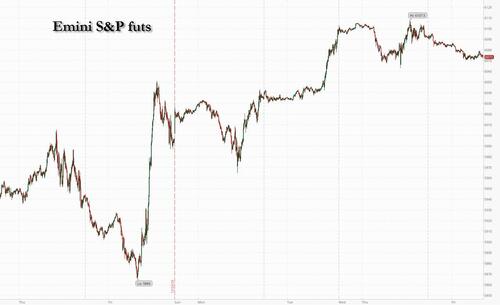

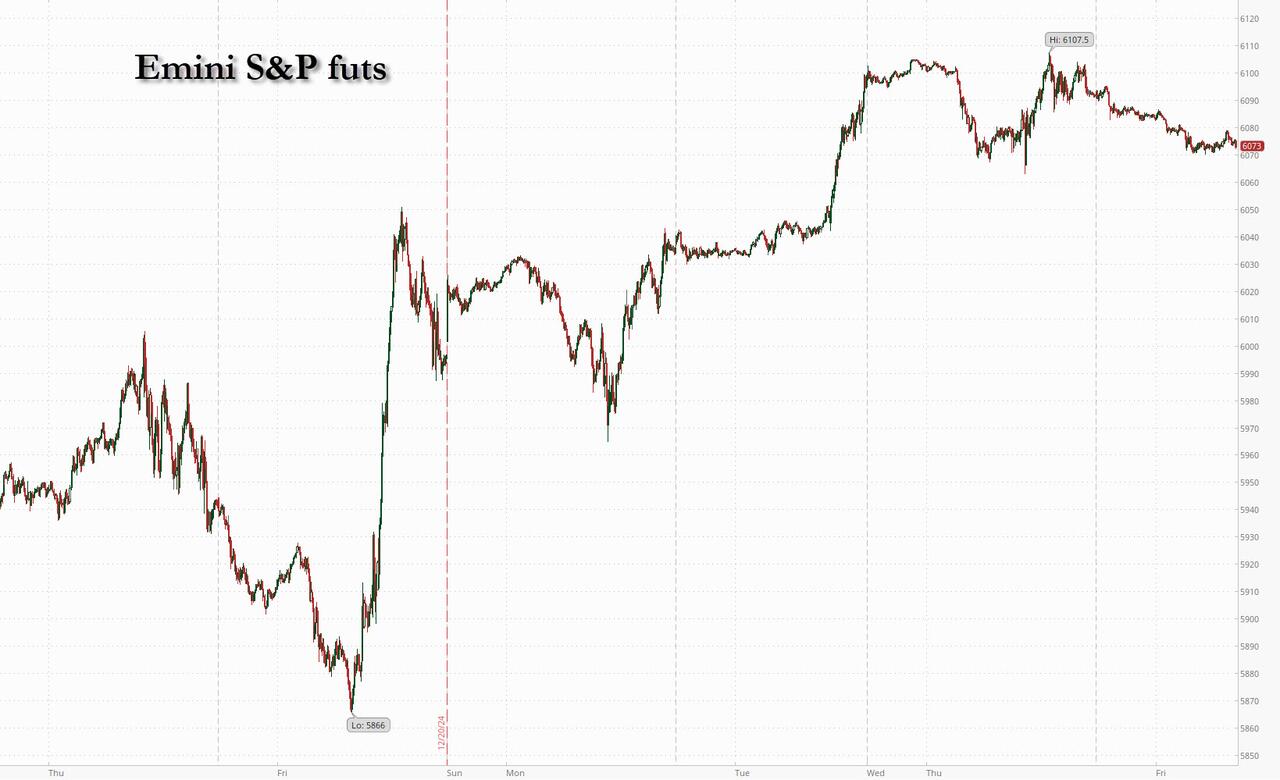

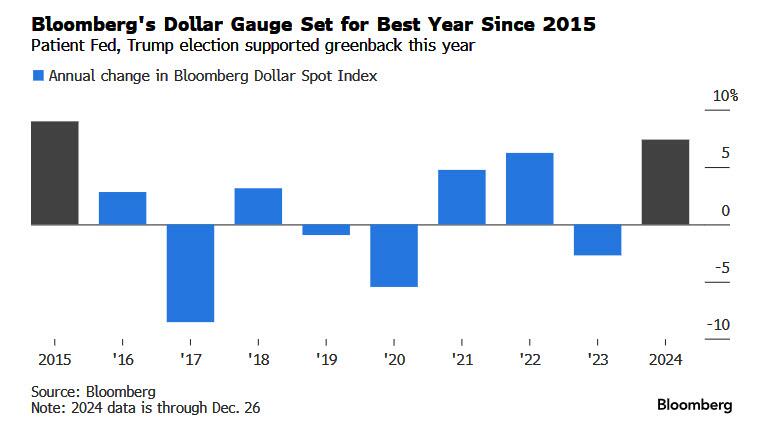

US equity futures declined after Thursday’s muted session on Wall Street, while markets in Europe and Asia advanced in muted holiday trading as the year draws to a close. As of 8:00am, S&P futures were down 0.3%, after ending Thursday flat, while the tech-heavy Nasdaq 100 fell 0.2% in quiet post-holiday session as mixed jobless claims data did little to change bets on the Fed’s policy outlook. The 10-year Treasury yield hovered near a seven-month high around 4.60%, and the dollar was steady, on track for its best year since 2015. Oil reversed Thursday's losses and was set to gain. The macro calendar is quiet: we get the advance goods trade balance, as well as wholesale and retail inventories.

In premarket trading, Arena Group climbed 18% after the company said it was notified by NYSE American that its plan to regain compliance with continued listing standards had been accepted. SES AI soared 64% and is set to extend gains for a fifth session after shares of the EV battery maker climbed as much as 168% on Thursday.

With the economy remaining resilient, investors are concerned President-elect Donald Trump’s policies, which could include tariffs and tax cuts, will stoke price rises, forcing a more hawkish stance from the central bank.

"The most important move in this year-end is the rise of the US 10-year bond; this shows how much everybody is waiting for Trump’s inauguration and its impact on inflation,” said David Kruk, head of trading at La Financiere de L’Echiquier in Paris.

“Other than that, most of the trades are technical ones, short-covering and profit taking but there’s no big trend going on as is typical during this time of the year.”

