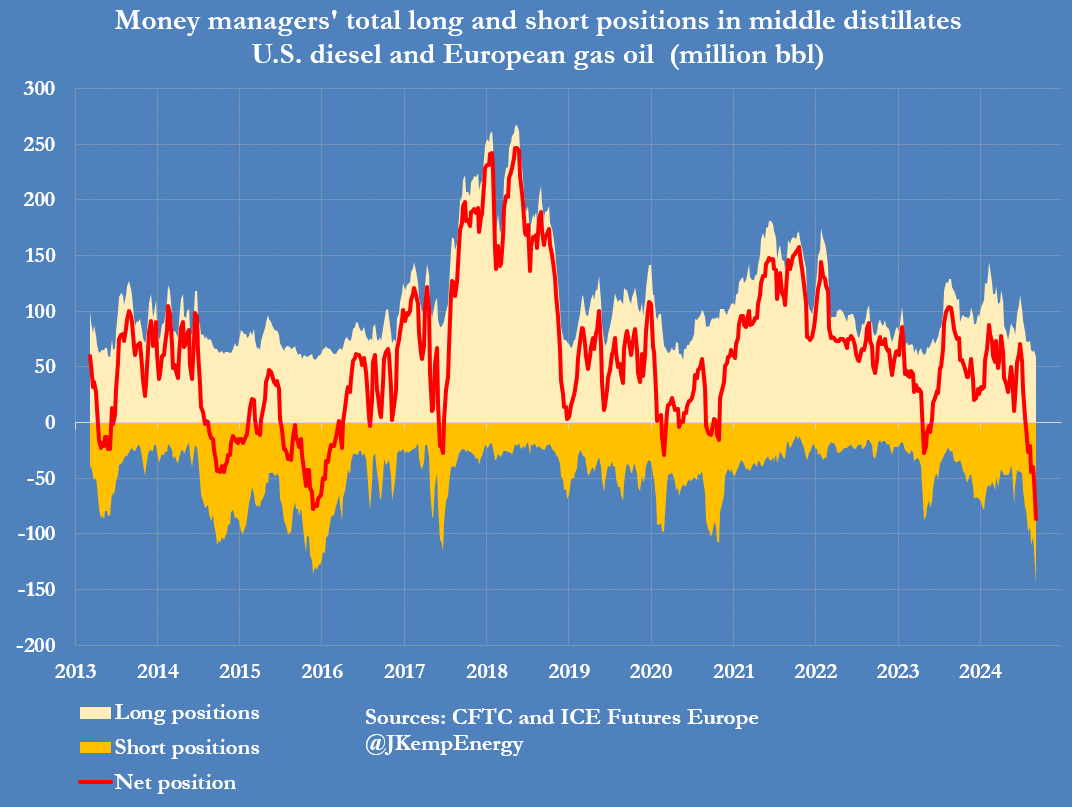

Fund managers also held a record net short position of 48 million barrels in European gas oil and a near-record net short position of 39 million barrels in U.S. diesel.

