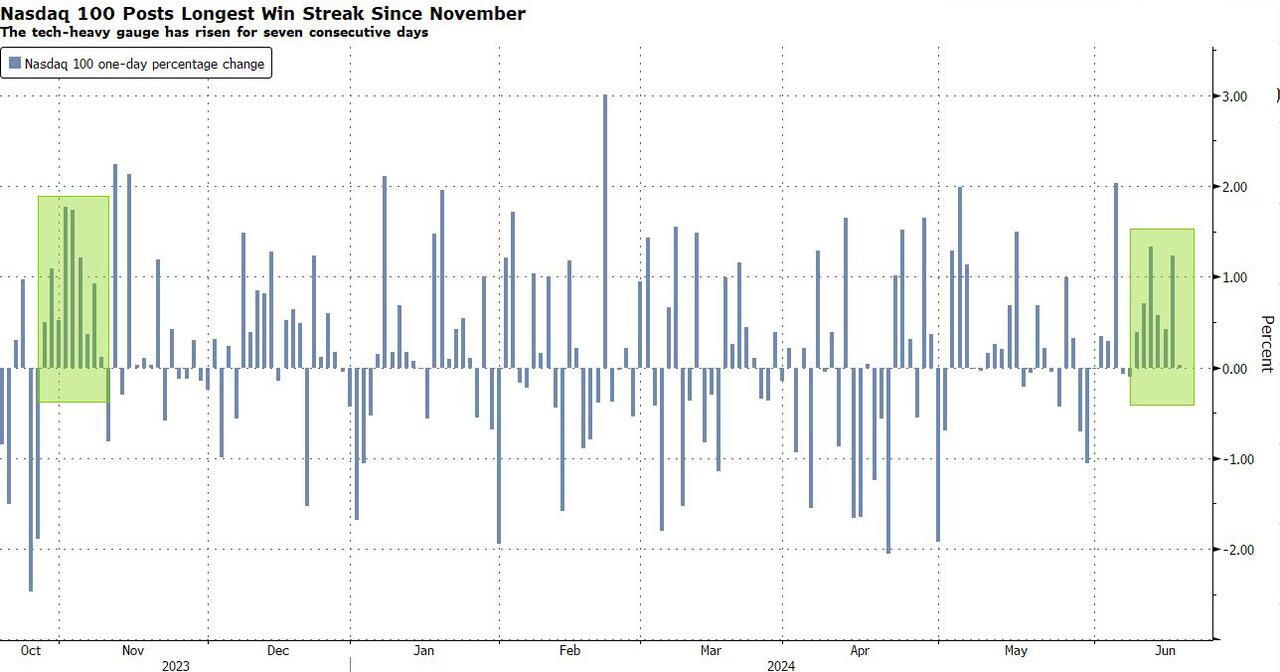

The cash market may be closed for the woke, virtue-signaling Juneteenth holiday, but that won't stop algos from gorging on the latest tech bubble, and sure enough, Nasdaq 100 futures extended their gains to an 8th consecutive day, following a strong run for technology shares that saw Nvidia become the world’s most valuable company Wednesday.

As of 8:00am, Nasdaq 100 futures rose 0.2% after a seven-day winning streak for the underlying gauge. Contracts on the S&P 500 were steady, while Dow Jones futures, not that anyone even looks at them any more, edged lower.

Despite the big 3 US stocks - NVDA, MSFT and AAPL - fast approaching an idiotic $10 trillion valuation, the US tech rally shows no signs of waning as data suggested that investors kept piling into the tech behemoths. The sector gained fresh momentum after a slowdown in consumer inflation in May bolstered bets for a potential rate cut in November. That helped lift market value of AI poster child Nvidia to the top ranking globally on Tuesday.

“We believe that there is still strong support for the information technology sector,” said Marija Veitmane, head of equity research at State Street Global Markets. With economic growth slowing, “we find it important to focus on companies with better earnings growth and stronger margin defense – this is exactly what large-cap tech is offering,” she said.

Nvidia, which rallied 174% this year, is responsible for over one third of S&P 500’s gain in 2024, according to Goldman. Together with Microsoft, Meta and Apple, the four stocks accounted for half of the index’s 15% advance.

“It’s an uneven picture, but I’m concerned of the momentum going solely into technology,” said Joe Davis, chief economist and global head of investment strategy at Vanguard, in a Bloomberg TV interview.

Meanwhile, a chorus of Federal Reserve officials on Tuesday urged more patience on rate cuts and emphasized the need for further evidence of cooling inflation. St. Louis Fed President Alberto Musalem said it could take “quarters” for the data to support a cut.