Europe's Stoxx index climbed 0.5% as trading resumed after a two-day break, with volumes at about 60% of the 20-day average for the time of day, and were poised for modest weekly gains. Novo Nordisk shares extended their rebound into a second session. Delivery Hero shares drop as much as 9% after Taiwan blocked the sale of its subsidiary there to Uber Technologies.

Earlier in the session, the MSCI Asia Pacific index climbed for the fifth straight day, its longest such streak since July. Shares in Tokyo jumped after the yen dropped to a five-month low of 158 per dollar in the previous session, following Bank of Japan Governor Kazuo Ueda’s comments Wednesday that avoided giving a clear signal on interest rates next month. Elsewhere in Asia, Hong Kong and mainland Chinese shares fluctuated. Equities rose in Australia, with their South Korean counterparts declining as the country’s political turmoil continued.

In FX, the Bloomberg dollar index was steady, on pace for its best year since 2015.

The yen rebounded slightly Friday, after Finance Minister Katsunobu Kato said the government will take appropriate steps against excessive movements in the foreign exchange market. Data released Friday also showed inflation in Tokyo accelerated for a second month, with retail sales also beating estimates. Bank of Japan board members held mixed views when they discussed the timing of an interest-rate hike at last week’s meeting, according to minutes released on Friday. A summary of opinions from the central bank’s December meeting showed mixed views among its board members on the timing of another rate hike partly due to uncertainties over the US economy. USD/JPY traded 0.2% lower at 157.75, having fallen as low as 157.51 in Asian trade; the pound drifted higher against the dollar while the euro held its ground at $1.0421.