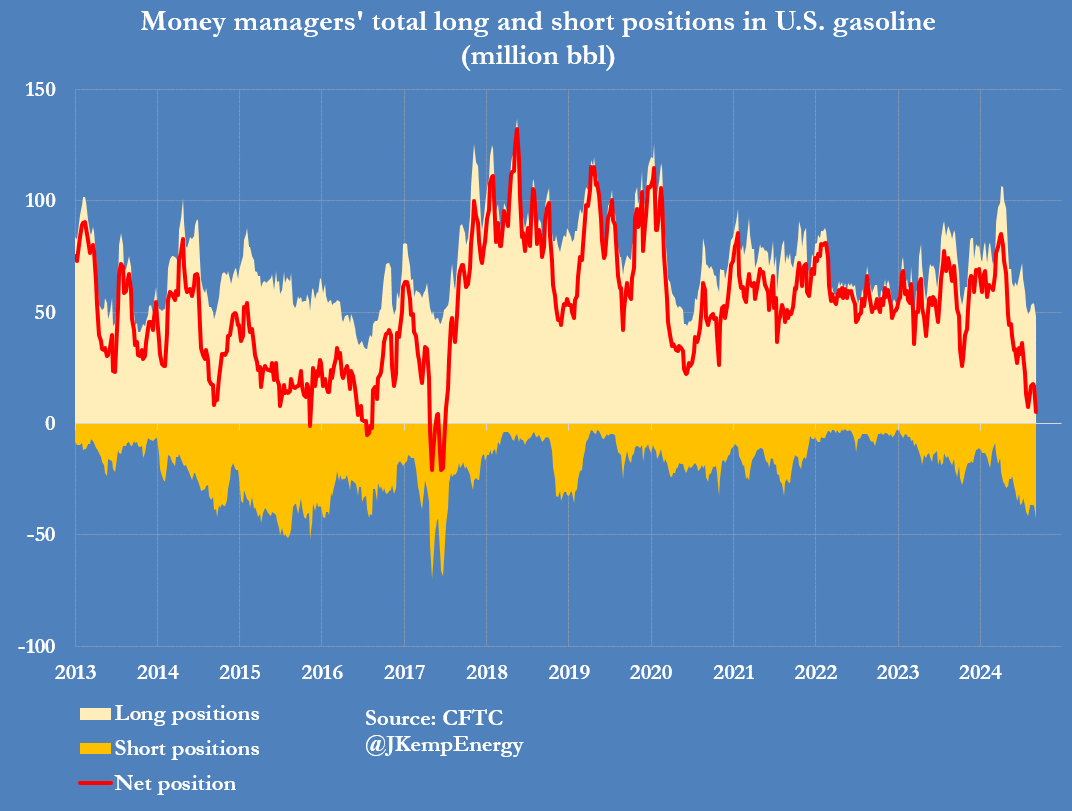

Even in WTI and gasoline, where sentiment was not quite as gloomy, positions were only a few million barrels above record lows.

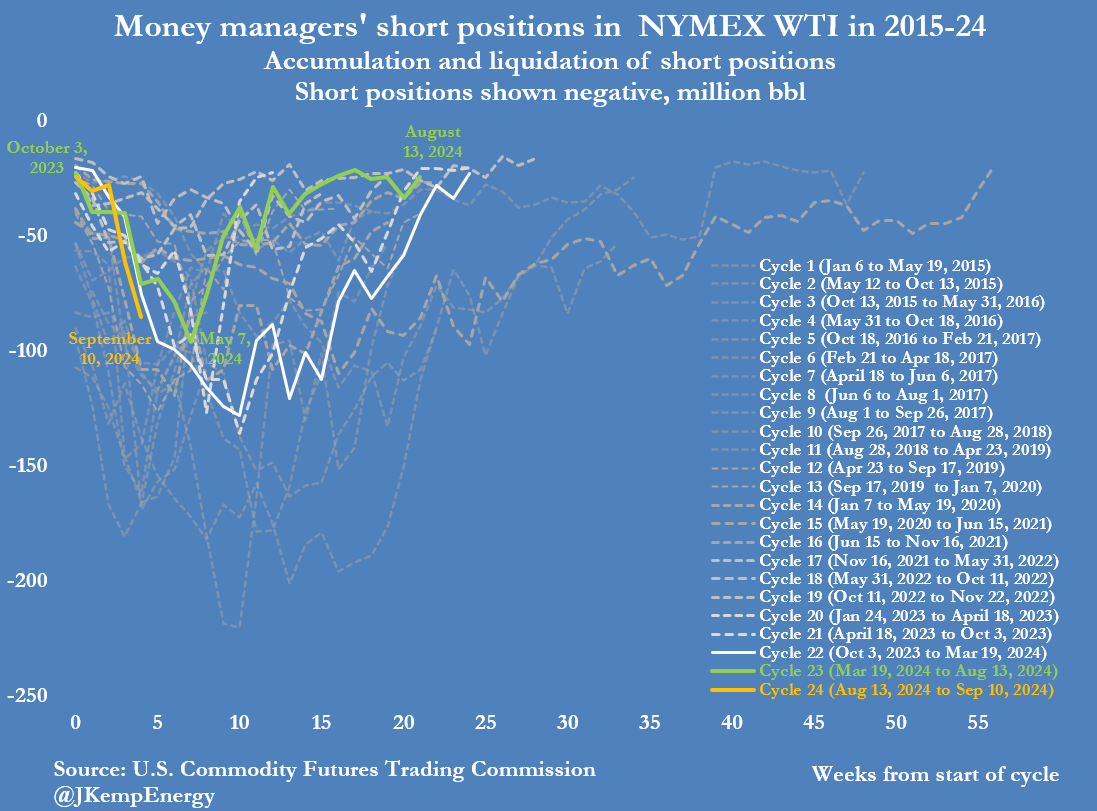

In the premier NYMEX WTI contract, fund managers have boosted short positions by a total of 61 million barrels in the last four weeks.

