By Irina Slav of Oilprice

Traders are not buying the oil deficit story.

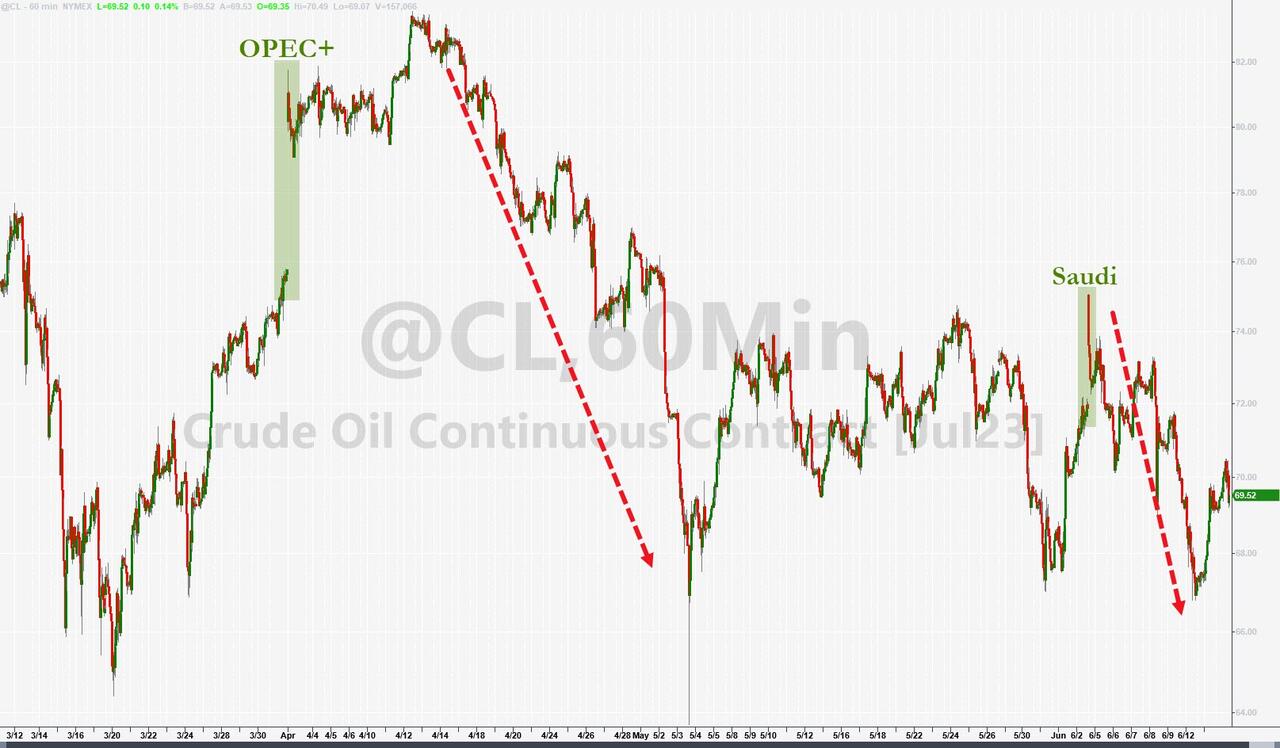

That’s the conclusion that forces itself based on the latest oil and fuel buying and selling developments ahead of the latest OPEC+ meeting.

The price movements that followed that meeting were proof that this attitude was correct.

The initial price jump that every production cut announcement from OPEC+ causes fizzled out less than a day after the announcement.

Over the past six weeks, institutional traders have reduced their positions in crude oil and fuels by 238 million barrels, Reuters’ John Kemp reported earlier this week, which was one of the lowest weekly positions in those contracts since 2013.

These six weeks were marked by some strongly bearish developments reinforcing the sentiment, such as weaker than expected Chinese economic index readings and the U.S. debt ceiling negotiations.

It appears that traders have focused entirely on those economic index readings instead of the fact that Chinese crude oil demand hit a record in April despite refineries shutting down for seasonal maintenance.

They also did not really acknowledge U.S. legislators’ success in passing the debt ceiling bill that averted a federal debt default, even though the uncertainty surrounding the issue was a major driver for bullish behavior on the oil market.