In rates, treasuries are under pressure as US trading gets under way, trailing steeper declines for European bond markets, many of which are reopening after a two-day holiday. US yields remain inside ranges from Thursday, the 10-year Treasury yield rising 3bps to 4.61%, near the May high of 4.64% hit on Thursday. Traders are betting that the Fed will deliver less than two rate cuts by end-2025. 5- to 30-year yields have risen more than 15bp since Dec. 17, the day before the Fed, while cutting interest rates for the third straight time, signaled a slower pace for future moves. Bloomberg Treasury Index lost 1.7% this month through Thursday, paring its YTD gain to less than 0.5%; index may benefit next week from month-end rebalancing that will extend its duration by an estimated 0.07 year

In commodity markets, iron ore sank to the lowest in more than five weeks, falling below $100 a ton, as poor industrial profits in China highlighted the nation’s economic weakness. Oil gained while gold was steady.

Bitcoin edged higher after the cryptocurrency’s rally showed signs of fizzling Thursday.

The US economic data calendar includes November advance goods trade balance and November preliminary wholesale inventories at 8:30am. Fed speaker slate is blank until Jan. 3.

Market Snapshot

- S&P 500 futures down 0.4% to 6,073.75

- STOXX Europe 600 up 0.3% to 505.34

- MXAP up 0.4% to 182.70

- MXAPJ down 0.2% to 573.66

- Nikkei up 1.8% to 40,281.16

- Topix up 1.3% to 2,801.68

- Hang Seng Index little changed at 20,090.46

- Shanghai Composite little changed at 3,400.14

- Sensex up 0.3% to 78,727.26

- Australia S&P/ASX 200 up 0.5% to 8,261.80

- Kospi down 1.0% to 2,404.77

- German 10Y yield up 6 bps at 2.39%

- Euro little changed at $1.0412

- Brent Futures up 0.2% to $73.42/bbl

- Gold spot down 0.3% to $2,625.09

- US Dollar Index little changed at 108.17

Top Overnight News

- The Bank of Japan signaled that a rate hike next month still remains on the table even as cautious views among the majority swayed the stand-pat decision at a policy meeting last week.

- German President Frank-Walter Steinmeier dissolved parliament and set the country’s snap election for Feb. 23, formally endorsing a timetable proposed by Chancellor Olaf Scholz after he pulled the plug on his ruling coalition last month.

- A Bitcoin rally is fizzling in the final days of a record-breaking year for the digital asset, as investors assess the remaining impetus from President-elect Donald Trump’s embrace of the cryptocurrency sector.

US equity futures declined after Thursday’s muted session on Wall Street, while markets in Europe and Asia advanced in muted holiday trading as the year draws to a close. As of 8:00am, S&P futures were down 0.3%, after ending Thursday flat, while the tech-heavy Nasdaq 100 fell 0.2% in quiet post-holiday session as mixed jobless claims data did little to change bets on the Fed’s policy outlook. The 10-year Treasury yield hovered near a seven-month high around 4.60%, and the dollar was steady, on track for its best year since 2015. Oil reversed Thursday’s losses and was set to gain. The macro calendar is quiet: we get the advance goods trade balance, as well as wholesale and retail inventories.

In premarket trading, Arena Group climbed 18% after the company said it was notified by NYSE American that its plan to regain compliance with continued listing standards had been accepted. SES AI soared 64% and is set to extend gains for a fifth session after shares of the EV battery maker climbed as much as 168% on Thursday.

With the economy remaining resilient, investors are concerned President-elect Donald Trump’s policies, which could include tariffs and tax cuts, will stoke price rises, forcing a more hawkish stance from the central bank.

“The most important move in this year-end is the rise of the US 10-year bond; this shows how much everybody is waiting for Trump’s inauguration and its impact on inflation,” said David Kruk, head of trading at La Financiere de L’Echiquier in Paris.

“Other than that, most of the trades are technical ones, short-covering and profit taking but there’s no big trend going on as is typical during this time of the year.”