Bearish petroleum positions have become very crowded and the accumulation of short positions is creating conditions for a sharp jump in prices if and when the news flow becomes less negative.

For now, however, investors are focused on the limited options available to OPEC⁺ to counter the deteriorating economic outlook.

DEPTHS OF DESPAIR

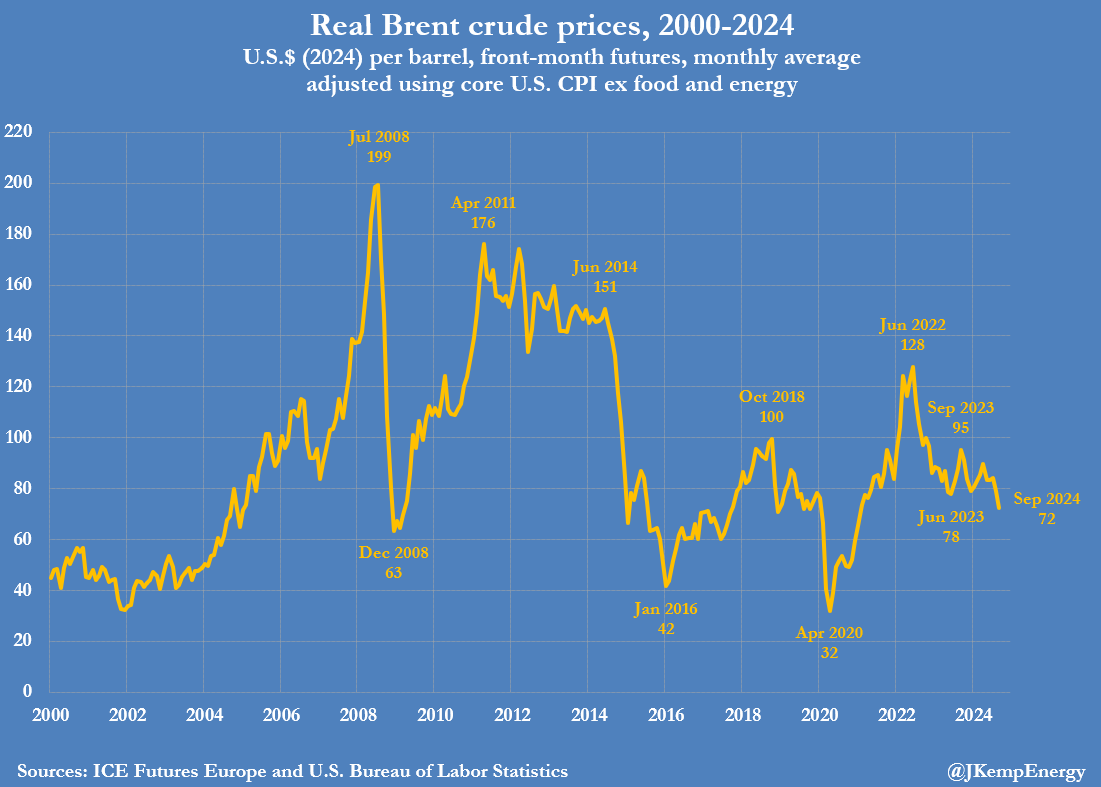

Investors are extraordinarily pessimistic even though benchmark Brent futures prices have already fallen to their lowest in real terms since early 2021.

After adjusting for inflation, crude prices have retreated to levels last seen when the major economies were still in the grip of the coronavirus pandemic and the first successful vaccines had only recently been announced.