Perhaps this has something to do with news about a recession in the U.S. manufacturing and freight transport sectors, which has hurt oil consumption in these industries. It seems that institutional oil traders have been focusing almost exclusively on consumption lately.

If analysts, who almost invariably predict much higher oil prices for the second half of the year, are right, this could boomerang. But if traders’ fears of a recession materialize, oil prices will be going nowhere near $100. In fact, prices might even fall further.

This would be good news for the White House: it has set a range of $67 to $72 per barrel to refill the strategic petroleum reserve.

The twist is that the moment the Department of Energy starts buying oil for the SPR, prices will jump.

It will not be good news for OPEC, however. The cartel cannot keep cutting deeper and deeper – at some point, this will start playing to the advantage of U.S. shale. In fact, according to some, it already is, with analysts predicting higher U.S. exports as Saudi Arabia trims production by another 1 million bpd.

Meanwhile, Germany has officially fallen into recession, which has likely reinforced expectations of a faster slowdown elsewhere as well, which has dampened appetite for oil, inelastic or not. And since the non-news of the German recession broke after months of upbeat messaging that the worst was over and the EU’s largest economy was in fact, recovering, hedge funds and other institutional traders have every reason to play it safe.

The U.S. is not out of the woods yet, either.

Per Reuters’ Kemp, “Only the residual strength of service sector spending has so far prevented the “industrial recession” becoming a whole-economy recession.”

That wouldn’t be a good sign for oil demand in the world’s largest consumer, and oil traders appear to be acting in anticipation of that recession.

Importantly, they are acting in this way regardless of OPEC+ actions aimed at curbing supply in a way that should return the market to balance.

By Irina Slav of Oilprice

Traders are not buying the oil deficit story.

That’s the conclusion that forces itself based on the latest oil and fuel buying and selling developments ahead of the latest OPEC+ meeting.

The price movements that followed that meeting were proof that this attitude was correct.

The initial price jump that every production cut announcement from OPEC+ causes fizzled out less than a day after the announcement.

Over the past six weeks, institutional traders have reduced their positions in crude oil and fuels by 238 million barrels, Reuters’ John Kemp reported earlier this week, which was one of the lowest weekly positions in those contracts since 2013.

These six weeks were marked by some strongly bearish developments reinforcing the sentiment, such as weaker than expected Chinese economic index readings and the U.S. debt ceiling negotiations.

It appears that traders have focused entirely on those economic index readings instead of the fact that Chinese crude oil demand hit a record in April despite refineries shutting down for seasonal maintenance.

They also did not really acknowledge U.S. legislators’ success in passing the debt ceiling bill that averted a federal debt default, even though the uncertainty surrounding the issue was a major driver for bullish behavior on the oil market.

Perhaps this has something to do with news about a recession in the U.S. manufacturing and freight transport sectors, which has hurt oil consumption in these industries. It seems that institutional oil traders have been focusing almost exclusively on consumption lately.

If analysts, who almost invariably predict much higher oil prices for the second half of the year, are right, this could boomerang. But if traders’ fears of a recession materialize, oil prices will be going nowhere near $100. In fact, prices might even fall further.

This would be good news for the White House: it has set a range of $67 to $72 per barrel to refill the strategic petroleum reserve.

The twist is that the moment the Department of Energy starts buying oil for the SPR, prices will jump.

It will not be good news for OPEC, however. The cartel cannot keep cutting deeper and deeper – at some point, this will start playing to the advantage of U.S. shale. In fact, according to some, it already is, with analysts predicting higher U.S. exports as Saudi Arabia trims production by another 1 million bpd.

Meanwhile, Germany has officially fallen into recession, which has likely reinforced expectations of a faster slowdown elsewhere as well, which has dampened appetite for oil, inelastic or not. And since the non-news of the German recession broke after months of upbeat messaging that the worst was over and the EU’s largest economy was in fact, recovering, hedge funds and other institutional traders have every reason to play it safe.

The U.S. is not out of the woods yet, either.

Per Reuters’ Kemp, “Only the residual strength of service sector spending has so far prevented the “industrial recession” becoming a whole-economy recession.”

That wouldn’t be a good sign for oil demand in the world’s largest consumer, and oil traders appear to be acting in anticipation of that recession.

Importantly, they are acting in this way regardless of OPEC+ actions aimed at curbing supply in a way that should return the market to balance.

Loading…