While the US is closed today, Europe is certainly open yet the continent's stocks struggled to build on a two-day rally as traders sought fresh catalysts in the wake of the latest tech-driven gains in the US. The Stoxx 600 slipped 0.1%, though the basic resources and travel sectors gained. French stocks once again lagged their regional peers with the CAC 40 falling 0.4%. While the selloff in French assets has abated somewhat, the political risks are keeping investors and companies on edge. On Wednesday, Italian sneaker firm Golden Goose Group SpA pulled the plug on its stock market IPO, citing a “significant deterioration in market conditions.” Here are the biggest European movers:

- Games Workshop shares jump as much as 9.5% after the tabletop war-game company delivered a brief trading update, showing annual results came in ahead of expectations. Jefferies says this should boost consensus estimates.

- GEA Group rises as much as 4.2% after Jefferies upgrades to buy from hold, based on an expected rebound in order intake for the farm machinery company.

- Just Eat shares rise as much as 2.1% after the food delivery firm announced that Amazon Prime users in some European markets will be able to order takeout without a delivery fee.

- Accor climbs as much as 2.9% and is leading gainer on the Stoxx 600 travel and leisure index on Wednesday after Barclays upgrades to overweight from equal-weight, saying the stock’s underperformance against its hotel peers is unjustified.

- SMA Solar falls as much as 33% after the German solar energy equipment maker slashed its outlook for the year late on Tuesday.

- Spectris shares drop as much as 14%, the steepest drop in more than 11 years, after the UK manufacturer of electronic control and process instrumentation products said full-year adjusted operating profit is likely to be “at, or marginally below, the bottom end of the range of consensus analyst expectations.”

- Autostore drops as much as 9.7% after SEB Equities initiates coverage with a sell recommendation on the Norwegian warehouse automation group, expecting a recovery to be “slow and steady.”

- Munters fall as much 5.9%, the most since April, after Carnegie downgraded its view on the Swedish industrial climate firm to sell from hold due to stretched valuations and excessively high expectations.

- Berkeley shares fall as much as 4% after the housebuilder delivered results slightly ahead of expectations and raised its profit guidance for FY25, but analysts remain cautious on its valuation, with Liberum warning it remains “fully valued” versus its rivals.

Global stocks have broadly shrugged off political tensions in France and signs the Federal Reserve could wait until December to cut interest rates. Instead, investors are focusing on the resilient economic growth picture that should continue to support corporate earnings, especially in the technology sector. UK data on Wednesday added to signs inflation is slowing across the developed world.

“We are in a soft landing scenario, central banks have started easing policy or will start to ease soon, and we may be facing a wave of positive productivity shock thanks to technology,” said Benoit Anne, head of investment solutions at MFS Investment Management. “Put all that together and you have a very supportive environment for global equities.”

In rates, US cash treasuries although treasury futures - which are trading - slipped modestly. UK government bonds fell as traders pared bets that the Bank of England will lower interest rates in the coming months after data showed services sector inflation slowed less than forecast in May. UK 10-year yields rise 4bps to 4.08% while the pound rises 0.2% against the greenback. The data all but rules out a rate cut at the BOE’s Thursday meeting, according to Zara Nokes, global market analyst at JPMorgan Asset Management. “If this stickiness in domestic price pressures continues, alongside ongoing resilience in economic activity, an August rate cut could well be off the table too,” she said.

Elsewhere, French bonds were in the red, underperforming their German counterparts and widening the 10-year yield spread by 2 basis points to around 79bps. Despite the easing of tensions, investors kept an eye on developments in France, which got a scolding from the European Union for breaking the bloc’s deficit and debt rules. The spread between 10-year French bond yields relative to German peers is just under 80 basis points amid concerns that the upcoming snap election will result in a win for right-wing groups with high-spending policies. France is among seven countries that may face a European Union infringement procedure for their excessive deficits last year. The list is due to be announced later Wednesday.

In commodities, oil prices continued their ascent, reversing an earlier loss of 0.5% with Brent trading higher on the session at around $85.50 as CTAs are forced to cover their huge shorts. Spot gold is steady around $2,330/oz.

There is nothing on the macro calendar since the US is closed for the Juneteenth holiday.

The cash market may be closed for the woke, virtue-signaling Juneteenth holiday, but that won’t stop algos from gorging on the latest tech bubble, and sure enough, Nasdaq 100 futures extended their gains to an 8th consecutive day, following a strong run for technology shares that saw Nvidia become the world’s most valuable company Wednesday.

As of 8:00am, Nasdaq 100 futures rose 0.2% after a seven-day winning streak for the underlying gauge. Contracts on the S&P 500 were steady, while Dow Jones futures, not that anyone even looks at them any more, edged lower.

Despite the big 3 US stocks – NVDA, MSFT and AAPL – fast approaching an idiotic $10 trillion valuation, the US tech rally shows no signs of waning as data suggested that investors kept piling into the tech behemoths. The sector gained fresh momentum after a slowdown in consumer inflation in May bolstered bets for a potential rate cut in November. That helped lift market value of AI poster child Nvidia to the top ranking globally on Tuesday.

“We believe that there is still strong support for the information technology sector,” said Marija Veitmane, head of equity research at State Street Global Markets. With economic growth slowing, “we find it important to focus on companies with better earnings growth and stronger margin defense – this is exactly what large-cap tech is offering,” she said.