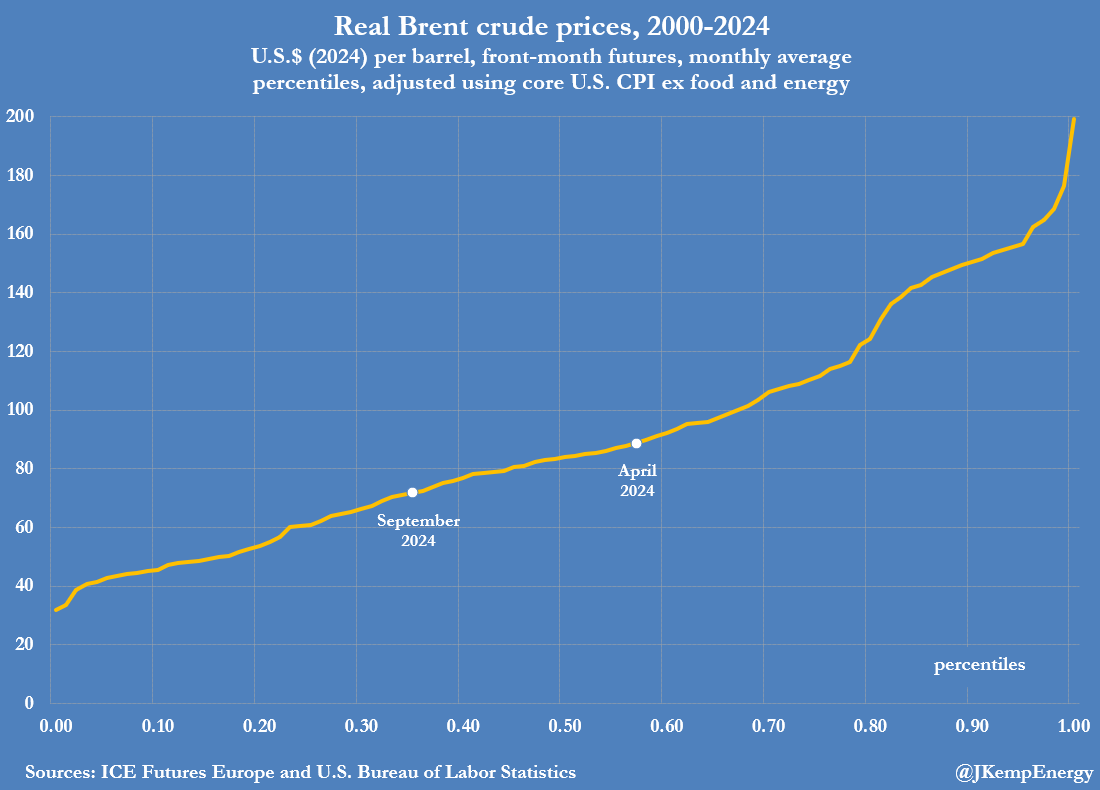

Inflation-adjusted Brent prices have averaged $72 per barrel so far in September, putting them in the 35th percentile for all months since the turn of the century, down from a recent high of $90 (57th percentile) in April.

The price slide is sending an increasingly strong signal about the need for a further deceleration in production growth to match the deteriorating macroeconomic environment and worsening outlook for consumption.

Since October 2022, Saudi Arabia and its OPEC⁺ partners have announced production cuts totalling 5.66 million barrels per day (b/d) to reduce excess inventories and drive prices higher.

Recently the group has been trying to unwind some of those cuts but has been forced to postpone planned output increases by the slowdown in consumption and renewed slump in prices.

Investors have concluded the group does not have an appetite to cut production further in the short or medium term.

The burden of adjustment must therefore fall on rival producers in the United States, Brazil, Canada and Guyana, which have accounted for nearly all output growth in recent years

Prices will decline until they enforce a further slowdown in drilling and production growth by U.S. shale producers, the most price-sensitive suppliers in the short term.