Europe’s Stoxx index climbed 0.5% as trading resumed after a two-day break, with volumes at about 60% of the 20-day average for the time of day, and were poised for modest weekly gains. Novo Nordisk shares extended their rebound into a second session. Delivery Hero shares drop as much as 9% after Taiwan blocked the sale of its subsidiary there to Uber Technologies.

Earlier in the session, the MSCI Asia Pacific index climbed for the fifth straight day, its longest such streak since July. Shares in Tokyo jumped after the yen dropped to a five-month low of 158 per dollar in the previous session, following Bank of Japan Governor Kazuo Ueda’s comments Wednesday that avoided giving a clear signal on interest rates next month. Elsewhere in Asia, Hong Kong and mainland Chinese shares fluctuated. Equities rose in Australia, with their South Korean counterparts declining as the country’s political turmoil continued.

In FX, the Bloomberg dollar index was steady, on pace for its best year since 2015.

The yen rebounded slightly Friday, after Finance Minister Katsunobu Kato said the government will take appropriate steps against excessive movements in the foreign exchange market. Data released Friday also showed inflation in Tokyo accelerated for a second month, with retail sales also beating estimates. Bank of Japan board members held mixed views when they discussed the timing of an interest-rate hike at last week’s meeting, according to minutes released on Friday. A summary of opinions from the central bank’s December meeting showed mixed views among its board members on the timing of another rate hike partly due to uncertainties over the US economy. USD/JPY traded 0.2% lower at 157.75, having fallen as low as 157.51 in Asian trade; the pound drifted higher against the dollar while the euro held its ground at $1.0421.

In rates, treasuries are under pressure as US trading gets under way, trailing steeper declines for European bond markets, many of which are reopening after a two-day holiday. US yields remain inside ranges from Thursday, the 10-year Treasury yield rising 3bps to 4.61%, near the May high of 4.64% hit on Thursday. Traders are betting that the Fed will deliver less than two rate cuts by end-2025. 5- to 30-year yields have risen more than 15bp since Dec. 17, the day before the Fed, while cutting interest rates for the third straight time, signaled a slower pace for future moves. Bloomberg Treasury Index lost 1.7% this month through Thursday, paring its YTD gain to less than 0.5%; index may benefit next week from month-end rebalancing that will extend its duration by an estimated 0.07 year

In commodity markets, iron ore sank to the lowest in more than five weeks, falling below $100 a ton, as poor industrial profits in China highlighted the nation’s economic weakness. Oil gained while gold was steady.

Bitcoin edged higher after the cryptocurrency’s rally showed signs of fizzling Thursday.

The US economic data calendar includes November advance goods trade balance and November preliminary wholesale inventories at 8:30am. Fed speaker slate is blank until Jan. 3.

Market Snapshot

- S&P 500 futures down 0.4% to 6,073.75

- STOXX Europe 600 up 0.3% to 505.34

- MXAP up 0.4% to 182.70

- MXAPJ down 0.2% to 573.66

- Nikkei up 1.8% to 40,281.16

- Topix up 1.3% to 2,801.68

- Hang Seng Index little changed at 20,090.46

- Shanghai Composite little changed at 3,400.14

- Sensex up 0.3% to 78,727.26

- Australia S&P/ASX 200 up 0.5% to 8,261.80

- Kospi down 1.0% to 2,404.77

- German 10Y yield up 6 bps at 2.39%

- Euro little changed at $1.0412

- Brent Futures up 0.2% to $73.42/bbl

- Gold spot down 0.3% to $2,625.09

- US Dollar Index little changed at 108.17

Top Overnight News

- The Bank of Japan signaled that a rate hike next month still remains on the table even as cautious views among the majority swayed the stand-pat decision at a policy meeting last week.

- German President Frank-Walter Steinmeier dissolved parliament and set the country’s snap election for Feb. 23, formally endorsing a timetable proposed by Chancellor Olaf Scholz after he pulled the plug on his ruling coalition last month.

- A Bitcoin rally is fizzling in the final days of a record-breaking year for the digital asset, as investors assess the remaining impetus from President-elect Donald Trump’s embrace of the cryptocurrency sector.

Loading…