Nvidia, which rallied 174% this year, is responsible for over one third of S&P 500’s gain in 2024, according to Goldman. Together with Microsoft, Meta and Apple, the four stocks accounted for half of the index’s 15% advance.

“It’s an uneven picture, but I’m concerned of the momentum going solely into technology,” said Joe Davis, chief economist and global head of investment strategy at Vanguard, in a Bloomberg TV interview.

Meanwhile, a chorus of Federal Reserve officials on Tuesday urged more patience on rate cuts and emphasized the need for further evidence of cooling inflation. St. Louis Fed President Alberto Musalem said it could take “quarters” for the data to support a cut.

While the US is closed today, Europe is certainly open yet the continent’s stocks struggled to build on a two-day rally as traders sought fresh catalysts in the wake of the latest tech-driven gains in the US. The Stoxx 600 slipped 0.1%, though the basic resources and travel sectors gained. French stocks once again lagged their regional peers with the CAC 40 falling 0.4%. While the selloff in French assets has abated somewhat, the political risks are keeping investors and companies on edge. On Wednesday, Italian sneaker firm Golden Goose Group SpA pulled the plug on its stock market IPO, citing a “significant deterioration in market conditions.” Here are the biggest European movers:

- Games Workshop shares jump as much as 9.5% after the tabletop war-game company delivered a brief trading update, showing annual results came in ahead of expectations. Jefferies says this should boost consensus estimates.

- GEA Group rises as much as 4.2% after Jefferies upgrades to buy from hold, based on an expected rebound in order intake for the farm machinery company.

- Just Eat shares rise as much as 2.1% after the food delivery firm announced that Amazon Prime users in some European markets will be able to order takeout without a delivery fee.

- Accor climbs as much as 2.9% and is leading gainer on the Stoxx 600 travel and leisure index on Wednesday after Barclays upgrades to overweight from equal-weight, saying the stock’s underperformance against its hotel peers is unjustified.

- SMA Solar falls as much as 33% after the German solar energy equipment maker slashed its outlook for the year late on Tuesday.

- Spectris shares drop as much as 14%, the steepest drop in more than 11 years, after the UK manufacturer of electronic control and process instrumentation products said full-year adjusted operating profit is likely to be “at, or marginally below, the bottom end of the range of consensus analyst expectations.”

- Autostore drops as much as 9.7% after SEB Equities initiates coverage with a sell recommendation on the Norwegian warehouse automation group, expecting a recovery to be “slow and steady.”

- Munters fall as much 5.9%, the most since April, after Carnegie downgraded its view on the Swedish industrial climate firm to sell from hold due to stretched valuations and excessively high expectations.

- Berkeley shares fall as much as 4% after the housebuilder delivered results slightly ahead of expectations and raised its profit guidance for FY25, but analysts remain cautious on its valuation, with Liberum warning it remains “fully valued” versus its rivals.

Global stocks have broadly shrugged off political tensions in France and signs the Federal Reserve could wait until December to cut interest rates. Instead, investors are focusing on the resilient economic growth picture that should continue to support corporate earnings, especially in the technology sector. UK data on Wednesday added to signs inflation is slowing across the developed world.

“We are in a soft landing scenario, central banks have started easing policy or will start to ease soon, and we may be facing a wave of positive productivity shock thanks to technology,” said Benoit Anne, head of investment solutions at MFS Investment Management. “Put all that together and you have a very supportive environment for global equities.”

In rates, US cash treasuries although treasury futures – which are trading – slipped modestly. UK government bonds fell as traders pared bets that the Bank of England will lower interest rates in the coming months after data showed services sector inflation slowed less than forecast in May. UK 10-year yields rise 4bps to 4.08% while the pound rises 0.2% against the greenback. The data all but rules out a rate cut at the BOE’s Thursday meeting, according to Zara Nokes, global market analyst at JPMorgan Asset Management. “If this stickiness in domestic price pressures continues, alongside ongoing resilience in economic activity, an August rate cut could well be off the table too,” she said.

Elsewhere, French bonds were in the red, underperforming their German counterparts and widening the 10-year yield spread by 2 basis points to around 79bps. Despite the easing of tensions, investors kept an eye on developments in France, which got a scolding from the European Union for breaking the bloc’s deficit and debt rules. The spread between 10-year French bond yields relative to German peers is just under 80 basis points amid concerns that the upcoming snap election will result in a win for right-wing groups with high-spending policies. France is among seven countries that may face a European Union infringement procedure for their excessive deficits last year. The list is due to be announced later Wednesday.

In commodities, oil prices continued their ascent, reversing an earlier loss of 0.5% with Brent trading higher on the session at around $85.50 as CTAs are forced to cover their huge shorts. Spot gold is steady around $2,330/oz.

There is nothing on the macro calendar since the US is closed for the Juneteenth holiday.

Loading…