U.S. NATURAL GAS

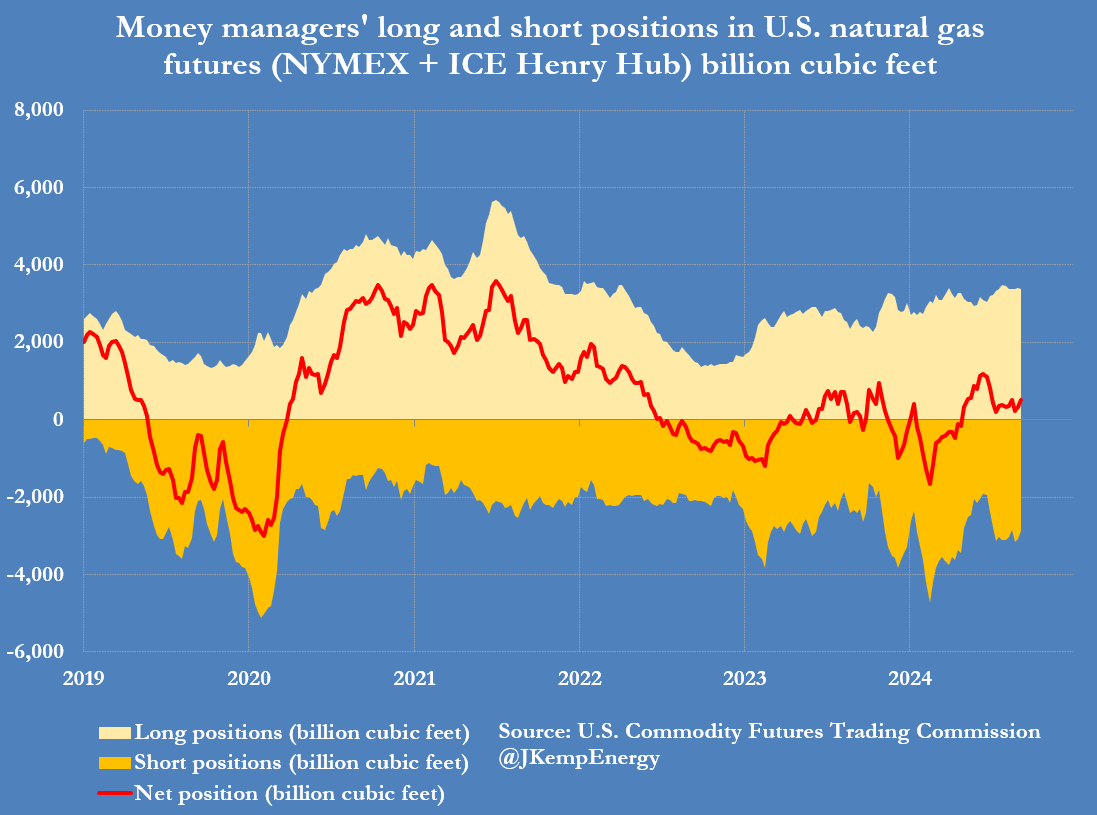

Investors are cautiously building a bullish position in U.S. natural gas as ultra-low prices and record consumption by gas-fired generators whittle away excess inventories inherited from the exceptionally mild winter of 2023/24.

Hedge funds purchased the equivalent of 192 billion cubic feet (bcf) in the two major futures and options contracts tied to prices at Henry Hub in Louisiana over the seven days ending on September 10.

Funds have purchased a total of 290 bcf over the last two weeks taking their net long position to 507 bcf (45th percentile for all weeks since 2010) though the position is still far below the recent high of 1,170 bcf (60th percentile) in mid-June.

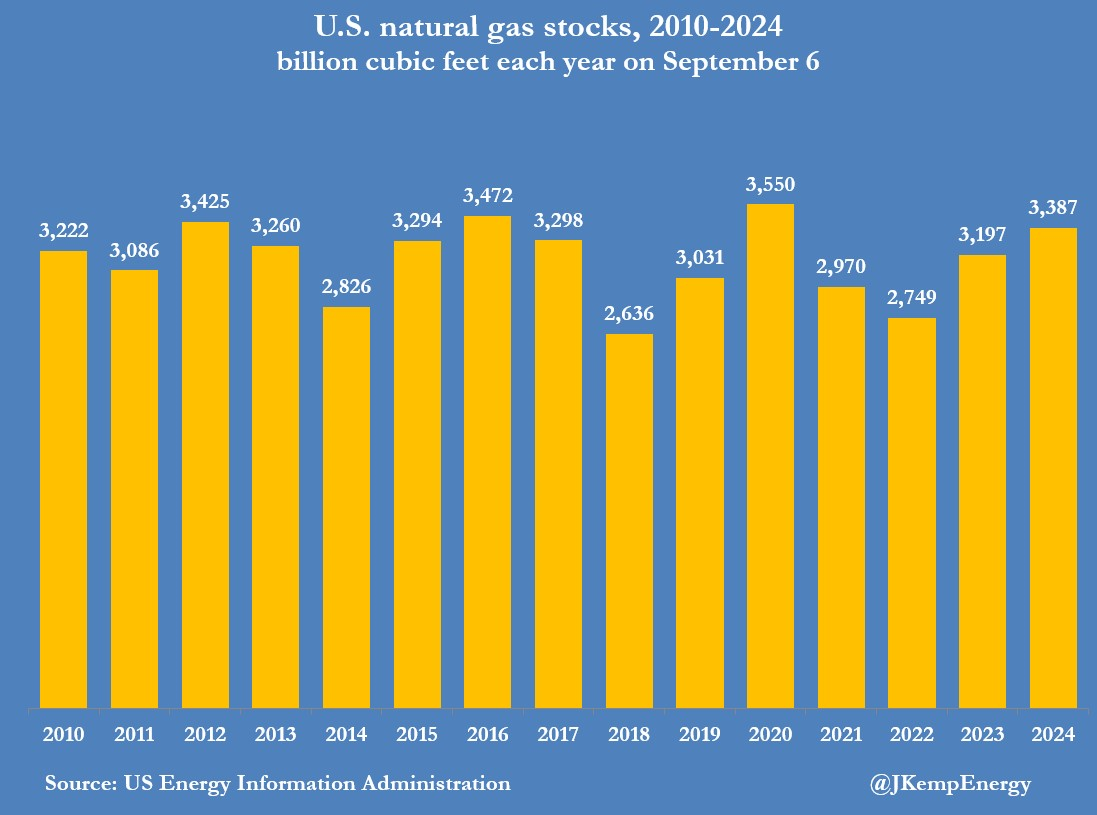

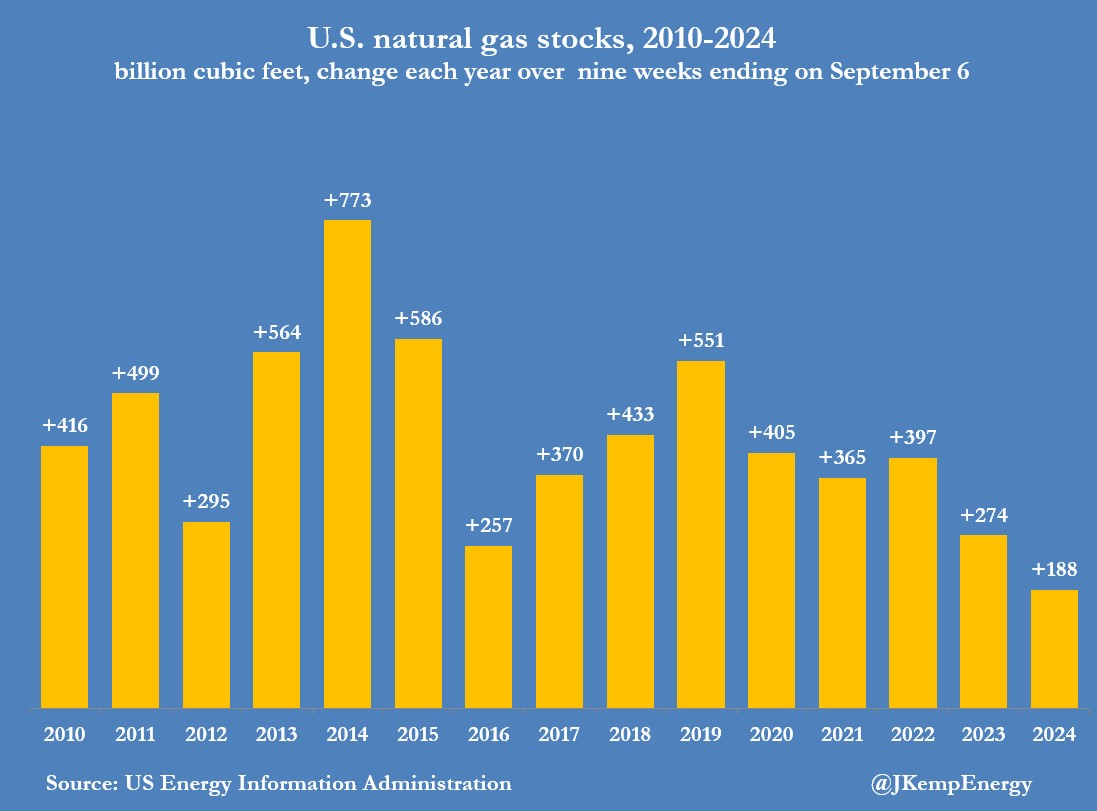

Inventories have been normalising rapidly as ultra-low prices have encouraged maximum consumption by power generators in the last stages of the summer airconditioning season.

Working inventories increased by a total of just 188 bcf over the nine weeks ending on September 6, the smallest seasonal accumulation for more than a decade, and less than half the average of 441 bcf in the past ten years.

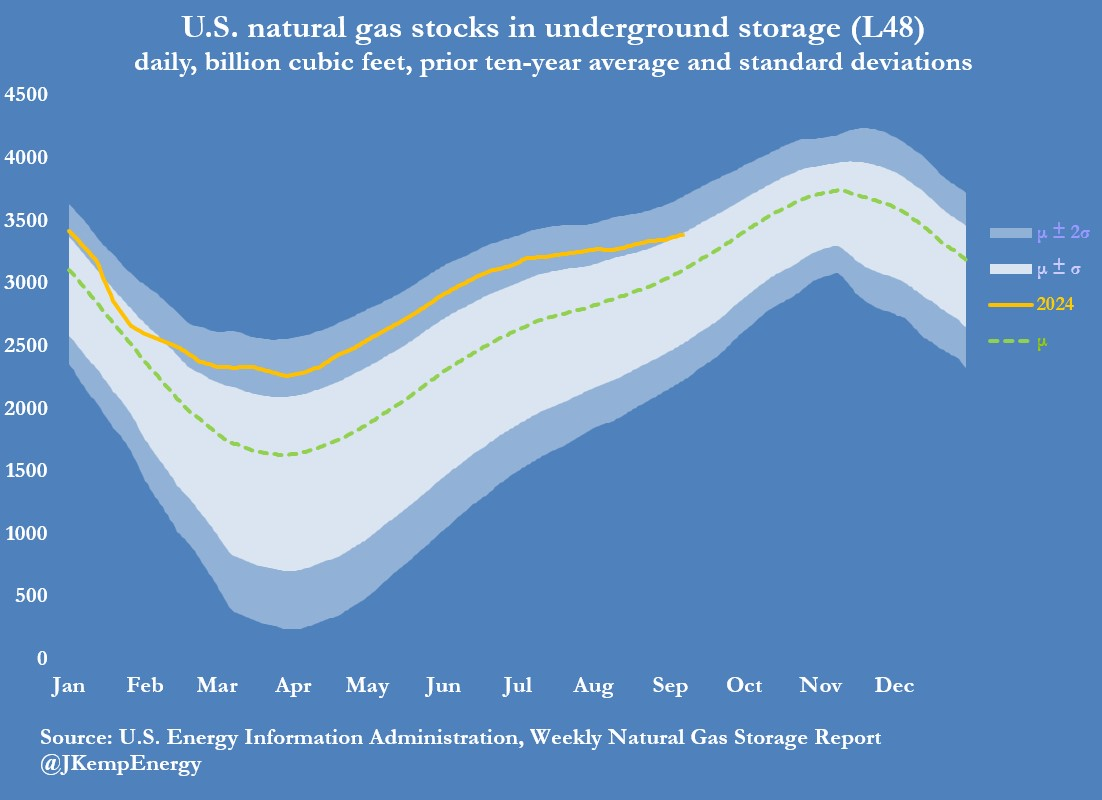

As a result, in early September stocks were still high but back within the normal range of ± 1 standard deviations away from the average for the first time since early February.

With the main airconditioning season almost over, inventories will soon start rising faster, and are likely still to be above average when the main winter heating season starts on November 1.

But the surplus will be much smaller than a few months ago, and prices have begun to climb, reflecting the more balanced outlook for winter 2024/25.

Hedge funds and other asset managers have never been more pessimistic about the outlook for petroleum prices, as signs multiply that the major industrial economies are losing momentum according to energy analyst John Kemp. Investors have also concluded Saudi Arabia and its OPEC+ allies have run out of options and either cannot or will not restrict their own production further to offset the slowdown in consumption growth and slide in prices.

Hedge funds and other money managers sold the equivalent of 128 million barrels in the six most important futures and options contracts over the seven days ending on September 10. Fund managers have sold petroleum in eight of the most recent ten weeks, cutting their combined position by a total of 558 million barrels since the start of July.

And for the first time on record, funds held a net short position of 34 million barrels down from a net long position of 524 million barrels on July 2.

The most recent week saw heavy sales across the board, led by Brent (-54 million barrels), but including NYMEX and ICE WTI (-27 million), European gas oil (-20 million), U.S. diesel (-15 million) and U.S. gasoline (-11 million).

Fund managers have sold Brent in seven of the most recent nine weeks, slashing their position by a total of 213 million barrels since July 9. For the first time on record, funds held a net short position in Brent of 13 million barrels down from a net long position of 200 million nine weeks earlier.

Fund managers also held a record net short position of 48 million barrels in European gas oil and a near-record net short position of 39 million barrels in U.S. diesel.

Even in WTI and gasoline, where sentiment was not quite as gloomy, positions were only a few million barrels above record lows.

In the premier NYMEX WTI contract, fund managers have boosted short positions by a total of 61 million barrels in the last four weeks.

Bearish petroleum positions have become very crowded and the accumulation of short positions is creating conditions for a sharp jump in prices if and when the news flow becomes less negative.

For now, however, investors are focused on the limited options available to OPEC⁺ to counter the deteriorating economic outlook.

DEPTHS OF DESPAIR

Investors are extraordinarily pessimistic even though benchmark Brent futures prices have already fallen to their lowest in real terms since early 2021.

After adjusting for inflation, crude prices have retreated to levels last seen when the major economies were still in the grip of the coronavirus pandemic and the first successful vaccines had only recently been announced.

Inflation-adjusted Brent prices have averaged $72 per barrel so far in September, putting them in the 35th percentile for all months since the turn of the century, down from a recent high of $90 (57th percentile) in April.

The price slide is sending an increasingly strong signal about the need for a further deceleration in production growth to match the deteriorating macroeconomic environment and worsening outlook for consumption.

Since October 2022, Saudi Arabia and its OPEC⁺ partners have announced production cuts totalling 5.66 million barrels per day (b/d) to reduce excess inventories and drive prices higher.

Recently the group has been trying to unwind some of those cuts but has been forced to postpone planned output increases by the slowdown in consumption and renewed slump in prices.

Investors have concluded the group does not have an appetite to cut production further in the short or medium term.

The burden of adjustment must therefore fall on rival producers in the United States, Brazil, Canada and Guyana, which have accounted for nearly all output growth in recent years

Prices will decline until they enforce a further slowdown in drilling and production growth by U.S. shale producers, the most price-sensitive suppliers in the short term.

U.S. NATURAL GAS

Investors are cautiously building a bullish position in U.S. natural gas as ultra-low prices and record consumption by gas-fired generators whittle away excess inventories inherited from the exceptionally mild winter of 2023/24.

Hedge funds purchased the equivalent of 192 billion cubic feet (bcf) in the two major futures and options contracts tied to prices at Henry Hub in Louisiana over the seven days ending on September 10.

Funds have purchased a total of 290 bcf over the last two weeks taking their net long position to 507 bcf (45th percentile for all weeks since 2010) though the position is still far below the recent high of 1,170 bcf (60th percentile) in mid-June.

Inventories have been normalising rapidly as ultra-low prices have encouraged maximum consumption by power generators in the last stages of the summer airconditioning season.

Working inventories increased by a total of just 188 bcf over the nine weeks ending on September 6, the smallest seasonal accumulation for more than a decade, and less than half the average of 441 bcf in the past ten years.

As a result, in early September stocks were still high but back within the normal range of ± 1 standard deviations away from the average for the first time since early February.

With the main airconditioning season almost over, inventories will soon start rising faster, and are likely still to be above average when the main winter heating season starts on November 1.

But the surplus will be much smaller than a few months ago, and prices have begun to climb, reflecting the more balanced outlook for winter 2024/25.

Loading…